Brent -15% as US and Iran reach 2 week ceasefire, NZD outperforms amid RBNZ hike discussion - Newsquawk US Market Open

- US President Trump announced he is to suspend the bombing of Iran for two weeks, subject to Iran opening up the Strait of Hormuz, while he stated that this will be a double-sided ceasefire. Energy slumps, with Brent slipping below USD 95/bbl.

- Trump confirmed they received a 10-point proposal from Iran, and believe it is a workable basis on which to negotiate, while he stated that almost all of the various points of past contention have been agreed to between the US and Iran.

- Iranian Press SNN noted of a potential ceasefire violation, highlighting several explosions that occurred in Siri and Lavan islands.

- Iran’s National Security Council said that within a few hours, if firing does not stop in southern Lebanon, the air and missile unit will bomb Tel Aviv

- Global equities find comfort, airlines and miners highly benefit.

- USD hit, Kiwi outperforms amid RBNZ hike discussion.

- Bonds soar and the curve steepens, with central bank paring back hawkish bets.

- Looking ahead, highlights include FOMC Minutes, Speakers including Fed's Daly, Waller & US President Trump, Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

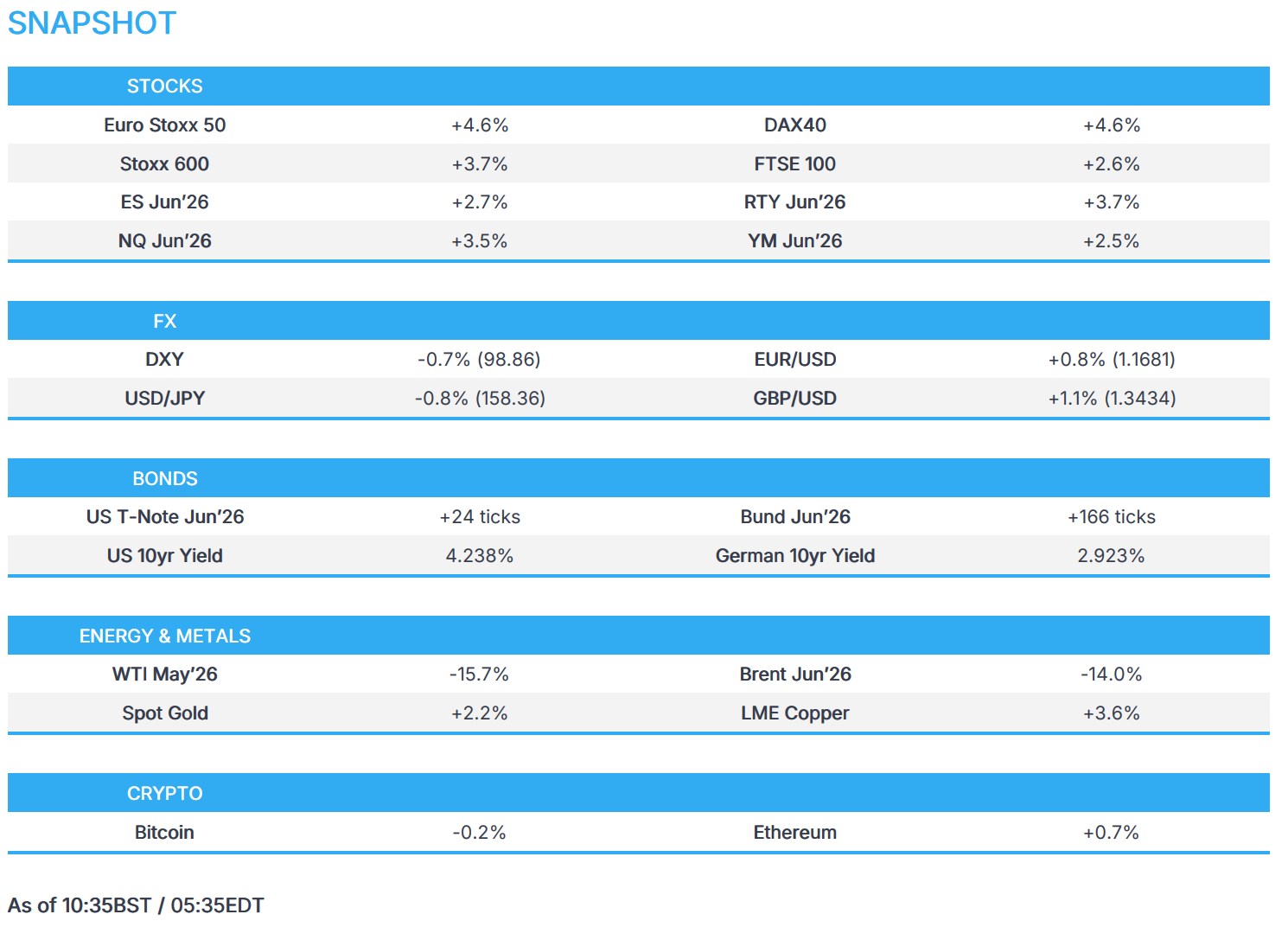

- European bourses (STOXX 600 +3.7%) have expressed relief from the announcement of a two-week Iran ceasefire, with all indices gaining by over 2%.

- European sectors are entirely in the green, ex. Energy and Utilities. Cyclicals benefit the most, with Travel and Leisure, Technology and Consumer Products and Services topping the pile.

- US equity futures (ES +2.7% NQ +3.5% RTY +3.7%) have surged alongside their global peers. ES has now returned to the wide 6635-7063 range that formed in the latter part of 2025, and thus far, finding some resistance at the 50-SMA at 6819.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX markets began the session firmly risk-on as the US and Iran agreed to a two-week ceasefire, clearing a path for the "re-open" of the Hormuz Strait. Unsurprisingly, the Buck has been knocked with DXY -0.7%, as it loses its favour as the preferred hedge against energy with Brent crude below the USD 100/bbl mark. In a note this morning, Jefferies set out three potential future scenarios: 1) a narrow diplomatic Off-Ramp, centred on reopening the Strait of Hormuz under a face-saving framework for Iran, 2) frozen conflict, where the ceasefire is extended or repeatedly renewed without a formal peace agreement, with oil trading below crisis peaks but above pre-war levels. 