Crude slips amid reports of a potential Strait of Hormuz breakthrough, US equity futures modestly firmer - US Market Open

- Al Arabiya reported that "the coming hours will witness a breakthrough for the situation of the ships stuck in the strait", spurring pressure in the crude complex.

- Iran is expected to provide its reply to the US proposal for ending the war to mediators on Thursday, according to CNN, citing a regional source.

- US President Trump could turn to military action without an agreement with Iran ahead of the China trip, according to Axios, citing US officials.

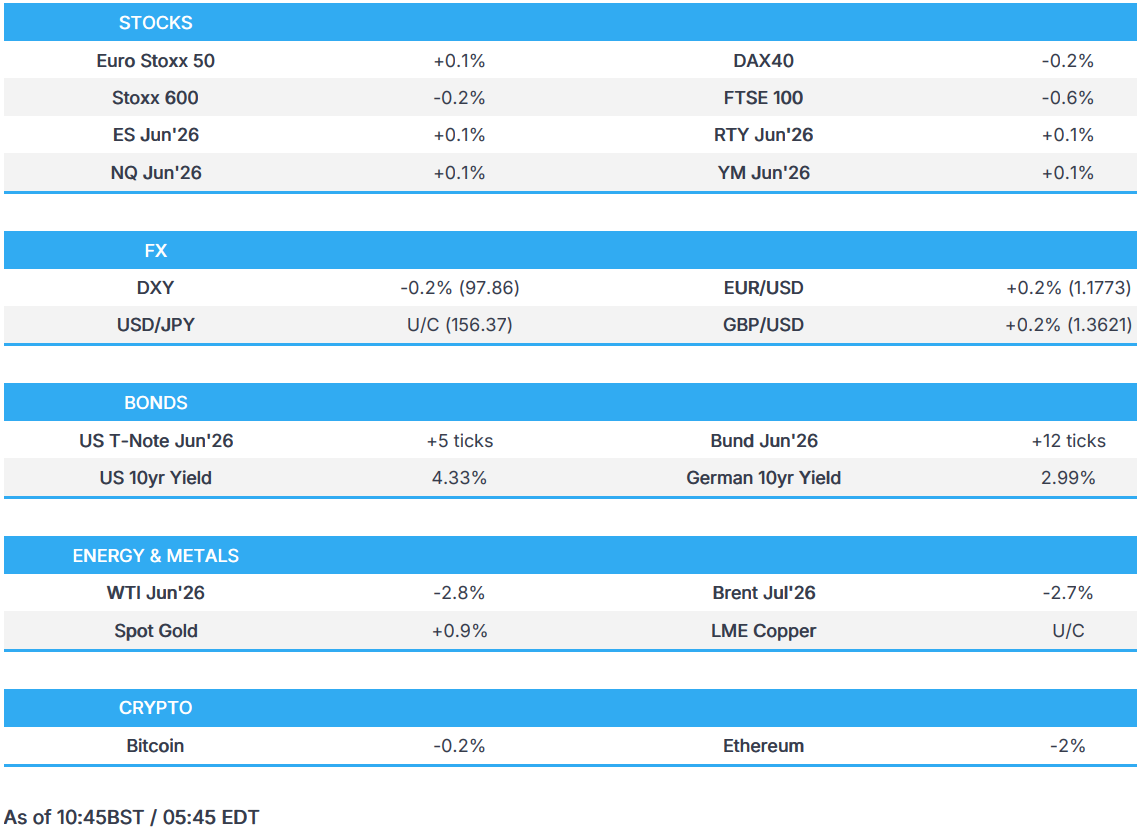

- European and US equity futures are modestly firmer; ARM -6.5% post-earnings.

- DXY downbeat as positive geopolitical headlines pressure crude; Antipodeans lead whilst the JPY lags vs peers.

- Fixed benchmark made new WTD highs amidst geopolitical optimism, but now off best levels.

