DXY firms in tandem with Energy benchmarks amidst a US and Iran flare-up; Stocks firm as NVDA/MSFT unveil PC chip - Newsquawk US Market Open

- US President Trump sent tougher terms to Iran re. the peace framework, NY Times reported. Tasnim outlined that Iran could propose changes to the MOU.

- Israel expanded its ground offensive in Lebanon; PM Netanyahu said that it will attack targets in the southern suburbs of Beirut.

- Iran's FM Baghaei said that a ceasefire in Lebanon is an integral part of any agreement, adding that they are considering options for responding to the escalation of Israeli attacks in Lebanon.

- Crude benchmarks gain amidst a US and Iran flare-up and after Kuwait reports drone attacks; Brent Aug’26 +3%.

- Tentative trade across European/US equity futures; focus on Nvidia (+1.9%) and Microsoft (+2.9%) after debuting a new AI PC chip.

- DXY incrementally firmer, GBP marginally leads, whilst the Kiwi lags.

- Looking ahead, highlights include Global Manufacturing Final PMIs (May), US ISM Manufacturing (May), and Atlanta Fed GDP.

IRAN CONFLICT

IRANIAN COMMENTARY

- Iran may propose changes to the US peace draft memorandum of understanding, according to Tasnim. This follows a report that President Trump proposed further changes to the existing text, while a source stated that text exchanges continue and that Iran may submit its own edits.

- Iranian Foreign Minister Araghchi told state media that talks and message exchanges with the US are ongoing, and that the talks cannot be judged until a clear result is reached.

- Iranian Foreign Ministry Spokesperson said the negotiation team's visit to Qatar was positive.

- Iranian Foreign Ministry spokesperson said that they have a legal obligation to prevent aggressors from using their territory and facilities to attack another country.

- Iran’s Presidential Office denied reports that Iranian President Pezeshkian submitted his resignation to the Supreme Leader, and stated that the stories were spread by some foreign media.

- Iranian Supreme Leader’s military adviser Mohsen Rezaei said Iran has no intention of yielding or compromising with the US and will not place itself in a weak position, while he also stated that US President Trump is betraying diplomacy for the third time by continuing a naval blockade on Iran and making excessive demands.

- IRGC said following aggression of US Army on a communication tower on Sirik Island, located in the Homozgan province an hour ago, fighters of the IRGC Aerospace Force targeted airbase where aggression originated and predicted targets were destroyed.

- Iran's top negotiator said "The naval blockade and escalation of war crimes in Lebanon by the genocidal Zionist regime are clear evidence of US noncompliance with the ceasefire".

- Iranian Foreign Ministry Spokesperson said at this moment they do not believe that the US has good intentions towards Iran.

- Iran's FM Baghaei said "No negotiations have taken place on the details of the nuclear issue at this stage". One point being discussed is the allocation of funds for reconstruction. We are considering options for responding to the escalation of Israeli attacks in Lebanon.

- Iran's Baghaei said a ceasefire in Lebanon is an integral part of any agreement and end to the war; lack of trust and constant change in US and Israeli positions in Lebanon are causing a delay on the diplomatic process. The continuation of maritime piracy and attacks on Iranian shipping is an example of a violation of the ceasefire. The diplomatic apparatus is closely following developments and we will take every measure to defend Iran's sovereignty. The exchange of messages is still ongoing.

- Iran's Deputy Foreign Minister Gharibabadi said Iran's goal is not to hold ships in the Strait, but to declare a procedure that is not contrary to international law; these arrangements are not temporary and Iran will not back down. Stopping ships behind the Strait of Hormuz incurs storage and delay costs, and war insurance has increased by up to 500%. Accompanying Iranian forces costs less than war insurance and eliminates the risk of stoppage, inspection, and seizure. Iran's goal is not to hold the ships, but to declare a procedure that is not contrary to international law; these arrangements are not temporary and Iran will not back down.

- "Three consecutive explosions were heard in Bandar Abbas", Iran International reported.

