DXY firms alongside crude, equities broadly bid despite some Chinese ADRs hit; Waller and Warsh ahead - Newsquawk US Market Open

- Al Arabiya and Al Hadath exclusively report the text of the anticipated US-Iran agreement in case of its approval. A Pakistani source said that cautious optimism is the prevailing sentiment in the ongoing discussions regarding the planned agreement.

- However, another Pakistani source said the US and Iran's insistence on raising the bar for their demand regarding uranium and the Strait of Hormuz has led to a "crisis in negotiations."

- Crude on a firmer footing despite diplomatic efforts.

- Global equities set to end the week with gains, ahead of the UK/US extended weekend.

- FX broadly within Thursday's wide ranges; GBP unfazed by PSNB and retail sales, AUD weaker as banks shift tightening call.

- Fixed income higher, Gilts benefit from cooler-than-expected Retail Sales.

- Looking ahead, highlights include Canadian Retail Sales (Mar), University of Michigan Consumer Sentiment Final (May), BoC SLOS (May), Kevin Warsh sworn in as Fed Chair with US President Trump to attend. Speakers include Fed's Waller. Credit Ratings: Scope Ratings on China, S&P on Norway, Moody's on Hungary, Portugal & UK.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- Al Arabiya and Al Hadath exclusively report the text of the anticipated US-Iran agreement in case of its approval. The agreement includes: an immediate, comprehensive, and unconditional ceasefire on all fronts, a halt to military operations, ensuring freedom of navigation in the Arabian Gulf, the Strait of Hormuz, and the Sea of Oman and establishing a joint mechanism for monitoring and resolving disputes.

- US Secretary of State Rubio said there has been slight progress on Iran. Iran is trying to create a tolling system in the Strait, and no nation should accept that. We will be continuing talks with Iran, and there is progress.

- "A Pakistani source says that cautious optimism is the prevailing sentiment in the ongoing discussions regarding the planned agreement.", Al Arabiya reported.

- Pakistan source said the US and Iran's insistence on raising the bar for their demand regarding uranium and the Strait of Hormuz has led to a "crisis in negotiations", Al Jazeera reported.

- Pakistani Interior Minister met again with Iran's Foreign Minister to study proposals for resolving disputes between US and Iran, Al Jazeera reported, citing the Pakistani Embassy.

- Pakistan's Interior Minister will remain in Tehran on Friday to continue consultations and meet with Iranian officials, while a high-level source said the Pakistani Army Chief would not travel to Tehran on Thursday night, according to Al Arabiya.

- Pakistan's Foreign Ministry spokesperson said China supports mediation efforts and has presented a 5-point initiative.

- Iranian National Security Commission member Rezei posted "These negotiations are probably also a hoax and the Americans have no desire for diplomacy"; says "instead of diplomats, send missiles to negotiate."

- Iranian Foreign Ministry said "Everything being circulated about the status of the negotiations is not accurate", Al ArabyTV reported.

- UAE official said there is a '50-50' chance of US-Iran Strait of Hormuz agreement, AFP reported.

- Unconfirmed reports of explosions in the UAE, Tasnim reported. Details of the explosions have not yet been released.

- Iraqi ports said search teams have been mobilised within territorial waters after contact was lost with two ships, while they did not receive any distress calls from the two Bolivian-flagged ships with which contact has been lost.

