Axios reports US plans for a final blow despite possible ceasefire agreement upcoming - Newsquawk US Market Open

- Axios reported that the US Pentagon is preparing for massive "final blow" of Iran war that could include the use of ground forces and a massive bombing campaign.

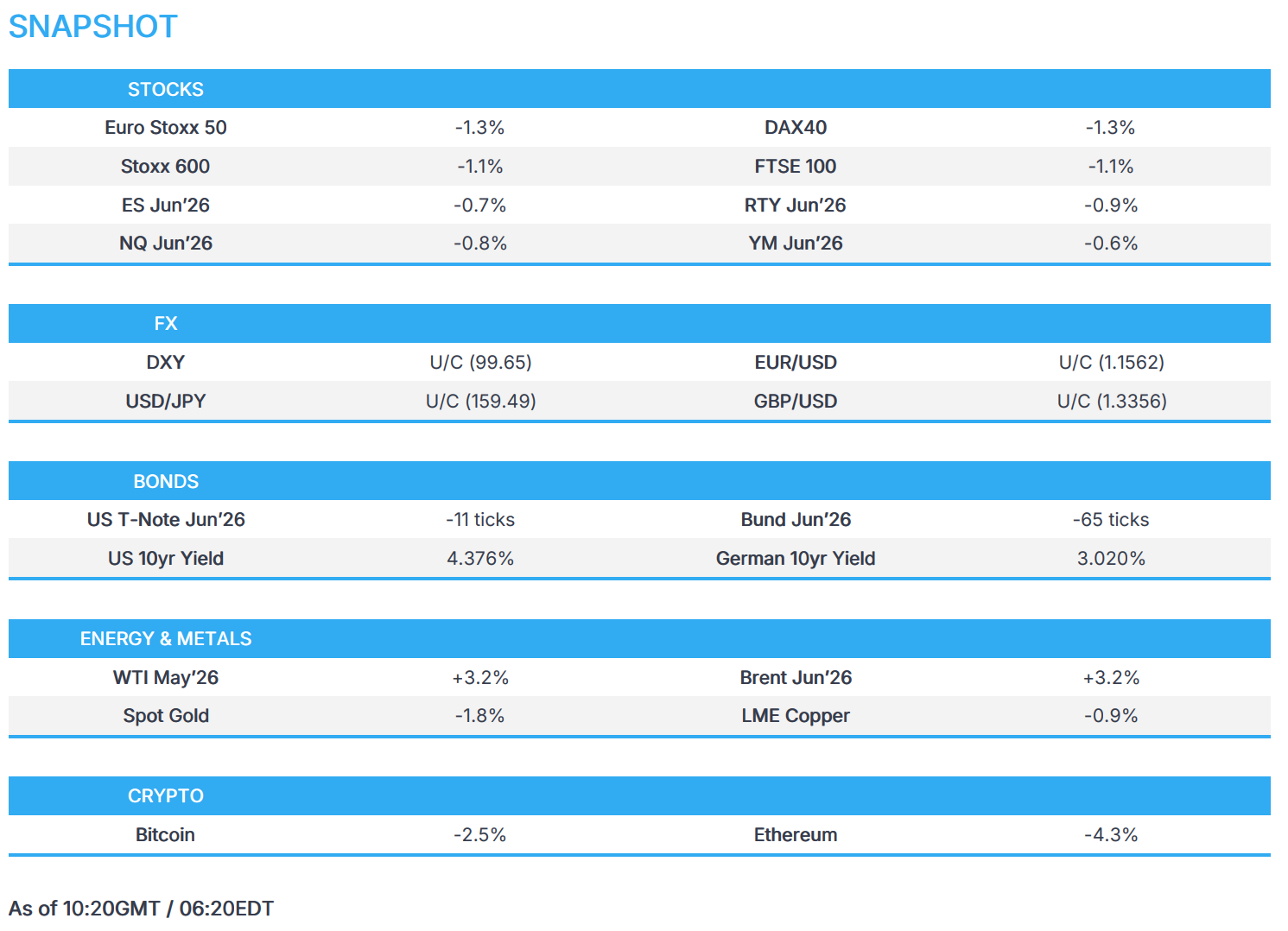

- Global equities under pressure as the Iran war persists, Tech falters following Google update.

