- Alt-Market

- AntiWar.com

- Bitcoin Magazine

- Bombthrower

- BULLIONSTAR

- Capitalist Exploits

- Christophe Barraud

- Dollar Collapse

- Dr. Housing Bubble

- Financial Revolutionist

- ForexLive

- Forum Geopolitica

- Gains Pains & Capital

- Gefira

- GMG Research

- Gold Core

- Implode-Explode

- Insider Paper

- Libertarian Institute

- Liberty Blitzkrieg

- Max Keiser

- Mises Institute

- Mish Talk

- Monetary Metals

- Newsquawk

- Of Two Minds

- Oil Price

- Open The Books

- Peter Schiff

- Portfolio Armor

- QTR’s Fringe Finance

- Safehaven

- Slope of Hope

- SpotGamma

- TF Metals Report

- The Automatic Earth

- The Burning Platform

- The Economic Populist

- Themis Trading

- Thoughtful Money

- Value Walk

- Visual Combat Banzai7

- Wolf Street

Democrats have a list of 10 'non-negotiable' reforms...

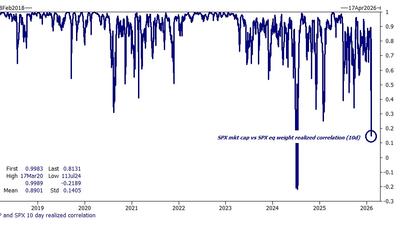

...and it argues for running a bit smaller until technicals rebuild – better liquidity, less crowded shorts, more balanced positioning.

...top Goldman trader suggests this feels like a classic “what would Warren Buffett buy” market.

"The NFL having a Super Bowl Halftime Show where their performer sings ENTIRELY in Spanish & waves other nation's flags..."

Estimate your earnings

%22%2F%3E%0A%3C%2Fsvg%3E%0A)

oz

%22%2F%3E%0A%3C%2Fsvg%3E%0A)

Calculate earnings

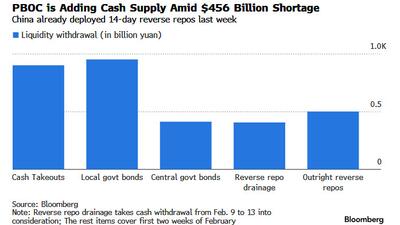

The People’s Bank of China is boosting the supply of money available to banks to ensure they can meet the surge in demand for cash during the Lunar New Year holidays.

