Brent nears USD 110/bbl as Trump reignites Middle East tensions - Newsquawk US Market Open

- US President Trump said in his primetime address that the mission in Iran will be finished very fast and the US will hit Iran very hard over the next 2–3 weeks.

- Trump warned that the US will strike Iran’s electric plants if there is no deal and could also target its oil facilities.

- Energy surges as Brent nears USD 110/bbl; metals slump.

- Equities fall as Trump reignites tension with Iran, BAYN GY subject to potential 100% levy.

- DXY regains the 100 handle, CHF little-moved following inflation print.

- Fixed income under pressure as benchmarks continue to be driven by energy prices.

- Looking ahead, highlights include US Challenger Job Cuts (Mar), Initial Jobless Claims (Mar/28), Trade Balance (Feb), Canadian Trade Balance (Feb). Speakers include Fed's Logan & Bowman.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

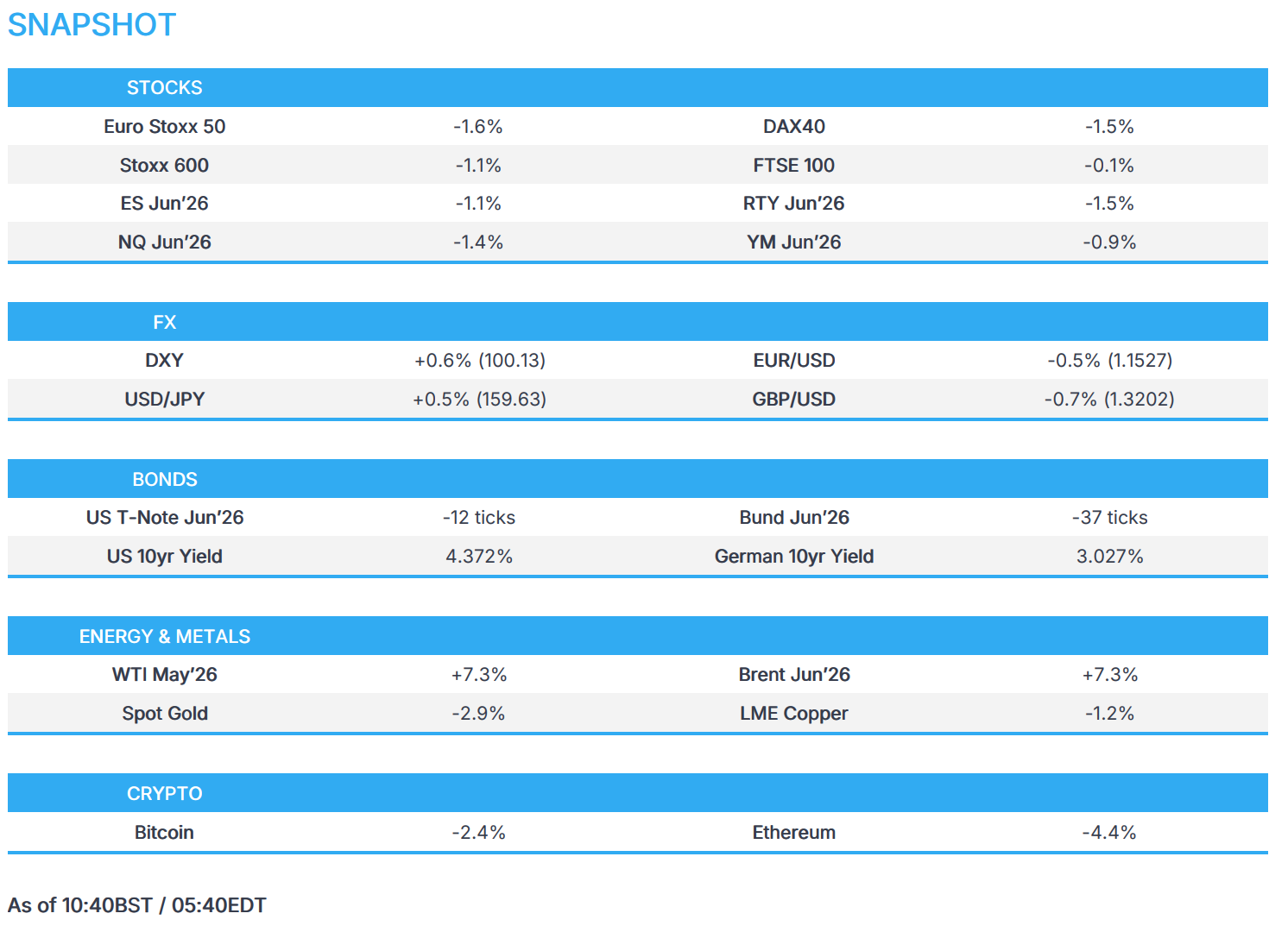

- European bourses (STOXX 600 -1.1%) began the session with decent losses after US President Trump's nationwide address reignited tensions. He said that the mission in Iran will be finished very fast and the US will hit Iran very hard over the next 2–3 weeks, while warning of strikes on electric plants if there is no deal and could also target its oil facilities. Since the start of cash trade, losses have pared back slightly but indices are holding around the -1% mark.

- European sectors are broadly in the red. Energy is the outperformer while Food, Beverage and Tobacco follow closely behind. Technology sits at the bottom of the pile, after performing well over the past 3 sessions, while Basic Resources also suffers as precious metals slip.

- US equity futures follow their European peers, with the ES losing the 6,600 handle that it regained in Wednesday's session.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is stronger this morning, with traders flocking back to the USD after US President Trump’s address dampened hopes of de-escalation with Iran. Overnight, he stated that he will hit Iran very hard over the next two to three weeks, adding that the US could also target Iran’s oil facilities. Trump's rhetoric has seemingly shifted from a focus on the timeline for wind-down to a more aggressive military escalation within that same window. DXY jumped back above the 100 mark, to currently trade at the upper end of a 99.44-100.17 range; recent levels above this include 100.64 (high from 31 Mar).

