Crude benchmarks hit on Mehr MoU reporting, equities bid into SPCX debut - Newsquawk US Market Open

- Iran's Mehr News reports that the US-Iran MoU includes the reopening of the Strait of Hormuz, lifting oil sanctions, and releasing frozen Iranian funds. The draft is still being reviewed. Brent -4.1%.

- The US and Iran deal signing could occur around the June G7 meeting in Geneva (June 15th - 17th).

- Global equities gain on the constructive risk tone, SPCX set to debut today.

- DXY rangebound, EUR holds above 1.1580 despite somewhat conflicting ECB reports.

- Fixed income benchmarks benefit from the softer energy prices.

- Looking ahead, highlights include Canadian Wholesale Sales (Apr), US UoM Prelim. (Jun) & SpaceX Debut.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- Iranian media Mehr News reported that the US-Iran 14-point MoU includes a US commitment to lift sanctions, withdraw its forces from around Iran, lift the naval blockade, reopen the Strait of Hormuz, lift oil sanctions, and release frozen Iranian funds; nuclear issue pushed back by 60 days for final agreement. Additionally, the US is required to present a plan to rebuild Iran’s economy, while the final negotiations between the two countries should focus on nuclear and economic issues, without discussing Iran’s missile program. This text still needs to be reviewed and finalized by the relevant institutions in Iran. [Click here for the full 14-point MoU]

- The US-Iran MoU is likely to be signed next week, according to CBS citing sources, with Bloomberg later reporting that it could happen at the G7 meeting in Geneva next week. First steps include ensuring "freedom of trade" by demining and opening the Strait of Hormuz. The signing would kick off 60 days of talks to negotiate details. In principle, Iran would commit to a lockout of 15-20 years during which it would not enrich uranium and would dismantle its nuclear sites. In exchange for taking these steps, Iran would receive financial relief staggered over time and sequenced to correspond with compliance.

- US President Trump said he understands that Iran’s Supreme Leader has approved the deal and that lifting the blockade is part of the Iran deal, while he added that Iran will not have a nuclear weapon and that they want to make a deal a lot more than he does. Trump added it's a very strong MOU, they found Iran to be rational, and they will make a deal. Furthermore, he said the Strait will open immediately upon MOU signing, maybe Saturday or Monday, but doesn't want to set a deadline for the deal, and stated a Kharg Island deal would be off the table now.

- US President Trump said at a virtual campaign rally that they settled up with Iran and it is pretty much completed, while they got everything they wanted and claimed they ended the war with Iran.

- Israeli PM Netanyahu held a call with US President Trump on Thursday night regarding the possibility of a pending peace deal between the US and Iran, according to CBS News.

- Airplanes associated with US VP Vance's advance team are moving ahead of potential Iran MoU signing, according to New York Post reporter.

- Iran state media said Tehran would not cede control of Hormuz under draft US deal, AFP reported.

- Iranian Foreign Ministry spokesperson said the issues raised about the agreement are speculation and the issue has not been finalised, while it added that the situation in the Strait of Hormuz is less secure due to US actions and that what is being said about the time and place of signing the agreement is media speculation. Furthermore, the spokesperson said that Iran has so far not reached a final conclusion about the agreement, but stated that the text of the agreement is almost ready.

- Sources cited by Al Hadath said Iran has given final approval, which Qatar conveyed to the US.

- Iranian state media reported that explosions heard in Sirik was related to a confrontation with a vessel that violated regulations whilst attempting to pass through the Strait of Hormuz.

- Israeli airstrike reported in Jebchit, southern Lebanon, according to Al Araby.