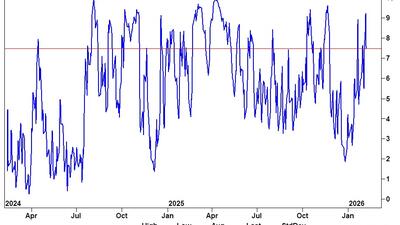

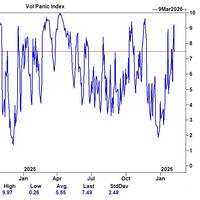

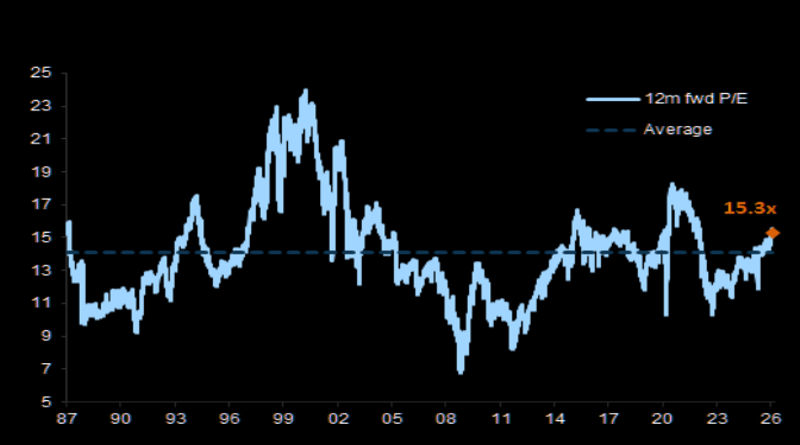

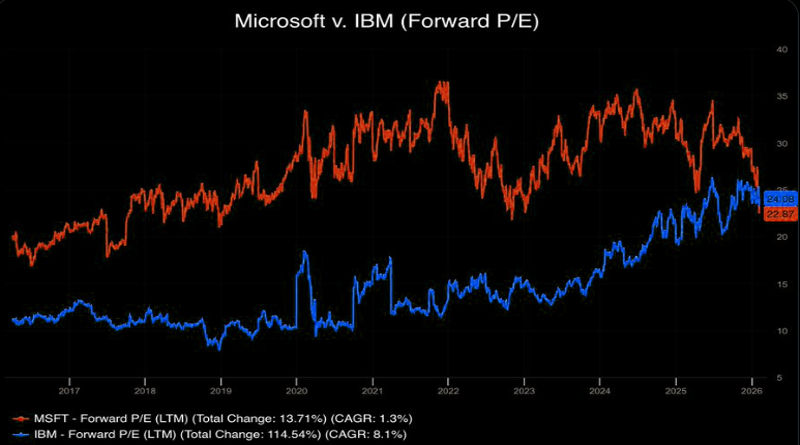

Is Tech Screamingly Cheap Now?

"That gives us confidence that we can lean into that group in a more meaningful way, whether ..."

Tactical Upswing Confirmed

Taking advantage of cheaper energy and less restrictive regulations, Chinese producers are aggressively entering the European market, from fertilizers to plastics...

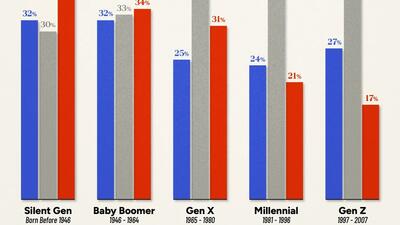

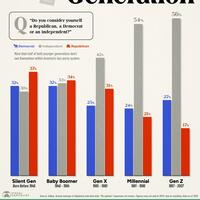

More than half of Gen Z and Millennials identify as politically independent...

It is obvious to everyone that the objective is to silence independent media...

"Our engineers made one final push to test the limits of full-body control and mobility..."

In Groß-Gerau, Hesse, a billion-euro project has been blocked by citizen opposition and the local council’s majority. The town now seems the epitome of Germany’s decline: backward-looking, stubborn, and hopelessly lost in an era that leaves no room for passive solipsism.

"We find ourselves in a world that, to a large extent, is morally, cognitively, and spiritually already collapsing..."

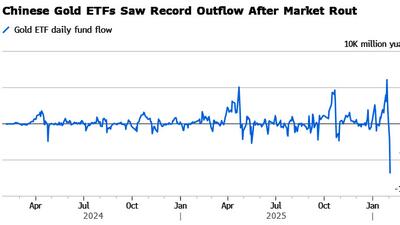

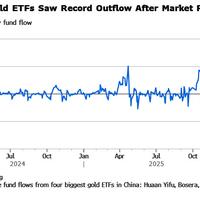

China’s four largest gold-backed exchange-traded funds posted record outflows — about 6.8 billion yuan ($980 million) on Tuesday — just days after they notched record inflows.

Estimate your earnings

oz

Calculate earnings

Today's Top Stories

Assistance and Requests: Contact Us

Tips: tips@zerohedge.com

General: info@zerohedge.com

Legal: legal@zerohedge.com

Advertising: Contact Us

Abuse/Complaints: abuse@zerohedge.com

Make sure to read our "How To [Read/Tip Off] Zero Hedge Without Attracting The Interest Of [Human Resources/The Treasury/Black Helicopters]" Guide

It would be very wise of you to study our privacy policy and our (non)policy on conflicts / full disclosure.Here's our Cookie Policy.