EUROPEAN TRADE

EQUITIES

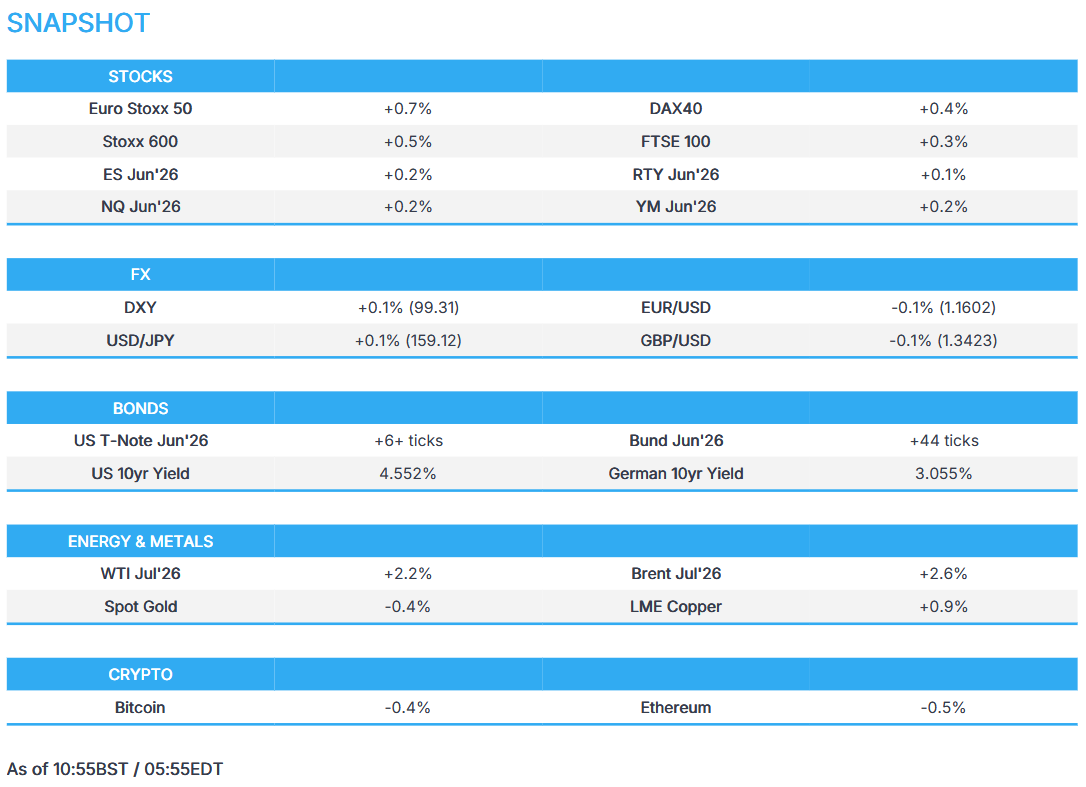

- European bourses (STOXX 600 +0.5%) start the final day of the week entirely in the green, heading into an extended weekend for UK and US assets. This follows comments by US Secretary of State Rubio, via the FT, noting "some good signs" in the US-Iran talks, while Reuters reported, citing an Iranian official, that "gaps have been narrowed". More recently, Al Arabiya released the text of the anticipated US-Iran agreement, which includes an immediate and unconditional ceasefire. However, commentary out of Iran earlier in the morning continues to downplay negotiations, with the Iranian Foreign Ministry saying that everything that has been circulated about the status of negotiations is inaccurate.

- Sectors highlight the positive bias. Technology (+1.8%) leads, closely followed by Telecoms (+1.3%) and Industrial Goods & Services (+0.9%). To the downside lie Real Estate (-0.6%) and Energy (-0.7%). Chemicals (+0.7%) are eking out mild gains despite a flurry of downgrades within the sector (IMCD/Arkema/Evonik to underweight by JPMorgan).

- US equity futures follow the positivity seen in European and Asian equities, with the ES (+0.2%) looking set for an 8th consecutive week of gains. The rebound from the week's earlier losses has been supported by the pullback in bond volatility.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is higher on the session after closing +0.1% in a choppy Thursday session, Antipodeans lag amid the risk environment and shifting tightening bets.

- Conflicting reports from the Gulf whipsawed the Buck on Thursday. Traders circulated fabricated reports that a final US-Iran draft had been reached, attributing the report to Al Arabiya, though this was later denied by the outlet. Despite this, progress in talks appears evident, while gaps remain on key issues, uranium and Hormuz. Energy benchmarks have rebounded, and as such, DXY is a touch firmer. The index resides well above significant DMAs, and within recent ranges - today supported by 99.20. Today sees the UoM final release for May.

- AUD is the worst G10 performer as domestic banks push back on RBA calls. Recent soft PMI, and labour market data which showed a surprise contraction in headline employment change, and an uptick in the unemployment rate prompted NAB and Westpac to push calls for tightening back to August, which both previously expected the first hike expected in June. AUD/USD resides within Thursday's ranges, remaining below 0.72 and supported by 0.71.

- GBP is unchanged against the Buck, and a touch firmer against the EUR. Retail Sales missed estimates, with the ONS noting that the poor figure was driven lower by fuel purchases. The PSNB figure also rose from April's print and overshot the OBR's forecast.

- EUR/GBP lower by 0.1% and within Thursday's broad ranges. Support around 0.8640. GBP/USD little changed, within recent ranges.

FIXED INCOME

- Global benchmarks are firmer this morning, albeit modestly so. Action throughout the week has been at the whim of mixed geopolitical newsflow, which has led to choppy trade across the energy space. Today, oil prices are firmer (Brent Jul +3%), but reside towards WTD lows. As such, fixed benchmarks trade with tentative gains this morning as negotiation efforts continue.