EUROPEAN TRADE

EQUITIES

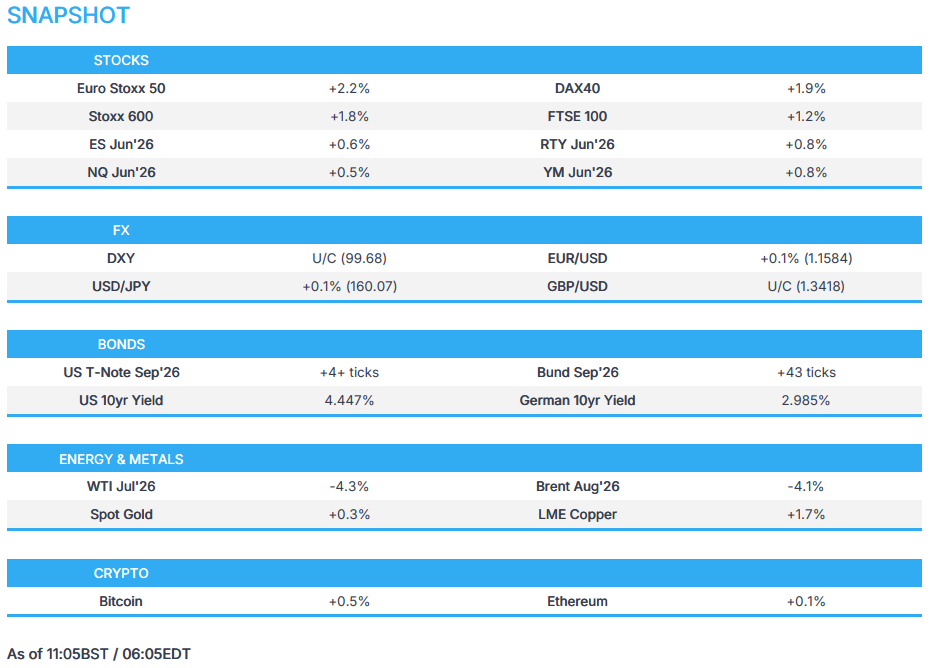

- European bourses (STOXX 600 +1.8%) start the last trading day of the week on a firmer footing and have completely reversed the losses seen at the start of the week. This comes on hopes of a US-Iran deal, with US President Trump stating that it could be signed as early as this weekend in Europe. Further upside was spurred after Mehr News reported that the MoU with the US includes reopening the Strait of Hormuz, lifting oil sanctions, and releasing frozen Iranian funds.

- European sectors are entirely in the green bar Energy (-3.1%). Travel & Leisure (+5.2%) is the clear outperformer, followed by Banks (+4.2%) and Consumer Products & Services (+3.7%). Cyclicals have been affected the most since the start of the Iran war, so hopes of an end would benefit these sectors the most.

- US equity futures hold onto Thursday's gains; NQ +0.5%. SpaceX is to begin trading today on the Nasdaq, after raising USD 75bln in the biggest IPO, passing Saudi Aramco's USD 25.6bln IPO back in 2019.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- Snapshot: DXY is incrementally firmer, whilst G10s mixed vs the USD this morning. The tentative action comes after US President Trump claimed that he had a deal with Iran, and that the signing of the MoU would probably happen in Europe. However, the Iranians pushed back on this claim. This morning, a Mehr report revealing the details of the 14-point plan garnered some attention, which helped boost global sentiment - though action was fairly muted in the FX space.

- DXY is slightly firmer today despite significantly lower oil prices after a number of geopolitical updates in the last 24 hours. (See commodities for more details). In recent trade, USD was hit as details of the 14-point US-Iran MoU accelerated the risk-on bias. On this reporting, DXY moved towards Thursday's lows of 99.58, currently 99.72 at the time of writing. Focus for the remainder of the day shifts to the UoM Sentiment survey, but market participants will likely be more attentive of the geopolitical environment and potentially some early positioning heading into a weekend which could see a deal between US-Iran be signed.

- EUR and GBP trade has chopped on either side of the unchanged mark this morning. The single currency has had a number of ECB speak to contend with, but by in-large has been largely in-fitting with President Lagarde’s comments on Thursday. A notable Bloomberg sources piece suggested that some policymakers could see a hike as soon as July. Elsewhere, the GBP had a weak growth report to digest – overall it does little to shift the mood heading into the next week’s meeting, but will exacerbate the growth woes had the Bank.

- NOK is the worst G10 performer on account of lower oil prices as participants assess implications for Terms of Trade and the Norges Bank. Popular carry trade NOK/SEK has seen downside in excess of a percent today due to the above. NOK/SEK slipped below par, to mark a session low of 0.9882.

