DXY vaults 99.00, Crude boosted on Axios report that US was considering further Iran strikes - Newsquawk EU Market Open

- US CENTCOM is to brief US President Trump on new plans for potential military action in Iran on Thursday, Axios reported citing sources. The plan includes a short and powerful strike potentially targeting infrastructure to break the nuclear issue deadlock.

- The FOMC held rates at 3.50-3.75% as expected; voted 8-4 to hold rates (Miran voted for a 25bps rate reduction; Hammack, Kashkari, Logan dissented on easing bias in statement).

- Within the FOMC statement, a key shift in language was on inflation, with the line that inflation "remains somewhat elevated" being replaced with "elevated", amid the surge in energy prices.

- In the post-meeting statement, Chair Powell stated that the policy stance is appropriate and not on a pre-set course.

- AMZN (+2.7%), META (-7.0%), GOOGL (+7.1%), and MSFT (+0.3%) reported earnings after-hours, with all four beating on its EPS and revenue metrics. However, post-earnings performance was mixed.

- Looking ahead, highlights include French GDP (Q1), German Retail Sales (Mar), German Import Prices (Mar), French Inflation (Apr), Spanish GDP (Q1), German Jobs (Apr), EZ HICP, GDP (Q1), EZ Unemployment Rate (Mar), US PCE Price Index (Q1/Mar), US GDP Growth Rate (Q1), Jobless Claims (Apr/25), US Chicago PMI (Apr), ECB Policy Announcement (Apr), BoE Policy Announcement & MPR (Apr), CBRT Minutes (Apr). Speakers include BoE Governor Bailey and ECB President Lagarde. Earnings from Apple, SanDisk, Reddit, Amgen, Caterpillar, ConocoPhillips, Eli Lilly, Schneider Electric, Air France, DHL, Volkswagen, MTU Aero & Puma.

