Crude extending ahead of OPEC+ and another round of nuclear talks next week; DXY steady going into US PPI - Newsquawk US Market Open

- PBoC announced it will cut the FX Risk Reserve Ratio for forward FX sales to 0% from 20%, effective March 2nd to promote FX market development and support corporate exchange rate risk management.

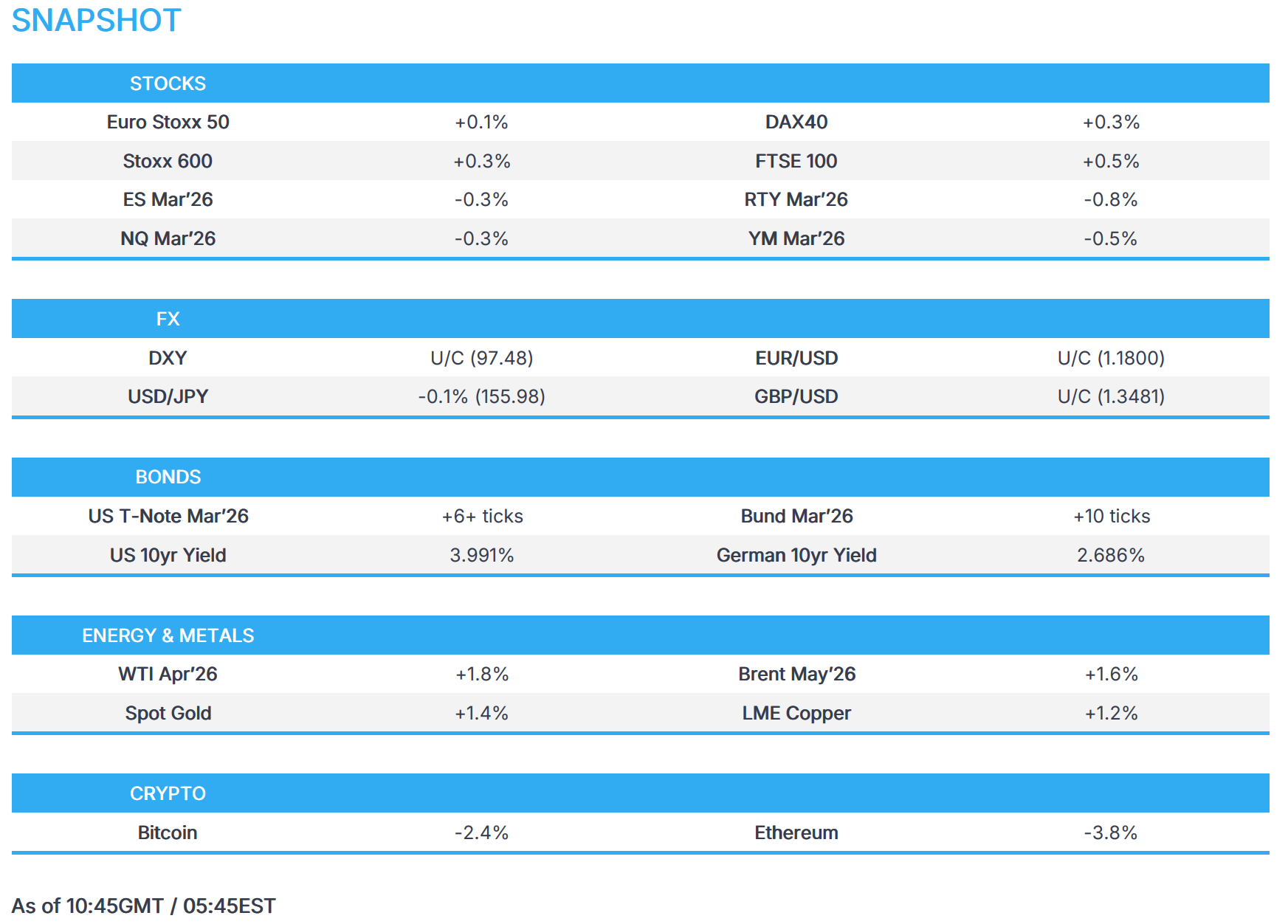

- European equities firmer, Telecoms lead following potential M&A; US equity futures lower in the continuation of Thursday's tech-led selloff.

