Equities gain, DXY flat ahead of FOMC decision; Iran rejects ceasefire as missiles hit Tel Aviv - Newsquawk US Market Open

- Israel attempted to assassinate Iran's Intelligence Minister Khatib overnight, Jerusalem Post reported, citing an Israeli official, but is still awaiting the results of the target.

- Iran's Foreign Minister said Iran will target US forces wherever they assemble, including near urban areas. Iran fired retaliatory missiles towards Tel Aviv for the killing of Larijani.

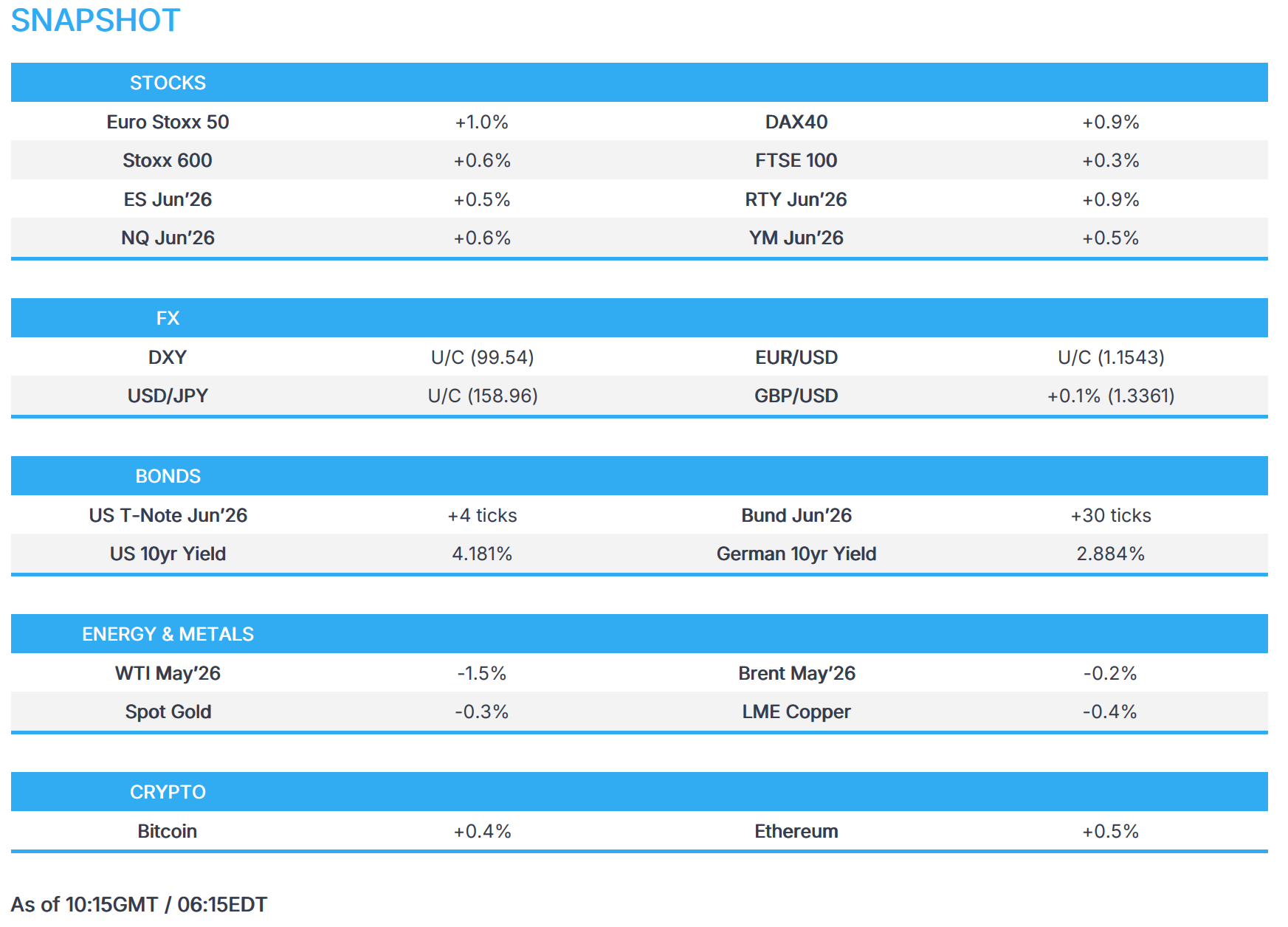

- European equities gain, Banks benefiting from a delay in capital requirements; US equity futures follow peers.

- Mostly flat FX trade heading into the FOMC; CHF narrowly lags ahead of tomorrow’s SNB.

- Crude continues to dictate macro sentiment; Gold rotates around USD 5,000/oz.

- Fixed income firmer amid energy downside ahead of key central bank announcements.

- Looking ahead, highlights include US PPI (Feb), New Zealand GDP (Q4), BoC, Fed & BCB Policy Announcements. Speakers include BoC's Macklem & Rogers, Fed Chair Powell & NVIDIA (NVDA) CEO Huang. Earnings from Micron.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European Bourses are broadly higher with the IBEX 35 leading on bank strength, while the CAC 40 also gains. The SMI underperforms as Logitech declines following a downgrade at UBS. Softer oil prices, after the resumption of exports through Ceyhan port, provide a modest tailwind to equities.