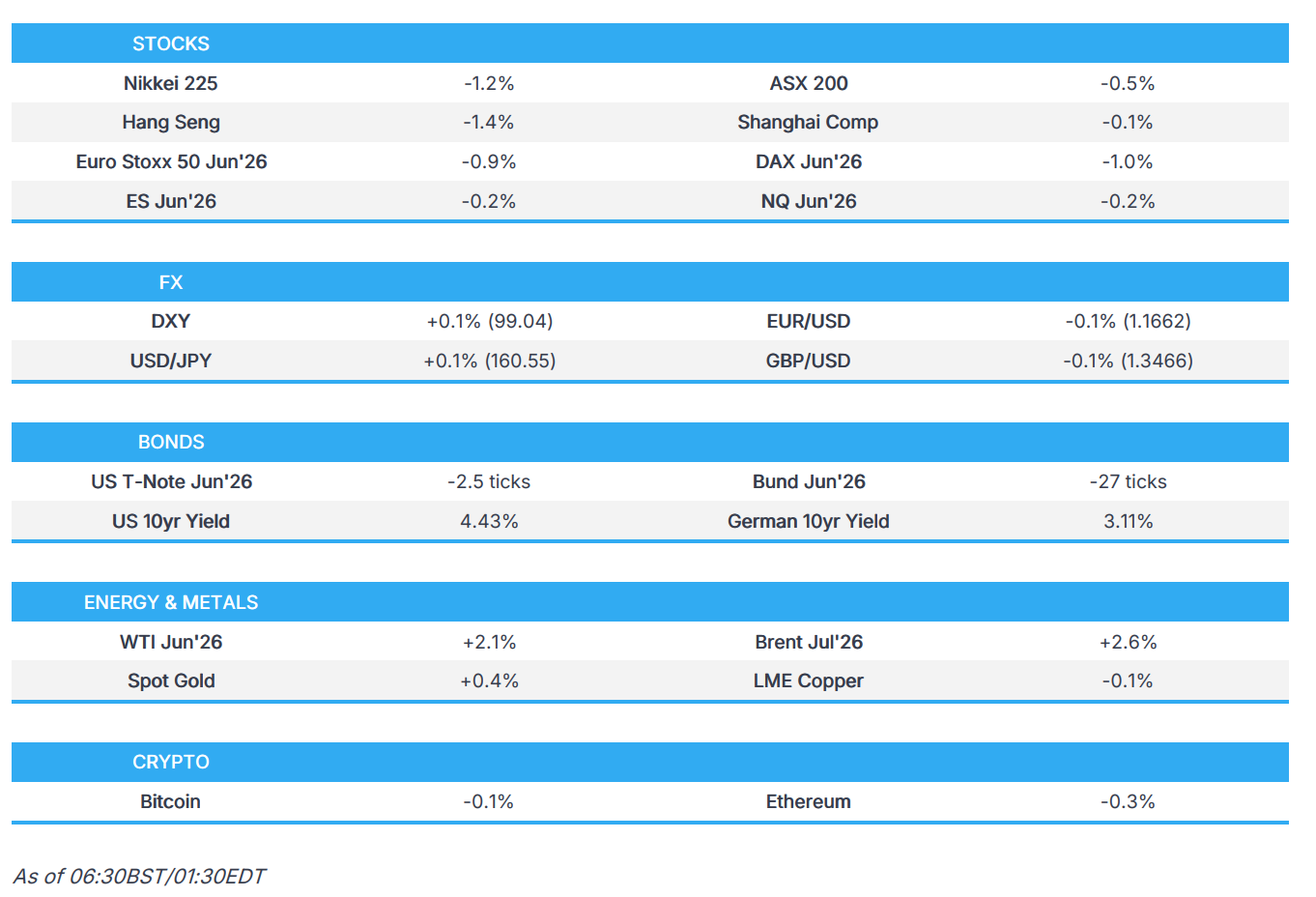

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US CENTCOM is to brief US President Trump on new plans for potential military action in Iran on Thursday, Axios reported citing sources. The plan includes a short and powerful strike potentially targeting infrastructure to break the nuclear issue deadlock. Other options expected to be presented include a plan to take over part of the Strait to allow for commercial shipping, which could involve ground forces, and a special forces op to secure Iran's uranium stockpile.

- US President Trump said the Hormuz blockade has been genius and foolproof. The blockade shows how good the US Navy is and says all Iran has to do is "cry uncle". He added that Iran has come a long way, question is whether they will go far enough and reiterated that there will never be a deal with Iran until they agree to no nuclear weapon.

- US President Trump told N12 News that without a nuclear deal he will not lift the blockade on Iran.

- US CENTCOM has asked to send the Army's hypersonic missile to the Middle East for possible use against Iran, Bloomberg reported citing sources.

- The US administration is asking countries to join a new international coalition that would enable ships to navigate through the Strait of Hormuz.

- US President Trump and Russian President Putin held a phone call, according to Kremlin media. The call lasted over 1.5 hours, in which Putin proposed ideas on Iran nuclear programme and warned against new military action in Iran while Trump believes a deal to settle Ukraine conflict is close.

- US Treasury Secretary Bessent said we are sprinting for the finish line with Iran and are willing to do secondary sanctions on Iran oil buyers.

- US will reportedly seek forfeiture of Iran-linked oil tankers seized at sea.

- Iranian Navy Commander said we have closed the Strait of Hormuz from the Arabian Sea side and will take swift action if enemy advances.

- Iran's military adviser to supreme leader said revenge for the martyred leader remains in place.

- Khamenei's military advisor said new rounds of diplomacy and negotiation must be initiated.

- A surveillance drone near the US embassy in Baghdad has been shot down, according to Iraqi security sources.

- US CENTCOM said the US navy has redirected 42 vessels from the blockade in the Strait of Hormuz and that the military is fully committed to enforcing the blockade.

- US President Trump told Israeli PM Netanyahu that Israel should only take surgical military action in Lebanon and avoid a full resumption of the war, according to Axios.

- Israel is asking the US to limit negotiations with Iran to a timeframe ending in mid-May, Channel 12 reported citing sources.

- The Iranian oil minister has urged the public to reduce energy consumption, while dismissing the impact of the US naval blockade, CNN reports; the government has instructed government offices to cut electricity use by up to 70%.