- DXY is flat; G10s broadly firmer, ex-EUR and GBP.

- USTs mildly firmer, Bunds choppy after mixed regional inflation prints.

- Crude gains and awaits the next chapter of the US-Iran saga and the OPEC+ meeting; Metals shine ahead of US PPI.

- Looking ahead, highlights include German CPI (Feb), Canadian GDP (Jan), US PPI (Jan), Comments from BoE's Pill.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) are broadly firmer, with the SMI (+0.7%) the clear outperformer after Swiss Re (+3.6%) posted a 47% Y/Y rise in 2025 net profit while announcing a USD 500mln share buyback. Lagging behind its peers is the CAC 40 (-0.1%), with very company-specific news to drive the index.

- European sectors are mixed. Telecommunications (+1.3%) outperform after Spain's Cellnex (+0.6%) saw 2025 operating profit rise more than double annually and Telefonica (+3.7%) reportedly negotiating the purchase of 1&1 (+9.4%)in Germany in a EUR 5bln deal. On the flip side, Travel and Leisure (-1.8%) is underperforming despite positive IAG (-5.5%) earnings, in which the Co. beat FY profit expectations and announced a EUR 1.5bln share buyback.

- US equity futures (NQ -0.1%, ES -0.2%, RTY -0.7%) have held onto Thursday's losses, which were hit by losses in NVIDIA (closed -5.5%) and then Financials following the MFS exposure risk.

- BASF (BAS GY) Q4 2025 (EUR): Revenue 14.0bln (exp. 14.04bln), Net profit 560mln (exp. 285mln), EBITDA 1.03bln (prev. 1.43bln Y/Y), sees FY26 Adj. EBITDA between 6.2-7.0bln (exp. 7.22bln).

- Dell Technologies (DELL) - Q4 adj. EPS 3.89 (exp. 3.51), Q4 revenue USD 33.38bln (exp. 31.68bln). AI-optimised server orders USD 64bln, with a record AI backlog of USD 43bln. Increased dividend +20%, added USD 10bln to its share repurchase authorisation. Sees Q1 adj. EPS 2.90 (exp. 2.39), sees Q1 revenue between USD 34.7-35.7bln (exp. 29.07bln). For FY27, sees adj. EPS at 12.90 (exp. 9.95), sees FY27 revenue between USD 138.0-142.0bln (exp. 124.87bln), expecting AI revenue of USD 50bln and operating income growth of 18%. DELL shares +10.7% pre-market

- Netflix (NFLX) declines to raise its offer for Warner Brothers (WBD) and said the deal is no longer financially attractive.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is choppy but ultimately slightly softer following subdued APAC trade amid mixed sentiment, whilst the tone in Europe is tentative. Modest downticks in the index were seen as the EUR strengthened following the hotter-than-expected French CPI data (more below). Aside from that, newsflow in the European morning has been on the quieter side as USD traders gear up for US PPI data later in the session. DXY resides in a current 97.611-97.824 range at the time of writing, within Thursday’s 97.489-97.984 parameter.

- EUR/USD eked mild gains after oscillating around the 1.1800 focal point overnight, with a more convincing move above the level seen after the hotter-than-expected French and Spanish Prelim CPI metrics. EUR/USD resides in a 1.1789-1.1822 range awaiting the German Prelim CPI later today. The single currency then slipped to the unchanged mark after German state CPI metrics, where the Y/Y metrics generally showed a bit more cooling than what is forecasted for the mainland.

- GBP/USD languished near the 1.3500 level following the prior day's underperformance owing to credit concerns, and with overnight price action contained after UK GfK consumer confidence fell to its lowest level that was last seen in November. Overnight, UK journalists focused on the Gorton and Denton by-elections in which the Green party won, with Reform second and Labour third. With Labour losing a seat they held for almost 100 years, UK PM Starmer's leadership could be at risk. Nonetheless, GBP/USD saw little reaction to the results announcement, and currently resides in a 1.3461-1.3507 range, after finding support at its 200 DMA (1.3442) yesterday. Ahead, BoE’s Chief Economist Pill is due to give some remarks.