- USTs are firmer by a handful of ticks, though the bias throughout the European morning has been choppy. Nonetheless, US paper remains in the green and within a 109-08 to 109-14+ range. From a geopolitical front, Al Arabiya obtained the text of the anticipated agreement between the US and Iran. All key details can be found on the board at 09:16 BST, but the next sticking points incl. the exchanging of text, and then the beginning of negotiation, which the text suggested should begin within 7 days. Ahead, focus will be on speak from Fed’s Waller, where he will touch on the economic outlook, whilst the final US Michigan Consumer Sentiment is also scheduled. Yields have been of great attention this week, with the US 10yr printing multi-month highs (4.68%), whilst the 30yr soared to levels not seen since 2007 (5.2%). As for today, the 10yr is hovering towards WTD lows (4.56%) as markets remain focused on continued negotiations.

- Bunds are firmer by c. 35 ticks, and trade within a 125.06 to 125.30 range. German paper has ultimately followed peers, but has had some domestic data to digest. Early this morning, Final German GDP (Q/Q) was unrevised, whilst the Y/Y metric was revised slightly firmer. Overall, indicative of a resilient economy, though external leads (PMIs) suggest that this may be short-lived. This theme is also seen in the latest Ifo survey, which has stabilised since the last month, though still does not indicate any material improvement in sentiment.

- Gilts started with slight outperformance, but now trade alongside peers. Strength followed peers, with outperformance stemming from a cooler-than-expected Retail Sales report. ONS noted the poor figure was driven lower by fuel purchases, suggesting motorists had full tanks, or had stopped stockpiling as fuel prices stabilised higher, given the length of the energy disruption. The PSNB was also published, which rose to 24.3bln (prev. 12.6bln, exp. 24.3bln). Gilts trade within an 87.56 to 87.86 range.

COMMODITIES

- In terms of the latest on geopolitics, Al Arabiya/Al Hadath reportedly obtained a draft US-Iran agreement which, if approved, would see an immediate and unconditional ceasefire across all fronts. The draft also calls for a halt to military operations and media escalation, a commitment not to target military, civilian or economic infrastructure and guarantees for freedom of navigation in the Arabian Gulf, Strait of Hormuz and Sea of Oman. The agreement would take effect immediately once officially announced by both sides. Pakistan sources said the US and Iran's insistence on raising the bar for their demand regarding uranium and the Strait of Hormuz have led to a "crisis in negotiations”.

- WTI and Brent July futures are on a firmer footing heading into a weekend of risk, and with the sides reportedly hitting a crisis in talks amid raising the bar for demands regarding uranium and the Strait of Hormuz. WTI resides in a USD 96.92-99.43/bbl range while its Brent counterpart trades in a USD 103.77-106.36/bbl parameter.

- Spot gold and silver are softer amid the elevated crude prices. Spot gold trades within a narrow USD 4,507-4,546/oz range, while spot silver trades on either side of USD 76/oz in a USD 75.69-77.04/oz range.

- Base metal futures are mostly firmer amid the overall risk appetite across stocks amid ongoing headlines regarding Pakistani efforts to narrow the gaps between the US and Iran. 3M LME copper resides in a USD 13.56k-13.69k/t. Note that the LME is closed on Monday amid a UK bank holiday.

- China refined fuel exports (ex Hong-Kong) expected to rise slightly from May-June to around 550k MT, according to Reuters sources.

- Japan to receive first oil tanker to exit the Strait of Hormuz since US-Iran war began.

- Hungary's PM said an explosion took place at a MOL's Tiszaujvaros energy plant. One person dead and several injured.

- UAE Presidential Advisor said they were losing out in terms of production under OPEC, leaving it was under consideration for a three-year period.

- Barclays said they have maintained their Brent forecast of USD 100/bbl for 2026, with risks skewed higher.

TRADE/TARIFFS

- China adjusts drug-making chemicals export list to countries, reports suggest. Exports of relevant chemicals to the US, Mexico and Canada must apply for licenses in accordance with regulations.

- The EU has suspended customs tariffs on certain nitrogen-based fertilisers for one year.

NOTABLE EUROPEAN HEADLINES

- The next EU-UK summit could be postponed until July at the earliest (vs initial June date), Bloomberg reported citing sources. The prospect that substantial deals won’t be agreed in time.

- US Secretary of State Rubio said President Trump is disappointed with some NATO allies. Meeting will set groundwork for NATO leader’s summit.

- German Foreign Minister said defence spending will reach more than 4% of GDP in 2026 and on the way to 5%

NOTABLE EUROPEAN DATA RECAP

- UK Retail Sales MoM (Apr) M/M -1.3% vs. Exp. -0.6% (Prev. 0.7%, Low. -1.4%, High. 0.5%).