- Looking ahead, highlights include US Challenger Job Layoffs (Apr), US Jobless Claims (May 2), Atlanta Fed GDP, CNB/Banxico Policy Announcement (May), CBR Minutes (May), UK Local Elections. Speakers include ECBʼs Elderson, Schnabel, Lane, BoEʼs Mann, Taylor, Fedʼs Hammack, Williams, Kashkari. Earnings from CoreWeave, IREN, Coinbase, Cloudflare, DraftKings, ACM Research, Datadog, McDonald's.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRANIAN CONFLICT

- Iran is expected to provide its reply to mediators on Thursday, CNN reported citing a regional source.

- "Arabic sources: Reaching understandings regarding easing the siege in exchange for the gradual opening of the Strait of Hormuz ", Al Arabiya reported; "The coming hours will witness a breakthrough for the situation of the ships stuck in the strait".

- Pakistani Foreign Ministry spokesperson said, "We do not talk about war and instead talk about dialogue and diplomacy. However, if any aggression similar to what we saw last year, we will respond; Pakistan will respond just as it did", Mallick posted.

- Pakistani Foreign Ministry Spokesperson said "We have not yet received a response from Iran regarding the US amendments", Al Jazeera reported.

- "Pakistani source to Al Arabiya said Iran may hand over its response to the US proposal to the Pakistani mediator today", Al Arabiya. "No arrangements for any direct meetings between the Iranians and the Americans so far.". "Contacts with the Iranians are ongoing and there are no obstacles hindering continued". "Discussions are ongoing regarding the status of the Strait of Hormuz, and reaching understandings is still possible".

- Pakistani Foreign Ministry said "We expect an urgent agreement between Iran and the United States", Al Araby reported.

- "Israel was informed that Iran has agreed to transfer its stockpile of 60% enriched uranium to a third country that remains unknown", Sky News Arabia reported citing Israeli Channel 12.

- Pakistani Foreign Ministry spokesperson, on US-Iran agreement, said "we would expect an agreement sooner rather than later", Pakistani journalist Mallick posted. "We will welcome any settlement wherever that takes place, if it takes place in Islamabad, it would be an honour and privilege.”.

- The proposed agreement between the US and Iran may limit the IDF's action in Lebanon, Israeli press reported citing an Israeli official.

- US President Trump, on Iran, said it will all work out very quickly.

- IDF said it has intercepted suspicious aerial target launched from Lebanon towards Israel following sirens that sounded in Manara, Margaliot and Kiryat Shmona.

- Lebanon's PM Salam said it is not seeking normalisation with Israel and it is too early to discuss any possible meeting with Israeli PM Netanyahu.

- Iran has issued a message to commercial vessels in the Strait of Hormuz, saying Iran's port is fully prepared to provide general maritime services and support to the vessels, IRNA reported.

- US President Trump could turn to military action without an Iran agreement ahead of the China trip, Axios reported citing US officials.

- US President Trump's reversal on his plan to help ships go through the Strait of Hormuz came after Saudi Arabia suspended the US's ability to use its bases and airspace to carry out Project Freedom, NBC reported citing US officials.

- IRGC Navy Political Affairs Official said we will impose our control over the Strait of Hormuz, and any attack will be met with a plan beyond the enemy's calculations, Al Jazeera reported.

EUROPEAN TRADE

EQUITIES

- European bourses are broadly modestly firmer, attempting to build on the hefty gains seen in the prior session. Geopolitics remains the key focus this morning, with Iran expected to provide its reply to the US proposal for ending the war to mediators on Thursday, CNN reported. Sentiment in early morning trade was lifted after Al Arabiya reported that "the coming hours will witness a breakthrough for the situation of the ships stuck in the strait".

- European sectors are mixed. Travel & Leisure takes the top spot, joined closely by Consumer Products and then Autos. Sectors which have broadly benefited from the risk-tone and/or lower energy prices. Elsewhere, Utilities is found right at the foot of the pile, joined closely by Telecoms.

- In terms of key movers: Henkel (+3.9%, sales topped exp.), Rheinmetall (-3.1%, missed on Q1 EPS, but reaffirmed outlook), Telecom Italia (+3.2%, revenue +1.4% amidst strong Brazil growth), Shell (-1.7%, EPS and Rev. topped expectations whilst announcing a USD 3bln buyback), Flutter (-3.6%, cut guidance despite reporting higher Q1 revenue).

