Crude a little lower on geopolitical optimism, US equity futures mostly unchanged, bourses outperform; Fed speak ahead - Newsquawk US Market Open

- The text of the possible memorandum of understanding between the US and Iran has not been finalised and confirmed to this point, according to Tasnim.

- A Romanian radio station reported that a drone hit a residential building in Romania's Galati, near the border with Ukraine.

- The EU is to discuss restrictions on Chinese imports, although no decision was expected on Friday.

- Crude benchmarks are currently trading towards lows; Brent Aug’26 -1.6%.

- European bourses are broadly firmer this morning, whilst US equity futures are contained; Dell +37% post-earnings.

- DXY gains slightly, whilst the Kiwi outperforms after hawkish speak from RBNZ officials.

- Looking ahead, highlights include German Nationwide CPI (May), Canadian GDP (Q1). Speakers include Fed's Schmid, Bowman, Paulson & Daly. Credit Rating updates include S&P on France & Hungary, Morningstar DBRS on Spain.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- Many points regarding the Iranian nuclear file have been resolved; Iran has agreed to international oversight of its nuclear facilities to prevent their dismantling, Al Arabiya reported citing sources. Iran wants to transfer the enriched uranium to China with a commitment not to deliver it to America.

- Chairman of the Iranian National Security Committee of the Iranian Parliament said there are no plans to transfer enriched uranium out of the country, Asharq reported.

- Iran Deputy for Foreign Policy and International Security Ali Baqeri held separate meetings in Moscow with the Foreign Policy Advisor to Brazil's President and the Secretary General of Egypt's National Security Council.

- IRGC Commander said Iran forces are ready to act on Supreme Leader's order and enemies should not make mistakes as they will get themselves and others into trouble.

- Iran military source said US drone was intercepted near Bushehr in southern Iran, according to Al Jazeera.

- US Vice President Vance said that US President Trump is not yet ready to endorse the Iran agreement, while Vance noted that US and Iran made a lot of progress towards a ceasefire deal, according to AFP. Vance said US and Iran are at odds on uranium enrichment and stockpiles, according to SNN.

- White House Deputy Chief of Staff for Policy Stephen Miller stating in an interview with Fox News that US President Trump is directly involved in negotiations with Iran.

- US President Trump said we completely sank the Iranian Navy and destroyed their air force, did not target all of Iran’s military leadership so that what happened in Iraq would not be repeated.

- US military said Iran's state TV claim that Iranian forces downed a US aircraft near Bushehr is false and no US aircraft was shot down by Iran, with all US air assets are accounted for.

- US VP Vance said US and Iran are exchanging proposals regarding some drafting points including issue of enrichment, adds time is still early to know when an agreement with Iran will be reached and if it will happen at all.

- US Treasury imposes fresh sanctions targeting Iran's military oil sales, according to Reuters. IRNA reported US sanctions 25 individuals, firms and vessels over Iran oil.

- US President Trump said that US has all the cards, Iran has been defeated militarily, according to a Fox interview.

- Al Hadath posted Iranian television reported “the downing of an American fighter jet” in the vicinity of Bushehr, with no American confirmations.

- US official denies what Iranian TV announced about downing any American plane near Bushehr, according to Al Hadath.

- Israel's Channel 12, citing military sources, said "The army recommends to the political leadership intensifying the air and ground strikes in Lebanon".

