- Alt-Market

- AntiWar.com

- Bitcoin Magazine

- Bombthrower

- BULLIONSTAR

- Capitalist Exploits

- Christophe Barraud

- Dollar Collapse

- Dr. Housing Bubble

- Financial Revolutionist

- ForexLive

- Forum Geopolitica

- Gains Pains & Capital

- Gefira

- GMG Research

- Gold Core

- Implode-Explode

- Insider Paper

- Libertarian Institute

- Liberty Blitzkrieg

- Max Keiser

- Mises Institute

- Mish Talk

- Monetary Metals

- Newsquawk

- Of Two Minds

- Oil Price

- Open The Books

- Peter Schiff

- Portfolio Armor

- QTR’s Fringe Finance

- Safehaven

- Slope of Hope

- SpotGamma

- TF Metals Report

- The Automatic Earth

- The Burning Platform

- The Economic Populist

- Themis Trading

- Thoughtful Money

- Value Walk

- Visual Combat Banzai7

- Wolf Street

Dow record high, gold green on the week, tech wrecked but S&P unch, crypto dump-and-pump...

Unchecked immigration policies have opened the floodgates for criminal networks to bleed taxpayers dry...

"We note that these pushbacks mostly originated from local communities with little exposure to data centers. In such cases, we expect proposed data centers to relocate..."

Minority Shia communities repeatedly targeted in sectarian violence...

"Bitcoin is crashing so I have to say bye to the love of my life..."

Estimate your earnings

%22%2F%3E%0A%3C%2Fsvg%3E%0A)

oz

%22%2F%3E%0A%3C%2Fsvg%3E%0A)

Calculate earnings

The latest announcement from the People's Bank of China follows months of flip-flopping on privately issued yuan-pegged stablecoins.

"We created a dollar shortage in the country. It came to a swift conclusion."

The governor aims to spend his political capital to see guardrails put on the pervasive and rapidly expanding tech before leaving office in a year.

Tlaib's campaign and leadership PAC funneled nearly $600,000 to Unbought Power...

Fresh off federal arrest for storming a Minnesota church, ex-CNN host unleashes on VP...

The same person connected to an illegal biolab shut down in Reedley, California, in 2023.

....without "interference in our internal affairs."

Just a little PSA for the folks who are clearly confused...

“Humans are not just labor units..."

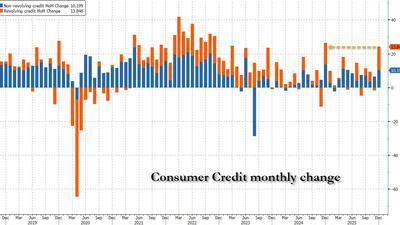

Meanwhhile, the average credit card APR has gone up in the past 2.5 years despite 1.75% in rate cuts by the Fed.

"This week’s tape can only be categorized as adult swim... and then some..."

Jackson's actions raise genuine concerns about impartiality...

Estimate your earnings

oz

Calculate earnings

Today's Top Stories

Assistance and Requests: Contact Us

Tips: tips@zerohedge.com

General: info@zerohedge.com

Legal: legal@zerohedge.com

Advertising: Contact Us

Abuse/Complaints: abuse@zerohedge.com

Make sure to read our "How To [Read/Tip Off] Zero Hedge Without Attracting The Interest Of [Human Resources/The Treasury/Black Helicopters]" Guide

It would be very wise of you to study our privacy policy and our (non)policy on conflicts / full disclosure.Here's our Cookie Policy.