- US equity futures are all trading modestly firmer this morning, with gains of circa. 0.1%. As for pre-market movers: Arm (-5.2%, weaker-than-expected royalty revenue and rising operating expenses offset enthusiasm for its AI server opportunities). Snap (-9.8%, issued cautious guidance, the end of its Perplexity partnership, and uncertainty from Middle East headwinds).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is on a softer footing amid renewed downside in crude prices following headlines in Arabian press that a breakthrough may be reached between the US and Iran in the coming hours regarding the Strait of Hormuz. Further, Israeli press suggested Iran has agreed to transfer its 60% HEU to a third unknown country. That being said, it’s worth noting that none of the reports thus far have come from Iranian outlets. DXY resides in a 97.856-98.058 range, still within yesterday’s 97.625-98.342 parameter.

- G10 price action has largely been dictated by the Iranian war optimism. EUR/USD is back over 1.1750 in a 1.1741-1.1775 range and still within yesterday’s parameter.

- GBP/USD rose back above the 1.3600 mark but remains within Wednesday’s parameter, although traders also eye UK local elections. A full preview can be found on the headline feed, but in brief, a worse-than-expected outcome for the Labour Party could see renewed pressure on PM Starmer.

- USD/JPY is softer but only marginally, and within a narrow 156.02-156.53 range. Japanese participants returned overnight from Golden Week. Japan’s Chief FX Diplomat Mimura made comments earlier in the APAC session but refused to comment on FX intervention, and reiterated that FX is being closely watched. USD/JPY did see some fleeting pressure as Mimura spoke. Further on the FX front, US Treasury Secretary Bessent is to meet with Japanese PM Takaichi, Finance Minister Katayama and BoJ Governor Ueda for 3 days, starting Monday 11th, to discuss the weak yen.

- Antipodeans are firmer amid their high-beta properties coupled with upside across base and precious metals, albeit both the AUD/USD and NZD/USD pairs reside within the upper end of yesterday’s range.

FIXED INCOME

- A modestly firmer session for fixed benchmarks, driven higher by a pullback in energy this morning on a handful of constructive geopolitical updates ahead of the expected Iranian response, via Pakistan, to the US proposal.

- Updates that lifted the benchmarks from near-enough unchanged this morning to gains of a handful of ticks in USTs, but pertinently to a new WTD high of 111-01+. Bunds were similarly bid at the time, got to 126.12, also a new WTD peak, posting gains of 42 ticks at the time.

- Since, the benchmarks have pulled back modestly from the above peaks but remain in the green by a few ticks into an afternoon that is likely to be dominated once again by geopolitical updates, but the docket is also packed with data and Fed speak.

- For Gilts, they gapped higher by 31 ticks to a 87.70 session high, driven by the above geopolitical move being in full swing at the time. Gilts have also waned from best and currently hold onto gains of c. 10 ticks. Voting in the UK's local elections is now underway, polls close at 22:00BST. Thereafter, a drip feed of results will occur throughout the night and well into Friday, the results of which could spark the formal start of a leadership challenge against PM Starmer, in the days and weeks ahead.

- Saudi Arabia's PIF is offering three-, seven- & 30yr USD benchmarks bonds, Bloomberg reported citing sources; IPTs are USTs +130-170bps.

- Australia sold AUD 150mln 0.25% 2032 I/L bonds: b/c 3.97x, average yield 2.172%.

COMMODITIES

- Renewed downside was seen in crude prices following headlines in Arab press that a breakthrough may be reached between US and Iran in the coming hours regarding the Strait of Hormuz. Further, Israeli press suggested Iran has agreed to transfer its 60% HEU to a third unknown country. That being said, it’s worth noting that none of the reports thus far have come from Iranian outlets.

- Regarding the state of talks, US President Trump is optimistic about a framework, and Iran is expected to respond to the US proposal via mediators on Thursday. Axios reported Trump could still turn to military action without an agreement before his China trip. Iran is expected to provide its reply to the US proposal for ending the war to mediators on Thursday, CNN reported, citing a regional source. WSJ editorial said, from its discussions with senior officials, current US red lines in the talks include Iran confirming it does not seek nuclear weapons; the dismantlement of Fordow, Natanz and Isfahan; a ban on underground nuclear work; and on-demand inspections with penalties for violations.