US COMMENTARY:

- US President Trump reportedly sent tougher terms to Iran regarding the peace framework, according to officials cited by The New York Times.

- US President Trump posted "Iran really wants to make a deal, and it will be a good one for the U.S.A. and those that are with us". Full post "Iran really wants to make a deal, and it will be a good one for the U.S.A. and those that are with us. But don’t the Dumocrats, and various seemingly unpatriotic Republicans, understand that it is MUCH tougher for me to properly do my job and negotiate, when political hacks keep negatively “chirping,” at levels never seen before, over and over again, that I should move faster, or move slower, or go to war, or not go to war, or whatever. Just sit back and relax, it will all work out well in the end - It always does! President DJT".

- US President Trump posted "Fake News CNN said today, routinely, that my Iran Nuclear Deal doesn’t talk about Nuclear, when actually it states, very clearly, that Iran will not have a Nuclear Weapon". Full post "ScraperFake News CNN said today, routinely, that my Iran Nuclear Deal doesn’t talk about Nuclear, when actually it states, very clearly, that Iran will not have a Nuclear Weapon. It then goes on, in very strong and lengthy detail, to discuss various other aspects of Nuclear. In fact, that’s what most of the agreement is about. CNN, and so many others in the Fake News Media, is a Low Ratings disaster. Even with new ownership, it is unlikely to ever get better!!! President DJT".

- US Secretary of State Rubio spoke in the last 48 hours with Lebanon's President and Israel's PM to try and promote a new ceasefire initiative, according to a senior US official cited by Axios's Ravid. said:. US senior official said that the new initiative was proposed as part of the negotiations taking place between Israel and Lebanon, as another round of talks between diplomats from both sides is scheduled to take place this week in Washington. In order to advance the talks, US proposed that as a first step, Hezbollah stop all attacks on Israel, and in return, Israel will refrain from escalation in Beirut.

- US Central Command confirmed military forces conducted strikes against Iranian radar at command and control sites located in Goruk and Qeshm Island over the weekend.

- Kuwait Army said air defences are intercepting hostile missile and drone attacks.

LEBANON

- Israeli PM Netanyahu said they will attack targets in the southern suburbs of Beirut, in response to Hezbollah violating the ceasefire agreement.

- "Walla News, citing a source: Washington is open to Israel's request to expand its military operation in Lebanon", Al Araby reported.

- Israeli jets hit Al-Qatrani, Al-Mawahani and Bin Jabal in Lebanon, according to IRIB.

- Sirens sounded in Tiberias and surrounding areas after rockets were launched from Lebanon.

- Lebanon is intensifying its efforts to solidify the ceasefire and is conducting international contacts, particularly with the Americans, in light of Israeli threats, Al-Araby reported citing sources. Talks with the US are still scheduled for tomorrow.