US TRADE

EQUITIES

- US stocks ended mixed, with the tech-heavy Nasdaq 100 the sole gainer, while the small-cap Russell 2000 lagged amid a deluge of earnings, US data, Middle East rhetoric and the latest FOMC meeting. Sectors were broadly lower, with energy the clear gainer, buoyed by notable gains in crude benchmarks as the US and Iran seemed no closer to any breakthrough, with punchy rhetoric from both sides on Wednesday.

- AMZN, META, GOOGL and MSFT reported earnings after-hours, with all four beating on its EPS and revenue metrics. However, performance was mixed with GOOGL the only Mag-7 printing gains. AMZN traded mixed after Q2 operating income guidance missed estimates however, beating revenue guidance. META plummeted after missing Q2 revenue guidance expectations while MSFT was choppy.

- SPX -0.04% at 7,136, NDX +0.58% at 27,187, DJI -0.57% at 48,862, RUT -0.60% at 2,739.

CENTRAL BANKS

- The FOMC held rates at 3.50-3.75% as expected; voted 8-4 to hold rates (Miran voted for a 25bps rate reduction; Hammack, Kashkari, Logan dissented on easing bias in statement). Within the statement, a key shift in language was on inflation, with the line that inflation "remains somewhat elevated" being replaced with "elevated", with the Fed explicitly attributing this to the recent surge in global energy prices, a hawkish tilt suggesting the Committee views the oil shock as more than purely transitory. Growth and labour market language was largely unchanged.

- In the post-meeting statement, Chair Powell stated that the policy stance is appropriate and not on a pre-set course. The economy is expanding at a solid pace however job gains have remained low and the outlook is highly uncertain. He described inflation as elevated and sees PCE at 3.5% Y/Y in March, with core PCE at 3.2% Y/Y. On the leadership transition, he announced that he will stay on as Governor after his term as Chair ends, until the DoJ probe is well and truly over.

- Within the Q&A, Powell stated that there was a vigorous debate on guidance, highlighting that a number of policymakers see a hike as likely as cut with the number of officials supporting a change to a neutral bias increased. He added that policymakers are not saying a hike is needed now. He reiterated that the Fed will need to wait and see, policy stance is in a good place and in the high-end of the neutral range estimates. On tariffs, he said the Fed has hypothesised that tariffs would be a one-off and that progress on energy and tariffs needs to be seen before lowering rates. On inflation, he said the prospects for a rise in core inflation are real and does not see the labour market as a source of inflation.

- BCB cuts 25bps to 14.50%, as expected.

- Morgan Stanley expects the Fed to leave rates unchanged in 2026 (prev. forecasted cuts in Sep and Dec), expects 25bps of rate cuts each in Jan'27 and Mar'27.

NOTABLE HEADLINES

- US President Trump posted that the US is studying and reviewing the possible reduction of troops in Germany with a determination to be made over a short period of time.

- US Senators Grassley and Banks are demanding answers from major tech and AI companies over concerns that employees with ties to China could access US AI systems, Axios reported.

- The White House opposes Anthropic's plan to expand access to Mythos due to national security concerns and worries about computing power, WSJ reported citing sources.

- US House has approved a Republican plan making way for a USD 70bln bill for ICE and Border Patrol.

NOTABLE EARNINGS

- Alphabet (GOOGL) Q1 2026 (USD): EPS 2.82 (exp. 2.63), Revenue 113.8bln (exp. 106.88bln). Shares +7.1% aftermarket.

- Amazon.com (AMZN) Q1 2026 (USD): EPS 2.78 (exp. 1.63), Revenue 181.5bln (exp. 177.22bln), guides Q2 revenue between 194-199bln (exp. 188.69bln) and operating income between 20-24bln (exp. 22.6bln). Shares +2.7% aftermarket.

- Meta Platforms (META) Q1 2026 (USD): Diluted EPS 10.44 (exp. 6.66), Revenue 56.3bln (exp. 55.54bln). Shares -7.0% aftermarket.

- Microsoft (MSFT) Q3 2026 (USD) EPS 4.27 (exp. 4.05), Revenue 82.9bln (exp. 81.37bln). Shares +0.3% aftermarket.