- UK Retail Sales YoY (Apr) Y/Y 0.0% vs. Exp. 1.3% (Prev. 1.7%, Low. 0.4%, High. 1.7%).

- UK Retail Sales ex Fuel MoM (Apr) M/M -0.4% vs. Exp. -0.3% (Prev. 0.2%, Low. -1.3%, High. 0.4%).

- UK Retail Sales ex Fuel YoY (Apr) Y/Y 1.1% vs. Exp. 1.5% (Prev. 1.7%, Low. 0.7%, High. 2.0%).

- UK Public Sector Net Borrowing Ex Banks (Apr) 24.3B vs. Exp. 20.9B (Prev. 12.6B, Low. 21.1B, High. 17B).

- UK Gfk Consumer Confidence (May) -23 vs. Exp. -28 (Prev. -25).

- German GDP Growth Rate QoQ Final (Q1) Q/Q 0.3% vs. Exp. 0.3% (Prev. 0.2%, Low. 0.2%, High. 0.3%).

- German GDP Growth Rate YoY Final (Q1) Y/Y 0.4% vs. Exp. 0.3% (Prev. 0.4%, Low. 0.3%, High. 0.3%).

- German Ifo Business Climate (May) 84.9 vs. Exp. 84.2 (Prev. 84.4, Low. 83, High. 85.9).

- German GfK Consumer Confidence (Jun) -29.8 vs. Exp. -34 (Prev. -33.3, Low. -35, High. -30).

CENTRAL BANKS

- ECB President Lagarde said long term inflation expectations are broadly well anchored and are particularly attentive to second-round effects.

- ECB's Demarco said the ECB will probably need to hike in June. There is not much evidence of indirect inflation effects and the 2026 inflation outlook likely to be revised upwardly. Projections to show if one hike is enough or more is needed.

- Westpac pushes back its RBA rate hike call to August and September from a previous call of June and August.

NOTABLE US HEADLINES

- US House Republicans delay war powers vote, according to Reuters.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukrainian President Zelensky said Ukraine attacked Russian oil refinery in Yaroslavl (300k BPD).

OTHER

- China Foreign Ministry said China firmly opposes the US selling arms to Taiwan.

- US President Trump announces that the US will be sending an additional 5,000 troops to Poland.

CRYPTO

- Bitcoin held above USD 77k, Ethereum extends lower and trades just below USD 2.2k.

APAC TRADE

- APAC stocks were mostly higher following the positive handover from Wall Street, where all major indices gained and the Dow notched a record close on what was a choppy session, amid cautious optimism due to contradicting geopolitical headlines.

- ASX 200 gained with outperformance in the mining, materials and resources sectors, although the upside in the broader market was capped by weakness in telecoms, real estate and defensives.

- Nikkei 225 rallied amid continued tech strength, with SoftBank shares adding to the recent advances with another double-digit percentage gain, while the latest inflation data was softer-than-expected and could compel policymakers to think twice about a June rate hike.

- Hang Seng and Shanghai Comp were in the green with the Hong Kong benchmark led higher by tech stocks, including Lenovo and NetEase, as the former was boosted by its earnings results, which showed record FY revenue, while the mainland kept afloat after the PBoC upped liquidity efforts for a third day.

NOTABLE ASIA-PAC HEADLINES

- Chinese regulators and exchanges intensify scrutiny of AI-fuelled market frenzy, pressing listed firms and fund managers to justify valuations, Bloomberg reported citing sources.

- China CSRC and seven other departments said they will establish a routine collaborative regulatory mechanism to conduct comprehensive monitoring and inspections. CSRC plans penalties against Futu Holdings, Up Fintech’s Tiger Brokers and Longbridge Securities, including confiscating illegal gains.

- China's NDRC said regarding the question on investment from the US, that they never told Chinese tech firms they couldn't take foreign investment, while it added that foreign investment must follow Chinese laws and rules, and should not harm national security and interests. Furthermore, it is planning a policy support framework to accelerate AI commercialisation, and stated that prices are set to remain stable as the domestic supply demand outlook improves.

- RBI is said to be likely selling dollars through state-run banks.

NOTABLE APAC DATA RECAP

- Japanese Inflation Rate YY (Apr) 1.4% vs Exp. 1.8% (Prev. 1.5%).

- Japanese Inflation Rate Ex-Fresh Food YY (Apr) 1.4% vs. Exp. 1.7% (Prev. 1.8%, Low. 1.6%, High. 1.8%).

- Japanese Inflation Rate Ex-Food and Energy YY (Apr) 1.9% vs. Exp. 2.2% (Prev. 2.4%).

Loading...