Equities gain on hopes of potential end of Iran conflict; DXY slips further below 100 - Newsquawk US Market Open

- US President Trump to deliver a nationwide address on Wednesday to give an important update on Iran at 21:00EDT/02:00BST, according to the White House.

- US President Trump told NBC News on Iran war "it is coming to an end".

- Iranian Deputy Speaker of Parliament said the "Strait of Hormuz will never be opened, there has been no negotiation and there will be no negotiation", Fars reported.

- Global equities rebound on positive US-Iran commentary, Banks benefit the most while NKE hit after weak China guidance.

- Crude softer but off lows; metals mostly firmer.

- DXY slips on a "de-escalation" trade, ADP Employment ahead.

- Fixed income benefitting from lower energy prices as hawkish pricing pares back slightly.

- Looking ahead, highlights include US ADP Employment Change (Mar), Retail Sales (Feb), S&P Manufacturing PMI Final (Mar), ISM Manufacturing PMI (Mar), Atlanta Fed GDP, BoC Minutes (Mar), Speakers including ECB's Cipollone, Fed's Musalem, Barr and President Trump.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

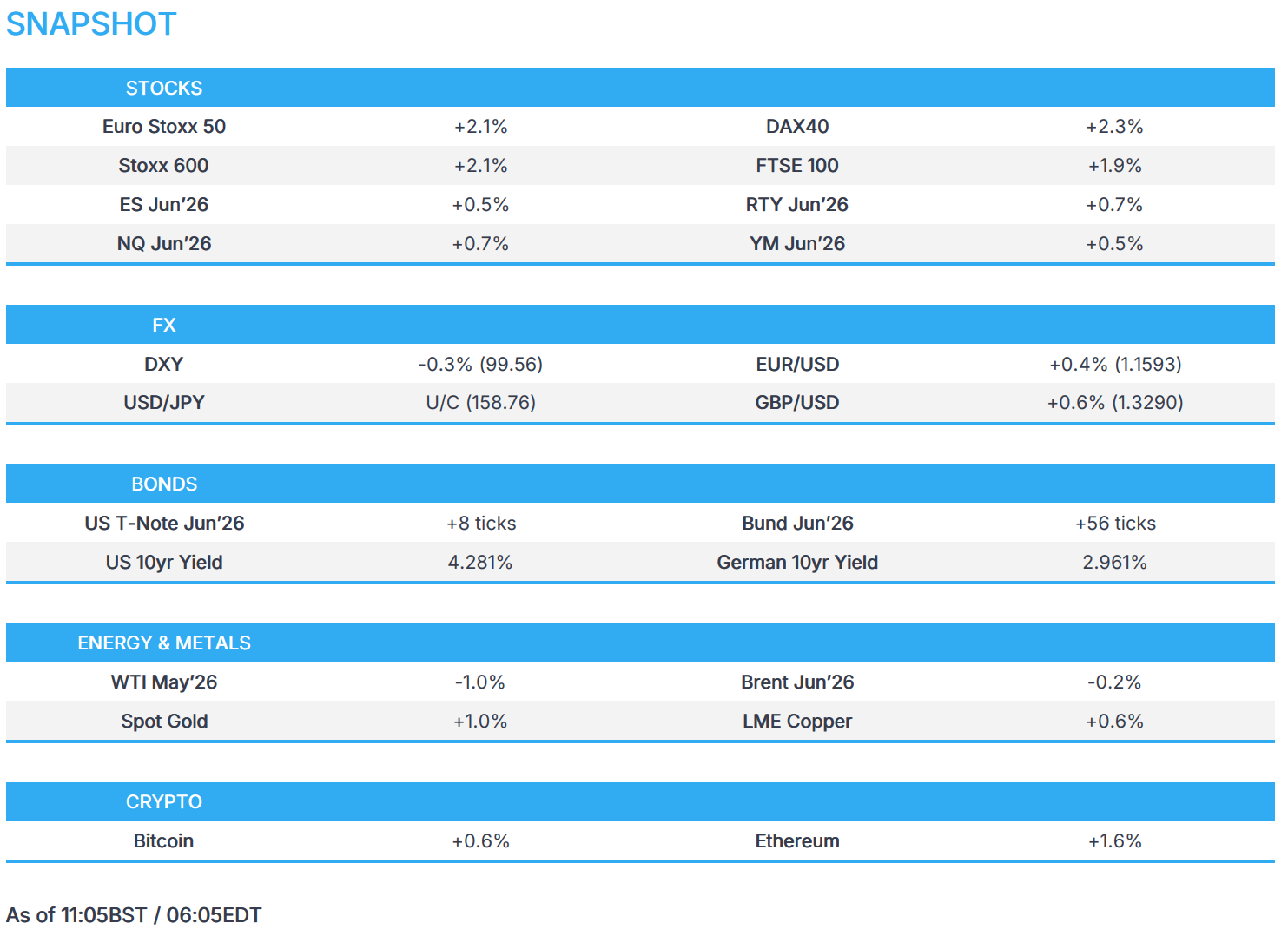

- European bourses (STOXX 600 +2.1%) continue to rebound, printing a third straight day of gains thus far. The positive was helped following reports that Iranian officials are leaning towards dialogue, while President Trump said that the war is coming to an end.

- European sectors are entirely in the green, ex. Energy. Banks and Travel and Leisure top the sector pile. Oil prices have been the main driver for airlines, with the drop in energy prices making jet fuel cheaper. Banks have been hit throughout the Iran war, so the prospects of it coming to an end have boosted the sector. To add, HSBC was added to Goldman Sachs' European conviction list.