- Focus for today remains on any geopolitical updates, but that aside, there are a few important domestic data points to keep an eye on. Weekly initial jobless claims (212k expected from 210k) and continuing claims (1.84mln expected from 1.819mln), Revelio’s public labour statistics report, Challenger job cuts (90k expected in March from 48.3k) and international trade data are due. This all precedes the March NFP report on Good Friday, which is expected at 65k.

- G10s are all losing against the stronger USD; Antipodeans underperform, given the risk tone, whilst the Loonie fares a little better than peers, given it does not rely on external energy. GBP also sits right towards the foot of the G10 pile and is underperforming vs the EUR. A Wednesday rally in Gilts and traders believing the BoE may be slower vs the ECB in containing the energy shock may explain the slight underperformance between the two. This also comes after BoE Governor Bailey suggested earlier in the week that markets were getting ahead of themselves by pricing in rate hikes. Cable currently sits at the bottom end of a 1.3195-1.3320 range.

- CHF is also amongst the worst performers against the USD, but is incrementally losing against the EUR. Earlier, a cooler-than-expected (but stronger-than-prior) Swiss inflation report spurred some modest pressure in the Franc, before then reversing soon after. In a bit more detail, headline Y/Y printed at 0.3% (exp. 0.6%, prev. 0.1%); M/M 0.2% (exp. 0.5%). Much of the upside was facilitated by stronger energy prices, leading inflation to the strongest in over a year, and back away from the lower end of the SNB’s 0-2% target. For the time being, this will help alleviate fears at the Bank of bringing back negative interest rates, though policymakers have long reiterated that there is a high bar for such a move.

FIXED INCOME

- A bearish start to the day as US President Trump's primetime address reignited geopolitical tensions (recap on the feed, 07:35BST), lifting energy and in turn fanning the inflationary flame.