FIXED INCOME

- Global fixed benchmarks are entirely in the green and currently hold towards highs. Strength, which has been facilitated by lower energy prices after US President Trump claimed that he had a deal with Iran, and that the signing of the MoU would probably happen in Europe. However, the Iranians pushed back on this claim. The bullish bias then extended after Iran-affiliated, Mehr News, reported the details of the US-Iran 14-point MoU. This spurred another bout of pressure in the energy complex, which in-turn weighed on global yields.

- USTs (+4+ ticks) gain, and hold at the upper end of a 109-19 to 109-29 range. Action which has been facilitated by the positive geopolitical mood music, but still remains the underperformer vs peers. That can potentially be explained by the ongoing hawkish repricing at the Fed, heading to the Bank’s policy announcement next week. Elsewhere, yields are lower across the curve with underperformance in the short-end/belly; the 10yr currently holds at 4.43%, marking the WTD low. Should the geopolitical environment materially improve in the coming days, and the Strait entirely opens up, the 10yr could dip its head back towards support levels at 4.33% and then 4.25%. Do note that the 10yr resided below the 4.00% mark before the Iran conflict started.

- Bunds (+43 ticks) and Gilts (+87 ticks) both follow the bullish bias, with the latter outperforming given its relatively high dependence on external energy and poor domestic growth data. For EGBs, there have been a number of ECB speakers this morning following the Bank’s decision to hike rates on Thursday. Most have echoed the comments made by President Lagarde at her presser; focus has been on a Bloomberg report, which suggested that some ECB members see another hike as soon as July.

- For UK paper, the GDP release this morning indicated that the UK economy shrank by 0.1% in April, amidst the Iranian war. This will only exacerbate growth woes for some policymakers at the BoE, where policymakers are set to meet next week, expected to keep rates on hold.

COMMODITIES

- On Thursday, US President Trump said a deal could be signed with Iran as soon as this weekend in Europe, following an earlier post on Truth Social that the US was going to strike Iran hard for the third straight day and then later pulling back the threat. Trump said VP Vance would attend if the deal materialises and added that the Iranian Supreme Leader had agreed to a deal. The deal was described as a very strong MoU which would restart shipping in the Strait and include commitments from Tehran to not pursue a nuclear weapon.

- Markets were awaiting any kind of confirmation from Iranian media that the MoU has been received. Mehr News reported the 14-point MoU includes the reopening of the Strait of Hormuz, lifting oil sanctions, and releasing frozen Iranian funds. (Full 14 points on the headline feed) Awaiting official commentary from the Iranian government on the MoU.

- Crude futures were already on the softer side before the Mehr news report, but it has given an additional catalyst for further downside. WTI Jul'26 slides below a key support range of USD 84.46-85.95/bbl, currently trading at the bottom of USD 83.20-86.98/bbl range. For Brent Aug'26, the benchmark trades slips below the USD 86/bbl handle (USD 85.80-89.72/bbl).

- Precious metals trade in narrow ranges after rebounding in excess of 3% in Thursday's session. Spot gold oscillates in a USD 4170-4247/oz range. Given the positive news of a potential US-Iran deal, worries of higher inflation/rates due to energy prices may temper and result in some unwinding of the hawkish rate bets by the Fed.

- 3M LME Copper bids higher, currently trading in a USD 13.6k-13.72k/t range, amid the positive tone. The red metal gapped higher alongside gains in Asia-Pac equities and held amid constructive reporting.

- Venezuela has signed five agreements with Shell (SHEL LN) to advance oil and gas projects, which includes the Co.'s participation in the 5tln cubic-feet Loran offshore gas field.

- JPMorgan still expects aluminium to reach USD 4k/t, now forecasting an average price of USD 3750/t in H2'26.

NOTABLE EUROPEAN HEADLINES

- Bundesbank sees German GDP growth at 0.5% in 2026, 0.8% in 2027; German inflation seen at 2.9% in 2026, 2.7% in 2027.

NOTABLE EUROPEAN DATA RECAP

- UK GDP MoM (Apr) M/M -0.1% vs. Exp. -0.1% (Prev. 0.3%, Low. -0.3%, High. 0.3%).

- UK GDP YoY (Apr) Y/Y 1.2% (Prev. 1.2%).

- UK Goods Trade Balance (Apr) -26.05B vs. Exp. -22.85B (Prev. -27.22B, Low. -26.8B, High. -21.3B).

