DXY rebounds, US equity futures helped by strong AAPL results; Europe set to be quiet amid Labour Day - Newsquawk EU Market Open

- US President Trump said Iran is dying to make a deal and stated that Iran cannot be nuclear-armed. He added that he doesn't know if the ceasefire with Iran needs to be broken, but "we may do".

- The US may allow Israel to target Iran's energy facilities if negotiations fail, according to Channel 12 cited by Al Arabiya.

- Apple (AAPL) Q2 2026 (USD): EPS 2.01 (exp. 1.95), Revenue 111.2bln (exp. 109.45bln). Raised its dividend by 4% to USD 0.27/shr. Apple provided Q3 revenue growth guidance that beat estimates (+14-17% vs exp. +9%). Shares +2.4% after-market.

- Japan's Top FX Diplomat Mimura will not comment on intervention speculation and reiterated being in close contact and shares understanding with the US.

- Looking ahead, highlights include Global Manufacturing Final PMIs (Apr), US ISM Manufacturing (Apr), Speakers include BoE's Pill, Earnings from Chevron, Colgate, Exxon, Moderna, Estee Lauder & NatWest.

- Holiday: Labour Day (Eurozone cash and derivatives closed).

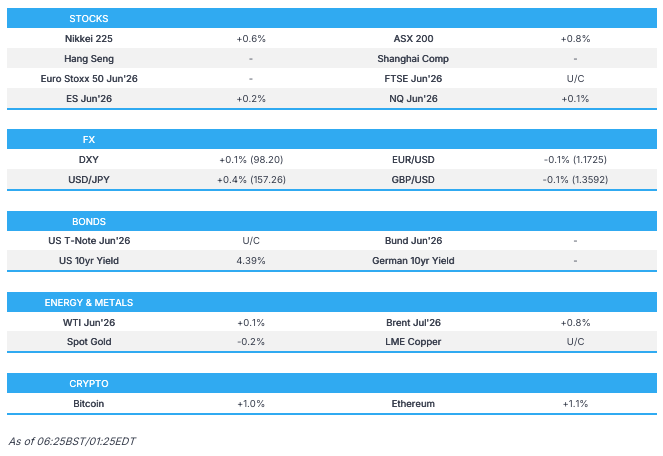

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US President Trump said Iran is dying to make a deal and stated that Iran cannot be nuclear-armed. He added that he doesn't know if the ceasefire with Iran needs to be broken, but "we may do". Furthermore, he commented that Iran's drone and missile factories are significantly down and that Iran is in very bad shape. On a deal, he said he doesn't know if we need a deal with Iran but later backtracked and said a deal might be needed. Later, he stated that he would not have approved enriched Uranium for Iran and needs guarantees that Iran will not have a nuclear weapon ever.

- US President Trump is expected to make a decision on the path forward [on Iran] in the coming days, according to NBC citing a US official.

- US CENTCOM Commander Cooper briefed President Trump for 45 minutes on new operational plans for potential strikes against Iran, Axios' Ravid reported citing sources.

- Two Pakistani officials in Islamabad, with direct knowledge of the talks between the US and Iran told MS NOW they expect a revised Iranian proposal to end the war by the end of the week.

- Iran President Pezeshkian and Ghalibaf, are dissatisfied with the way Foreign Minister Araghchi is advancing diplomacy, especially the nuclear negotiations, and are calling for his dismissal, according to Iran International citing sources.

- Iranian Foreign Ministry Spokesperson said that it is not responsible to expect a quick conclusion of the negotiations and that the other party has not used the opportunity provided by Iran's proposal. Iran must be ready for any eventuality.

- Israel prepares to announce the failure of negotiations with Iran, via Channel 12 cited by Al Arabiya, with Iran International stating that Israeli officials consider the collapse of negotiations between Washington and Tehran likely as early as next week.

- The US may allow Israel to target Iran's energy facilities if negotiations fail, according to Channel 12 cited by Al Arabiya.

- Air defence sounds were heard in some areas of Tehran, due to countering micro-birds and reconnaissance drones, according to Tasnim.