- DXY is essentially flat, G10s incrementally lower.

- Fixed income action is dictated by energy movements as numerous BoE and Fed officials await.

- Crude futures on a firmer footing as geopolitical tensions show no tangible signs of abating.

- Looking ahead, highlights include US Initial Jobless Claims (Mar/21). Speakers include BoE's Taylor & Greene, Fed's Cook, Miran, Jefferson & Barr, BoC's Rogers. Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -1.1%) have gotten off to a softer start to Thursday's session. The DAX 40 underperforms, hindered by poor Porsche SE (-2.6%) earnings, while the SMI outperforms with only mild losses, as Kuehne+Nagel, along with the broader shipping sector, is supported by Hapag-Lloyd earnings.

- European sectors are entirely in the red, with Basic Resources, yet again, sitting at the bottom of the pile as metals prices continue to fall. Technology also prints decent losses, following news stateside by Google that its new TurboQuant tech can reduce the amount of memory needed for AI workloads, which is weighing on computer memory and storage makers (ASML -3.8%).

- Other key movers include Boliden, STMicroelectronics and BMPS. Boliden announced that its Q1 earnings will take a SEK 400mln hit due to the seismic activity at the Garpenberg mine. The Co. further guides that production at the mine will resume at 30% capacity until further notice. For the Italian bank, the Board has reappointed Luigi Lovaglio as CEO after he challenged the bank’s plan to replace him when his term ends in April.

- US equity futures are under pressure, following their European peers. ES remains below the 200-SMA and is struggling to return above the key range lows of 6635, a worrying sign of market sentiment. The 20-, 200-SMA bearish cross has also been confirmed. However, there are metrics that point to a short-term bounce: 1) recent significant de-grossing, 2) fear index showing 'extreme fear', and 3) the increased probability of a significant low being printed in late March/early April based on historical data.

- H&M (HMB SS) Q1 2026 (SEK): Op. Profit 1.51bln (exp. 1.39bln), Revenue 49.6bln (exp. 50.5bln), EPS 0.45 (exp. 0.44), Net Income 704mln (exp. 706.6mln); March Sales +1% Y/Y.

- Hapag Lloyd (HLAG GY) FY 2025 (USD): Revenue 21.1bln (prev. 20.7bln Y/Y), EBITDA 3.18bln (prev. 4.64bln Y/Y); co. noted that the conflict in the Middle East is now causing considerable disruptions and sharply increasing operational costs. Outlook remains subject to considerable uncertainty due to the highly volatile development of freight rates and the conflict in the Middle East.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is essentially flat and trades within a narrow 99.56-99.75 range, with price action taking a breather after a string of ceasefire related volatility. Recent reports surrounding the Middle East situation suggests that US President Trump told aides he wants a speedy end to the Iran war and wants to wrap up the conflict in the coming weeks, via WSJ. Elsewhere, Israeli Media reported that US President Trump may announce a ceasefire with Iran by next Saturday. Jobless claims and a slew of Fed speak is due throughout the day.

- G10s are incrementally lower against the USD (ex-Antipodeans). Ultimately, subdued price action as markets await updates related to concrete progress on the ceasefire plan, or the risk of another bout of escalation measures. Most recently, Axios reported that Trump is preparing for a massive “final blow” against Iran. Antipodeans are at the bottom of the G10 pile this morning, with the Kiwi underperforming – pressure which follows the broader downbeat risk-tone. EUR/USD trades within a very thin 1.1547-1.1572 range, and ultimately little moved to ECB’s Nagel and de Guindos. Elsewhere, Cable is incrementally lower, as traders await commentary from BoE’s Breeden, Taylor and Greene. Focus will be on the former, given Taylor spoke last week (remained dovish), whilst Greene spoke on Wednesday.

- NOK is net-unchanged in the aftermath of the Norges Bank policy announcement, where the Bank kept rates steady at 4% (as expected). There was some volatility at the time, with EUR/NOK moving higher as traders unwound outside bets of a hike. That move since entirely pared. Decision aside, focus was on the MPR and accompanying commentary was hawkish, with the Bank noting that "it will likely be appropriate to raise the policy rate at one of the forthcoming monetary policy meetings". This was also reflected by the updated MPR, whereby the end-2026 rate is now seen at 4.35% (prev. 3.71%); 2027 was revised higher to 3.98% (prev. 3.31%), and the "terminal rate" was raised to 3.54% (prev. 3.20%).