EUROPEAN TRADE

EQUITIES

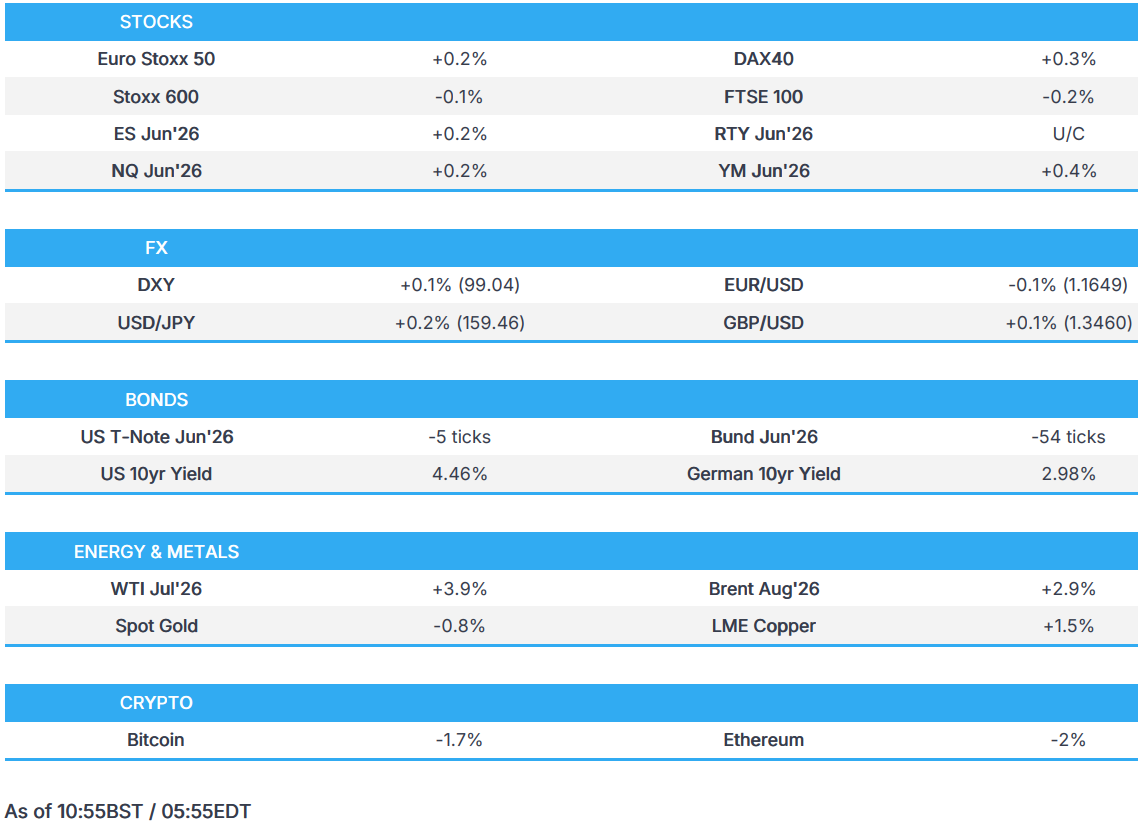

- European bourses are broadly lower this morning, as markets digest another flare-up between the US and Iran, with Israel also seemingly upping its presence in southern Lebanon once again. From an index perspective, the AEX (-0.4%) mildly underperforms whilst the DAX 40 (+0.2%) holds afloat.

- European sectors are mixed. Energy unsurprisingly tops the pile, given the gains in underlying oil prices; Tech and Basic Resources complete the top three. To the downside reside Media and then Healthcare; the former has been weighed by losses in UMG (-2%), after it rejected Pershing Square’s unsolicited offer.

- US equity futures are incrementally firmer/flat. The ES/NQ (+0.2%) post incremental gains, whilst the RTY (U/C) holds around the unchanged mark. Tentative action encapsulated by the uncertain geopolitical environment, but focus ahead will turn to key data incl. ISM Manufacturing and Final Manufacturing PMIs. The former takes more focus where the headline is expected at 53.0 (prev. 52.7).

- Nvidia (+1.8%) and Microsoft (+3%) unveiled RTX Spark, a 1-petaflop superchip for Windows PCs built for personal AI agents.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- Mixed performance across G10s with most currencies lower against the Greenback (ex. GBP/NOK given oil/yield moves.)

- GBP is the mild outperformer after reporting over the weekend suggested unofficial UK PM candidate Burnham was eyeing right-leaning Home Secretary Shabana Mahmood as potential Chancellor. The Sun reported Mahmood “is meant to have done a deal with Burnham”. Mahmood has previously defended efforts to reduce the amount spent on welfare, and is known for a right-leaning stance on immigration. Though these updates are speculative at the moment, Sterling has attracted buyers and is one of the only G10 currencies positive against the Buck. GBP/USD +0.1%, EUR/GBP -0.1%.