EUROPEAN TRADE

EQUITIES

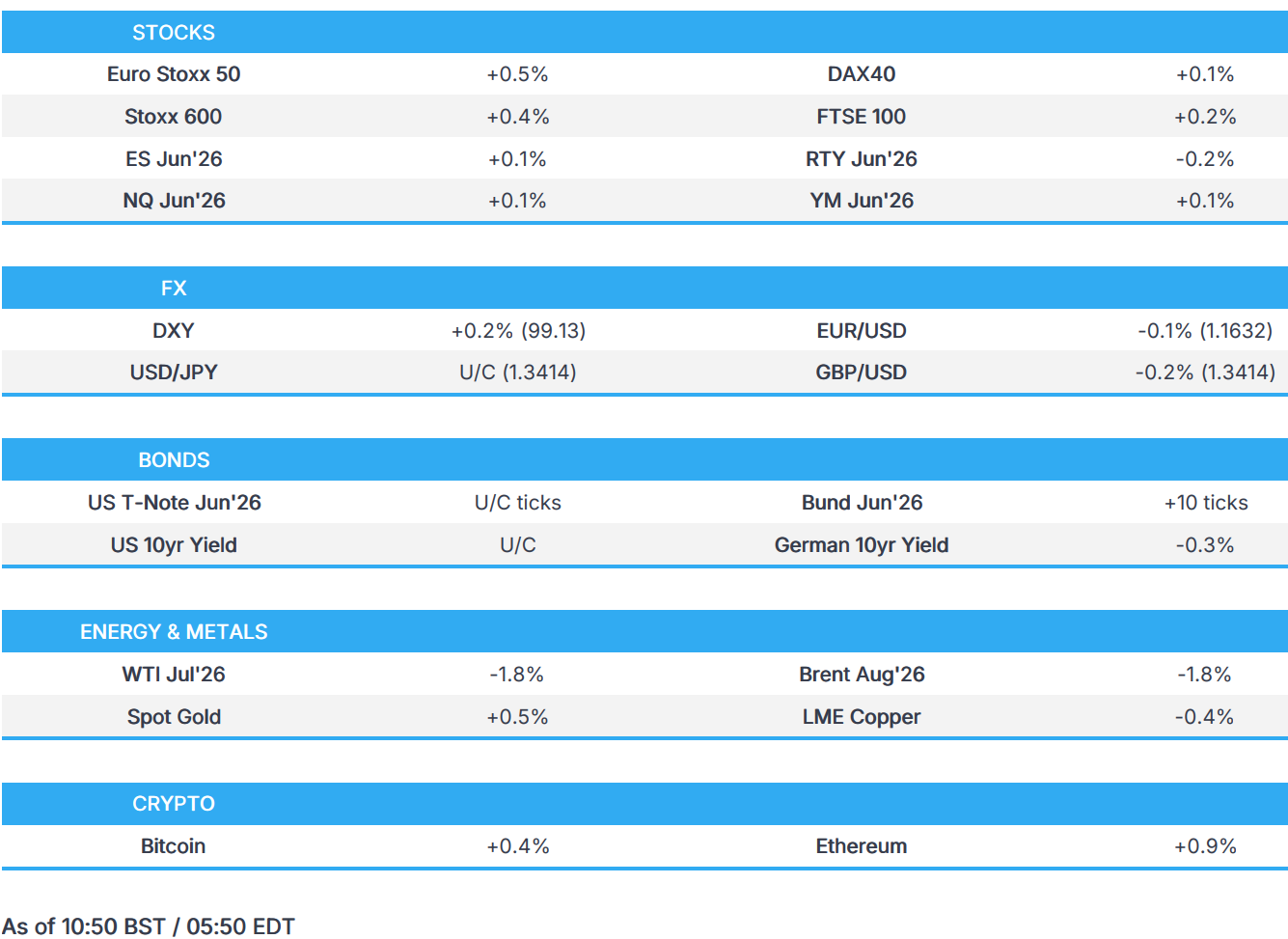

- European bourses (STOXX 600 +0.4%) are firmer across the board, attempting to rebound from recent losses and as markets digest reports that the US and Iran are nearing an agreement to extend the ceasefire. (See the commodities section for details.) From an index standpoint, the CAC 40 (+1%) outperforms in Europe whilst the FTSE 100 (+0.2%) lags vs peers, given its exposure to energy names.

- European sectors hold a positive bias. The cyclical industries (Consumer Products / Travel & Leisure / Autos) top the sectoral list, whilst the likes of Energy and Utilities hold towards the bottom of the pile. The Energy sector, unsurprisingly, has been dragged down by losses across the underlying oil complex.

