- Alt-Market

- AntiWar.com

- Bitcoin Magazine

- Bombthrower

- BULLIONSTAR

- Capitalist Exploits

- Christophe Barraud

- Dollar Collapse

- Dr. Housing Bubble

- Financial Revolutionist

- ForexLive

- Forum Geopolitica

- Gains Pains & Capital

- Gefira

- GMG Research

- Gold Core

- Implode-Explode

- Insider Paper

- Libertarian Institute

- Liberty Blitzkrieg

- Max Keiser

- Mises Institute

- Mish Talk

- Monetary Metals

- Newsquawk

- Of Two Minds

- Oil Price

- Open The Books

- Peter Schiff

- Portfolio Armor

- QTR’s Fringe Finance

- Safehaven

- Slope of Hope

- SpotGamma

- TF Metals Report

- The Automatic Earth

- The Burning Platform

- The Economic Populist

- Themis Trading

- Thoughtful Money

- Value Walk

- Visual Combat Banzai7

- Wolf Street

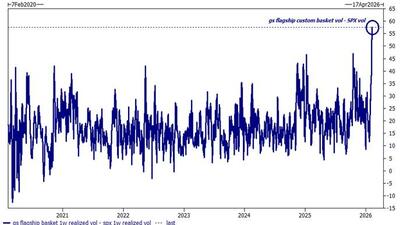

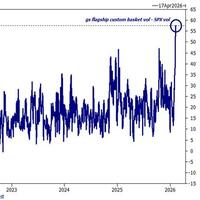

This past week's selloff exposed how much of the market's recent support was transient...

Democrats have a list of 10 'non-negotiable' reforms...

The end-game of debt-debasement is already visible. The only thing that's still up in the air is our response...

This can't be good.

In an age of rage, it is often difficult to stand out in the mob as so many pander to the perpetually irate...

Estimate your earnings

%22%2F%3E%0A%3C%2Fsvg%3E%0A)

oz

%22%2F%3E%0A%3C%2Fsvg%3E%0A)

Calculate earnings

...there is no respite to the sensory overload...

"KD was a disaster, with a miss-and-cut report, several mgmt. changes, and a delayed 10Q filing."

The question is whether the Clintons are again gaming the system after avoiding a bipartisan vote to hold them in contempt...

...our macro models suggest that equity valuations are higher than the macro backdrop would normally justify.

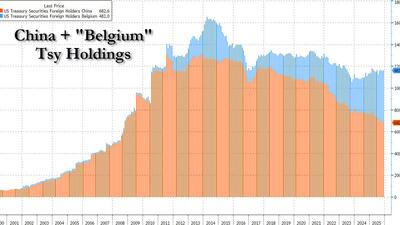

“what is left for the banks is small, and China doesn’t exactly set the Treasury market on fire at the monthly auctions.”

The pattern of freer trade for friends and restricted trade elsewhere is a template that is now being repeated globally as the world coalesces into interest blocs with geopolitical hedgerows erected in between...

"It's like watching a fatal car crash in slow motion..."

...market turmoil sparks rumors.

...and it argues for running a bit smaller until technicals rebuild – better liquidity, less crowded shorts, more balanced positioning.

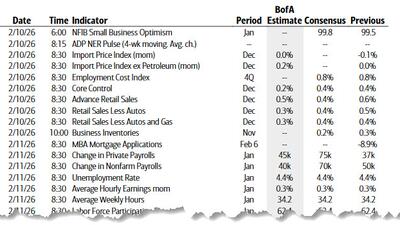

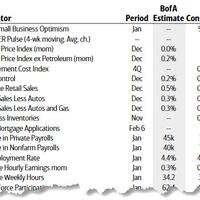

The next five days will feature an unusual pairing of major US data releases: the January employment report on Wednesday and the January CPI report on Friday, two reports which usually never appear in the same week

Navy issues photo set of A-10 Thunderbolt doing strafing runs...

"Once again, Big Pharma is weaponizing the US..."

Estimate your earnings

oz

Calculate earnings

Today's Top Stories

Assistance and Requests: Contact Us

Tips: tips@zerohedge.com

General: info@zerohedge.com

Legal: legal@zerohedge.com

Advertising: Contact Us

Abuse/Complaints: abuse@zerohedge.com

Make sure to read our "How To [Read/Tip Off] Zero Hedge Without Attracting The Interest Of [Human Resources/The Treasury/Black Helicopters]" Guide

It would be very wise of you to study our privacy policy and our (non)policy on conflicts / full disclosure.Here's our Cookie Policy.