DXY firms alongside energy benchmarks, fixed income falters with crude at $103/bbl - Newsquawk US Market Open

- "Somalia closes Bab al-Mandab Strait to Israeli shipping", IRNA reports; "The move comes as a direct response to Israel’s recognition of the breakaway region of Somaliland, Yemen Press Agency reported on Wednesday".

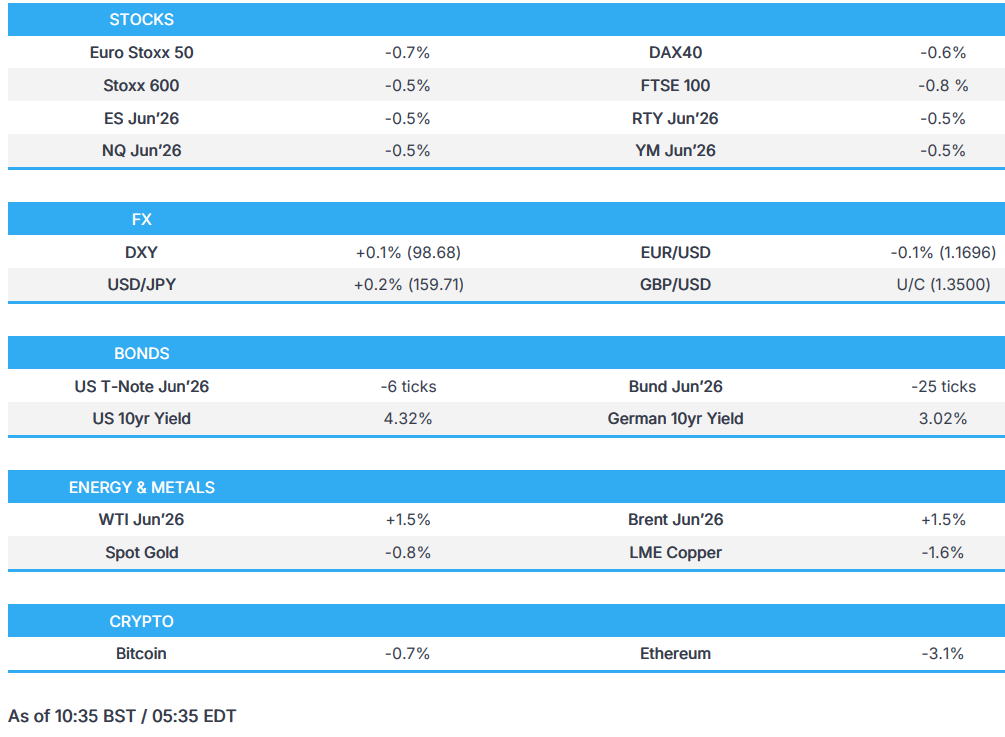

- European bourses are mostly lower; US equity futures also extend lower, TSLA -2.7% post-earnings.

- USD and NOK outperform, GBP shrugs off political instability as PMIs firm, NZD underperforms.

- EZ PMIs initially helped fixed income off lows, but an inflationary UK release sparked new lows.

- Geopolitics keeps crude prices underpinned and metals softer amid a firmer USD.

- Looking ahead, highlights include Global Flash PMIs (Apr), Mexican Inflation (Apr), Canadian PPI (Mar), US Jobless Claims (Apr/18). Supply from the US. Earnings from Blackstone, Freeport-McMoran, American Airlines, Keurig Dr Pepper, Intel, Lockheed Martin, and SAP.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

IRAN

- Sources familiar with Trump admin's moves say "the next stages have already been set"; "After the ceasefire ends, an overwhelming military strike is expected to go ahead, with even greater force than the one the US has inflicted on Iran so far". According to the source, the ceasefire that Trump decided to extend will end within a few days. After that, an overwhelming military strike will be launched, with even greater force than the one the US has inflicted on Iran so far. That attack will continue for several days, after which the military operations against Iran will come to an end.

- Iran Parliament Deputy Speaker said the first payments from Hormuz Strait toll has been transferred to Iran's central bank, Tasnim reported.

- Iran’s Supreme Leader Khamenei opposes extending negotiations under current conditions, according to an Iranian parliament national security member.