- US equity futures trade modestly on either side of the unchanged mark, with the ES and NQ holding afloat (+0.1%), whilst the RTY is a touch lower (-0.2%). Tentative action following the strength seen in the prior session, and as markets await further updates on the US-Iran ceasefire agreement. The US data slate is lacking today, but with focus on a slew of Fed speakers, including: Fed's Schmid, Bowman, Paulson & Daly.

- Dell (DELL) shares +37% in pre-market trade after it beat expectations, posted its fastest post-listing sales growth, benefited from strong AI server demand and raised its outlook. It reported Q1 adj. EPS of 4.86 (exp. 2.96), Q1 revenue USD 43.8bln (exp. 35.77bln). Said its record Q1 results reflected strong in-quarter demand and innovation across PCs, compute and storage, with USD 24.4bln of AI orders, USD 16.1bln of AI server revenue and a record USD 51.3bln AI backlog at quarter-end. AI demand remains exceptionally strong and continues to exceed supply, with memory the primary constraint, while pricing discipline and margin stability seen in Q4 and Q1 continue to hold.

- NVIDIA’s (NVDA) VR200 reportedly delayed by two months amid cooling challenges, Tech Taiwan reports.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are mixed against the Dollar. Kiwi leads after hawkish RBNZ speak overnight after the hawkish-leaning RBNZ hold early in the week, while Sterling lags after Cable dipped below its 200DMA.

- The Greenback is a touch firmer in a rebound from hefty losses on Thursday, when the DXY closed 0.6% from highs. (See Commodities on the headline feed). In short, a deal seems near, but uncertainty remains over whether Trump will sign off on the proposal and whether Tehran will formally endorse the reported terms. Aside from US-Iran, eyes are also on tensions between NATO’s Romania and Russia after a drone hit a residential building in Romania's Galati. DXY is firmer by 0.2% within 98.95-99.19 parameters.

- French, Spanish and German state inflation imply cooler German nationwide (due 13:00 BST), and EZ (due Tuesday) prints. French GDP: Final measures softer than expected. Q1 rate was revised into contraction from flat, yearly basis was also revised a touch lower. French HICP: Softer than expected and ticks up from the prior. Spanish HICP: Ticks up a touch on a yearly basis, in line with expectations, the monthly rate falls a touch beneath expectations and previous. German CPI: Implies the nationwide rate (due at 13:00 BST) will cool at a faster rate than expected. Limited moves were seen on the metrics with EUR/USD falling around 15 pips from 08:00BST. ECB pricing for June continues to price a c.89% probability of a 25bps hike.

- Tokyo CPI softened across the board in May, with core CPI slowing to 1.3% Y/Y from 1.5%, below expectations of 1.5%. The downside was largely driven by government subsidies on utilities and education costs. The release marks a fourth consecutive month of Tokyo core inflation running below the BoJ’s 2% target and contrasts with stronger activity data elsewhere in the economy. For the BoJ, the print provides ammunition for doves arguing for patience. Markets continue to expect the bank to raise rates at the June confab, with 18bps, or 71% probability of a 25bps hike. We expect the release of data which could show intervention occurred in April, which is due around 11:00 BST. USD/JPY trades unchanged within a narrow 18-pip 159.20-159.38 range.

- Kiwi is the best G10 performer after hawkish speak from RBNZ officials overnight. Breman (Consensus voter) said she sees ongoing uncertainty around inflation and that, on balance, the OCR is likely to increase. Assistant Governor Silk (Consensus voter) said she did not think interest rates need to increase yet, though she cautioned that the bias is for rate hikes in the coming meetings. As such, following the hawkish speak from non-dissenting members, the bias for July is tightening with markets assigning a 70% probability of such action.

FIXED INCOME

- A modestly bearish start to the day for fixed income, as we ease modestly off the post-Axios peaks on Thursday and continue to await the assessment of US President Trump on the MOU. Note, a recent dip in energy has provided some modest support.