- UK Industrial Production MoM (Apr) M/M 0.0% vs. Exp. 0.1% (Prev. -0.2%, Low. -0.2%, High. 0.5%).

- German HICP Final Y/Y 2.7% vs. Exp. 2.70% (Prev. 2.90%).

- German HICP Final M/M -0.1% vs. Exp. -0.10% (Prev. 0.50%).

- French HICP Final Y/Y 2.8% vs. Exp. 2.80% (Prev. 2.50%).

- French HICP Final M/M 0.1% vs. Exp. 0.10% (Prev. 1.20%).

- Spanish HICP Final Y/Y 3.6% vs. Exp. 3.60% (Prev. 3.50%).

- Spanish HICP Final M/M 0.1% vs. Exp. 0.10% (Prev. 0.70%).

CENTRAL BANKS

- ECB's Nagel said all policy options remain on the table for July while adding that the ECB is prepared to respond if required.

- ECB's Makhlouf said we need to get ahead of inflation and are seeing more broad-based inflation impact. It would be a mistake for us to do nothing.

- ECB's Kocher said the war's impact on price trends are increasingly clear and he does not expect inflation to match 2022 or 2023 levels. Will act decisively to ensure 2% mid-term target.

- ECB's Dolenc said the rate hike is just enough for now to follow the baseline, and they had a robust set of data to make a decision. Dolenc also stated that it is pretty obvious inflation will be higher and growth lower, while services inflation is stubborn and hard to fight.

NOTABLE US HEADLINES

- US Senate Banking Committee is weighing a markup of export control legislation, Punchbowl reported citing sources. It could tee up the bills for inclusion in the next annual defense policy package, no final decision has been made yet.

- US President Trump said regarding fertiliser prices, that they might look into federal aid, and are looking at doing some form of help.

- BofA weekly flow data shows USD 20.8bln into bonds (59th straight week of inflows), USD 2.5bln out of cash, USD 31.5bln into stocks, USD 0.7bln out of crypto (record inflows over 5 weeks), USD 2.3bln out of gold (4th straight week of outflows).

GEOPOLITICS

OTHER

- US plans to significantly cut fighter jets and warships for NATO operations in Europe, with the US to pull a third of fighter jets, according to the New York Times.

CRYPTO

- Bitcoin holds above USD 63k amid a constructive risk tone across markets.

APAC TRADE

- APAC stocks rallied following on from the gains on Wall St, after President Trump cancelled planned strikes on Iran and touted a US-Iran deal, which could be signed as soon as the weekend and would open the Strait of Hormuz, while Trump claimed the US ended the war with Iran and he understood that Iran’s Supreme Leader has approved the deal. However, Iran pushed back on this as a Foreign Ministry spokesperson stated the issues raised about the agreement are speculation and that Iran has so far not reached a final conclusion about the agreement, but acknowledged that the text of the deal was almost ready.

- ASX 200 climbed higher as outperformance in mining, materials and resources led the advances, while energy was pressured due to the drop in oil prices, and defensives also lagged amid the risk-on environment.

- Nikkei 225 surged at the open and briefly tested the 67,000 level, with the index helped by lower oil prices and with tech and mining stocks sitting comfortably among the list of biggest gainers.

- Hang Seng and Shanghai Comp joined in on the euphoria with mining stocks among the notable gainers, while Chow Tai Fook was front-running the advances after it reported record full-year profit.

NOTABLE ASIA-PAC HEADLINES

- China tells big banks to curb interbank loans to ease cash glut.

- Japanese Finance Minister Katayama said they are aiming to broaden retail JGB offerings and that retail Japanese government bonds remain unappreciated by households, while she stated that no impact is expected on the central bank policy meeting after BoJ Governor Ueda was hospitalised.

- India is willing to let fiscal gap widen to as much as 4.8% of GDP from a previous 4.3%, according to Bloomberg.

NOTABLE APAC DATA RECAP

- Japanese Industrial Production YoY Final (Apr) Y/Y 2.0% (Prev. 2.4%).

- Japanese Industrial Production MoM Final (Apr) M/M 0.5% vs. Exp. 0.8% (Prev. -0.4%).

Loading...