- WTI and Brent futures have been trading off the hopes of oil flowing through the Strait once again. Brent July resides towards the bottom end of a USD 97.44-102.55/bbl range; WTI June sits towards the bottom of a 91.92-96.48/bbl range at the time of writing. Dutch TTF this morning dropped to EUR 42/MWh on the report from near EUR 45/MWH before stabilising around EUR 43.50/MWh.

- Spot gold topped Wednesday’s USD 4,723/oz high to reach a current peak of USD 4,753.43/oz, amid the aforementioned pullback in energy. Spot gold sees its 100 DMA at USD 4,774.67/oz.

- Base metals are mostly firmer as the pullback in crude prices bodes well for risk sentiment and broader global economic growth. That being said, 3M LME copper is flat within a USD 13,331.58-13,448.83/t range as it takes a breather from yesterday’s gains.

- Chinese Gold Reserves at 74.64mln troy oz at end-April (prev. 74.38mln in March); extends gold buying streak to 18 months.

- German government has rejected a return to nuclear power.

- A drone crashed into an oil storage facility in a Latvian town close to the Russian border, according to LSM.

- LME's CEO said it is ready to expand its suite of approved warehouses in Hong Kong.

- Australia set domestic gas reservation scheme at 20%.

- HKEX CEO said the LME warehouses approved in Hong Kong are close to full capacity.

- China has reportedly asked banks to pause new loans to US-sanctioned refiners, Bloomberg reported citing sources.

- The Trump administration is studying using oil under land at US military bases and other DoW sites to help refill the emergency reserves, Bloomberg reported citing sources.

- North Korea said it will not join the nuclear non-proliferation treaty, according to KCNA.

TRADE/TARIFFS

- A South Korean official said the country's first US investment under trade deal is to be announced after law takes effect in June.

- European Parliament's Top Negotiator said that good progress has been made in the EU-US talks though issues remain unsolved and that we will continue advancing progress and ensure stronger protections for citizens and businesses.

NOTABLE EUROPEAN HEADLINES

- A Cyprian official said EU countries and lawmakers have reached a provisional deal to delay the implementation of watered-down AI rules.

NOTABLE EUROPEAN DATA RECAP

- EU Retail Sales MoM (Mar) M/M -0.1% vs. Exp. -0.4% (Prev. -0.2%, Low. -1%, High. 0.3%).

- EU Retail Sales YoY (Mar) Y/Y 1.2% vs. Exp. 1% (Prev. 1.7%, Low. 0.2%, High. 1.5%).

- EU HCOB Construction PMI (Apr) 41.7 (Prev. 44.6).

- UK S&P Global Construction PMI (Apr) 39.7 vs. Exp. 46.2 (Prev. 45.6).

- Norwegian Norges Bank Interest Rate Decision 4.25% vs. Exp. 4.25% (Prev. 4%, Low. 4%, High. 4.25%).

- Swedish Riksbank Rate Decision 1.75% vs. Exp. 1.75% (Prev. 1.75%, Low. 1.75%, High. 1.75%).

- French HCOB Construction PMI (Apr) 38.1 (Prev. 38.4).

- French Balance of Trade (Mar) -6.9B vs. Exp. -5.6B (Prev. -5.8B).

- French Current Account (Mar) -8.20B (Prev. -1.8B).

- French Exports (Mar) 52.5B (Prev. 52B).

- French Imports (Mar) 59.3B (Prev. 57.8B).

- Italian HCOB Construction PMI (Apr) 44.8 (Prev. 46.8).

- German HCOB Construction PMI (Apr) 42.1 (Prev. 48.0).

- German Factory Orders MoM (Mar) M/M 5.0% vs. Exp. 1.1% (Prev. 0.9%, Low. -1.5%, High. 5%).

NOTABLE EUROPEAN EQUITY HEADLINES

- Palliser Capital has reportedly begun building a stake in FTSE-100 firm Autotrader Group (AUTO LN) and pushing for it to set out plans to return up to GBP 700mln to shareholders alongside full-year results this month, Sky News reported.