3) escalation resumes: triggering renewed disruption fears, pushing oil prices higher, and driving a sharp risk-off move in global markets.

- NZD is the clear outperformer against the USD, helped by both the positive Middle East development and remarks in RBNZ's post-meeting presser, where Governor Breman said the MPC discussed the possibility of raising rates in April and May meetings, and the "Frequency of rate hikes could be every meeting or every second meeting" Despite the Kiwi's strength, AUD/USD has also been helped alongside risk sentiment and a rebound in precious metals.

- GBP is relieved by the slump in crude prices, with Cable +1% at the time of writing. Markets are still expecting c. 30bps of hiking for the BoE, a pullback of the same magnitude since Tuesday's close. The Cable rally stalled just above the 1.3440 mark; EUR/GBP has recently fallen just below its 200 DMA, and beneath the 0.87 mark – next up, 50 DMA at 0.8687.

FIXED INCOME

- Global fixed benchmarks are soaring this morning, with upside facilitated by the announcement of a two-week ceasefire between the US and Iran, which has helped to pressure the crude complex. As a whole, bonds are stronger, and a clear curve steepening bias is seen across the complex.

- USTs are currently trading at session highs, holding at the top end of a 111-05+ to 111-21 range. US paper moved higher on the announcement itself, and then gradually strolled to peaks as the session progressed. European price action has been fairly muted, with the benchmark ultimately trading sideways. From a yield perspective, the 2yr yield now resides around 3.719% (vs Tuesday's close at 3.80%) and well below the peaks from the Iranian conflict at 4.027%. Geopols aside, focus today will turn to the FOMC Minutes of the March confab, where the Bank left rates unchanged at 3.50-3.75%, with no change to forward guidance, balance sheet plans or implementation guidance. A US 10yr auction is also due.