- "Somalia closes Bab al-Mandab Strait to Israeli shipping", IRNA reported; "The move comes as a direct response to Israel’s recognition of the breakaway region of Somaliland, Yemen Press Agency reported on Wednesday". "external meddling could lead to countermeasures, such as restricting access to the key maritime route of Bab al-Mandab.".

- Israel and Lebanon talks in the US are slated for Thursday at 16:00EDT/21:00BST.

- Pakistani Interior Minister said, "We expect to make progress with Iran regarding the negotiations", Al Hadath reported.

- Iranian opposition sources said air defences were activated in Iran last night against unmanned aerial vehicles, according to N12.

- Iranian-American academic Marani said if Iran's infrastructure is attacked, there will be a lot of heat in the region, SNN reported; adds that people should leave Gulf countries if US President Trump carries out his threat to bomb critical infrastructure.

- Ukrainian President Zelensky said a longer Iran conflict could boost the risk for Ukraine's missile defences, added that US anti-missile production is limited.

- Iran sends a protest letter to the UN Security Council and said US and Israel fully responsible for illegal attacks, while Iran demands serious response to attacks on infrastructure, according to ISNA.

- Lebanon PM said Israel's targeting of journalists and obstruction of relief efforts constitute war crimes.

- US Senate votes 46-51 against limiting US President Trump's Iran war powers, rejecting a fifth attempt to limit Trump's Iran war powers, according to CBS.

- Five Palestinians were reportedly killed in an Israeli strike on Gaza.

- Iran seizes two ships in the Strait of Hormuz citing violations and dangerous navigation, according to SNN.

- The Trump administration is exploring ways to reset ties Eritrea along the Red Sea coast line amid US/Iran war, via WSJ.

- Lebanon is to request a one-month ceasefire extension in Washington talks, according to NNA.

- Iranian Foreign Minister Araghchi tells South Korea envoy that aggressors are responsible for all fallout from the war, according to Yonhap.

- British military divers are preparing to conduct mine-clearing operations in the case that they are needed in the Strait of Hormuz, according to POLITICO citing the UK MoD.

- US Central Command has commented on the Strait of Hormuz blockade, stating that 31 vessels have been directed to turn around from the blockade, adds no vessels are allowed to enter or exit Iranian ports.

- Saudi Arabia rejects Israeli project for Hormuz alternative, according to ISNA.

- The US military intercepts at least 3 Iranian oil tankers in Asian waters and are redirecting the tankers, according to shipping and security sources.

EQUITIES

- European bourses opened mostly lower, and price action has been fairly tentative since the cash open. In terms of individual indices, the AEX (-1%) underperforms, whilst the SMI (+1%) outperforms. The former lags, with ASML (-3%) weighing on the index; the Swiss index has been buoyed by post-earnings strength in both Nestle (+6.9%) and Roche (+2.2%). In a bit more detail, Nestle reported strong Q1 organic sales and maintained its outlook.

- European sectors hold a negative bias this morning. Telecoms takes pole position, led higher by Nokia (+10%) and Orange (+3.5%); the former reports 4% sales growth in Q1, benefiting from the recent AI boom. Food, Beverage & Tobacco takes second spot, helped by Nestle, whilst Energy completes the top three.

- US equity futures are broadly in the red, continuing the downbeat risk tone seen across Europe. In pre-market trade, Tesla (-2.6%, revenue miss & spending rise), Texas Instruments (+10%, upbeat guidance), IBM (-7.4%, u/c guidance offsets beat). Ahead, US jobless claims, PMI and a slew of earnings.

- Tesla (-2.6%): Despite an earnings beat and stronger auto margins, revenue missed expectations, and it said spending would be higher than previously guided.

- Texas Instruments (+10%): Q1 beat and better than expected guidance, driven by data-centre demand, a broad industrial recovery, rising optimism about further growth ahead.

- IBM (-7.4%): Q1 EPS 1.91 (exp. 1.81), Q1 revenue USD 15.92bln (exp. 15.65bln). Said Q1 was a strong start to the year with broad-based revenue growth across segments.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10 FX is showing a picture of higher oil prices, with USD and NOK outperforming.

- NZD is the worst performer today, but it remains positive for the week as markets continue to add to tightening bets: 90bps expected by year-end, 50/50 in May meeting, first fully priced in July. Aussie benefits from encouraging flash Manufacturing and Services PMI. AUD/NZD +0.2% after bouncing off support at Wednesday's low of 1.2105. In recent trade, the Antipodean cross found resistance at 1.2150.