- USD/JPY retreated amid the early subdued risk appetite and following a slew of data, including Tokyo CPI, which printed firmer-than-expected across the board, but slowed from the previous with Core inflation back beneath the BoJ's price goal. The pair pared back some losses as the DXY recouped some overnight losses. USD/JPY trades in a 155.54-156.12 range vs yesterday’s 155.70-156.43 parameter.

- Antipodeans rebounded from the prior day's trough and narrowly outperform in the European morning, but with further upside contained by the mixed risk appetite and amid a weaker CNH, which was pressured after the PBoC actions to slow currency appreciation, in which it cut the FX risk reserve ratio to 0% and set a weaker-than-expected CNY fix by maintaining it at the prior day's level.

FIXED INCOME

- USTs are firmer by a handful of ticks this morning, and trades within a 113-16 to 113-19 range. Really not much driving things for the US paper this morning, and remains towards the prior day’s peaks. The upside in USTs on Thursday was facilitated by subdued risk appetite and a decent 7yr auction. Focus remains on the geopolitical situation, following US-Iran talks. Meetings have concluded, and whilst there have reportedly been some positive developments, uncertainty remains. Reports suggest that US President Trump is expected to convene senior advisers on Friday for detailed discussions on Iran and to decide on a course of action toward Tehran. Internal deliberations are said to be focused not on whether a strike would occur but on its scope and potential targets. Next up, US PPI.

- Bunds are incrementally firmer/flat, and currently reside within a 129.76 to 129.99 range. Initially held towards recent highs, but has since slipped towards the unchanged mark following the hotter-than-expected French/Spanish inflation metrics. Though the German State CPIs thereafter spurred some modest upticks in Bunds, given the Y/Y metrics generally showed a bit more cooling than what is forecasted for the mainland.

- Gilts are firmer by around 10 ticks, to currently trade near the upper end of a 93.00-93.30 range. Overnight, UK journalists focused on the Gorton and Denton by-elections in which the Green party won, with Reform second and Labour third. With Labour losing a seat they held for almost 100 years, UK PM Starmer's leadership could be at risk – which in theory would place pressure on UK-assets. This has not been reflected in price action this morning, though analysts at GS opined that the risk had already been priced in by markets.

- Japan sold JPY 2.15tln in 2-year JGBs; b/c 3.32x (prev. 3.88x); average yield 1.244% (prev. 1.253%).

- Australia sold AUD 800mln 2.75% November 2028 bonds, b/c 3.86, avg. yield 4.1849%.

COMMODITIES

- WTI Apr’26 and Brent May’26 futures are firmer within USD 64.85-65.90/bbl and USD 70.42-71.49/bbl intraday ranges thus far, respectively. Gains follow yesterday’s US-Iran negotiations, which ultimately failed to reach an accord, but the sides agreed to continue technical talks. Mediators reported "unprecedented openness to new and creative ideas". Both sides reportedly moved closer on specific elements of an agreement related to nuclear limits and sanctions relief. That being said, major sticking points remain.

- Spot gold trades within a narrow range after only modestly gaining on yesterday’s US-Iran saga, which ended in no deal, but talks are poised to continue next week. Traders will be focused on any potential US military action this weekend in a bid to pressure Iran. Spot gold resides tight USD 5,167-5,200.64/oz range at the time of writing. Spot silver is firmer by some 1.5% intraday but contained to within Wednesday’s ranges.

- Base metals are firmer across the board despite the choppy risk tone in Asia, but prices are underpinned by the softer USD. Some desks attribute the rise to the stalled US-Iran talks and strengthening demand signals from China. The upside also comes ahead of next week’s China “Two Sessions”, where formal approval of the 15th Five-Year Plan and new stimulus measures for infrastructure and technology (AI, EVs, grid networks) are anticipated. 3M LME copper resides in a USD 13,243.73-13,508.13/t.

- London Metal Exchange announces the consultation for introducing regulatory position limits, exemptions and position management controls.