- USD is unchanged/modestly firmer and either side of the 99.00 mark. No US-specific newsflow over the weekend, just Geopolitics as explained below. Set to be a busy week of Labour market data, today sees the release of S&P/ISM manufacturing PMIs, Tuesday sees JOLTs Job Openings, ADP weekly payrolls on Wednesday, Challenger layoffs on Thursday, and then NFP on Friday. ING writes, “Should the jobs data stay supportive and price pressures through the ISM surveys remain intense, markets can probably shift towards pricing one full 25bp Fed rate hike this year. That compares to +17bp of tightening priced currently.”

- NOK is being helped by energy benchmarks with Brent Aug’26 +3% after NYT reported Trump sent tougher terms to Iran regarding the peace framework, Tasnim outlined that Iran could propose changes to the MoU, while both sides exchanged fire over the weekend. USD/NOK -0.2%, NOK/SEK +0.5%.

- Aussie lacks direction after mixed Chinese PMI data overnight, while Kiwi lacks demand with domestic participants absent amid a market holiday. AUD/NZD +0.4%, AUD/USD U/C, NZD/USD -0.5%.

FIXED INCOME

- A softer start for fixed income as the energy space climbed in APAC hours, given a handful of detrimental updates on the US-Iran situation. Since, the press conference from Iran's spokesperson has provided further support to energy, with Araghchi noting that no negotiations have taken place on the details of the nuclear issue.

- USTs and Bunds lower overnight, in proximity to the troughs from Friday. Gilts opened lower by around 35 ticks and then slipped a handful more to a 88.31 trough, pressured but comfortably clear of levels below 88.00 at 87.94 and 87.86 from last week.

- USTs and Bunds are similarly at lows, down by five and 50 ticks respectively. Specifics for the US and Europe are a little light aside from a few Central Bank speakers, with the focus firmly on any geopolitical update(s) or a significant change to the equity space. On the latter, the focus has been firmly on South Korea given the stellar gains in the market YTD and the ongoing marked strength seen today, i.e. Samsung Electronics +10%.

- No move to the final PMIs for the EZ and UK thus far. Ahead, we get the US ISM Manufacturing PMI before the latest Atlanta Fed.

COMMODITIES

- The geopolitical environment is clouded by uncertainty, with a recent flare-up between the US and Iran once again leading to firmer trade in crude benchmarks. In brief, the US Central Command said that military forces conducted strikes against Iranian radar at command and control sites located in Goruk and Qeshm Island – this was then met with IRGC retaliation. Outside of Iran, Kuwait said air defences were intercepting hostile missile and drone attacks.

- As for the journey to negotiations, the US and Iran are both reportedly altering the draft MoU. President Trump reportedly sent “tougher terms” regarding the framework, NYT reported. In response, Tasnim suggested that Iran may propose its own changes.

- As for the European day, there have been a few appearances from Iranian officials; Deputy FM for Legal Affairs Gharibabadi noted that Iran’s goal is to accompany ships through the Strait, and “these arrangements are not temporary and Iran will not back down”. Elsewhere, Iran's FM Baghaei said, "no negotiations have taken place on the details of the nuclear issue at this stage". Comments which helped the upward bias in oil benchmarks.

- WTI and Brent are stronger this morning by c. 4.1% and 3.1% respectively. Prices gapped up at the open, and gradually moved higher as the session progressed; as it stands, the complex resides towards highs. WTI trades within a USD 88.45-91.26/bbl range, whilst Brent holds at the upper end of a USD 90.05-92.11/bbl range.

- Spot gold is lower by around a per cent and currently resides within a USD 4,490-4,546/oz range, and towards the bottom end of Friday’s range. Ultimately, action is dictated by the inflationary implications of heightened geopolitical risk. Elsewhere, base metals are broadly firmer, following on from a positive APAC session overnight. 3M LME copper posts gains of c. 1.4% and currently trades towards the day’s peaks, within a USD 13,635.4-13,814/t range.

- Russia to ban jet fuel exports until the end of November, Ifx reported.

- Citigroup raises its near-term copper price forecast to USD 14,500 per metric tonne and set a 6-12 month target of USD 15,000 per metric tonne.

TRADE/TARIFFS

- UK Business Secretary Kyle set to travel to India this week for talks about the recent trade deal as well as steel tariff measures announced by the government in March, SKY news reported.

