Crude above USD 100/bbl as Trump threatens Hormuz blockade, though reports suggest US-Iran talks to continue - Newsquawk US Market Open

- The US delegation left US-Iran talks in Pakistan without an agreement after 21 hours of talks. As a response, US President Trump said the US Navy will begin the process of blockading any and all ships trying to enter or leave the Strait of Hormuz, effective 10:00EDT/15:00BST.

- Pakistani, Egyptian and Turkish mediators will continue talks with the US and Iran in the coming days, aiming to help close the gaps between US-Iran, Axios reported citing sources. All parties believe a deal is possible.

- Energy spikes, Brent returns above USD 100/bbl as Trump threatens Hormuz blockade.

- European bourses weaker but off worst levels, LHA GY suffer from another strike; US equity futures in the red.

- DXY firmer on haven demand, HUF surges on Tisza supermajority.

- Global fixed income hit as energy surges; busy speaker slate ahead.

- Looking ahead, highlights include US Existing Home Sales (Mar), OPEC MOMR (Apr). Speakers include ECB's de Guindos, RBA's Hauser & Fed's Miran. Earnings from Goldman Sachs & LVMH.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US delegation led by Vice President Vance left US-Iran talks in Pakistan to return to the US without an agreement after 21 hours of talks, while Vance said the US had sought an affirmative commitment Iran would not seek a nuclear weapon or tools to quickly achieve one, and the US left behind a “final and best offer”. Iranian Foreign Ministry spokesperson Baqaei said any success depended on the US refraining from excessive demands and unlawful requests, and negotiating with seriousness and good faith, while an Iranian report noted there was disagreement on several issues and that the Americans demanded through negotiations what they could not obtain through war.

- US President Trump said the US Navy will begin the process of blockading any and all ships trying to enter or leave the Strait of Hormuz, while he stated that the meeting went well and most points were agreed to, apart from nuclear, which was the only point that mattered. Trump also stated that at some point, we will reach an “ALL BEING ALLOWED TO GO IN, ALL BEING ALLOWED TO GO OUT” basis, but Iran has not allowed that by saying there may be mines somewhere, which is world extortion, and leaders of world countries, especially the US, will never be extorted. Furthermore, he said at an appropriate moment, the US is fully locked and loaded, and the military will finish up the little that is left of Iran, and warned that any Iranians who fire at the US or at peaceful vessels will be blown to hell.

- US Central Command said it will begin implementing a blockade on all maritime traffic entering and leaving Iranian ports on April 13th at 17:00 Israeli time (15:00BST/10:00EDT), although it would "not impede" vessels transiting the Strait of Hormuz travelling to or from non-Iranian ports. US President Trump later posted that "The United States to Blockade Ships Entering or Exiting Iranian Ports on April 13 at 10:00 A.M. ET."

- US President Trump and his advisers are weighing resuming limited strikes in Iran, in addition to the US blockade, to break the stalemate in peace talks, according to WSJ citing officials and people familiar with the situation. However, it was also reported that Trump is said to remain open to a diplomatic solution.

- Pakistani, Egyptian and Turkish mediators will continue talks with the US and Iran in the coming days, aiming to help close the gaps between US-Iran, Axios reported citing sources; all parties believe a deal is possible. This follows on from earlier reports by Pakistani press stating that Pakistani officials are continuing efforts to convince the US delegation to return to talks; talks took place in a positive atmosphere, indicating both sides are interested in continuing dialogue.

- White House outlined the red lines it said Iran refused to agree onaccording to an official cited by CNN. Red lines included ending all of its uranium enrichment, dismantling its major nuclear enrichment facilities, retrieving the more than 400 kilograms of highly enriched uranium believed to be buried underground, accepting a broader “peace, security and de-escalation framework” that includes regional allies, ending funding for terrorist proxy groups Hamas, Hezbollah and the Houthis, fully opening the Strait of Hormuz, and charging no tolls for passage.

- Iran's Foreign Minister posted "In intensive talks at highest level in 47 years, Iran engaged with U.S in good faith to end war. But when just inches away from "Islamabad MoU", we encountered maximalism, shifting goalposts, and blockade".

- Iranian armed forces say if Iran’s ports are threatened, then "no port in the Persian Gulf and Oman Sea will be safe", IRIB News reported.

- Iranian National Security Commission Spokesman said US blockade claim is a bluff, ISNA reported.

- IDF troops are expanding targeted ground operations against Hezbollah infrastructure in the Bint Jbeil area of southern Lebanon to strengthen forward defence. The statement said troops killed more than 100 Hezbollah fighters, dismantled dozens of infrastructure sites and found hundreds of weapons in the area.