- Specifically, USTs dropped from 111-02 pre-Trump to a 110-24 knee-jerk low and have since hit a 110-16 trough. Lifting yields across the curve, 10yr to a 4.38% peak, though shy of Monday's 4.42% WTD peak. Similarly, the 2yr to a 3.86% peak, but shy of Monday's 3.89% WTD best. Action that has seen the implied magnitude of near-term tightening tick up by just under a bp worth. Geopols aside, Challenge Jobs, claims and import/export data; Fed speak is also due.

- EGBs and Gilts, in line with the above bearishness, Bunds hit a 125.19 trough with losses of 51 ticks at most, while Gilts got to a 87.85 low, with downside of 75 ticks. Since, they have bounced by around 20 ticks from extremes, but remain firmly in the red.

- The European docket is a light one; action will continue to be dictated by energy movements and associated inflation/central bank expectations from it. For the ECB and BoE, markets continue to price in 60bps and 41bps of 2026 tightening, respectively. Despite the recent inflation print from the EZ not yet showing second round effects, and despite Bailey pushing back on market pricing this week.

- France sold EUR 12.5bln vs exp. EUR 10.5-12.5bln 3.00% 2034, 3.50% 2035, 0.50% 2044 and 2.00% 2048 OAT.

- Japan sold JPY 1.97tln 10yr JGBs, b/c 2.57x (prev. 3.30x), average yield 2.350% (prev. 2.122%).

COMMODITIES

- In geopolitics, President Trump’s address largely repeated recent messaging on the Middle East, offering little fresh clarity on a path to de-escalation. That being said, Trump's rhetoric has seemingly shifted from a focus on the timeline for wind-down to a more aggressive military escalation within that same window. On March 31st, Trump claimed the US could "leave" Iran within "two or three weeks" because the mission to prevent a nuclear weapon had been "attained." He framed the upcoming period as "finishing the job," asserting that the US would exit regardless of whether a formal deal was reached. On April 1st, in his televised address, he paired the same timeframe with a promise of violence, stating the US would hit Iran "extremely hard" over the next two to three weeks and bring them back to the "Stone Ages".

- WTI and Brent futures have surged after US President Trump’s televised address, which dampened hopes of a near-term end to the conflict. Brent Jun’26 currently eyes USD 109/bbl to the upside (USD 99.08-108.97/bbl range) while WTI May’26 sits around USD 107/bbl (USD 97.50-107.38/bbl range). Meanwhile, European diesel futures hit USD 200/bbl as the Iranian war curbs supply. Dutch TTF is +3.5% at the time of writing, but off its best levels, with some citing forecasts of milder weather as a drag on prices despite the ongoing geopolitics. Analysts at ING suggest that “even if shipping through the Strait of Hormuz resumes, a return to pre‑war market conditions is likely to be slow, as upstream production restarts, logistics normalisation and inventory rebuilding will take time.”

- Spot gold reversed an earlier gain after Trump’s speech offered little clarity on how the war might end. The bullion entered the European day around USD 4,600/oz after trading above USD 4,800/oz earlier in the APAC session. Spot silver briefly dipped under USD 70/oz before recovering to around USD 71.50/oz, but well off its earlier high of USD 76.42/oz.

- Industrial metals also fell after Trump repeated that the US could strike Iran “extremely hard” and target its power plants if talks fail. 3M LME copper fell under USD 12,500/t but found support at USD 12,250/t. Elsewhere, the WSJ reported Trump is expected to overhaul US steel and aluminium tariffs, with finished goods made from imported metals potentially facing a 25% duty, while the administration is also preparing tariffs on drugmakers, possibly from Thursday, that have not agreed to guarantee low US prices.

- South Korea's Blue House denies the report regarding considering fees on passing through Hormuz. This comes following earlier reports that South Korea is reportedly considering whether to pay Iran to bring in Middle Eastern oil and gas.

- The 8 members of the OPEC+ group still plan to hold their virtual meeting on the 5th of April, according to Kpler's Bakr.

- China has reportedly asked private refiners to maintain fuel output at all costs.

- Russia imposes ban on gasoline exports for producers until the end of July, IFX reported.

- Kpler's Bakr posted "At this point and under the most optimistic scenario Hormuz will remain shut till May. Now brace for impact."