- QUALCOMM (QCOM) Q1 2026 (USD): EPS 2.65 (exp. 2.56), Revenue 10.6bln (exp. 10.58bln), Next Qtr. EPS 2.10-2.30 (exp. 2.42), Next Qtr. Rev. 9.2-10.0bln (exp. 10.19bln). Shares +13.5% aftermarket.

- Samsung Electronics (005930 KS) Q1 2026 (KRW): Net 47.1tln (exp. 38.3tln), Operating profit 57.2tln (exp. 57.2tln), Revenue 133.9tln (exp. 117.5tln), chip business aided by HBM4 and SOCAMM2 sales to NVIDIA (NVDA). Shares fell -1.1%.

APAC TRADE

EQUITIES

- Asia-Pac stocks traded with a negative bias, as weakness stateside in cash hours, earnings and recent geopolitical updates drive price action. More recently, Axios reported that US CENTCOM is to brief President Trump on new plans for potential military action, which is to include a short and powerful strike to break the nuclear issue deadlock.

- ASX 200 printed modest losses. IT and Tech topped the sector pile while consumer staples and mining underperformed.

- Nikkei 225 returned from holiday closure with losses in excess of 1%, returning to the 59,000 handle. Fujitsu weighed on the index after the Co.’s Q4 op. profit and FY forecast missed estimates. On the other hand, TDK was one of the outperformers, following FY net that rose by around 20%.

- KOSPI lacked direction, trading either side of the unchanged mark. Initial upside came after Samsung Electronics reported Q1 earnings that beat top- and bottom-line metrics. However, the earlier gains were erased as trade continued. LG Electronics held onto its earlier gains, after the Co. reported Q1 net that beat expectations.

- Hang Seng and Shanghai Comp. traded mixed, with the Hang Seng the clear underperformer. Stronger-than-expected manufacturing PMIs failed to support the indices, while China Construction Bank printed losses following its Q2 earnings.

- US equity futures surged higher at the start of futures trading, driven by guidance delivered by Microsoft and Amazon after-hours. However, as the session continued and sentiment soured, gains were completely pared back

- European equity futures are indicative of a weak open with the Euro Stoxx 50 future -1.0% after cash closed -0.4% on Wednesday.

FX

- DXY rebounded from the APAC open gap lower, as it held onto the Fed-driven bid higher. To recap, the FOMC left rates unchanged with an 8-4 vote split. Dissenters include Miran (voted for 25bp cut), Hammack, Kashkari and Logan (all 3 dissented on easing bias within the statement). The statement tilted hawkish, with the language describing inflation as “elevated” from “remains somewhat elevated”. In other news, a recent Axios scoop has lifted the USD, stating that US CENTCOM is to brief US President Trump on new plans for potential military action in Iran on Thursday. DXY currently trades at the upper end of a 98.81-99.09 range.

- EUR/USD picked up pace to the downside in recent trade, amid a firmer dollar after Axios reported on a briefing in which new plans for military action are to be presented to President Trump. Aside from geopols, the ECB is expected to keep rates unchanged at 2.0%.

- GBP/USD traded at the lower end of a 1.3455-1.3495 range, mainly driven by the greenback strength. The BoE is also expected to leave rates steady at its policy confab, with focus to lie on any clues or hints towards the timing of the next move, and the MPC’s current view on market pricing.

- USD/JPY held above the 160.00 handle, oscillating in a 160.07-160.58 band. The breach of the psychological 160 level has, in the past, prompted intervention. However, the lack of one-sided, rapid moves will make it difficult for the government to justify intervention. Moody’s Analytics noted that authorities often favour intervention in light liquidity. As it turns out, Japanese markets are closed between May 4th-6th for a public holiday.

- Antipodeans outperformed their G10 peers, as the Aussie and Kiwi rebounded from Wednesday’s losses.

FIXED INCOME

- UST futures consolidated in a tight 4 tick range, after the hawkish FOMC rate decision pushed benchmarks lower. The FOMC held rates steady at 3.50-3.75%, however it voted 8-4 (Miran voted for 25bp cut while Hammack, Kashkari and Logan dissented on the easing bias within the statement.) The statement also tilted hawkish, with the language around inflation changed to “elevated” from “remains somewhat elevated.” Market pricing indicates rates to stay on hold in 2026, with a 56% chance of a hike by Apr’27.