- This morning saw the release of EZ flash PMIs, which were broadly lower and saw a bout of pressure in EUR. The ECB will welcome the French print, which noted passthrough to prices charged for goods and services was contained. The German and EZ-wide figures put the council in a trickier place, where both noted price pressures not seen since the pandemic. Ultimately, the ECB will likely stand pat on rates until it can gauge second-round effects. As mentioned, EUR saw modest downside on the French figure, and there was no reaction to German and EZ print despite inflationary indications. EUR/USD unchanged and either side of the 1.17 mark.

- EUR/GBP is also unchanged despite continued UK political developments, where the PM's cabinet loyalists are said to have turned on the PM, according to the Telegraph. For now, the pound is unreactive as the PM is broadly expected to remain in post-up to the May local elections. This morning saw a stronger-than-expected PMI release, and as the internals pointed to marked inflationary pressures, GBP saw upside, though it remains flat against the EUR. The cross continues to trade below the 0.87 handle, currently 0.8660, marking April lows.

FIXED INCOME

- Initial action was somewhat contained, as the morning was dominated by European earnings and the digestion of overnight/late-Wednesday geopolitical updates. On the latter, the main development was pushback against the three-to-five-day deadline from Trump to Iran.

- Following the European cash equity open, modest upside was seen on the French PMIs, where the metrics were mixed vs expectations, but more pertinently, the commentary noted that "the passthrough to prices charged for goods and services remains contained", i.e. no significant second-round effects at this point. On the release, Bunds notched a 125.42 high and OATs to 119.30.

- Thereafter, the German metrics were lower across the board, aside from an in-line manufacturing print. A release that spurred Bunds to a 125.55 peak, though still lower by 16 ticks on the day. Concerningly, the German series pointed to "signs of widening inflationary pressures".

- Overall, the EZ figures were lower on a services and composite level vs consensus, while the manufacturing print beat. Internally, the series showed the "biggest surge in cost pressures" since 2000 ex-COVID. Given this, Bunds fell from the aforementioned peak by around 10 ticks into the UK data, as yields picked up across the curve but particularly at the short end as the curve flattens.

- Onto the UK, where the PMI release appears to have sparked some across-the-board selling in fixed income, taking USTs back to 111-00, though above the 110-31 trough. Bunds down to 125.38, but above the 125.06 base. The UK series was firmer across the board, sending Gilts lower in a knee-jerk by 15 ticks and then further to a 87.02 low, lower by over 80 ticks on the day, on the internal commentary. Commentary that pointed to some renewed momentum in the economy, though caveated, and more pertinently to significant price rises.

- For the BoE, the data will add to calls for tightening. However, the majority of Threadneedle St. will likely, on balance, take the view that they can wait for more data before acting, particularly given the hits to business and employment confidence.

- UK DMO Remit, Revision: 2026/27 Gilt issuance of GBP 246.2bln (prelim. 252.1bln). Breakdown (GBP). T-bill: 5bln (prelim. 5bln). Short: (prelim. 97.3bln). Medium: (prelim. 57.8bln). Long: (prelim. 8bln). I/L: (prelim. 16.5bln).

- Australia sold AUD 150mln in 2035 indexed bonds, b/c 4.10, avg. yield 2.4756%.

COMMODITIES

- In geopolitics, US President Trump said Iran’s Foreign Minister Araghchi is expected to remain involved in ongoing talks with Iran, while dismissing reports of a proposed 3–5-day ceasefire as inaccurate, according to Fox News. The White House Press Secretary echoed this, noting that Trump has not set a firm deadline for an Iranian proposal and reiterating that the reported ceasefire timeline is incorrect, adding that any ceasefire timing would ultimately be determined by Trump.

- Meanwhile, Israeli media reports suggest a more urgent timeline. Sources indicated that Washington is aiming to reach concrete understandings with Iran by Sunday, rather than merely initiating negotiations. N12 reported that Trump’s deadline for Iran falls this coming Sunday. Additionally, according to Israel’s Hayom, sources familiar with the Trump administration’s plans claimed that “next stages have already been set,” and reportedly include the end of a ceasefire within days, followed by a significant military strike and several days of continued operations before concluding.