FIXED INCOME

- Once again, another session dictated by energy movements and the associated implications for prices and yields.

- USTs are lower by 12 ticks at most, to a 110-16+ trough. If the move continues, we look to the 110-05+ mark from the 24th, and then the 109-31+ WTD base. Ahead, a handful of data points, numerous Fed speakers and supply features in a relatively busy schedule; however, geopolitics will likely continue to dictate.

- Bunds in-fitting. At a 125.30 low, with losses of nearly 70 ticks at most. If the move continues, we look to support at 125.02 and then the 124.77 WTD base. For Europe, newsflow is somewhat limited, with no move to a handful of data points or ECB officials. The region's docket ahead is a little light, and as such, action will be determined by the above US points and/or Middle East developments.

- Gilts took the lead from peers and opened with losses of over 60 ticks before falling another 35 or so to a 87.73 trough. If the move continues, we look to recent bases at 87.06, 86.81 and then the contract low of 85.91. A busy BoE docket today, with Taylor and Greene scheduled; though, we have yet to see anything of pertinence from Breeden.

- UK DMO sells GBP 300mln 5.375% January 2056 Gilts via tender: Avg. Yield 5.517% (prev. 5.476%), B/C 3.84x (prev. 3.07x).

- Australia sold AUD 150mln in 2030 indexed bonds, b/c 3.67, avg. yield 1.9698%.

COMMODITIES

- Crude futures gradually edged higher overnight and held onto that strength throughout the European morning, with Brent Jun'26 printing a USD 100.96/bbl peak (vs USD 97.69/bbl low) while WTI May'26 prints a current USD 94.13-90.71/bbl range.

- On the geopolitical front, US President Trump reportedly told aides that he wants a speedy end to the war and believes the conflict is in its final stages. Meanwhile, Israeli media reported that Trump may announce a ceasefire with Iran by next Saturday, even without a final agreement, while N12 News separately said the working assumption in Israel is that he could announce a ceasefire as soon as this coming Saturday. More recently, it was reported US Pentagon is reportedly preparing for a massive "final blow" of the Iran war, via Axios.

- Spot gold is lower after a two-day recovery, with bullion back under USD 4,450/oz at the time of writing, giving back most of the prior session gains, amid the conflicting US and Iranian statements. Spot gold currently resides in a USD 4,412-4,544/oz range after finding support on Monday at its 200-DMA (4,091.57/oz)

- Base metals are also softer, with copper under pressure as investors weigh the inflationary implications of the conflict alongside the risk of weaker global activity and softer demand. 3M LME copper resides in a USD 12,114.00- 12,276.08/t range at the time of writing.

- Russian Deputy PM Novak says "we will impose a gasoline export bank if necessary"; has possibility to increase oil production if required, but investment will be needed; is already trading oil without discount, and with a premium in a number of lines.

- French Commerce Minister said release of strategic oil reserves to be discussed at G7 minister meeting on Monday.

- Japan begins releasing national oil reserves, as expected, according to Kyodo.

- Turkish oil tanker was hit by a drone in the Black Sea near Istanbul.

- Saudi Arabia’s oil sales to China and India are set to be lower-than-usual levels next month, according to Bloomberg.

- Japan is reportedly to lift restrictions on coal-fired power plant operation as an emergency response to the Middle East situation for a one-year limit period, according to the Nikkei.

- Philippines suspends electricity market due to Middle East conflict and proposes modified administered pricing by April 1st, cites fuel supply risks and price volatility for the suspension.

- Pilbara ports in Australia said they closed the ports of Ashburton, Cape Preston West, Dampier and Varanus Island due to cyclone Narelle.

TRADE/TARIFFS

- Germany reportedly drafts a plan to hit US tech, drug supplies and companies, Bloomberg reported citing sources; officials are mapping vulnerabilities in US supply chains to apply pressure on the US.

- China's Foreign Ministry, on Trump's China visit announcement for May 14-15th, said the two sides have maintained communication.

- China Commerce Ministry will impose an additional 55% tariff on beef imports from Australia after quota threshold reached.

- EU's Dombrovskis said we have received assurances from the US that they intend to honour the trade deal.