- Tasnim Agency reported, citing sources, US President Trump will lose the Bab al-Mandab Strait should he decide to take action against the Strait of Hormuz.

- IRGC warns the approach of military vessels toward the Strait of Hormuz is a breach of the ceasefire, IRNA reported.

- Israeli forces carry out two airstrikes near Choukine in southern Lebanon.

- IDF defines Lebanon as the main arena at this stage, while Iran is defined as an "arena of readiness" – with high alertness for any development.

- Israel has decided to establish 15 permanent camps along the front line of the Lebanese villages, Al Jazeera reported, citing Channel 12.

- Israel reportedly conducts raid targeting Beyout Al-Siyad in southern Lebanon.

- Sirens sound in Kiryat Shmona, Northern Israel, according to SNN, while Tasnim also reported that Hezbollah is conducting missile attacks on Israeli towns.

- French President Macron said France and the UK will organise a conference in coming days aimed at restoring freedom of navigation in Hormuz. Macron said any Hormuz naval mission would be strictly defensive and stressed that every effort must be made to reach a lasting, solid diplomatic end to the Middle East conflict. He also reiterated the importance of finding a way to restore peace in Lebanon.

EUROPEAN TRADE

EQUITIES

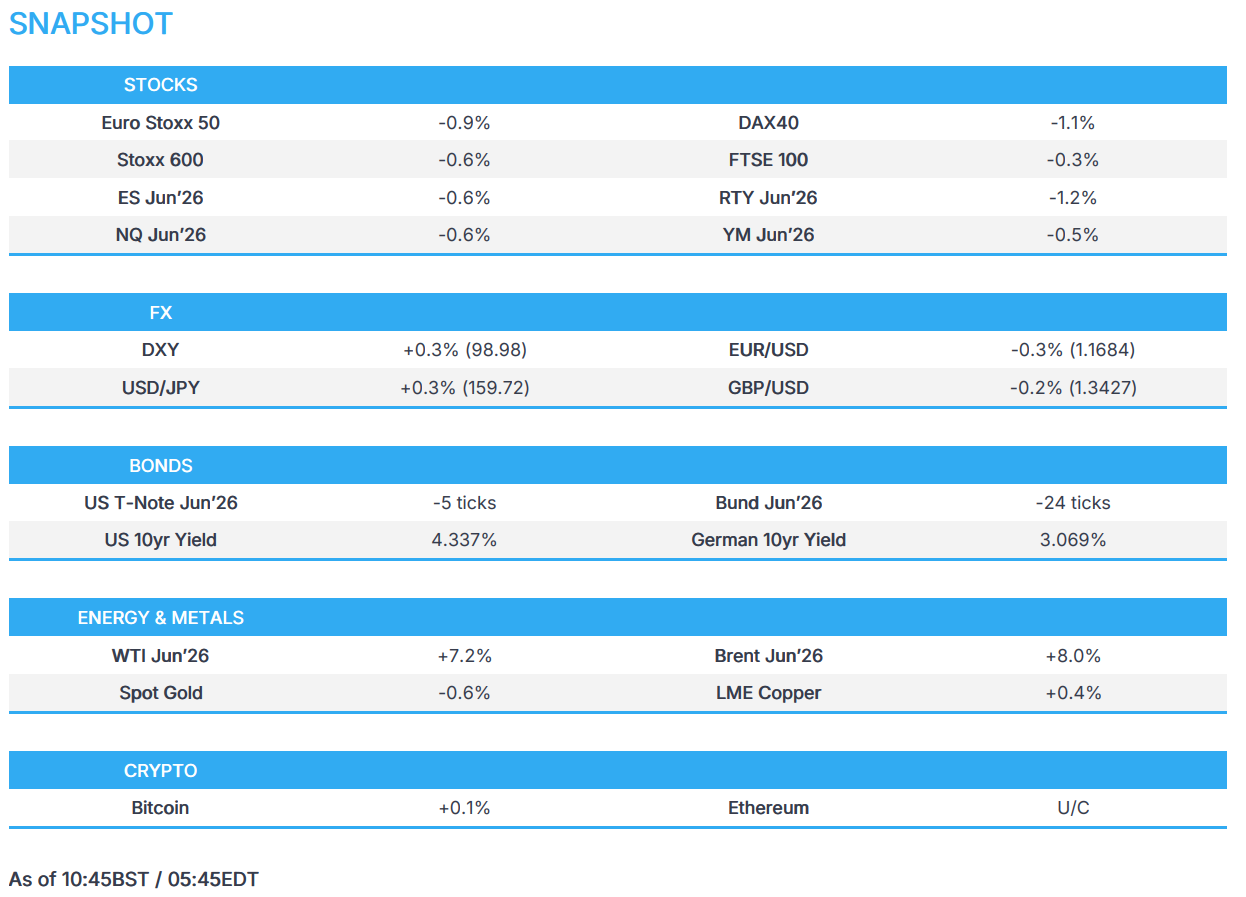

- European bourses (STOXX 600 -0.6%) have started the week on the backfoot, following talks between the US and Iran resulting in no agreement. US President Trump, in response, stated that the US Navy is to begin the process of blockading any and all ships trying to enter or leave the Strait of Hormuz, causing crude futures to surge. The DAX 40 is the underperformer, while the FTSE 100 is supported. Elsewhere, Hungary’s BUX index is surging following Peter Magyar’s Tisza party secured a supermajority.

- European sectors point negatively, with all sectors in the red, except Energy. Cyclical sectors continue to be hit the hardest, with Travel & Leisure and Consumer Products & Services lying at the bottom of the pile. To add, SocGen downgraded multiple airlines (Ryanair, easyJet, Wizzair) as a result of the higher energy prices hitting the sector.

- US equity futures have followed its peers but have come off worst levels. In pre-market trade Sandisk (+1.9%) moves higher, with the Co. set to join the Nasdaq 100.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX markets are displaying a slight risk-off bias. A somewhat calm move in currency markets follows the conclusion of US-Iran talks without an agreement on the nuclear issue; however, both sides framed negotiations as positive and recent Qatari reporting suggests Pakistani officials are continuing efforts to bring both sides back to the negotiating table, each reportedly interested in continuing dialogue.

- DXY trades without conviction on either side of a 99.00 handle. The buck looks towards a heavy week of Fed speak, alongside PPI data on Tuesday. On the docket today, uber-dove Miran is set to speak on "Building the Financial System."