- Overnight, crude futures saw an early aggressive move higher, rising by 4% in under 10 minutes, though the upside was faded shortly afterwards, amid a lack of fresh drivers behind the move. This morning, WTI and Brent June futures remain underpinned, with the latter now north of USD 103/bbl (in a USD 101.58-106.15 range). WTI trades around USD 94/bbl in a USD 92.33-97.22/bbl range. Nat gas futures are firmer by around 4% around EUR 45/MWh.

- Spot gold and silver are softer as the rise in oil prices keeps the USD supported. Spot gold dipped under its 100 DMA (at USD 4,735.45/oz) again, and currently resides in a USD 4,692-4,754/oz range. Spot silver remains under its 100 DMA (around USD 78.86/oz; ranging between USD 75.57-78.38/oz). Both remain within Tuesday’s parameters.

- Base metals are softer across the board amid the USD strength, and inflation concerns arising from the elevated oil prices. 3M LME copper trades in a USD 13,208.20-13,486.00/t range at the time of writing.

- IEA's Birol said expect nuclear power to get a "big boost" following Iran war, via CNBC TV.

- Slovakia said that as of 2AM CET, Druzhba flows have resumed, oil deliveries are currently proceeding in line with the agreed plan.

- Chinese Ministry of Agriculture said fertiliser supply is ample for spring farming, with domestic prices well below international levels.

- Chevron (CVX) announces the resumption of full production at wheatstone LNG following the outage in March.

TRADE/TARIFFS

- A number of EU member countries have resisted called from the French to overhaul a US trade deal, Politico reported citing people familiar with the matter.

- China's He said MOFCOM advises Chinese firms to seek a refund of US tariffs; US tax refund measures are a positive step in correcting mistakes.

- US House Foreign Affairs Committee advanced 20 bipartisan bills to tighten US export controls on AI and semiconductor technology to China.

NOTABLE EUROPEAN HEADLINES

- Japan is reportedly pushing the EU to revise its homemade EV incentives.

- Cabinet loyalists have turned on UK PM Starmer in a growing backlash over his handling of the Mandelson scandal, with a senior Government source telling the Telegraph that the wheels have stopped turning in No. 10 and that there is a sense that it is over.

NOTABLE EUROPEAN DATA RECAP

- UK S&P Global Manufacturing PMI Flash (Apr) 53.6 vs. Exp. 49.5 (Prev. 51.0, Low. 48, High. 51.8).

- UK S&P Global Services PMI Flash (Apr) 52.0 vs. Exp. 49.9 (Prev. 50.5, Low. 49, High. 50.7).

- UK S&P Global Composite PMI Flash (Apr) 52.0 vs. Exp. 50.2 (Prev. 50.3, Low. 49, High. 50.2).

- UK Public Sector Net Borrowing Ex Banks (Mar) 12.6B vs. exp. 10.4bln (Prev. 14.3B, Low. -7.4B, High. 16B); the lowest March borrowing since 2022.

- EU S&P Global Manufacturing PMI Flash (Apr) 52.2 vs. Exp. 50.9 (Prev. 51.6, Low. 49.6, High. 51.6).

- EU S&P Global Composite PMI Flash (Apr) 48.6 (Prev. 50.7, Low. 49.5, High. 51); “If the Covid-19 pandemic is excluded, this is the biggest surge in cost pressures that we have recorded since 2000".

- EU S&P Global Services PMI Flash (Apr) 47.4 vs. Exp. 49.9 (Prev. 50.2, Low. 49.2, High. 50.5).

- German S&P Global Composite PMI Flash (Apr) 48.3 (Prev. 51.9, Low. 50.2, High. 52); "Faced with rapidly increasing costs, firms raised average prices ... at the quickest rate in over three years in April, in a sign of widening inflationary pressures".

- German S&P Global Services PMI Flash (Apr) 46.9 vs. Exp. 50.4 (Prev. 50.9, Low. 49.5, High. 51.5).

- German S&P Global Manufacturing PMI Flash (Apr) 51.2 vs. Exp. 51.2 (Prev. 52.2, Low. 50.5, High. 52.2).

- French S&P Global Manufacturing PMI Flash (Apr) 52.8 vs. Exp. 49.5 (Prev. 50.0, Low. 48.8, High. 50).

- French S&P Global Services PMI Flash (Apr) 46.5 vs. Exp. 48.5 (Prev. 48.8, Low. 48, High. 49.5).