- USTs at the lower end of a 109-31 to 110-06 band, having faded from Thursday's 110-07+ WTD peak. The docket for the US ahead is primarily waiting for Trump to comment on the MOU situation, and as such USTs may be relatively rangebound until an update occurs. That aside, we look for remarks from various Fed speakers. This morning, Kashkari (2026) said it is unclear what the future path of policy is and, in the context of April's PCE, that it would be premature to conclude they need to tighten immediately.

- Bunds are in line with the above for the most part, but have been moved about a touch by European data for May. At first, the benchmark found itself at a 126.05 trough with downside of just under 15 ticks, having also faded from Thursday's 126.47 best; note, that was a tick shy of Monday's high and the WTD peak. Thereafter, EGBs saw some modest upside on the cooler-than-expected French preliminary inflation print for May. Albeit, the move was only c. 10 ticks in Bunds and OATs, as prices lifted from the prior level. Next up was Spain, which printed as expected at a harmonised level and a touch cooler on the headline Y/Y. Note, the core figure ticked up to 2.9% (prev. 2.8%). Modest two-way action followed the data. Followed by Germany, where the state figures came in cooler than the prior level and have shifted the mainland consensus to a cooler print, vs pre-state forecasts for another 2.9% Y/Y figure. Finally, Italy was hotter than expected for all components aside from the headline Y/Y.

- We await the German nationwide figure at 13:00BST before assessing next week's EZ HICP. As it stands, Bunds are just off a 126.33 high, lifted alongside peers following a bout of energy pressure.

- Gilts started the day unchanged before experiencing some modest pressure in line with the slight overnight bias in peers, moving to an 88.48 trough. Since, BoE's Bailey spoke and his remarks perhaps have a slight dovish skew, as he noted that the BoE removing expected cuts has already "tightened policy considerably" and tolerating temporarily above target inflation to help the economy is an appropriate approach. Albeit, Bailey made clear that such tolerance would erode if "signs of second-round effects begin to emerge".

- Japan sold JPY 2.1tln 2-year JGBs b/c 3.70 (prev. 5.24), average yield 1.369% (prev. 1.407%). Lowest accepted price 100.04 (prev. 99.980). Weighted average price 100.06 (prev. 99.985). Tail in price 0.02 (prev. 0.005).

- Australia sold AUD 1bln 2.75% November 2029 bonds b/c 3.67, avg yield 4.4692%.

COMMODITIES

- The week was marked by a sharp flare-up followed by renewed optimism around diplomacy. Following yesterday’s Axios reports regarding a 60-day MoU framework, Iran’s Tasnim reported that the text of the possible memorandum of understanding between the US and Iran had not been finalised or confirmed. Uncertainty remains over whether Trump will sign off on the proposal and whether Tehran will formally endorse the reported terms. This morning, there were mixed reports regarding the uranium file, in which Iran rebuffed reports that it wants to transfer the enriched uranium to China with a commitment not to deliver it to the US.

- Elsewhere in geopolitics, a Romanian radio station reported that a drone hit a residential building in Romania's Galati, near the border with Ukraine. NATO Secretary General Rutte affirmed "NATO’s absolute solidarity with Romania", and added that "NATO stands ready to defend every inch of Allied territory"; "will continue to enhance our readiness to deter and defend against any threat".

- The crude complex has been choppy this morning, with initial strength earlier in the session now entirely eroded; as it stands, benchmarks are towards session lows. WTI Jul currently trades towards the lower end of a USD 87.17-89.01/bbl range, while Brent Aug sits in a USD 91.28-92.95/bbl. Dutch TTF trades almost 2% firmer north of EUR 47.50/MWh.

- Spot gold continues the post-PCE rebound seen yesterday, with prices modestly firmer intraday above the USD 4,500/oz level in a USD 4,488-4,530/oz range. Spot silver, conversely, is lower with the precious metal towards the bottom of a USD 75.08-76.44/oz range.

