Crude at highs but below USD 100/bbl amid concerns on US-Iran ceasefire fragility - Newsquawk US Market Open

- US President Trump threatened massive military escalation if Iran deal terms are not met, vowed no nuclear weapons, and they are to secure the Strait of Hormuz.

- Iranian Deputy Foreign Minister said the Speaker of Parliament will lead Iran’s delegation for the talks, and the exchange of messages continues via Pakistan, Al Jazeera reported.

- European bourses pull back as ceasefire begins to crack, Citi reinforces its OW stance on Banks; US equity futures soft.

- DXY firms on hawkish Fed Minutes, NZD continues to gain amid hawkish Breman.

- Fixed benchmarks pull back from highs, US PCE ahead.

- Crude nurses losses as ceasefire hopes wane while the IRGC announces a new Hormuz corridor.

- Looking ahead, highlights include US Initial Jobless Claims (Apr/04), PCE Final (Feb), GDP Final (Q4), Atlanta Fed GDP, NBP Policy Announcement, Banxico Minutes. Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

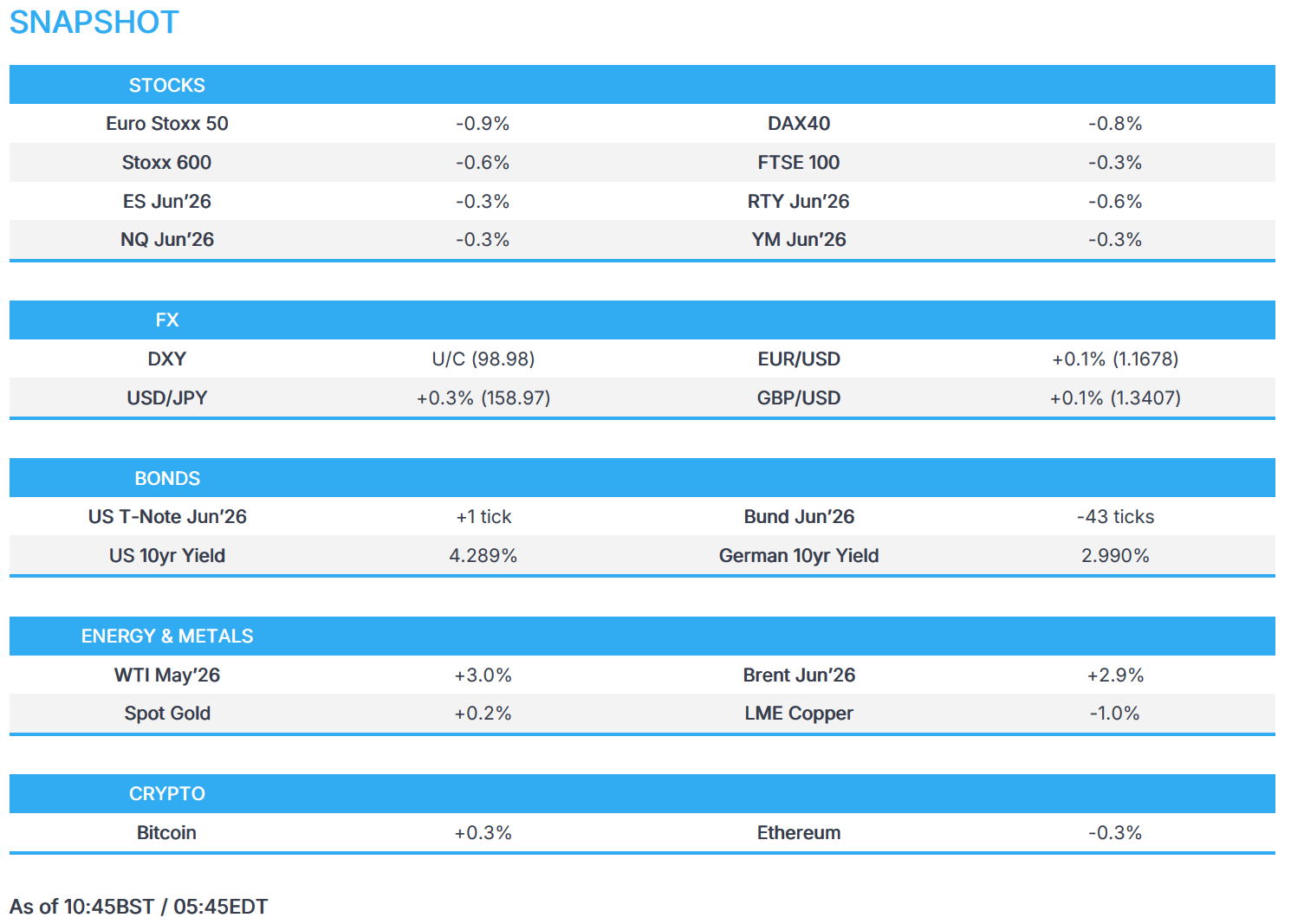

- European bourses (STOXX 600 -0.6%) have pulled back from Wednesday's ceasefire-related surge after cracks appeared in the agreement. US President Trump announced that the military will remain in and around Iran until a real agreement is fully complied with. Furthermore, the IRGC announced a new Hormuz corridor, effectively raising risks of disruption and bottlenecks. The IBEX 35 outperforms, with the index trading near flat. On the other hand, the DAX 40 is the underperformer.

- European sectors echo the above bias, with the majority in the red. Energy and Chemicals are amongst the sectors in the green, highlighting its defensive characteristics, while Consumer Products and Services and Technology sit at the bottom of the pile.

- US equity futures follow their European peers, with losses of between 0.3-0.6%. Despite equities pulling back from Wednesday's gains, the space could remain supported if bond volatility continues to pull back and the VIX remains below the 22 handle.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX Markets are paring some of Wednesday's optimism with crude gaining and general risk-off elsewhere as markets weigh Iran's claims of ceasefire breaches and subsequent concerns over Hormuz following reports from state media.

- DXY cautiously chugged higher throughout the European morning, supported by the key 99.00 mark. Overnight, FOMC Minutes were viewed as hawkish, with it stating many members said persistently higher oil prices could keep inflation elevated long enough to justify rate rises. Taking a look at rate expectations, markets moved to price just 7bps of easing by year-end compared to 15bps pre-minutes.