- Bunds and Gilts follow the above, and currently reside at highs. The former is higher by over 175 ticks and within a 125.74 to 126.45 range, whilst UK paper extends gains of over 230 ticks, in an 89.70 to 90.18 range. Europe and UK fixed income has been considerably pressured since the start of the Iranian war, given their high dependence on external energy. For now, some short term reprieve across assets – and this has been reflected in market pricing, with only 2bps worth of hikes priced in for the ECB’s April meeting (vs 12bps pre-ceasefire); however, the long-term outlook remains uncertain, with markets still pricing in 45bps worth of hikes by year-end. From a yield perspective, the UK 2yr yield sank at the open, bottoming at 4.044% (vs post-Iran war peak at 4.712%); GE 2yr yield now hovers around the 2.50% mark.

- Germany sells EUR 3.817bln vs exp. EUR 5.0bln 2.90% 2036 Bund: b/c 1.24x (prev. 1.18x), average yield 2.92% (prev. 2.89%), retention 23.66% (prev. 23.78%).

COMMODITIES

- The US and Iran have agreed in principle to a two-week ceasefire, brokered with support from Pakistan, under which the US will suspend bombing, and Iran will allow controlled reopening of the Strait of Hormuz. President Trump described the move as a “double-sided ceasefire,” saying most major disputes have already been resolved and that a broader peace agreement is close. Iran has accepted the pause, with its leadership approving negotiations set to begin in Islamabad, where both sides aim to finalise terms based on a 10-point proposal submitted by Tehran.

- The ceasefire remains conditional and fragile. Iran stated it will halt military responses only if attacks stop, while warning it remains ready to retaliate if provoked. The arrangement includes limited safe passage through the Strait of Hormuz under Iranian coordination, a critical step given the severe disruption to global shipping and energy flows. Israel has signalled support for the temporary pause, though there is conflicting information over whether Lebanon is included.

- However, it is worth noting recent reporting suggests that explosions were heard at Iran's Lavan refinery, and other reports suggest that explosions were also heard at Iran's Siri Island - details are light at this stage. But some may begin to question whether the ceasefire has already been violated.

- Energy prices plummeted. Crude futures both tumbled beneath the USD 100/bbl level following the announcement of a two-week US-Iran ceasefire within a couple of hours prior to President Trump's deadline. WTI May'26 resides towards the bottom of a USD 91.70-96.27/bbl and Brent Jun'26 towards the foot of a USD 91.05-109.19/bbl range. Dutch TTF slipped to under EUR 45/MWh.

- Spot gold rose above USD 4,850/oz before paring gains slightly to trade around the middle of a USD 4,713-4,858/oz range. Spot silver topped its 100 DMA (USD 76.11/oz) and resides near the top of a USD 73.38-77.65/oz parameter.

- Copper climbed to a three-week high, and aluminium also advanced as easing concerns over global growth lifted sentiment. 3M LME copper trades towards the top end of a USD 12,550.00-12,743.90/t range.

- China has reportedly given additional crude import quotas to independent refiners to maintain fuel production at the mandated 2025 levels.

- Abu Dhabi's media office announces that three people were injured after debris from air defence interception sparked fires at the Habshan gas complex, operations have been suspended temporarily.

- IATA chief said if Hormuz Strait were to reopen, it will still take a period of months to get where jet fuel supply needs to be.

TRADE/TARIFFS

- US carmakers accuse EU of blocking supersized pick-up trucks from roads, according to FT.

NOTABLE EUROPEAN DATA RECAP

- German Factory Orders MoM (Feb) M/M 0.9% vs. Exp. 2% (Prev. -11.1%).

- French Balance of Trade (Feb) -5.8B vs. Exp. -2.3B (Prev. -1.8B).

- French Imports (Feb) 57.8B (Prev. 55.3B).

- French Exports (Feb) 52.0B (Prev. 53.4B).