- Iraq's oil ministry said it has began exporting oil through Syria.

- Reconstructing Iran's Khuzestan steel factory will take between 6-12 months, Mizan news reported.

- New Zealand associate energy minister said will enter into an agreement to support an additional 90mln litres of storage for diesel at Marsden Point in Northland.

- Colonial pipeline is reportedly down due to damage in Georgia.

- Venezuela's oil exports in March surpassed 1mln bpd for the first time n six months, according to shipping data.

TRADE/TARIFFS

- US President Trump's administration is readying to impose tariffs of 100% on certain medicines as it pushes pharmaceutical companies to manufacture more in the US, according to FT.

- US President Trump is expected to overhaul steel and aluminium tariffs, while altered rates on finished products would simplify compliance, but could increase costs for many imports, according to WSJ. Plans to alter tariff duties to 25% on the entire value of finished products. 50% tariff will remain for commodity-grade steel and aluminium products. Executive order could come as early as this week.

- China's MOFCOM said they are to enhance communications with the US on trade.

- The EU is discussing setting up digital tech dialogue with the US and reiterates that digital legislation is not up for negotiation.

NOTABLE EUROPEAN DATA RECAP

- Swiss Inflation Rate YoY (Mar) Y/Y 0.3% vs. Exp. 0.6% (Prev. 0.1%, Low. 0.1%, High. 1.0%); Core 0.4% (prev. 0.4%).

- Swiss Inflation Rate MoM (Mar) M/M 0.2% vs. Exp. 0.5% (Prev. 0.6%, Low. 0.2%, High. 0.9%).

CENTRAL BANKS

- ECB's Panetta said leading indicators are pointing towards a slowdown in the economy; tensions in energy markets are a cause for concern not only for the immediate impact, but also on growth. Non-bank financial intermediaries in some sectors show levels of leverage and liquidity which could prove inadequate during periods of acute stress.

- ECB Economic Bulletin Issue 2, 2026: The risks to the growth outlook are tilted to the downside, especially in the near term.

- ECB's Simkus said caution is needed on rates and it is too early to say what is needed at the April meeting.

- BoE DMP (Mar): 1yr ahead CPI expectation 3.5% (prev. 3.00%), 3yr ahead CPI expectation 2.7% (prev. 2.8%).

NOTABLE US HEADLINES

- Canadian PM said he spoke with US President Trump this evening to discuss Artemis II and the Middle East conflict.

- US President Trump discussed firing Attorney General Pam Bondi and replacing Bondi with EPA Chief Zeldin, although he has not yet made a decision whether to fire Bondi, according to NYT.

- US Senate may vote on DHS funding bill on Thursday, while the bill would fund DHS without ICE and CBP, according to NBC.

GEOPOLITICS

MIDDLE EAST

- US President Trump said in his primetime address that Iran's navy is gone and its air force is in ruins, while he noted most of Iran’s leaders are dead, and its ability to launch missiles and drones has been curtailed. Trump stated they will never allow Iran to have a nuclear weapon and that US strategic objectives are nearing completion, as well as stated that the mission in Iran will be finished very fast and the US will hit Iran very hard over the next 2–3 weeks, and will bring Iran back to the stone ages, where they belong. Furthermore, he said countries reliant on Hormuz oil should take the lead and that Hormuz will reopen once the conflict ends, while he warned the US will strike Iran’s electric plants if there is no deal and could also target its oil facilities.

- US President Trump said strategic objectives are nearing completion, must complete mission in Iran and will finish the job very fast, adds Iran can never be trusted with nuclear weapons. US has plenty of gas. Countries that get oil via Hormuz must cherish it and must take the lead and suggests countries buy oil from the US. Hormuz will naturally open when conflict is over.

- US intelligence agencies assessed that Tehran is not currently willing to engage in substantial negotiations to end the conflict, while US intelligence agencies believe Iran's government thinks Trump is not serious about negotiations, according to NYT.

