Sponsored Content

Barrick Just Bet $23 Million on This Copper District. One Tiny U.S. Copper Explorer Still Trades for $10 Million

Sponsored on Behalf of Zeus North America Mining

Markets don’t price mining districts in real time.

They ignore them, then slowly re-rate them, then suddenly behave as if the opportunity was obvious from the start.

Copper is increasingly entering one of those phases again.

With supply constraints tightening globally, decades of underinvestment in new mines, and structurally rising demand from electrification and data infrastructure growth, copper prices have pushed to all-time highs. Increasingly, analysts point to AI data centres, grid expansion, and energy-intensive compute infrastructure as long-term demand drivers that could keep pressure on supply well beyond traditional cycle expectations.

In this environment, capital doesn’t move randomly—it moves in district waves, where one mining discovery pulls in senior money, and the market quickly begins searching for the next adjacent re-rating opportunity.

That process is already underway in Idaho.

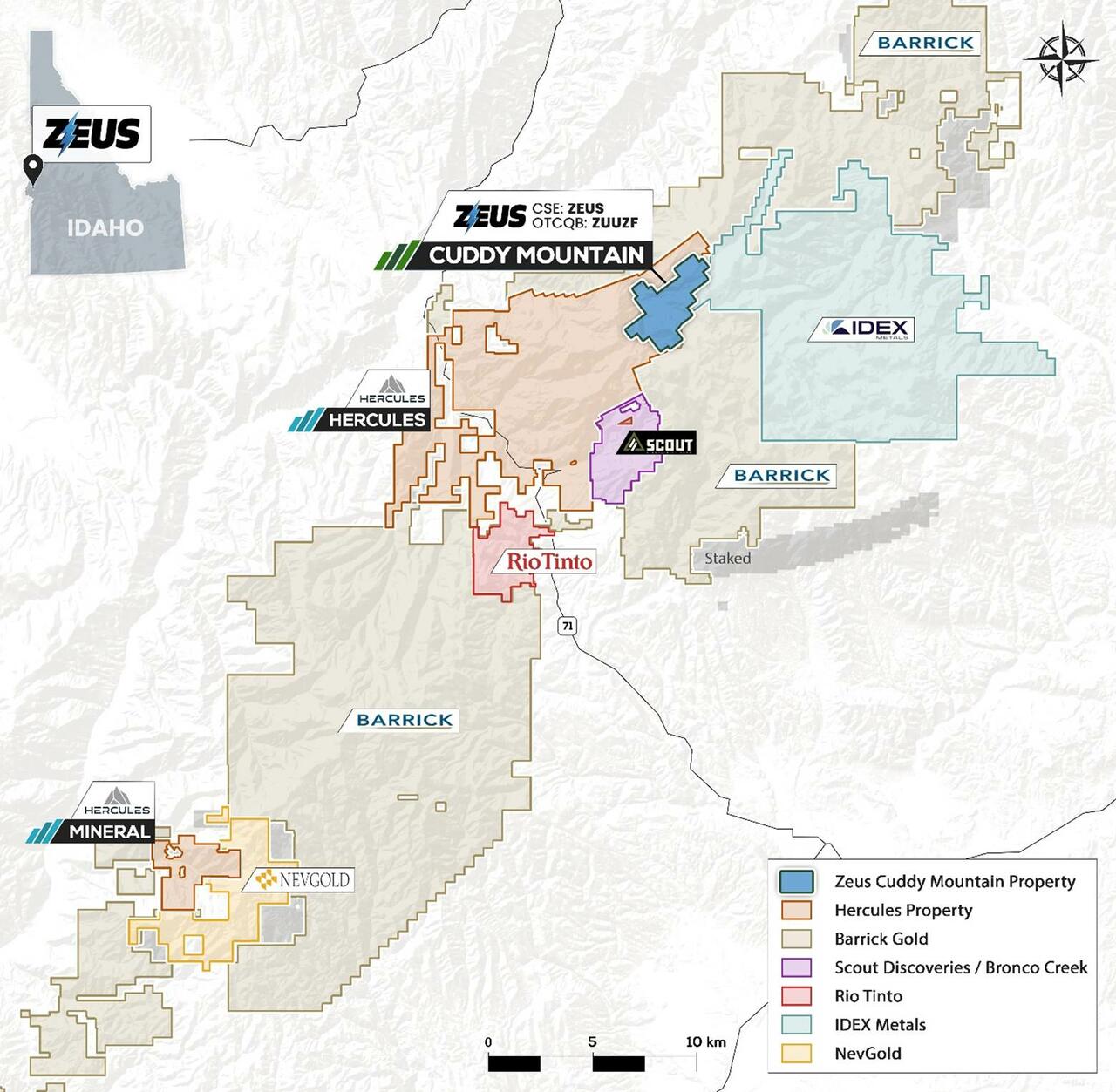

And Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) sits directly inside that emerging U.S. copper district.

Barrick Has Already Entered the District Through Hercules Silver

Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) owns the flagship Cuddy Mountain Property, located within the same emerging copper system as Hercules Silver Corp., where exploration success has outlined the Leviathan copper porphyry discovery and significantly increased attention across the broader district.

Critically, the narrative took a sharp turn when Barrick stepped into Hercules Silver with a $23 million equity investment.

That kind of cheque doesn’t just get noticed—it gets studied, dissected, and immediately over-interpreted by the market.

And it matters far beyond Hercules itself.

Because when a major mining name is willing to deploy capital at that scale into an early-stage district, it is rarely read as a single-asset event. It is interpreted as a signal that something larger is forming at the system level.

While the capital is directed at Hercules Silver, markets rarely have the discipline to keep that story contained.