- Iron ore port stockpiles hit record levels in China as mines continue to add supply.

- Abu Dhabi reportedly offers more oil to partners, heading into the OPEC+ meeting, Bloomberg sources say.

- India is reportedly looking to cut coal imports for power plants at least 30% this year, sources say.

- China SHFE warehouses weekly changes: Copper +43.7%, Aluminium +19.7%, Zinc +44.9%.

- A local ceasefire has been established near the Zaporizhzhia nuclear power plant, TASS reported. Further by RIA stating one power line is being repaired at the power plant.

- Kazakhstan's energy minister said oil exports from Kazakhstan in 2026 will remain at last year's level and said oil output at Tengiz is almost at full capacity.

TRADE/TARIFFS

- China's MOFCOM announces adjustments to anti-discrimination measures against Canada effective Mar 1st till Dec 31st 2026, will not impose relevant tariffs on some imports from China.

- Japan's PM Takaichi said US needs to honour its commitments on tariffs.

NOTABLE EUROPEAN HEADLINES

- UK former Deputy PM Rayner noted the Gorton and Denton by-election results are a "wake up call" and Labour "has to be braver"; Sky News suggests these remarks will be taken as a direct aim at UK PM Starmer and his leadership.

- EU Commission eyes a legal loophole to bypass Hungary's veto of a EUR 90bln euro loan, according to FT.

- UK Green Party wins parliamentary seat in Gorton and Denton, defeating UK PM Starmer's Labour in the by-election.

NOTABLE EUROPEAN DATA RECAP

- Spanish Core Inflation Rate YoY Prel (Feb) Y/Y 2.7% (Prev. 2.6%).

- Spanish Inflation Rate MoM Prel (Feb) M/M 0.4% (Prev. -0.4%).

- Spanish Inflation Rate YoY Prel (Feb) Y/Y 2.3% vs. Exp. 2.2% (Prev. 2.3%).

- French GDP Growth Rate QoQ Final (Q4) Q/Q 0.2% vs. Exp. 0.2% (Prev. 0.2%, Rev. From 0.5%, Low. 0.1%, High. 0.2%).

- French GDP Growth Rate YoY Final (Q4) Y/Y 1.1% vs. Exp. 1.1% (Prev. 0.9%).

- French Inflation Rate MoM Prel (Feb) M/M 0.7% vs. Exp. 0.5% (Prev. -0.3%).

- French Inflation Rate YoY Prel (Feb) Y/Y 1.0%% vs. Exp. 0.8% (Prev. 0.3%, Low. 0.7%, High. 0.8%).

- German North Rhine Westphalia CPI MoM (Feb) M/M 0.2% (Prev. 0.1%).

- German North Rhine Westphalia CPI YoY (Feb) Y/Y 1.8% (Prev. 2.0%, Rev. From 2%).

- German Unemployment Rate (Feb) 6.3% vs. Exp. 6.3% (Prev. 6.3%, Low. 6.3%, High. 6.4%).

- German Import Prices YoY (Jan) Y/Y -2.3% (Prev. -2.3%).

- German Import Prices MoM (Jan) M/M 1.1% vs. Exp. 0.6% (Prev. -0.1%).

- Swiss GDP Growth Rate YoY (Q4) Y/Y 0.8% (Prev. 0.9%, Rev. From 0.8%).

- Swiss GDP Growth Rate QoQ Final (Q4) Q/Q 0.2% vs. Exp. 0.2% (Prev. -0.5%).

- UK Gfk Consumer Confidence (Feb) -19 vs. Exp. -15 (Prev. -16).

CENTRAL BANKS

- EU ECB Consumer Inflation Expectations (Jan) 2.6% (Prev. 2.8%).

- The PBoC has announced a new set of rules to facilitate cross-border CNY funding between local and foreign financial institutions.

- PBoC is to cut FX Risk Reserve Ratio for forward FX sales to 0% from 20% effective March 2nd to promote FX market development and support corporate exchange rate risk management.

- BoJ outright bond buying operations unchanged in March vs Feb (as expected).

GEOPOLITICS

MIDDLE EAST

- US authorises the departure of some embassy personnel and families from Israel amid safety risks.