- Base metals are mostly but modestly softer as traders look ahead to further geopolitical headlines, with price action rather contained at the time of writing. 3M LME copper trades towards the middle of a narrow USD 13,653.93- 13,748.38/t range.

- Kazakhstan Energy Minister said planned maintenance at the Kashagan oil field (400k bpd) is likely to be delayed until 2027.

- Commerzbank expects copper to rise to USD 14,250/ton by mid-2027 and Brent crude to reach USD 90/bbl by end-September before declining to USD 85/bbl by year-end.

TRADE/TARIFFS

- EU Commissioners will meet for a "orientation debate", which will cover the investigation of Chinese trade practices and an "overcapacity instrument", Politico reported; two probes re. chemicals are already being considered.

- China will retaliate against EU's overcapacity tool and may probe EU supply chains, according to state-linked Yu Yuantan.

NOTABLE EUROPEAN HEADLINES

- Communications between former UK Minister Wes Streeting (potential PM candidate) and Peter Mandelson will be published next week, The Sun reported.

NOTABLE EUROPEAN DATA RECAP

- German State CPIs were cooler than what the nationwide expectations imply.

- German Unemployment Rate (May) 6.3% vs. Exp. 6.4% (Prev. 6.4%, Low. 6.3%, High. 6.5%).

- German Unemployed Persons (May) 2.987M (Prev. 3.006M).

- German Unemployment Change (May) -12K vs. Exp. 10K (Prev. 20K).

- German Import Prices YoY (Apr) Y/Y 5.3% (Prev. 2.3%).

- German Import Prices MoM (Apr) M/M 1.2% (Prev. 3.6%).

- Italian Unemployment Rate (Apr) 5.1% vs. Exp. 5.3% (Prev. 5.2%).

- Spanish Inflation Rate Prel (May) Y/Y 3.2% vs. Exp. 3.4% (Prev. 3.2%).

- Spanish Inflation Rate Prel (May) M/M 0.1% (Prev. 0.4%).

- Spanish HICP Prel (May) M/M 0.1% vs. Exp. 0.2% (Prev. 0.7%).

- Spanish HICP Prel (May) Y/Y 3.6% vs. Exp. 3.6% (Prev. 3.5%).

- Spanish Core Inflation Rate Prel (May) Y/Y 2.9% (Prev. 2.8%).

- French GDP Growth Rate YoY Final (Q1) Y/Y 0.9% vs. Exp. 1.1% (Prev. 1.3%).

- French GDP Growth Rate QoQ Final (Q1) Q/Q -0.1% vs. Exp. 0% (Prev. 0.2%, Low. 0.0%, High. 0.1%).

- French Prelim. HICP (May): 2.8% Y/Y vs Exp. 2.9% (prev. 2.5%); 0.1% M/M vs Exp. 0.3% (prev. 1.2%).

- French Private Non Farm Payrolls QoQ Final (Q1) Q/Q -0.1% vs. Exp. -0.1% (Prev. -0.1%).

- French Inflation Rate MoM Prel (May) M/M 0.1% vs. Exp. 0.2% (Prev. 1%).

- French Inflation Rate YoY Prel (May) Y/Y 2.4% vs. Exp. 2.6% (Prev. 2.2%, Low. 2.5%, High. 2.7%).

- French Household Consumption MoM (Apr) M/M -0.5% vs. Exp. 0.1% (Prev. 0.7%).

- Swedish Retail Sales MoM (Apr) M/M 0.0% (Prev. 3.1%).

- Swedish Household Lending Growth YoY (Apr) Y/Y 3.0% (Prev. 3.1%).

- Swedish GDP Growth Rate YoY Final (Q1) Y/Y 2% vs. Exp. 1.6% (Prev. 1.8%).

- Swedish Retail Sales YoY (Apr) Y/Y 4.7% (Prev. 6.2%).

- Norwegian Registered Jobless Rate (May) 1.90% vs. Exp. 2.1% (Prev. 2.1%).