- US President Trump said Supreme Court ruling on tariffs will cost the US hundreds of millions.

NOTABLE EUROPEAN DATA RECAP

- Spanish GDP Growth Rate QoQ Final (Q4) Q/Q 0.8% vs. Exp. 0.8% (Prev. 0.6%).

- Spanish GDP Growth Rate YoY Final (Q4) Y/Y 2.7% vs. Exp. 2.6% (Prev. 2.7%).

- German GfK Consumer Confidence (Apr) -28.0 vs. Exp. -26.5 (Prev. -24.7, Low. -32.2, High. -25.6).

- Italian Business Confidence (Mar) 88.8 (Prev. 88.5).

- Italian Consumer Confidence (Mar) 92.6 (Prev. 97.4).

- French Consumer Confidence (Mar) 89 vs. Exp. 89 (Prev. 91, Low. 88, High. 90).

- French Business Confidence (Mar) 99 vs. Exp. 100 (Prev. 102, Low. 98, High. 103).

CENTRAL BANKS

- Norges Bank maintains its rate unchanged at 4.0% as expected; "it will likely be appropriate to raise the policy rate at one of the forthcoming monetary policy meetings". STANCE. The Committee judges that a tighter monetary policy stance is needed to return inflation to target within a reasonable time horizon. The inflation outlook indicates that an increase in the policy rate will likely be required. The Committee therefore wants to await further information on the prospects for inflation. FUTURE POLICY. The future path of the policy rate will depend on economic developments. If the outlook indicates higher inflation than currently projected, a higher policy rate than currently envisaged may be required.

- US Treasury Secretary Bessent said to have discussed ways to recast ties between the Fed and the Treasury in the Bank of England's image, and praises BoE's market intervention capabilities, according to FT.

- ECB's de Guindos said the outbreak for the Iran war has made the growth and inflation outlook significantly more uncertain, sharp increase in energy prices poses upside risks for inflation and downside risks for economic growth. ECB is well positioned to navigate this uncertain period.

- ECB's Nagel said the ECB will have enough data by April to determine if they need to act or whether to wait and see.

- ECB hopes to look through energy price shock from Iran war and Lagarde said it's too early to know the impact of the Iran war, while it sees rates steady if shock is temporary but may hike rates twice if energy shock is persistent, according to FT.

- BoE's Breeden (neutral) says firms and workers are likely to have less price and wage bargaining power, so second round effects less likely.

- BoJ Governor Ueda said large JGB holding doesn't make policy adjustments difficult, adds conducting policy to achieve price stability target.

- RBA Assistant Governor Kent said the board will set monetary policy to achieve low and stable inflation and full employment. Will continue to assess the countervailing forces operating on the economy. Middle East conflict has tightened financial conditions. The longer the conflict persists, the larger the economic impacts will be.

- CNB Minutes (Mar): Ready to tighten policy if core inflation rises, agreed a rate hike is premature now.

- UBS expects the Fed to deliver two 25bps cuts in September and December (prev. saw cuts in June and September).

NOTABLE US HEADLINES

- White House confirms that US President Trump is to hold a cabinet meeting is to be held from 10:00EDT/14:00GMT on Thursday.

GEOPOLITICS

MIDDLE EAST

- US Pentagon reportedly prepares for massive "final blow" of Iran war, Axios reported. The Pentagon developing military options for a "final blow" in Iran that could include the use of ground forces and a massive bombing campaign. Options include: Invading or blockading Kharg Island; Invading Larak, an island that helps Iran solidify its control of the Strait of Hormuz; seizing the strategic island of Abu Musa and two smaller islands, which lie near the western entrance to the strait and are controlled by Iran but also claimed by the UAE; Blocking or seizing ships that are exporting Iranian oil on the eastern side of the Hormuz Strait.

- Pakistan Foreign Minister says US-Iran indirect talks are taking place through messages being relayed by Pakistan.

- US President Trump says NATO nations have done absolutely nothing to help with Iran.

- US Pentagon is considering diverting Ukraine military aid to the Middle East, WaPo reported. Comes as the war in Iran depletes some of the US military’s most critical munitions, according to sources cited.

- US President Trump said Iran is negotiating and wants a deal, but is afraid to say so, adds no one in Iran wants to be Supreme Leader right now.