- UAE bans travel by citizens to Iran, Lebanon, and Iraq.

US TRADE

EQUITIES

- US stocks rallied as markets leaned risk-on despite ongoing geopolitical uncertainty around US/Iran developments. Sentiment was boosted by strong earnings. Alphabet and Amazon impressed with robust growth and strong cloud demand, while Qualcomm reversed earlier losses on upbeat commentary about China phone shipments. However, mega-cap tech saw some divergence, with Microsoft and Meta pressured by concerns over elevated AI-related capex. Elsewhere, cyclicals and defensives broadly gained, with Communication Services leading sectors while Technology lagged.

- Apple (AAPL) Q2 2026 (USD): EPS 2.01 (exp. 1.95), Revenue 111.2bln (exp. 109.45bln). Raised its dividend by 4% to USD 0.27/shr. Beat revenue metrics except for iPhone net sales. Authorised additional program to repurchase up to USD 100bln. In the earning call, CFO guided Q3 revenue growth between 14-17% Y/Y, gross margin between 47.5-48.5% and stated that AAPL will no longer targeting a net cash neutral position.

- SPX +1.02% at 2,709, NDX +0.98% at 27,452, DJI +1.62% at 49,652, RUT +2.21% at 2,800.

TARIFFS/TRADE

- US President Trump said the US will be removing the tariffs and restrictions on Whiskey having to do with Scotland's ability work with the Commonwealth of Kentucky on whisky and bourbon, and in honour of the King and Queen in the UK.

- USTR Greer said he suggested a US-China Board of Trade in his meeting with Chinese VP He Lifeng.

- USTR Greer said the US will extend preferential treatment to other UK goods.

NOTABLE HEADLINES

- Fitch said large US deficits to keep debt above "AA" peers and cuts 2026 US tariff revenue estimate by USD 150bln.

DATA RECAP

- Atlanta Fed GDPNow (Q2 initial): 3.7%.

APAC TRADE

EQUITIES

- Asia-Pac stocks traded with decent gains, helped by the positivity seen stateside. The majority of markets are closed today for Labour Day.

- ASX 200 rebounded after 8 straight days of losses. Miners led gains while Energy underperformed following Thursday’s drop in oil prices. ANZ reported cash profit that beat estimates; however shares have slipped lower after it raised its coverage ratio by 4bps due to the heightened geopolitical risk.

- Nikkei 225 posted decent gains, despite the sudden JPY strength amid intervention talk. Tokyo Electron benefited following its positive Q4 results, in which net profit beat estimates.

- US equity futures traded with modest gains. The start of futures trade started positively after Apple provided Q3 revenue growth guidance that beat estimates (+14-17% vs exp. +9%). AAPL +2.5% overnight.

- European equity futures are closed today for Labour Day.

FX

- DXY took to breather following Thursday's selloff. To recap, the index weakened by a near 1%, primarily driven by surging JPY and the risk-on sentiment across equities. Currently, DXY trades in a 98.13-98.18 range.

- EUR/USD traded around the unchanged mark and oscillated in a tight 1.1724-1.1736 range. The ECB kept rates unchanged at 2.0% and stuck to its data-dependent and meeting-by-meeting guidance. Following the meeting, ECB sources via Reuters noted that policymakers see a June hike as very likely with further reporting by Bloomberg stated that officials see a June hike if energy prices do not ease first.

- GBP/USD rotated in a 1.3599-1.3609 band, consolidating after the hawkish tilt by the BoE, as Pill voted for a 25bp hike. EUR/GBP has extended to a trough of 0.8618 thus far, just shy of the YTD lows of 0.8612.

- USD/JPY climbed back above the 157.00 handle, following Thursday’s 2.4% selloff. The selloff came amid jawboning and the confirmation of intervention by Japanese officials. Top FX Diplomat Mimura spoke again, however, refused to comment on intervention speculation. A Mizuho analyst highlighted that despite the recent JPY strength, the currency is likely to remain weak as long as tensions in the Middle East persist. On the data front, Tokyo CPI printed cooler-than-expected, with core CPI falling to 1.5% Y/Y (exp. 1.8%, prev. 1.7%). USD/JPY steadily moved higher to a peak of 157.31; final manufacturing PMI failed to spur a reaction.