- Norwegian Retail Sales MoM (Apr) M/M 0.3% (Prev. -0.1%).

CENTRAL BANKS

- Fed's Kashkari (voter) said it is now unclear what the future path of monetary policy will be due to the Iran war; it is premature to conclude that the Fed needs to raise rates immediately after the April PCE inflation data. Speaking on PCE data, Kashkari said it makes him pay even more attention to inflation risks.

- Former BoJ Board Member Sakurai said BoJ will likely raise rates in June, Bloomberg reported.

- ECB’s Panetta said medium-term inflation expectations remain firmly anchored to target. For the June rate decision, it is crucial to assess the extent of the pass-through of higher energy prices. The forward-looking picture seems to call for a recalibration of the monetary policy stance. ECB will act in a timely and measured manner to stop the energy shock from turning into persistent inflation. Consumers’ inflation expectations are rising and firms have already started planning price increases.

- BoE Governor Bailey says have to monitor the situation in the Middle East and how it affects the UK economy and inflation very closely and adjust policy as required. Having taken expected cuts off the table for now, we have already tightened policy considerably in response to the shock relative to what had been expected by markets. Uncertainty about the strength of second-round effects means that monetary policy needs to balance the costs of leaning too little against these effects against the costs of responding too much. Tolerating temporarily above-target inflation to provide some support for the real economy is an appropriate way to approach the trade-off. But that tolerance would weaken if signs of second-round effects begin to emerge. Higher inflation expectations are not coming through in wage expectations and settlements. Hope a fall in UK bond market curve will go on but depends on events in the Middle East. Markets "obviously" see pressure on fiscal plans of government from Iran war impact.

- RBNZ Governor Breman said sees ongoing uncertainty around inflation and that on balance, the OCR is likely to increase.

- RBNZ Assistant Governor Silk said did not think interest rates need to increase yet, but inflation pressures are building in the near term, adds looking at high frequency data for July decision, bias is we're going to see rate hikes in coming meetings.

- RBNZ's Gourley said rates likely to rise sooner rather than later, but speed and size of any increase will depend on data.

- PBoC set USD/CNY mid-point at 6.8176 vs exp. 6.7685 (prev. 6.8240).

- Riksbank Financial Stability Report: The war in the Middle East entails risks to financial stability. The financial system has functioned well, but uncertainty is high. Favourable initial position for the Swedish financial system but risks remain. Maintains the CCyB at 2%.

NOTABLE US HEADLINES

- US State Department designates Brazilian criminal organisations Comando Vermelho and PCC as specially designated global terrorists, effective June 5th.

GEOPOLITICS

RUSSIA-UKRAINE

- Romanian President said the unprecedented nature of the drone incident requires a firm, coordinated response at both the national and international levels; Romania summoned Russia's ambassador.

- European Commission President von der Leyen said the EU is preparing the 21st package of sanctions on Russia. EU will bolster security and deterrence, particularly on its eastern border, while maintaining pressure on Russia.

- Ukraine said that Russia carried out a drone strike on a Turkish vessel overnight.

- Fuel storage facilities in Russia’s Yaroslavl region were hit by drones.

- Romanian radio station reported a drone hit a residential building in Romania's Galati, close to the border with Ukraine.

- Currently no plans to have an extra NATO North Atlantic Council, Free Radio's Jozwiak reported.

- NATO Secretary General Rutte affirms "NATO’s absolute solidarity with Romania"; adds "NATO stands ready to defend every inch of Allied territory"; "will continue to enhance our readiness to deter and defend against any threat".

- EU Foreign Policy Chief Kallas said Moscow cannot be allowed to breach European airspace with impunity following the drone incident in Romania.

CRYPTO

- Bitcoin is a little firmer this morning and trades around USD 74k, whilst Ethereum holds around USD 2k.