- Iran urges US to abandon "excessive demands" to reach deal, Sky News Arabia reported citing AFP.

- Iranian spokesperson said "In the event of any conflict, American soldiers and their equipment will be destroyed, and all US resources and interests in the region will be within the range of Iranian forces", via Iran International.

- Top Middle East commander briefed US President Trump on military options on Iran, according to ABC News.

- US VP Vance said negotiations depend on what the Iranians do and there is no chance that any potential strikes on Iran will result in engaging in a war for years.

- US President Trump is expected to convene senior advisers on Friday for detailed discussions on Iran and to decide on a course of action toward Tehran, according to Israel Hayom citing US officials. Internal deliberations are said to be focused not on whether a strike would occur but on its scope and potential targets, while options under discussion include nuclear facilities, missile sites, state institutions and infrastructure.

- Iranian Foreign Minister said further progress has been made in our diplomatic engagement with the US, also said mission of the technical teams is as important as our mission.

- Oman's Foreign Minister is scheduled to meet with US VP Vance and other US officials in Washington on Friday.

OTHERS

- China said it is not possible to join denuclearisation talks at this stage.

- AFP reported of clashes near a major border crossing between Afghanistan and Pakistan.

- Afghan Ministry of Defence said their military operation resulted in casualties among Pakistani forces and came in defence of their territory and people, while it vowed to respond to future attacks.

- Loud explosion heard in Afghanistan's capital of Kabul and Pakistani fighter jets are reportedly conducting a raid on Kabul.

CRYPTO

- Bitcoin oscillates around USD 67,000 and Ethereum hovers above USD 2,000.

APAC TRADE

- APAC stocks were ultimately higher heading into month-end but with price action choppy following the weak handover from the US, where sentiment was clouded by tech weakness, while participants also digested the recent US-Iran talks in Geneva.

- ASX 200 mildly gained as strength in tech and telecoms atoned for the losses in financials and consumer stocks.

- Nikkei 225 traded indecisively amid a firmer currency and a slew of mixed data releases from Japan, in which Industrial Production disappointed, Retail Sales topped forecasts, and Tokyo CPI printed firmer-than-expected but slowed across the board with the Core reading falling beneath the central bank's 2% price target for the first time since October 2024.

- Hang Seng and Shanghai Comp were varied with outperformance in Hong Kong as participants digested earnings releases from the likes of Baidu and Sun Hung Kai Properties, while the mainland initially lacked direction in the absence of fresh catalysts and ahead of next week's annual "two sessions", while Trump-Xi summit preparations were said to falter. However, late upside was seen after comments from China's Politburo meeting in which it stated that China's development process during the 14th Five-Year Plan is extraordinary and that it is necessary to continue to implement a more active fiscal policy and a moderately loose monetary policy.

NOTABLE ASIA-PAC HEADLINES

- China Politburo held a meeting on Friday and noted that China's development process during the 14th Five-Year Plan is extremely unusual and extraordinary. Said that it is necessary to continue to implement a more active fiscal policy and a moderately loose monetary policy. Necessary to focus on building a strong domestic market and step up the cultivation and expansion of new growth momentum.

NOTABLE APAC DATA RECAP

- Tokyo Core CPI YoY (Feb) Y/Y 1.8% vs. Exp. 1.7% (Prev. 2.0%, Rev. From 2%, Low. 1.6%, High. 2%).

- Tokyo CPI YY (Feb) 1.6% vs Exp. 1.4% (Prev. 1.5%).

- Tokyo CPI Ex. Fresh Food & Energy YY (Feb) 2.5% vs Exp. 2.3% (Prev. 2.4%).

- Tokyo CPI Ex. Fresh Food YY (Feb) 1.8% vs Exp. 1.7% (Prev. 2.0%).

- Australian Housing Credit MoM (Jan) M/M 0.6% (Prev. 0.7%).

- Australian Private Sector Credit MoM (Jan) M/M 0.5% vs. Exp. 0.7% (Prev. 0.8%).

- Australian Private Sector Credit YoY (Jan) Y/Y 7.7% (Prev. 7.7%).

Loading...