- China's State Council said new rules regarding China tightening oversight of outbound investments in selected technologies take effect July 1st.

- China vowed to resolutely retaliate if the EU proceeds with new restrictive trade measures, following a European Commission discussion on China policy last Friday.

NOTABLE EUROPEAN HEADLINES

- Hungarian PM Magyar said will amend constitution to oust Hungarian President.

- Morningstar DBRS confirms Spain at A (high), Stable Trend.

- S&P affirms Hungary at BBB-; Outlook negative.

- Former UK Health Secretary and potential leadership contender Wes Streeting flagged the idea of lowering employers’ national insurance and favours new North Sea oil drilling.

- S&P confirmed France’s sovereign rating at A+; Outlook Stable, according to French Finance Minister Lescure.

- SoftBank pledged to spend at least USD 52bln on building a network of data centres in France as it seeks to deliver as much as 3.1 gigawatts of computing capacity in the country by 2031, according to WSJ.

NOTABLE EUROPEAN DATA RECAP

- EU Unemployment Rate (Apr) 6.3% (Prev. 6.2%).

- EU Loans to Households YoY (Apr) Y/Y 3% (Prev. 3%).

- EU S&P Global Manufacturing PMI Final (May) 51.6 vs. Exp. 51.4 (Prev. 52.2).

- EU Loans to Companies YoY (Apr) Y/Y 3.4% (Prev. 3.2%).

- EU M3 Money Supply YoY (Apr) Y/Y 2.7% (Prev. 3.2%).

- UK S&P Global Manufacturing PMI Final (May) 53.9 vs. Exp. 53.7 (Prev. 53.7).

- UK Nationwide Housing Prices YoY (May) Y/Y 1.7% (Prev. 3%).

- UK Nationwide Housing Prices MoM (May) M/M -0.6% (Prev. 0.4%).

- German S&P Global Manufacturing PMI Final (May) 50.1 vs. Exp. 49.9 (Prev. 51.4).

- German Retail Sales YoY (Apr) Y/Y -0.3% (Prev. -2%).

- German Retail Sales MoM (Apr) M/M -0.3% (Prev. -2%).

- French S&P Global Manufacturing PMI Final (May) 49.7 vs. Exp. 48.9 (Prev. 52.8).

- Italian S&P Global Manufacturing PMI (May) 52.9 (Prev. 52.1).

- Spanish S&P Global Manufacturing PMI (May) 51.2 (Prev. 51.7).

- Swiss GDP Growth Rate QoQ Final (Q1) Q/Q 0.7% vs. Exp. 0.5% (Prev. 0.2%).

- Swiss GDP Growth Rate YoY (Q1) Y/Y 0.5% (Prev. 0.7%).

CENTRAL BANKS

- Fed's Powell (voter) said Fed will lose credibility if the President removes officials over policy, while he remain on the board according to Barron's.

- Fed’s Waller (voter) said the spread of stablecoins globally could broaden the reach of US monetary policy.

- BoJ's Koeda said oil is a negative supply shock for Japan.

- EU ECB Consumer Inflation Expectations (Apr) 1yr ahead 4% (prev. 4%); 3yr ahead 2.9% (prev. 3%).

- ECB's Villeroy said Bank of France estimates for French Economic growth in 2026 will be revised down, in view of bad Q1 surprise. Growth estimates should remain positive in most scenarios.

- ECB Schnabel said supply shock is seen as large and highly persistent, adds that oil prices are expected to stay elevated for some time.

- BoE’s Mann said the long run of good luck central bankers experienced in containing inflation has run out with a more shock-prone era setting in.

- ECB’s Pereira said the central bank shouldn’t hesitate to act and thinks that it is better to act sooner rather than later, so that they don’t have much greater second-order effects later on.

- ECB’s Vujcic said Croatia’s inflation is likely to ease in May after accelerating to the fastest annual pace in the euro area of 5.8% in April.