- Bund futures were muted ahead of the ECB policy announcement. It is widely expected for the GC to keep rates steady at 2.0%, with markets pricing in a 99% chance of a hold.

- JGB futures gapped lower and underperformed its peers, as it had to play catch-up due to the holiday closure. 10-year JGBs briefly rebounded off its 129.17 trough before returning to session lows.

- Japan sells JPY 2.8tln 2-year JGBs: Average yield 1.407%, b/c 5.24x, price tail 0bps.

COMMODITIES

- Crude futures extended on Wednesday's gains, mainly driven by the Axios report. Within the report, journalist Ravid stated that US CENTCOM is to brief US President Trump on new plans for potential military action in Iran on Thursday. The plan includes a short and powerful strike potentially targeting infrastructure to break the nuclear issue deadlock while other options include a plan to take over part of the Strait to allow for commercial shipping, which could involve ground forces, and a special forces op to secure Iran's uranium stockpile. WTI Jun'26 and Brent Jul'26 briefly topped USD 110/bbl and USD 114/bbl respectively.

- Precious Metals initially traded on the front foot but has since pared back the majority of its gains amid the firmer dollar. Spot gold peaked at USD 4583/oz before returning to the unchanged mark of USD 4544/oz.

- 3M LME Copper initially took impetus from the positive risk tone stateside, but has since reversed amid the souring risk tone. Chinese manufacturing PMIs beat estimates, which briefly helped support copper prices.

- OPEC+ is likely to agree an oil output hike at Sunday meeting without the UAE, according to Reuters sources. OPEC+ likely to hike quotas by 206k BPD minus the UAE share of 18k BPD.

- US National Emergency Dominance Council Director Agun is set to travel to Venezuela on Thursday for meetings with oil, gas and mining execs.

- The Japanese Government is considering reviving power and gas subsidies this summer, according to sources. Plan is to use reserve funds and no extra budget eyed for now.

- Fire at PDVSA's Cardon refinery's FCC unit is reportedly under control.

CRYPTO

- Bitcoin held above the USD 75k handle.

DATA RECAP

- Chinese RatingDog Manufacturing PMI (Apr) M/M 52.2 vs exp. 50.9 (prev. 50.8).

- Chinese NBS Manufacturing PMI (Apr) 50.3 vs. Exp. 50.2 (Prev. 50.4).

- Chinese NBS Non Manufacturing PMI (Apr) 49.4 vs. Exp. 49.9 (Prev. 50.1).

- Chinese NBS General PMI (Apr) 50.1 (Prev. 50.5).

- Japanese Consumer Confidence (Apr) 32.2 vs. Exp. 33.1 (Prev. 33.3).

- Japanese Industrial Production MoM Prel (Mar) M/M -0.5% vs. Exp. 1.1% (Prev. -2.0%).

- Japanese Industrial Production YoY Prel (Mar) Y/Y 2.3% (Prev. 0.4%).

- Japanese Retail Sales MoM (Mar) M/M 1.3% (Prev. -2.0%).

- Japanese Retail Sales YoY (Mar) Y/Y 1.7% vs. Exp. 0.8% (Prev. -0.2%).

- South Korean Industrial Production MoM (Mar) M/M 0.3% vs. Exp. 0.2% (Prev. 5.4%).

- South Korean Industrial Production YoY (Mar) Y/Y 3.6% vs. Exp. 3.8% (Prev. -2.2%).

EU/UK

NOTABLE HEADLINES

- The EU is preparing a package of short-term benefits for Ukraine, which would include greater market access and deeper participation in EU programmes, Politico reported citing diplomats.

- UK total vehicle production -8.2% Y/Y; hit by commercial vehicle output, parts shortages and weaker exports to Asia and the US.

- The BoE has raised concerns over plans to cut the capital requirements of specialist trading firms, the FT reports; BoE officials are worried they could increase financial stability risks by making firms less able to withstand a crisis.

Loading...