- EU Retail Sales MoM (Feb) M/M -0.2% vs. Exp. -0.2% (Prev. -0.1%).

- EU Retail Sales YoY (Feb) Y/Y 1.7% vs. Exp. 1.6% (Prev. 2%).

- EU PPI MoM (Feb) M/M -0.7% vs. Exp. -0.7% (Prev. 0.7%).

- EU PPI YoY (Feb) Y/Y -3.0% vs. Exp. -3% (Prev. -2.1%).

- UK Halifax House Price Index MoM (Mar) M/M -0.5% vs. Exp. 0.1% (Prev. 0.3%).

- UK Halifax House Price Index YoY (Mar) Y/Y 0.8% vs. Exp. 1.5% (Prev. 1.3%).

- Hungarian Core Inflation Rate YoY (Mar) Y/Y 1.9% (Prev. 2.1%).

- Hungarian Inflation Rate YoY (Mar) Y/Y 1.8% (Prev. 1.4%).

- Hungarian Inflation Rate MoM (Mar) M/M 0.40% (Prev. 0.1%).

CENTRAL BANKS

- RBNZ keeps the OCR at 2.25%, as expected, while it stated in the near term inflation, is expected to increase and economic recovery to weaken, while committee is focused on ensuring that inflation returns at a 2% target midpoint over the medium-term.

- RBNZ Governor Breman said in online post-meeting press conference that the decision to hold rates was a consensus, adds discussed raising rates at today's meeting but were not close to hiking. We were not close to hiking rates today and there were no strong advocates for a hike today. If oil prices keep falling our inflation forecast would be on the high side. Frequency of rate hikes could be every meeting or every second meeting, it depends.

- Fed Vice Chair Jefferson (voter) said sees downside risks to employment and upside risks to inflation, while he is cautious on the economic outlook and noted uncertainty is elevated. Current policy rate is well-positioned to respond and rate is broadly in range of neutral. US labour market is roughly in balance and susceptible to adverse shocks. US inflation remains above the central bank's targets and warns that persistent elevated energy prices can weigh in consumer and business spending.

- ECB's Dolenc said that if the Iran war drags on, it will be very bad for inflation and growth.

- RBI keeps Repurchase Rate unchanged at 5.25%, as expected, with the decision unanimous and it maintains a neutral stance.

- ASB Bank now sees RBNZ raising rates in September and December of this year vs prev. forecast of a December hike.

GEOPOLITICS

MIDDLE EAST

- US President Trump announced he is to suspend the bombing of Iran for two weeks, subject to Iran opening up the Strait of Hormuz, while he stated that this will be a double-sided ceasefire. Trump said the reason for doing so is that they have already met and exceeded all military objectives, and are very far along with a definitive agreement concerning long-term peace with Iran, and peace in the Middle East. Furthermore, he confirmed they received a 10-point proposal from Iran, and believe it is a workable basis on which to negotiate, while he stated that almost all of the various points of past contention have been agreed to between the US and Iran, although a two-week period will allow the agreement to be finalised and consummated.

- US President Trump posted "A big day for World Peace! Iran wants it to happen, they’ve had enough! Likewise, so has everyone else! The United States of America will be helping with the traffic buildup in the Strait of Hormuz. There will be lots of positive action! Big money will be made. Iran can start the reconstruction process...this could be the Golden Age of the Middle East!!!"

- US President Trump tells AFP that Iran deal is complete and comprehensive victory for the US, also said Iran uranium will be perfectly taken care of and that he believes China got Iran to negotiate.

- Iranian Press SNN notes of a potential ceasefire violation, highlighting several explosions that occurred in Siri and Lavan islands. Furthermore, Iran’s National Security Council says within a few hours, if firing does not stop in southern Lebanon, the air and missile unit will bomb Tel Aviv.

- Iran said negotiations with the US will be held in Islamabad to finalise details, with the aim of confirming Iran's battlefield achievements politically within maximum of 15 days, with talks to begin April 10th and may be extended if both sides agree. Talks with the US do not mean of the war, according to Iranian media. The safe passage through Hormuz is possible for two weeks and Foreign Minister Araghchi said their forces will halt operations if attacks on Iran cease.