- PBoC set USD/CNY mid-point at 6.8167 vs exp. 6.7645 (prev. 6.8176).

GEOPOLITICS

RUSSIA-UKRAINE

- Russia to ban jet fuel exports until the end of November, Ifx reported.

- Ukraine's Air Force said Russian guided bombs strike the Donetsk region and drones are heading from Kharkiv to the Poltava region.

- Ukraine Air Force said enemy drones were detected over northwestern Kharkiv region.

CRYPTO

- Bitcoin is on the backfoot today, and trades back below USD 73k; Ethereum also posts losses of c. 2% and trades back below the USD 2k mark.

APAC TRADE

- APAC stocks began the new month predominantly in the green with the Nikkei 225 and KOSPI extending on fresh record highs amid tech-related strength and following a lack of any major geopolitical developments over the weekend, with a US-Iran peace agreement remaining elusive, while participants also got to digest mixed Chinese PMI data.

- ASX 200 traded rangebound with demand constrained as the strength in tech and miners is offset by underperformance in defensives, telecoms and real estate.

- Nikkei 225 rose to a fresh record high and briefly surpassed the 67,000 level for the first time amid tech strength, which saw SoftBank overtake Toyota as the largest Japanese company by market cap.

- KOSPI outperformed with index heavyweight Samsung Electronics rallying around 10% amid the tech momentum, while an industry report noted that the Co. surpassed Micron to become the world’s leading supplier of automotive memory chips last year.

- Hang Seng and Shanghai Comp were varied, with the mainland indecisive following mixed Chinese PMI data in which official Manufacturing PMI missed forecasts, but Non-Manufacturing PMI showed a surprise return to expansion territory, while RatingDog Manufacturing PMI topped forecasts. In addition, trade frictions linger as China vowed to resolutely retaliate if the EU proceeds with new restrictive trade measures, while the State Council announced that new rules tightening the oversight of outbound investments in selected technologies will take effect on July 1st.

NOTABLE ASIA-PAC HEADLINES

- Japanese S&P Global Manufacturing PMI Final (May) 54.5 vs. Exp. 54.5 (Prev. 55.1).

- Australian S&P Global Manufacturing PMI Final (May) 50.7 vs. Exp. 50.2 (Prev. 51.3).

NOTABLE APAC DATA RECAP

- Indian HSBC Manufacturing PMI Final (May) 55.0 vs. Exp. 54.3.

- Chinese RatingDog Manufacturing PMI (May) 51.8 vs. Exp. 51.4 (Prev. 52.2).

- Chinese NBS General PMI (May) 50.5 (Prev. 50.1).

- Chinese NBS Non Manufacturing PMI (May) 50.1 (Prev. 49.4).

- Chinese NBS Manufacturing PMI (May) 50 (Prev. 50.3).

- Australian ANZ-Indeed Job Ads MoM (May) M/M 1.8% (Prev. -0.8%).

- Australian TD-MI Inflation Gauge MoM (May) M/M -0.3% (Prev. 0.6%).

- Korea (Republic of) S&P Global Manufacturing PMI (May) 54.8 (Prev. 53.6).

- Korea (Republic of) Exports YoY (May) Y/Y 53.2% vs. Exp. 48% (Prev. 48%).

- Korea (Republic of) Balance of Trade (May) 26.95B (Prev. 23.77B).

- Korea (Republic of) Imports YoY (May) Y/Y 20.8% vs. Exp. 16.7% (Prev. 16.7%).

- Japanese Capital Spending Ex. Software YoY (Q1) Y/Y -1.4% vs. Exp. 5.4% (Prev. 7.3%).

- Japanese Company Profits YoY (Q1) Y/Y 14.6% vs. Exp. 5.3% (Prev. 4.7%).

- Japanese Company Sales YoY (Q1) Y/Y 1.1% (Prev. 0.7%).

- Japanese Capital Spending YoY (Q1) Y/Y 0.0% vs. Exp. 4.0% (Prev. 6.5%)

Loading...