- Kiwi continues to perform well, amid hawkish remarks from RBNZ Governor Breman, she said inflation is expected to increase considerably in the near-term, and they will ‘act decisively’ if core prices pick up. This marks the second day of gains against the greenback, with NZD the sole currency that outperforms a mildly stronger USD. In terms of market pricing, 75bps of easing is expected by year-end, an increase of 15bps since last week.

- JPY is the worst performer in the G10, as energy prices weigh on the net importer nation. The pair marked a session low of 158.45 and sits on a 159 handle at the time of writing. Elsewhere, EUR/GBP trades a touch above the 0.87 mark. In a note this morning, ING suggests rate differentials will help the cross with EUR; rate expectations are likely to prove sticky and BoE dovish pricing potentially coming "through more smoothly" should energy prices continue to decline.

FIXED INCOME

- Global fixed benchmarks are trading flat to lower, as benchmarks pull back from the extremes seen on Wednesday, and as traders begin to find holes within the current ceasefire agreement. This comes after Iran’s Parliament Speaker Ghalibaf said three clauses of the 10-point plan have been violated so far, and as such, a bilateral ceasefire or negotiations is unreasonable. Another interesting point is that Iran introduced controlled shipping routes and coordination with the IRGC, effectively shifting from free transit to monitored flows—raising risks of disruptions and bottlenecks. (Full details on the Newsquawk headline feed). This, alongside continued strikes on both Lebanon and Iran, has led to a rebound in the energy complex, once again renewing inflationary concerns.

- USTs are currently flat, and mildly outperforming vs peers – currently trading within a 111-04+ to 111-10 range, and have entirely reversed the initial ceasefire-related optimism. Much of the action facilitated by the geopolitical factors mentioned above, but the complex is also weighed on by hawkish-leaning FOMC Minutes and heading into a 30yr auction later today. On the data front, markets will await weekly claims, February’s PCE data (exp. +0.4% M/M vs prev. +0.3%) and core PCE (exp. +0.4% M/M vs prev. +0.4%); final Q4 GDP stats. From a yield perspective, the 2yr has rebounded back towards 3.785% (vs Wednesday’s trough at 3.713%).