- Sectors show a positive bias. Banks outperform amid reports the EU may delay stricter capital requirements, lifting names such as Banco Santander, Société Générale, and Intesa Sanpaolo. Food, Beverages & Tobacco lag after HelloFresh guides adj. EBITDA below expectations. Elsewhere, Heidelberg Materials gains on a double upgrade at Morgan Stanley, Unilever slips on reports it is exploring a food division separation, and Diploma surges after raising organic revenue growth guidance.

- US equity futures are firmer (ES +0.5%, NQ +0.6%, RTY +0.9%), extending gains for a third session ahead of the Federal Reserve decision, where policymakers are expected to keep rates unchanged.

- Tencent (0700 HK) Q4 (CNY): Revenue 194.3bln (exp. 194.1bln), Operating Profit 60.34bln (exp. 60.45bln), Adj. Net Income 64.69bln (exp. 64.93bln).

- Multiple Chinese companies were said to have received approval from authorities to purchase NVIDIA (NVDA) H200 AI chips, according to Reuters.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is flat in a tight 99.46–99.71 range after two sessions of declines, tracking softer oil prices. Focus turns to the Federal Reserve decision, where rates are expected to be maintained, with markets not pricing cuts until Q4 2026 and Chair Powell likely to avoid firm guidance given geopolitical uncertainty.

- EUR and GBP trade muted against the dollar amid limited fresh catalysts. EUR/USD trades within 1.1518–1.1549, while GBP/USD sits in a 1.3341–1.3375 range as markets look ahead to the ECB and BoE tomorrow, both expected to signal a data-dependent stance.

- JPY is choppy ahead of the BoJ decision overnight, where no policy change is expected. USD/JPY briefly dips to 158.57 before stabilising near 159.00, with some late pressure as oil prices ease.

- Antipodeans are quiet with a slight upward bias. AUD/USD holds recent gains following the RBA decision, while broader macro drivers remain limited.

FIXED INCOME

- UST is firmer in contained trade, tracking the broader fixed income bid driven by softer energy and yield expectations. Futures trade in a 111-30+ to 112-07 range, with focus squarely on the Federal Reserve decision, where updated projections and Chair Jerome Powell’s tone will guide expectations on how the Fed assesses Middle East-driven inflation risks.

- Bund is stronger, with gains of up to 34 ticks and a high of 126.81 as energy-driven yield pressure eases. Upside levels are seen at 127.00, then 127.20–127.53, with a gap toward 128.00. Focus turns from final HICP (no reaction seen) and German supply to the FOMC as a signal for how the European Central Bank may position policy amid the energy shock.

- Gilt outperform, rising over 50 ticks to a 90.26 peak, continuing the recent trend of UK strength versus peers. Resistance sits at 90.85 (11 March high). Attention remains on the FOMC as a precursor to Thursday’s BoE decision, alongside domestic political noise after criticism of UK PM Starmer from former Deputy PM Rayner.

- Australia sold AUD 1bln 4.25% October 2036 bonds, b/c 4.14, avg. yield 4.9122%.

COMMODITIES

- Crude futures are softer, but off APAC lows as markets digest geopolitical updates without fresh escalation. Iran confirms the death of security chief Ali Larijani, while officials rule out a ceasefire, maintaining elevated uncertainty. Elsewhere, Iraq and Kurdish authorities agree to resume exports via Ceyhan, adding some supply relief, while private inventory data shows a crude build and gasoline draw. WTI trades within USD 91.45–95.65/bbl and Brent within USD 100.34–103.67/bbl.

- Spot gold trades rangebound around the USD 5,000/oz level, balancing oil-driven inflation risks against persistent geopolitical uncertainty. Trades within a USD 4,977.21–5,016.20/oz range, with silver also contained.

- Base metals are softer, extending the recent pullback as a firmer dollar and rising inventories weigh. Copper trades in a narrow USD 12,642–12,803/t range, with positioning also lighter on the bullish side.

- Senior NATO military official pushes for extension of alliance's pipeline system towards the east to supply NATO troops in a conflict with Russia. Adds that the NATO pipeline network should be extended to Poland, the Baltic states, Finland and Romania.

- South Korea envoy said to receive 18mln barrels of crude oil from UAE and that UAE pledges to give number 1 priority to South Korea for crude supply.

- Indian Government official says they are to give 10% more commercial LPG to states if they help if the long-term shift from LPG to piped gas, adds that LPG situation is still of concern.

- India's government is in talks with Iranian authorities for safe passage of six India-bound vessels carrying LPG and two crude oil carriers, according to two people aware of the matter cited by Mint.

- Libya's Sharara oilfield is gradually shutting down following a pipeline explosion.

TRADE/TARIFFS

- Japanese PM Takaichi said it will be tough regarding her visit to meet US President Trump on Thursday, while she will do her best to protect Japan's interests.