- French S&P Global Composite PMI Flash (Apr) 47.6 (Prev. 48.8, Low. 48, High. 49.5); "What's most notable is that the passthrough to prices charged for goods and services remains contained".

- French Business Confidence (Apr) 100 vs. Exp. 98 (Prev. 99, Low. 96, High. 99).

- French Business Climate Indicator (Apr) 94 (Prev. 97, Low. 96, High. 98).

CENTRAL BANKS

- ECB is likely to maintain key rates at the April 30th meeting with the deposit rate seen to be maintained at 2.0% for the 7th consecutive meeting, according to Nikkei.

- BoK and South Korea's Finance Ministry are to strengthen harmonious policy coordination, with Finance Minister Koo and BoK's new Governor Shin set to maintain close communication through regular market meetings.

NOTABLE US HEADLINES

- US Senate Majority Leader Thune said he does not have assurances from Speaker Johnson that the House will pass it as-is, Punchbowl reported. Thune expressed frustration with the House over the broader DHS funding bill too and wants the White House to get more engaged.

- US Senate has reportedly approved a USD 70bln funding blueprint for ICE and border patrol, according to reported.

- New Zealand's Finance Minister said the Treasury projects inflation could reach 7.4% in 2025/26 under the worst-case scenario. Forecasts unemployment rate at 5.7% and real GDP of 0.8% if oil at USD 180/bbl. Seems highly unlikely that oil will hit USD 180/bbl. Economic recovery is delayed not derailed.

- US Treasury is launching the Investment Security Technology Initiate to convene leading experts and strengthen the safeguarding of critical investments and emerging technologies.

- US Pentagon said Navy Secretary Phelan is stepping down, effective immediately.

- US Senator Thune said a vote-a-rama could be tonight or tomorrow, according to a POLITICO reporter.

- White House Economic Advisor Hassett said inflation is very much declining at the core level and that falling inflation should help the Fed normalise rates, can imagine rate cuts alongside reducing balance sheet. President Trump wants Kevin Warsh at the Fed as soon as possible. Kevin Warsh will open up the books at the Fed to show what happened. Sure there will be talks on how to move Warsh forward.

CRYPTO

- Bitcoin is a little lower and trades around USD 78k; Ethereum dips lower and trades around USD 2.3k.

APAC TRADE

- APAC stocks were mostly negative despite the positive handover from Wall Street, with risk appetite souring amid higher oil prices and following the recent bout of mixed geopolitical headlines

- ASX 200 declined with the downside led by weakness in the consumer-related sectors and with nearly all industries subdued aside from energy, while the improvement in PMI data, which returned to expansionary territory, did little to spur a rebound.

- Nikkei 225 swung between gains and losses, in which the index retreated after hitting a fresh record high above the 60,000 level, with pressure seen amid fluctuations in oil.

- Hang Seng and Shanghai Comp were lower amid a slew of earnings updates and as the weakness seen in retailers and autos clouded over the gains in the energy majors.

NOTABLE ASIA-PAC HEADLINES

- Japan and Saudi leaders held a phone call, according to Japanese press.

NOTABLE APAC DATA RECAP

- Indian HSBC Services PMI Flash (Apr) 57.9 (Prev. 57.5).

- Indian HSBC Manufacturing PMI Flash (Apr) 55.9 (Prev. 53.9).

- Indian HSBC Composite PMI Flash (Apr) 58.30 (Prev. 57.0).

- New Zealand Credit Card Spending YoY (Mar) Y/Y 2.1% (Prev. -1.1%).

- Japanese S&P Global Services PMI Flash (Apr) 51.2 vs. Exp. 52 (Prev. 53.4).

- Japanese Stock Investment by Foreigners (Apr/18) 2380.9bln (prev. 3941.4bln).

- Japanese Foreign Bond Investment (Apr/18) -12.8bln (prev. 698.2bln).

- Australian S&P Global Manufacturing PMI Flash (Apr) 51.0 vs. Exp. 49 (Prev. 49.8).

- Australian S&P Global Services PMI Flash (Apr) 50.3 vs. Exp. 46 (Prev. 46.3).

- Australian S&P Global Composite PMI Flash (Apr) 50.1 vs. Exp. 46.3 (Prev. 46.6).

Loading...