- Bunds are in the red and down by around 50 ticks at this stage, and holding towards the bottom end of a 125.67 to 126.10 range. German paper did dip a tick below the high from 7th April, with market participants highlighting 125.53 as a potential area for intraday longs to be exited. Bunds are moving at the whim of energy prices this morning, but there have been some domestic updates. An interesting comment via Italy’s PM Meloni got some attention, after she suggested that the EU should consider a temporary suspension of budget deficit rules if the Iran war persists. No move in EGBs at the time, but traders will remain cognizant of any fiscal related concerns, should a suspension be enacted. From a data perspective, Industrial Production printed at -0.3% (exp. +0.9%), highlighting the turbulent recovery of Germany – even before the Iran war started.

- Gilts are underperforming vs peers, after leading the fixed complex on Wednesday. As above, moving at the whim of energy prices, with UK-specific newsflow light. UK 2yr has rebounded back towards 4.237% (vs trough of 4.044% on Wednesday). UK paper currently trades within an 89.10 to 89.61 range; further pressure could see a breach below the 89.00 mark, and then the high from 7th April at 88.88.

- UK sold GBP 4bln 4.125% 2033 Gilt: b/c 3.30x (prev. 3.37x), average yield 4.507% (prev. 4.075%), tail 0.2bps (prev. 0.2bps).

- Spain sold EUR 5.778bln vs exp. EUR 5-6bln 2.35% 2029, 2.60% 2031 and 3.30% 2036 Bono & EUR 0.676bln vs exp. EUR 0.25-0.75bln 1.15% 2036 I/L Bono.

- Japan sold JPY 1.9tln 5yr JGBs; b/c 3.58x (prev. 3.69x), average yield 1.826% (prev. 1.633%).

- Unicredit (UCG IM) to sell 6-year EUR-denominated noted, guidance seen +125bps to MS.

- Lloyds (LLOY LN) to sell 10-year GBP-denominated noted, guidance seen at +170bps to UK Treasuries.

- Japanese Finance Minister Katayama said it is important to base JGB issuance plans on market demand, when asked about extending duration of government debt.

COMMODITIES

- Optimism over the US–Iran ceasefire faded as both sides signalled breaches and diverging terms, with Trump warning of military escalation if compliance fails and Iran’s Parliament Speaker Ghalibaf saying multiple clauses of Tehran’s plan have already been violated. Lebanon has emerged as the key fault line—while the US and Israel insist it sits outside the agreement, Iran and its allies treat it as integral, raising the risk of collapse as Israeli strikes and Hezbollah activity continue. The situation in the Strait of Hormuz adds further fragility, as Iran introduced controlled shipping routes and coordination with the IRGC, effectively shifting from free transit to monitored flows—raising risks of disruptions and bottlenecks (Full Analysis available on the Newsquawk headline feed).

- Crude rebounded after Wednesday’s biggest one-day drop since April 2020, with Brent Jun'26 back above USD 97/bbl (after Wednesday’s 13% slump), as the Strait of Hormuz remained largely blocked and Israeli attacks on Lebanon raised concerns over the durability of the Middle East truce. WTI May'26 trades towards the top of a USD 96.25-98.38/bbl range and Brent Jun'26 towards the upper end of a USD 96.30-98.53/bbl parameter. Mizuho expects crude to remain near USD 90/bbl through Q2 before returning to pre-conflict levels, while CBA sees upside risks while the Strait remains largely closed and physical undersupply linked to the Iran war supports prices.

- Spot gold holds above USD 4,700/oz after rising 1.5% over the prior two sessions, as traders weighed hopes for a diplomatic resolution against sporadic fighting that threatened the ceasefire. However, some flagged a technical correction after the sharp rise in front-month Comex futures. The metal trades within a narrow USD 4,699-4,733/oz range at the time of writing, with the 100 DMA at USD 4,671.57/oz. Commerzbank said gold had been supported by lower oil prices, easing inflation risks and pulling down rate expectations and bond yields, though the outlook still depends on whether a lasting US-Iran settlement emerges.