- Maersk (MAERSKB DC) CEO said if the Middle East situation becomes more peaceful, will then assess whether Red Sea transit can resume.

- Maersk (MAERSKB DC) Q1 2026 (USD): Revenue 12.97bln (prev. 13.32bln Y/Y), EBITDA 1.75bln (prev. 2.71bln Y/Y), PBT 292mln (prev. 1.43bln Y/Y); maintains FY outlook. The Middle East conflict had limited impact on the quarter's realised financial results.

- Shell (SHEL LN) Q1 2026 (USD): EPS 1.22 (exp. 1.06), Adj. EBITDA 17.7bln (exp. 15.1bln); announces a USD 3bln share buyback and a 5% quarterly dividend increase. Other Metrics. Adj. Earnings 6.915bln (prev. 3.256bln Y/Y),. CFFO 6.062bln (prev. 9.438bln Y/Y). Cash capex 4.202bln (prev. 6.015bln Y/Y). Free cash flow 2.9bln (prev. 4.2bln Y/Y). Net debt 52.6bln (prev. 45.7bln Y/Y). Gearing 23%, dividend +5% to 0.3906. Capex guide USD 24-26bln FY. Comments. Q2 2026 outlook reflects lower expected volumes and a weaker margin environment. Q2 2026 production outlook reflects higher planned maintenance across the portfolio. Q2 2026 production and liquefaction outlook reflects the impact of Middle East conflict including Qatar and higher planned maintenance across the portfolio.

- EU Transport Commissioner said airlines must continue to reimburse passengers for flight cancellations caused by high energy prices, the FT reported.

CENTRAL BANKS

- Fed's Goolsbee (2027 voter) said he is open to new ways of thinking about inflation. Overhauling the Fed's inflation framework is 'not an easy space'. Kevin Warsh has some fresh ideas worth thinking about. Fed should incorporate all the data it can, but he doesn't think there is a silver bullet for the inflation problem. He would be on the lookout for 'underheating' demand if low consumer confidence translates into falling consumer spending. US might be approaching an era of labour scarcity due to a combination of population aging and limited immigration.

- BoJ data up to April 30th shows Japan spent around JPY 4.68tln to support the JPY.

- BoJ Minutes from the March 18th-19th meeting stated that many members shared the view that it was appropriate to maintain the policy rate at 0.75%.

- ECB's Villeroy said they must be data dependent.

- ECB's Nagel said likely to raise interest rates unless the outlook improves markedly.

- ECB's Kocher said ECB is to consider hikes in the next months if there is no improvement; ECB is in data-dependent meeting-by-meeting mode.

- BoE officials are privately concerned that UK economic data may be sending false signals that complicate the job of setting interest rates, according to Bloomberg citing sources.

- RBNZ Governor Breman said higher near term inflation and weaker growth is somewhat expected, still expect growth this year.

- PBoC injected CNY 27bln via 7-day reverse repos with the rate maintained at 1.40%.

- PBoC set USD/CNY mid-point at 6.8487 vs exp. 6.8087 (prev. 6.8562).

- BoC Governor Macklem said inflation forecasts in the July monetary policy report will not change much after including the government fiscal update.

- BoC Governor Macklem said if oil prices keep rising and stay elevated "there may be a need for consecutive increases in the policy rate". If the United States imposes significant new trade restrictions on Canada, we may need to cut the policy rate further to support economic growth. Alternatively, if oil prices continue to increase, and particularly if they remain elevated, the risk that higher energy prices become ongoing generalized inflation increases. If this starts to happen, there may be a need for consecutive increases in the policy rate.

- Norges Bank hikes rates by 25bps to 4.25% (prev. 4.00%); "The Committee judges that a higher policy rate is needed to return inflation to target within a reasonable time horizon".

- Riksbank maintains its Policy Rate at 1.75% as expected, "there is scope to wait until there is a clearer picture", "current level of the policy rate gives a good initial position to adjust monetary policy if required to safeguard the inflation target".