- Iran's Foreign Minister said Iran's current policy is to continue resistance in the face of ongoing unprovoked American-Israeli aggression while ruling out negotiations and ceasefire in the absence of required guarantees, according to Press TV. Vessels belonging to “friendly countries” including China, Russia, India, Iraq and Pakistan had been allowed to pass through the Strait of Hormuz.

- IRGC has reportedly imposed a de facto ‘toll booth’ regime in the Strait of Hormuz, requiring vessels to submit full documentation, obtain clearance codes and accept IRGC-escorted passage through a single controlled corridor, according to Lloyd's List.

- US Central Command said USS Abraham Lincoln aircraft carrier continues to carry out strikes on military targets in Iran, while CENTCOM also said most of the Iranian facilities used to build missiles, drones and warships, are badly damaged or destroyed.

- Iranian-linked Handala Hack Group say they have "initiated a new phase of Operation Lockheed Martin (LMT)", said Co. employees have 48 hours to respond, Mehr News reported.

- Pakistani official said Israel took Iran's Foreign Minister Araghchi and Parliamentary Speaker Ghalibaf off the hit list after Pakistan requested the US not to target them.

- Iran targeting an American fuel supplier, according to a report cited by Tasnim.

- The IRGC naval commander was eliminated in Bandar Abbas, according to the Jerusalem Post citing an Israeli source.

- Hezbollah said it targeted headquarters of Israel's Ministry of Defense with missiles on Thursday and barracks affiliated with the military intelligence department of Israel's army in the north of Tel Aviv, was also one of the targets of the operation.

- Egypt's Foreign Minister said Cairo is ready to host talks to support de-escalation between US and Iran, and backs President Trump's push for negotiations, adding he hopes there will be direct talks between the two sides.

- UAE Foreign Minister discussed developments in the region and the repercussions of Iran's missile attacks on the UAE and brotherly countries in a call with foreign ministers of Pakistan, Britain, Spain, France and Kazakhstan.

- Local sources say huge explosions occurred in the Amir Sultan Air Base in Saudi Arabia following drone attacks.

- Explosions heard in Iranian cities of Isfahan and Bandar Abbas.

- Arab sources report a loud explosion was heard in the capital of the UAE, according to SNN.

- Israel's Ben Gurion airport halts all operations amid Iranian missile barrage, according to Press TV.

RUSSIA-UKRAINE

- Russia's Kremlin says "we have not lost interest in peace talks"; territory is one issue that has not been settled.

- Ukrainian President Zelensky said Ukraine does not see any genuine desire from Russia to end the war.

- Russia attacked damaged ports and energy infrastructure in Ukraine's Odesa region, according to the regional governor.

- UK authorises armed forces to board Russian shadow fleet tankers in British waters, according to The Guardian.

CRYPTO

- Bitcoin falls back below USD 70k and Ethereum dips to USD 2.1k.

APAC TRADE

- APAC stocks traded cautiously as the geopolitical situation in the Middle East remained fluid, with mixed messages from the US and Iran about talks, while strikes persisted overnight against Iran and its regional neighbours.

- ASX 200 closed slightly lower with miners, tech and materials front-running declines, but with downside cushioned by gains in energy, defensives and financials, while price action was contained by a lack of data or fresh major catalysts.

- Nikkei 225 retreated as the rebound in oil stoked inflationary and growth concerns, given Japan's large dependency on Middle East oil, despite the government releasing emergency oil reserves, as planned.

- Hang Seng and Shanghai Comp were pressured amid a deluge of earnings releases and with developer debt concerns stoked as China Vanke seeks another bond repayment delay, whilst it works on a restructuring plan.

NOTABLE ASIA-PAC HEADLINES

- Japan's provisional budget is seen totalling around JPY 8.6tln, according to NHK.

NOTABLE APAC DATA RECAP

- Hong Kong Imports YoY (Feb) Y/Y 29.9% (Prev. 38.1%).

- Hong Kong Balance of Trade (Feb) -64.2B (Prev. -14.1B).

- Hong Kong Exports YoY (Feb) Y/Y 24.7% (Prev. 33.8%).

- Japanese Stock by Foreigners (Mar/21) -2509.7.

- Japanese Services PPI (Feb) 2.7% vs Exp. 2.6% (Prev. 2.6%).

Loading...