- Copper futures pulled back overnight and remain weak in the European session as the heightened risk appetite from the fragile US-Iran ceasefire petered out, with 3M LME copper in a narrow USD 12,587.00- 12,678.70/oz.

- Brazil court suspends oil export tax for Shell (SHEL LN), Equinor (EQNR), TotalEnergies (TTE FP) and Repsol (REP SM).

- OECD has urged governments to unwind expensive fuel duty cuts, according to the FT.

- Japan considers releasing an additional 20 days of oil reserves, according to Kyodo.

- US mulls lifting Venezuela's central bank sanctions with the aim of increasing oil output, according to sources.

- Russia is offering sanctioned LNG to Asia via intermediaries at a 40% discount.

- Goldman Sachs said Brent would average above USD 100/bbl through 2026 if the Strait of Hormuz stays closed for another month. Adds that the situation remains fluid after the start of a two-week US-Iran ceasefire, and that risks to its oil price forecast are still skewed to the upside.

TRADE/TARIFFS

- China’s Commerce Ministry, on EU trade, said that China is open to concluding economic and trade agreements between the pair.

NOTABLE EUROPEAN HEADLINES

- Italian PM Meloni said ruling out government reshuffle, not planning to resign; if the middle east crisis were to flare up again, Europe should consider temporary suspension of the stability and growth pact.

- EU's Dombrovskis said the bloc will still be hit by a “stagflationary shock” of low growth and rising inflation despite the US-Iran ceasefire, while European Commission is preparing to cut growth forecasts, according to FT.

NOTABLE EUROPEAN DATA RECAP

- German Industrial Production MoM (Feb) M/M -0.3% vs. Exp. 0.9% (Prev. -0.5%).

- German Balance of Trade (Feb) 19.8B vs. Exp. 18.5B (Prev. 21.2B).

- German Exports MoM (Feb) M/M 3.6% vs. Exp. 1% (Prev. -2.3%).

- German Imports MoM (Feb) M/M 4.7% vs. Exp. 4% (Prev. -5.9%).

- Spanish Industrial Production YoY (Feb) Y/Y -1.1% vs. Exp. 1.5% (Prev. 0.3%).

- UK BBA Mortgage Rate (Mar) 6.6% (Prev. 6.59%).

- UK RICS House Price Balance (Mar) -23% vs. Exp. -18% (Prev. -12%).

CENTRAL BANKS

- RBNZ Governor Bremen said more risk on inflation to the upside and inflation is expected to increase considerably in the near-term. said:. Previous rate cuts are still providing some stimulus to the economy, and a swift resolution to the conflict is expected to yield stronger growth this year. RBNZ to ‘act decisively’ if core prices pick up.

- BoJ Governor Ueda said short and medium-term interest rates are clearly negative, adds accommodative financial conditions are maintained, leading to moderate increase in capex.

NOTABLE US HEADLINES

- World Bank forecasts global growth for 2027 at 2.4%, while it said investment remains subdued as firms await clearer signals on the external environment and domestic policy, which it called a binding constraint on growth.

GEOPOLITICS

MIDDLE EAST

- US President Trump posted "All U.S. Ships, Aircraft, and Military Personnel....will remain in place in, and around, Iran, until such time as the REAL AGREEMENT reached is fully complied with".

- US President Trump posted "NATO WASN’T THERE WHEN WE NEEDED THEM, AND THEY WON’T BE THERE IF WE NEED THEM AGAIN. REMEMBER GREENLAND, THAT BIG, POORLY RUN, PIECE OF ICE!!!".

- Trump admin is considering a plan to punish some members of the NATO alliance that he believes were unhelpful to the US and Israel during the Iran war, WSJ reported citing admin officials. The proposal would involve moving US troops out of NATO member countries deemed unhelpful to the Iran war effort and station them in countries that were more supportive of the US military campaign. The proposal would fall far short of President Trump’s recent threats to fully withdraw the US from the alliance, which by law he can’t do without Congress. Plans could also include closure of at least 1 US base in a European country, possible Spain or Germany.