- Japanese PM Takaichi is to meet US President Trump on March 19th, Nikkei reported.

- Japan-US summit joint statement is said to agree up to JPY 11tln as second investment batch, according to NHK.

CENTRAL BANKS

- ECB reportedly urges lenders to keep a close watch on their USD funding after observing individual weaknesses on key metrics.

NOTABLE EUROPEAN DATA RECAP

- EU Inflation Rate YoY Final (Feb) Y/Y 1.9% vs. Exp. 1.9% (Prev. 1.7%, Low. 1.8%, High. 1.9%).

- EU Inflation Rate MoM Final (Feb) M/M 0.6% vs. Exp. 0.7% (Prev. -0.6%, Low. -0.6%, High. 0.7%).

- EU Core Inflation Rate YoY Final (Feb) Y/Y 2.4% vs. Exp. 2.4% (Prev. 2.2%).

- Swiss SECO Forecasts: Cuts 2026 GDP growth to 1.0% (prev. 1.1%), maintains 2027 GDP forecast at 1.7%; 2026 CPI raised to 0.4% (prev. 0.2%), 2027 CPI maintained at 0.5%.

- South African Inflation Rate YoY (Feb) Y/Y 3.0% (Prev. 3.5%).

GEOPOLITICS

MIDDLE EAST

- Several US officials described President Trump as the most bullish person in the White House on going to war with Iran, Axios reported. Three advisors to POTUS believe that Trump would want to end major operations before Israeli Prime Minister Netanyahu. However, the article noted that the leaders appear closer than ever.

- US President Trump reiterated that they are way ahead of schedule regarding Iran.

- Israel attempted to assassinate Iran's Intelligence Minister Khatib overnight, Jerusalem Post reported citing an Israeli official; still awaiting results of the target, however the initial assessment is that he has been eliminated.

- Iran's Foreign Minister said the new protocol [in the Strait of Hormuz] to ensure safe passage would be under "specific conditions" and based on Iranian and regional interests.

- Iran's Foreign Minister said Iran will target US forces wherever they assemble, including near urban areas, he understands neighbours' concerns and holds the US responsible for the conflict.

- Iranian Foreign Minister has ruled out a ceasefire.

- Iranian army spokesperson said armed forces will make use of more weapons that were not previously used in war, state TV reported.

- Iran targets Tel Aviv with missiles carrying cluster warheads in retaliation for the killing of security chief Larijani, while Iran's army vows decisive and regrettable revenge for Larijani killing.

- Australian PM Albanese said an Iranian projectile hit near an Australian airbase in the UAE, although no personnel were injured.

- Saudi Arabia is to host a meeting on Wednesday of Arab and Islamic foreign ministers in Riyadh on regional security according to the foreign ministry.

- USS Gerald R. Ford is to head to Crete for repairs after a large non-combat fire last week, while USS George H.W. Bush is to relieve USS Gerald R. Ford in the Middle East.

- Analysts warned that Iran is capable of sharply escalating its attacks on energy infrastructure in the Gulf, according to FT.

OTHERS

- US Secretary of State Rubio called New York Times report on Cuba fake news and denies the US is seeking to oust the Cuban president.

CRYPTO

- Bitcoin finds resistance at USD 75k while Ethereum holds below USD 2.4k.

APAC TRADE

- APAC stocks were mostly higher following the positive handover from Wall Street and as oil prices retreated, while markets now await a flurry of upcoming central bank policy decisions, including from the FOMC later today.

- ASX 200 gained with the help of strength in tech, utilities and real estate, but with gains limited amid weakness in health care and the consumer sectors following the recent central bank rate hike, while money markets are currently pricing a coin flip for a third consecutive hike in May.

- Nikkei 225 climbed back above the 55,000 level amid several positive factors, such as mostly better-than-expected trade data, which showed a surprise surplus and with exports topping forecasts. US and Japan are also set to agree on the joint development of rare earths, copper, and lithium at a summit on Thursday, while they will jointly develop AI shipbuilding robots. Furthermore, participants mull over the first wave of corporate responses to the Shunto wage demands, and the BoJ also kick-started its 2-day policy meeting.

- Hang Seng and Shanghai Comp were mixed with weakness seen in auto stocks and China's oil majors, while reports that multiple Chinese companies were said to have received approval from authorities to purchase NVIDIA H200 AI chips failed to inspire the mainland.

NOTABLE ASIA-PAC HEADLINES

- South Korea's financial regulator said will expand the KRW 100tln market stabilisation programme if needed. To prepare specific plans to ban dual listing of parent companies and subsidiaries.

NOTABLE APAC DATA RECAP

- Japanese Imports YoY (Feb) Y/Y 10.2% (Prev. -2.5%, Low. -1%, High. 18.5%).

- Japanese Exports YoY (Feb) Y/Y 4.2% (Prev. 16.8%, Low. -3.5%, High. 18.8%).

- Japanese Balance of Trade (Feb) 57.3B (Prev. -1152.7B, Low. -789B, High. 2299.7B).

- Australian Westpac Leading Index MoM (Feb) M/M -0.1% (Prev. -0.1%).

Loading...