- Pakistan's President invites US and Iran delegates to Islamabad on Friday, while reported also noted that EU envoys Witkoff, Kushner and VP Vance is expected to attend US-Iran talks.

- US official said ceasefire will begin this evening, but they believe it may take some time for orders to reach Revolutionary Guard units at the field level.

- Iran and Oman reportedly will be allowed to charge for passage in the Strait of Hormuz as part of a ceasefire.

- Israel's Ynet cites security sources stating that Iran ceasefire will also include Lebanon.

- Iran's Supreme Leader instructed negotiators to seek a truce, according to Axios.

- Iran's permanent ambassador to the UN said Iran categorically rejects any temporary ceasefire, while he stated that any solution to the end of the conflict must guarantee a definitive and irreversible anti-aggression and establish a just and lasting peace.

- The US will insist on removing nuclear materials from Iran, Al Hadath reported citing Israeli officials via Haaretz.

- White House official said Iran ceasefire takes effect once the Strait of Hormuz is reopened.

- Senior White House official said Israel is part of the 2-week ceasefire, according to CNN. Israel agrees to suspend bombing while talks are ongoing.

- Omani Transport Minister said no fees can be imposed on the Strait of Hormuz according to the signed agreements.

- Iraq's Islamic Resistance suspends operations for two weeks.

- Hezbollah will announce formal position on ceasefire and response to Israeli PM's assertion that Lebanon is not included, according to sources.

- New wave of Iranian missiles fired towards Israel.

- Israeli military official said Israel is still striking Iran, according to CNN.

- Several explosions reported at Iran’s Sirri Island on Wednesday morning; source of explosions unknown, Mehr News reported.

- Explosions heard at the Lavan oil refinery (50k BPD) in Iran, Mehr reported; origin of the explosion is not known.

- Bahrain sounds missile alert hours after the US and Iran ceasefire agreement, according to AP.

- N12 noted reported of explosion in Kermanshah northwestern Iran.

- IDF said it identified missiles launched from Iran towards Israel.

- Iran's Supreme Security Council said fingers are on the trigger and as soon as the enemy makes the slightest mistake, it will be answered with full force.

- Maritime Shipping Data shows traffic in the Strait of Hormuz remains light and limited, Arab News reported.

CRYPTO

- Bitcoin nears USD 72k after being supported by the constructive risk mood.

APAC TRADE

- APAC stocks rallied with markets euphoric and relieved after US President Trump announced a two-week ceasefire between the US and Iran in the final hours before his Tuesday evening deadline. The ceasefire was proposed by Pakistan and is subject to the opening of the Strait of Hormuz, which Iran was said to have agreed to, while the US and Iran are set to conduct talks on Friday in Islamabad. Furthermore, Israel and Lebanon were reported to be part of the ceasefire, although Israeli PM Netanyahu later denied that Lebanon was included.

- ASX 200 advanced with the gains led by outperformance in gold miners and tech, while energy was at the other end of the spectrum amid the slump in oil prices.

- Nikkei 225 rose above the 56,000 level with sentiment in Japan boosted by the lower oil prices, while participants also digested the firmer-than-expected wages data.

- Hang Seng and Shanghai Comp joined in on the widespread risk-on mood amid the US-Iran ceasefire and as Hong Kong participants returned to the market following a five-day closure.

NOTABLE APAC DATA RECAP

- Japanese Eco Watchers Survey Current (Mar) 42.2 vs. Exp. 47.9 (Prev. 48.9).

- Japanese Eco Watchers Survey Outlook (Mar) 38.7 (Prev. 50.0).

- Japanese Current Account (Feb) 3.933B vs. Exp. 3549B (Prev. 941.6B).

- Japanese Labour Cash Earnings (Feb) 3.3% vs Exp. 2.7% (Prev. 3.0%).

Loading...