- NATO Secretary-General Rutte pointed out to US President Trump that a large majority of European nations have been helpful.

- US officials say they do not rule out resuming fighting in Iran and that President Trump will not offer major concessions to Iran to open the Strait of Hormuz, adds Iran's insistence on controlling straight reformers could lead to a resumption of fighting.

- Iranian Deputy Foreign Minister said the Speaker of Parliament will lead Iran’s delegation for the talks, and the exchange of messages continues via Pakistan, Al Jazeera reported.

- Iran Ambassador to Pakistan said the Iranian delegation is to arrive on Thursday night in Islamabad for "serious talks", based on the 10 points proposed by Iran.

- IRGC Navy announces alternative shipping routes to avoid possible sea mines, according to ISNA.

- IRGC claimed on Thursday that shipping through the Strait of Hormuz slowed sharply and then stopped following what it said was an Israeli ceasefire violation in Lebanon, according to CNN.

- Iranian Parliament's Security and Foreign Policy Committee Chairman Ibrahim Azizi said '"Once again, you have proven that you do not know the meaning of a ceasefire" and "Only fire will discipline you...so wait for it".

- Saudi Arabia and Iran reportedly discussed de-escalation in a call, according to SPA.

- Pakistani Foreign Ministry senior source suggests US has walked back on including Lebanon in the ceasefire with Iran, Al Arabiya reported.

- Israeli PM Netanyahu says will continue to strike Hezbollah with force, overnight, the IDF struck a series of terror infrastructures in southern Lebanon.

- Israel's Ministry of Energy directs the resumption of operations at the Karish gas platform after it halted due to the war, according to Israel's Channel 12.

- Hezbollah said its attacks on Israel will continue until the aggression stops, according to Fars News Agency, while it fires rockets at Israel citing ceasefire breaches.

- Missile fired from Lebanon into Northern Israel, according to Fars News Agency.

- Israeli attacks continue in Lebanon, despite a ceasefire with Iran, according to Anadolu Agency.

- French President Macron spoke with Iran's President Pezeshkian and US President Trump, and told both that their decision to accept the ceasefire was the best possible one.

RUSSIA-UKRAINE

- Russia launched 119 drones at Ukraine overnight according to UKR media.

CRYPTO

- Bitcoin finds support at USD 70.5k, while Ethereum trades just shy of USD 2.2k.

APAC TRADE

- APAC stocks were lower in a mild pullback from yesterday's ceasefire-fuelled extremes and as the widespread euphoria gradually waned amid the wide gaps between each side's peace proposals. Furthermore, several strikes had continued in the 24 hours after the announcement, and the inclusion of Lebanon is seen as a key point of contention, while shipping in the Strait of Hormuz remains largely blocked, although a senior Iranian official stated that Iran could open Hormuz on Thursday or Friday ahead of their planned talks.

- ASX 200 traded little changed amid a lack of data or drivers and with resilience in energy, defensives and financials offsetting the firm losses in the tech sector.

- Nikkei 225 pulled back after the prior day's stellar performance, with the index returning to beneath the 56,000 level amid very few fresh catalysts and the absence of tier-1 data to sustain the previous momentum.

- Hang Seng and Shanghai Comp conformed to the uninspired mood amid concerns regarding the fragility of the US-Iran ceasefire, and with weakness in Chinese tech and property stocks, while there were prior reports that the US FCC will vote on a measure that would ban Chinese labs from testing US electronics.

NOTABLE ASIA-PAC HEADLINES

- South Korea's Finance Minister comments that financial and FX market volatility has eased a bit.

NOTABLE APAC DATA RECAP

- Japanese Consumer Confidence (Mar) 33.3 vs. Exp. 38 (Prev. 40.0).

- Japanese Machine Tool Orders YoY (Mar) Y/Y 28.1% (Prev. 24.2%).

- Japanese Foreign Bond Investment (Apr/04) -2462.4.

- Japanese Stock Investment by Foreigners (Apr/04) 2959.6.

Loading...