APAC TRADE

- APAC stocks headed into month-end on the front foot as the region took impetus from the gains stateside, where the S&P 500 and Nasdaq 100 posted fresh record highs amid reports of a tentative agreement regarding an MOU for a 60-day US-Iran ceasefire extension and to launch negotiations on Iran's nuclear programme, although it still needs approval from US President Trump, while Iranian sources also pushed back and stated it was not finalised.

- ASX 200 was led higher by outperformance in the mining, materials and resources industries, while the energy and defensive sectors were at the other end of the spectrum as geopolitics and oil moves remained the main catalyst for price action.

- Nikkei 225 rallied back above the 66,000 level amid lower oil prices and following a slew of data, including softer Tokyo CPI, lower Unemployment, and better-than-expected industrial output & retail sales.

- Hang Seng and Shanghai Comp were mixed as the mainland lagged and with headwinds from earnings, as automakers were pressured following weak results from XPeng, while sentiment was also not helped by trade frictions, with the EU set to discuss restrictions on Chinese imports.

NOTABLE ASIA-PAC HEADLINES

- Japanese Chief Cabinet Secretary Kihara said he is extremely concerned about speculative moves in the FX market; won't comment on FX levels and intervention. Government stance is to always take appropriate FX action.

- Japanese Finance Minister Katayama said we'll consider cost risk balance in reference to issuing bonds and to engage in dialogue with market on bond management, while she declines comment on future bond maturities at this time. said:. It's important to have broad bond investor base. Will continue appropriate debt management policies.

- Japanese Finance Minister Katayama said Japan can take decisive action on FX volatility, while she declined to comment on whether intervention has taken place or not.

NOTABLE APAC DATA RECAP

- Japanese Consumer Confidence (May) 33.6 vs. Exp. 32 (Prev. 32.2).

- Japanese Industrial Production MoM Prel (Apr) M/M 0.8% vs. Exp. -0.9% (Prev. -0.4%, Low. -2.2%, High. -0.5%).

- Japanese Retail Sales MoM (Apr) M/M 1.3% (Prev. 1.3%).

- Japanese Industrial Production YoY Prel (Apr) Y/Y 2.3%.

- Japanese Retail Sales YoY (Apr) Y/Y 2.1% vs. Exp. 1.3% (Prev. 1.7%, Low. 0.2%, High. 3.2%).

- Japanese Tokyo Core CPI YoY (May) Y/Y 1.3% vs. Exp. 1.5% (Prev. 1.5%, Low. 1.4%, High. 1.7%).

- Japanese Tokyo CPI Ex Food and Energy YoY (May) Y/Y 1.6% vs. Exp. 1.9% (Prev. 1.9%).

- Japanese Unemployment Rate (Apr) 2.5% vs. Exp. 2.7% (Prev. 2.7%, Low. 2.6%, High. 2.7%).

- Japanese Tokyo CPI YoY (May) Y/Y 1.4% vs. Exp. 1.6% (Prev. 1.5%).

- Japanese Jobs/applications ratio (Apr) 1.18 vs. Exp. 1.18 (Prev. 1.18, Low. 1.17, High. 1.19).

- New Zealand ANZ Activity Outlook (May) 25.6 (Prev. 19.6).

- New Zealand ANZ Business Confidence (May) 10.0 (Prev. -10.6).

- New Zealand ANZ Consumer Confidence Index (Apr) 86.5 (Prev. 80.3).

- New Zealand ANZ Roy Morgan Consumer Confidence (May) 86.5 (Prev. 80.3).

- Korea (Republic of) Retail Sales MoM (Apr) M/M -3.6% (Prev. 1.8%).

- Korea (Republic of) Industrial Production YoY (Apr) Y/Y 1.5% vs Exp. 2.5% (Prev. 3.6%).

- Korea (Republic of) Industrial Production MoM (Apr) M/M -0.7% vs Exp. 0.4% (Prev. 0.3%).

NOTABLE APAC EQUITY HEADLINES

- Japanese Finance Minister Katayama said she met with a senior OpenAI official today and agreed for some Japanese financial institutions to gain access to OpenAI’s new model.

Loading...