- US VP Vance is engaging with Pakistan mediators over Iran deal and passed a message to Iran via Pakistan on Tuesday, while US and Iran are discussing ceasefire for Hormuz reopening and Vance warned of increasing pressure without a deal, according to ABC.

- UAE reportedly preparing to help the US fight Iran and open the Strait of Hormuz by force after being repeatedly struck by Iranian drones and missiles since the war began, NY Post reported citing Arab officials.

- Senior Iran source said Tehran demands a guaranteed ceasefire to end war permanently and no talks have taken place via mediators for a temporary ceasefire, while intermediaries contacted Iran on Tuesday and discussions were about continuing diplomacy.

- Iran's military spokesperson said bigger, wider and more damaging attacks are coming soon, Tasnim reported.

- Iranian President Pezeshkian said attacking Iran’s vital infrastructure shows an inability to achieve a sustainable solution, IRNA reported.

- Faytuks Network posted on X citing Fox News that "Trump’s speech tonight will inform the public that we may require the use of ground troops to round up uranium in Iran" - UNCONFIRMED. This was later deleted.

- Israeli sources say they have not been given the green light from the US yet for Israel to target infrastructure in Lebanon, Al Hadath reported.

- US Embassy in Baghdad has told US citizens to leave Iraq with expectations of Iran-aligned militia to carry out attacks in central Baghdad within 24-48 hours.

- Iran Supreme Leader's advisor, Kamal Kharazi, was reportedly injured in US-Israeli attack on Tehran.

- Iran's atomic energy agency said US-Israeli attacks against facilities under IAEA supervision are a 'war crime'.

- Reports of strong explosions in proximity to US bases in Kuwait, N12 reported.

- Pakistan foreign ministry spokesperson said there is no confirmation so far of any US delegation arriving for talks.

- Explosion reported in Kuwait; explosions are caused by an attack on American positions, Mehr and Fars News report.

OTHERS

- US lifted sanctions on Venezuela’s acting president Delcy Rodríguez.

CRYPTO

- Bitcoin slips below USD 67k as global risk tone sours on a lack of geopolitical de-escalation.

APAC TRADE

- APAC stocks failed to sustain initial gains after US President Trump's primetime address disappointed those hoping for an immediate de-escalation in the Iran conflict, in which he said they will hit Iran very hard over the next 2-3 weeks and will 'bring Iran back to the stone age, where they belong', while he also threatened to hit Iran's electric plants if there is no deal and could hit their oil.

- ASX 200 reversed early gains as Trump's remarks soured the broad risk sentiment, and with the declines led by weakness in the tech, mining, materials and resources industries, while the latest trade data from Australia had very little influence on price action.

- Nikkei 225 wiped out the initial spoils and slumped beneath the 53,000 level as US President Trump's remarks triggered a broad risk-off mood and lifted oil prices.

- Hang Seng and Shanghai Comp were subdued amid notable weakness in the Hong Kong-listed blue chip tech stocks, and with the mainland also dampened following another paltry liquidity operation by the PBoC.

NOTABLE ASIA-PAC HEADLINES

- South Korean Vice Finance Minister said they are closely monitoring FX market as speculative trading is being seen; to respond sternly to excessive herd-like behaviour FX markets.

- Magnitude 7.8 earthquake strikes 119km WNW of Ternate, Indonesia, according to the USGS.

- EMSC announces a tsunami alert after earthquake in Indonesia region.

NOTABLE APAC DATA RECAP

- South Korean Inflation Rate YoY (Mar) Y/Y 2.2% vs. Exp. 2.4% (Prev. 2%).

- South Korean Inflation Rate MoM (Mar) M/M 0.3% vs. Exp. 0.6% (Prev. 0.3%).

- Australian Balance of Trade (Feb) 5.686B vs. Exp. 2.5B (Prev. 2.631B, Low. 1.5B, High. 3.0B).

- Australian Exports MoM (Feb) M/M 4.9% (Prev. -0.9%).

- Australian Imports MoM (Feb) M/M -3.2% (Prev. 0.8%).

Loading...