- HUF benefits from the election of the opposition Tisza’s Magyar. Preliminary results, based on more than 98% of counted votes, put Magyar on course for 138 seats (supermajority 133 seats). Although markets had already priced in a Magyar victory, a supermajority will catapult the incoming PM's bid to fast track various HUF-positive pledges (See Newsquawk Analysis on the headline feed). As such, EUR/HUF surpassed April 2022 lows, marking a session low of 364.02.

- NZD remains the most resilient in the face of energy prices as markets move to price in 82bps of hikes by year-end, an increase of c. 7bps from Friday. Kiwi trades just off highs, after facing resistance at the 0.5840 mark.

FIXED INCOME

- Global fixed benchmarks are entirely in the red this morning, with energy prices once again surging after the US-Iran peace talks in Pakistan ended without an agreement. Following this, US President Trump said the US Navy will begin the process of blockading any and all ships trying to enter or leave the Strait of Hormuz – this is expected to begin at 15:00 BST / 10:00 EDT.

- USTs currently trade lower by a handful of ticks, and are currently trading at the mid-point of a 110-22+ to 111-00 range. European trade has seen US paper edge off worst levels, potentially as traders digest reports of the possibility of further talks, and as the ceasefire remains for now. Geopols aside, US existing home sales for March is due later, with Fed’s Miran also on the docket.

- Bunds and Gilts have also been pressured, with some underperformance in Gilts, which are lower by around 50 ticks (vs Bunds -24 ticks). Both, as with USTs, are off worst levels. As above, Gilts and Bunds are moving at the whim of geopolitical developments, given the regions’ net-importer of oil statuses. Homing in on Germany, earlier today, the Merz coalition agreed on measures worth EUR 1.6bln to ease the impact of surging energy prices on the German consumer.

- From a yield perspective, the German 2yr has jumped back towards 2.637% (vs Friday close at 2.588%). The 2-year BTP-Bund spread has widened ever so slightly vs Friday’s close, but remains well off the peaks from the heights of the Iran war. Commerzbank’s rate strategist Siemssen said “we would probably need to see a more significant escalation for BTP-Bund spreads to test the March highs again”, adding that “BTPs should also underperform OATs again this week as they are more susceptible to energy prices”.

COMMODITIES

- US-Iran peace talks over the weekend collapsed, and Washington announced a naval blockade of the Strait of Hormuz, effective 10:00EDT/15:00BST on Monday, applying to all vessels entering or departing Iranian ports. Trump and his advisers are also weighing limited military strikes against Iran, though a full bombing campaign is considered less likely. Iran’s military adviser said Tehran “will not allow” the embargo. (full Newsquawk Analysis on the feed).