- Antipodeans traded with mild losses. Aussie/Dollar was little moved after manufacturing PMI printed at 51.3 (prev. 51.0).

FIXED INCOME

- UST Futures traded in a 110-17+ to 110-22+ range, primarily driven by the downside in JGBs. ISM Manufacturing PMI is expected later, with the headline figure expected at 53.1 (prev. 52.7).

- JGB Futures started the Asia-Pac session on the backfoot, initially reversing the majority of Thursday’s pre-cash gains before rebounding as the session progressed. The selloff came following Japan's weekly investment flows, in which foreigners sold a net JPY 786.9bln in long-term bonds. This seemingly overlooked the cooler-than-expected Tokyo CPI, as 10yr JGBs fell to a low of 129.30 low.

- Bund Futures are closed due to Labour Day holiday.

- Japan sells JPY 250bln 10-year I/L JGBs: b/c 3.40x, Yield at the Lowest Accepted Price 0.578%.

- Australia sells AUD 1.0bln 4.50% 2033 bond: b/c 3.56x, average yield 4.8608%.

COMMODITIES

- Crude futures rotated in a c. USD 1.40/bbl range amid light newsflow. The latest update came from the Iranian Foreign Ministry Spokesperson, stating that it is not responsible to expect a quick conclusion of the negotiations and that the other party has not used the opportunity provided by Iran's proposal. Markets will be awaiting Trump’s decision on the path forward on Iran. Reports in recent sessions have pointed to a plan that includes a short and powerful strike, potentially targeting infrastructure.

- Precious Metals initially started the Asia-Pac session on the front foot but pared back slightly as trade progressed. Spot gold oscillated in a USD 4609-4636/oz range, silver in a USD 73.56-74.43/oz band.

- 3M LME Copper surged higher at the open and peaked at USD 13.12k/t as the red metal played catch up to the risk-on sentiment seen stateside. Gains pared back slightly throughout the Asia-Pac session and neared USD 13.06k/t.

- US President Trump's mineral reserve reportedly plans to purchase rare earths from China.

CRYPTO

- Bitcoin bounced back above the USD 77k handle.

NOTABLE ASIA-PAC HEADLINES

- Japan's Top FX Diplomat Mimura will not comment on intervention speculation and reiterated being in close contact and shares understanding with the US.

DATA RECAP

- Japanese Tokyo Core CPI YoY (Apr) Y/Y 1.5% vs. Exp. 1.8% (Prev. 1.7%).

- Japanese Tokyo CPI Ex Food and Energy YoY (Apr) Y/Y 1.9% vs. Exp. 2.3% (Prev. 2.3%).

- Japanese Tokyo CPI YoY (Apr) Y/Y 1.5% vs. Exp. 1.6% (Prev. 1.4%).

- Japanese S&P Global Manufacturing PMI Final (Apr) 55.1 vs. Exp. 54.9 (Prev. 51.6).

- Australian S&P Global Manufacturing PMI Final (Apr) 51.3 (Prev. 49.8).

- South Korean Balance of Trade (Apr) 23.77B vs Exp. 23.77B (Prev. 25.74B).

- South Korean Imports YoY (Apr) Y/Y 16.7% vs Exp. 13.1% (Prev. 13.2%).

- South Korean Exports YoY (Apr) Y/Y 48.0% vs Exp. 44.9% (Prev. 48.3%).

GEOPOLITICS

RUSSIA-UKRAINE

- Ukrainian forces have reportedly launched another attack on Russia's Tuapse oil refinery causing a fire, according to the Kyiv Independent.

- Local governor said port infrastructure in Ukraine's Odesa region was damaged and wounded two people.

OTHER

- China's Foreign Minister said the Taiwan issue is the biggest risk in US relations and urged US Secretary of State Rubio to maintain the stability of bilateral relations.

Loading...