They start doing what they always do best: connecting dots that may or may not want to be connected.

And once that begins, pricing stops being isolated.

It begins to migrate across the system.

Which raises the question the market cannot avoid for long:

If Barrick is already in Hercules… what has not yet been repriced in the same district?

That is where Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) enters the picture - Hercules’ younger brother, still early, still overlooked, and still with room to run.

Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF): The Adjacent Repricing Candidate

Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) sits immediately adjacent to the same evolving geological trend now being validated through drilling and capital flow.

In early-stage copper belts, adjacency is not cosmetic—it is catalytic:

- A discovery confirms system scale

- Senior capital validates institutional interest

- The market expands beyond the original discovery

- Adjacent ground becomes the next re-rating target

This is the phase where value shifts from individual discoveries to entire districts.

And in that transition, Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) is positioned as a direct beneficiary of second-order capital attention.

The narrative becomes increasingly straightforward:

Barrick has already entered the district through Hercules.

Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) sits next in line if the re-rating expands outward.

Copper at Record Levels Meets Structural AI Demand

This district development is unfolding alongside one of the most powerful macro backdrops in commodities.

Copper is trading near historic highs, driven by tightening supply fundamentals and accelerating structural demand from:

- AI-driven data centre expansion

- Grid modernization and electrification

- Industrial reshoring and infrastructure buildout

- EV and battery-intensive material demand

Unlike prior cycles, this is not cyclical demand—it is structural, multi-decade consumption growth layered onto constrained supply.

That combination is forcing investors to reassess not just producers, but early-stage exploration districts that could define future supply.

How District Repricing Actually Happens

Mining markets rarely move in straight lines.

They re-rate in identifiable waves:

- Early geological indication

- Discovery confirmation (Leviathan system)

- Entry of senior capital (Barrick into Hercules)

- Broader recognition of district scale

- Rapid repricing of adjacent exploration ground

The most aggressive valuation moves typically occur at stages four and five—when the market realizes the discovery was not isolated, but part of a broader system.

ZEUS NORTH AMERICA MINING (CSE: ZEUS; OTCQB: ZUUZF) AT THE EARLIEST STAGE OF THE CURVE

At approximately a $10 million market capitalization, Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) remains at the earliest phase of district recognition.

At this stage, the market is not pricing defined resources or development timelines.

It is pricing asymmetric exposure to a district already being validated by senior capital.

That distinction matters—because it defines where repricing has not yet occurred, but historically tends to concentrate once attention expands outward from the original discovery.

Where the Market Is Now Looking

Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) is not the discovery story.

It is not the re-rated asset.

It is the adjacent position inside a district already being validated at the capital level.

With Barrick already flowing into Hercules, the market naturally shifts to the next question:

Does capital remain concentrated in the discovery… or does it begin expanding into adjacent targets like Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF)?

In past district cycles, that second phase is often where the most significant re-rating moves occur—when the market finally catches up to what the geology was signaling all along.

Capital Structure and Asymmetric Torque

Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) sits at the earliest stage of the U.S. copper exploration curve, with a structure that offers maximum torque to any shift in district perception or capital flow.

At a roughly $10 million market capitalization, Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) occupies deep microcap territory, where valuation is not driven by production or defined resources, but by perceived geological exposure within an emerging system.

The company’s structure reflects a classic early-stage exploration profile:

- Low base valuation

- Limited expectations embedded in price

- High sensitivity to district news flow

- Disproportionate reaction to incremental capital attention

In practical terms, this creates asymmetric torque—where upside re-rating potential can significantly exceed current market assumptions if district attention continues to expand.

This is precisely the stage in mining cycles where the largest moves tend to occur—not in already re-rated developers, but in early-stage explorers positioned within evolving discovery systems before full market recognition sets in.

Zeus North America Mining (CSE: ZEUS; OTCQB: ZUUZF) remains in that window.

Learn more about Zeus North American Mining at www.zeusminingcorp.com/

DISCLAIMER:

This article is a paid advertisement on behalf of Zeus North America Mining and should not be seen as investment advice.

Senergy Communications Capital Inc. has received compensation of CAD $90,000 from Zeus North America Mining in consideration for providing marketing and investor awareness services.

Statements and opinions expressed are those of the author and not necessarily those of Senergy, its directors, officers, or employees. The author is wholly responsible for the validity of the statements. Senergy has not independently verified all such information and does not guarantee its accuracy or completeness. The information provided is for informational purposes only and should not be construed as a recommendation to buy or sell any security. This article does not constitute investment advice. All investments carry risk, and readers should consult their own financial advisors before making any investment decisions. Any action taken by readers as a result of this information is at their own risk. This article is not a solicitation for investment, nor does Senergy provide general or specific investment advice.

Forward-Looking Information

This document may contain "forward-looking statements" within the meaning of applicable Canadian securities laws. Such statements reflect management's expectations regarding future growth, business plans, and opportunities of Zeus North America Mining. Forward-looking statements are based on numerous assumptions and are subject to known and unknown risks and uncertainties, many of which are beyond the control of Zeus North America Mining. Actual results may differ materially. Readers are cautioned not to place undue reliance on forward-looking statements. Except as required by law, Zeus North America Mining undertakes no obligation to update or revise any forward-looking statements. Please refer to SEDAR+ for all filings and updated information on Zeus North America Mining.

Investing involves significant risks, including the possible loss of the entire investment. Past performance is not necessarily indicative of future results. Readers should conduct their own due diligence, carefully consider their risk tolerance, and seek professional advice before investing.

Senergy Communications Capital Inc. is neither an investment adviser nor a broker-dealer. The information presented on the website is provided for informative purposes only and is not to be treated as a recommendation to make any specific investment. No such information on this article constitutes advice or a recommendation.