- Brent surged above USD 100/bbl, with some analysts forecasting prices could rise to USD 150/bbl if the blockade proceeds along the waterway, which carried around one-fifth of global oil and LNG before the conflict. Brent Jun resides in a current USD 100.94-103.87/bbl range and WTI Jun in a USD 93.58-96.93/bbl parameter. Dutch TTF futures jumped above EUR 51.30/MWh before paring gains, with Bloomberg noting the contract’s trading day was extended to 21 hours from 10. The May and June contracts currently reside sub-EUR 50/MWh.

- Spot gold fell below USD 4,650/oz before paring losses, and currently trades around USD 4,725/oz, pressured by a stronger USD and fears of central bank rate increases. Spot gold resides in a USD 4,644-4,740/oz range at the time of writing.

- Copper fell, and aluminium spiked, with metals broadly facing weaker demand risks as soaring energy prices weigh on the global economy. 3M LME copper oscillates in a USD 12,684.63- 12,920.23/t range at the time of writing.

- CPC’s oil exports rose 48% in March from February to 1.58mln bpd, boosted by recovery at the Tengiz field, according to sources cited by Reuters. CPC exports boosted by Tengiz field recovery.

- German Government to reduce energy tax on diesel and petrol by EUR 0.17/L for two months. Employers may provide employees with tax-free bonus of EUR 1000 as part of tax reform. Income tax reform will be adopted in January.

- Kuwait raises May crude prices for Asia, according to pricing document.

- Saudi Aramco's crude sales to China is set to half next month to around 20mln barrels, Bloomberg reported citing sources.

TRADE/TARIFFS

- Japan Post (6178 JT) to resume accepting all US-bound mail from Tuesday, after 7-month suspension due to end of ‘de minimis’ exemption, according to a statement.

- China Foreign Ministry, on Trump threatening tariffs if China supplies weapons to Iran, said trade wars have no winners.

- China is to remove tariffs on all products imported from 53 African nations starting May 1st, according to Caixin.

- India is to relax market access for European-standard medical devices.

NOTABLE EUROPEAN HEADLINES

- Peter Magyer's Tisza party wins the Hungarian election with a supermajority. Preliminary results, based on more than 98% of counted votes thus far, put Peter Magyar on course for 138 seats, exceeding the 133 seats needed for supermajority.

- German Finance Minister Klingbeil said tobacco tax is to be increased in 2026 as counter-financing measure for tax relief bonus.

- German CSU Leader Soeder said that it is right to tax excess profits from mineral oil companies at the European level.

- Spanish PM Sanchez said Spain wants to cooperate with China in all areas.

CENTRAL BANKS

- BoJ Governor Ueda said Japan's economy is recovering moderately but with some weakness; said the economy and prices are moving roughly in line with BoJ forecasts; underlying inflation is gradually accelerating towards the BoJ's target.

- ANZ revises outlook for RBNZ rate hikes in which it now sees hikes in July, September and October.

GEOPOLITICS

OTHERS

- Taiwan will carry out new drills in coming weeks to ensure the island has access to vital supplies in the event of a Chinese blockade.

CRYPTO

- Bitcoin trades either side of USD 71k, while Ethereum oscillates around USD 2k.

APAC TRADE

- APAC stocks declined after the negotiations marathon over the weekend between the US and Iran in Pakistan ended without an agreement, as the sides remained at loggerheads over Iran's nuclear ambitions. Furthermore, US President Trump announced a US naval blockade on ships travelling through the Strait of Hormuz, while the US military said it would start a blockade of Iranian ports on Monday at 10:00EDT/15:00BST, but would "not impede" vessels transiting the Strait of Hormuz travelling to or from other countries.

- ASX 200 was dragged lower by underperformance in tech and miners, while energy was at the other end of the spectrum following a surge in oil prices.

- Nikkei 225 retreated amid headwinds from the higher energy prices, which weighed heavily on power companies and large manufacturers, while there were also recent suggestions from Japan's economy minister that BoJ policy to boost the yen could be an option to curb inflation.

- Hang Seng and Shanghai Comp followed suit to the losses in regional peers, with sentiment not helped by another meagre PBoC liquidity operation and with a mixed performance seen in tech stocks.

NOTABLE APAC DATA RECAP

- Chinese Total Social Financing (Mar) 5230B vs. Exp. 5400B (Prev. 2380B).

- Chinese Outstanding Loan Growth YoY (Mar) Y/Y 5.7% vs. Exp. 5.9% (Prev. 6.0%).

- Chinese New Yuan Loans (Mar) 2990B vs. Exp. 3400B (Prev. 900B).

- Chinese M2 Money Supply YoY (Mar) Y/Y 8.5% vs. Exp. 8.9% (Prev. 9%).

- New Zealand Services NZ PSI (Mar) 46.0 (Prev. 48, Rev. 47.6).

- New Zealand Composite NZ PCI (Mar) 48.8 (Prev. 50.5).

Loading...