NOTABLE US HEADLINES

- US Challenger Job Cuts (Apr) 83.387K (Prev. 60.62K)

- The US and China are considering launching official discussions on AI when US President Trump visits China next week, WSJ reported citing sources. With the proposed recurring conversations, risks from unexpected AI model behaviour, autonomous military systems, and attacks by non-state actors using open source tools will be addressed.

GEOPOLITICS

RUSSIA-UKRAINE

- Romanian Defence Ministry said a drone briefly breached Romanian airspace during a Russian attack on Ukraine.

- A drone crashed into an oil storage facility in a Latvian town close to the Russian border, according to LSM.

- Ukrainian President Zelensky said Russia has ignored our ceasefire proposal.

- Russian Foreign Ministry spokesperson said that Russia is ready to negotiate about Ukraine and emphasises that Moscow has never refused called and talks that have real results.

- Russia has decided to use its veto against the US-Gulf draft resolution on Hormuz; Russia rejects the chapter VII wording of the draft resolution on Hormuz, via Al Hadath.

CRYPTO

- Bitcoin is a little weaker this morning and trades around USD 81k, whilst Ethereum is extending losses down to USD 2.33k.

APAC TRADE

- Asia-Pac stocks traded broadly in the green, as a continuation of gains seen stateside as hopes of an end of the US-Iran conflict spurred risk-on flows.

- ASX 200 continued its rebound and is set for 2 consecutive days of gains. Miners were the biggest gainers while Energy names slumped. Shares of Tabcorp have nose-dived after the Co. stated that AUSTRAC has commenced an enforcement investigation with serious concerns over money laundering and terrorism financing risks.

- Nikkei 225 returned from its holiday with the need to catch up to the gains seen in equities while it was closed. As a result, the Nikkei surged to new ATHs and extended above the 63,000 handle, driven by tech majors SoftBank and Ibiden.

- KOSPI underperformed its APAC peers, as it consolidated following its surge beyond the 7,000 handle. SK Securities raised its PT for Samsung Electronics and SK Hynix to a price that is 88% and 87% higher, respectively, than their current price, reaffirming the tech strength.

- Shanghai Comp. and Hang Seng gained despite a lack of single-stock news. Continuing on the chip theme, Montage has overtaken CATL as the most expensive dual-listed stock in Hong Kong relative to its mainland shares.

NOTABLE ASIA-PAC HEADLINES

- Philippine's Economic Minister said controlling inflation, even if it will cost growth, is not necessarily bad.

- China's top diplomat Wang Yi met with a delegation led by Steve Daines on Thursday, Xinhua reported.

- South Korea's government is to invest KRW 30bln in a project aimed at establishing an AI data platform for autonomous vessels, Yonhap reported.

- Indonesia's Planning Minister said the 2027 government working plan is set with GDP growth target in a range of 5.9-7.5%.

- Hong Kong Financial Secretary Chan announces plans to promote the use of the CNY in commodity pricing.

- China rural banks have reportedly cut its deposit rates, with further cuts expected.

- Japan's Top FX Diplomat Mimura does not comment on FX intervention but said FX is being closely watched and are in daily contact with US authorities. IMF's classification of free floating regime does not restrict frequency of intervention. Will not comment on FX levels. Too early to comment on US Treasury Secretary Bessent's upcoming visit.

- US Treasury Bessent is to meet with Japanese PM Takaichi, Finance Minister Katayama and BoJ Governor Ueda for 3 days, starting Monday 11th, to discuss the weak yen, Nikkei reported.

NOTABLE APAC DATA RECAP

- Chinese Foreign Exchange Reserves (Apr) 3.411T (Prev. 3.342T).

- Australian Exports MoM (Mar) M/M -2.7% (Prev. 4.9%).

- Australian Balance of Trade (Mar) -1.841B vs. Exp. 4.45B (Prev. 5.686B).

- Australian Imports MoM (Mar) M/M 14.1% (Prev. -3.2%).

- Japanese Monetary Base YoY Y/Y -11.3% vs. Exp. -10.5% (Prev. -11.6%).

NOTABLE GLOBAL EQUITY HEADLINES

- New Zealand's Defence Minister said they are in talks with Australia and the UK to replace its Navy frigates.

Loading...