- US equity futures are gaining pre-market, with ES regaining the 6,600 handle. In terms of stock specifics, Nike (-10.2%) shares have fallen pre-market after noting persistent weakness in China. However, the Co. did beat on its top- and bottom- line metrics.

- Nike (NKE) shares sank 10.2% after-hours following its Q3 results, where it reported a beat on its top- and bottom-line metrics, but noted of persistent weakness in China.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is on the backfoot this morning with markets pricing in a “de-escalation” trade, after US President Trump said to NBC News regarding the Iran war that "it is coming to an end", with a White House official suggesting Trump is confident an agreement will be reached soon. Interestingly, from the Iranian side, President Pezeshkian noted that Iran seeks to end the war with guarantees against further attacks. DXY currently holds at the lower end of a 99.41-99.88 range. It is worth highlighting that the index saw some strength after the Iranian Deputy Speaker of Parliament said that the "Strait of Hormuz will never be opened, there has been no negotiation and there will be no negotiation”.

- G10s are entirely stronger against the USD, albeit to varying degrees. The CHF outperforms, benefiting from lower energy prices – the likes of GBP and EUR also benefit. For the GBP specifically, the UK government confirmed new measures to ease the cost of living pressure are to come into force today, including an increase in the national living wage to GBP 12.71 and with energy bills to be cut by an average GBP 117 a year for millions across the UK, which will be locked in until end of June.

- JPY also gains vs USD, albeit to a lesser degree vs peers. The seemingly easing Iran tensions has benefited the JPY, which builds on the strength seen in recent sessions, facilitated by jawboning and a hawkish-leaning BoJ SOO earlier this week. As for today, Japan’s Tankan survey was mostly stronger-than-expected, which supports the case for an April BoJ rate hike. USD/JPY currently trades within a narrow 158.27-159.01 range.

FIXED INCOME

- An overall positive start in the fixed income benchmarks, with energy prices falling and higher hopes of a potential end to the Iran conflict. President Trump stated that the war is coming to an end, while a White House official said that the President is confident that an agreement will be reached soon.

- USTs are trading at the upper end of a 111-10 to 111-14+ range, albeit off best levels, as energy prices rebound slightly. Price action is set to remain rangebound ahead of a flurry of data and Fed speak, while Trump is set to speak at 21:00EDT/02:00BST.

- Bunds, in tandem with its peers, are gaining and currently holding above the 126 handle. The 10yr yield extends further below 3.0%, printing a trough at 2.933% before bouncing slightly. EZ final manufacturing PMI ticked slightly higher above the prelim. Figure but failed to drive any move in EGBs. In addition, ECB speakers reiterated the impact higher energy prices have on the European economy.

- Gilts outperform, continuing to be the beneficiary of lower energy prices, as BoE pricing remains sensitive to oil prices. Pricing for rate hikes have pulled back, now price in 44bps of hikes in 2026.

- Germany sells EUR 3.025bln vs exp. EUR 4.0bln 2.50% 2032 Bund: b/c 1.11x (prev. 1.51x), average yield 2.78% (prev. 2.60%), retention 24.3% (prev. 20.1%).

COMMODITIES

- In geopolitics, optimism was seen on Tuesday over a potential end to the war, particularly following Trump’s overnight comments that the US could leave Iran in two to three weeks. This follows reports that the US could exit Iran without reopening the Strait of Hormuz, with Trump calling on users of the strait to secure it themselves. Trump is due to make an announcement tonight at 21:00 EDT/02:00 BST. Some of yesterday’s optimism waned after commentary from the Iranian Deputy Speaker of Parliament, who said: “Strait of Hormuz will never be opened, there has been no negotiation, and there will be no negotiation.”

- WTI and Brent initially dipped to lows of USD 96.50/bbl and USD 98.35/bbl respectively as markets initially continued the move from yesterday, although a floor was later found on the Iranian deputy speaker comments, with Brent back above USD 100/bbl and WTI near USD 99/bbl at the time of writing, both still lower intraday by over USD 2/bbl apiece. Dutch TTF prices are softer once again after slipping over 7% in the prior session, with desks citing favourable weather alongside hopes of an Iranian war de-escalation.

- Spot gold is slightly firmer amid the softer USD and lower oil prices, with the yellow metal back above its 100 DMA (4,642.48/oz) in a current USD 4,661.61-4,747.77/oz parameter. Conversely, spot silver is softer on the day following yesterday’s +7% gains, with the metal today finding resistance near its 100 DMA (USD 75.22/oz).

- Base metals mostly eke out mild gains in what is seemingly a function of the USD alongside recent positive sentiment amid hopes of a de-escalation of the Iranian situation. 3M LME copper resides in a current USD 12,380.00- 12,499.75/t range after finding resistance around USD 12,500/t.

- IEA Chief Birol says more than 12mln BPD of oil supply has been lost so far due to the Middle East crisis; the current crisis is worse than the 1970s oil shocks and the loss of Russian gas in 2022 combined. Oil supply losses in April are expected to be twice as high as in March. Biggest problem is a lack of jet fuel and diesel, already affecting Asia and coming to Europe in April–May.

- UK PM Starmer said the fuel duty will remain where it is until September.

- South Korea has raised its energy disruption alert to the second-highest level due to the possible crude oil supply crisis, via Yonhap.

- US extended a Russian oil transit license via Kazakhstan to China until March 2027, according to IFX cites Kazakh Energy Ministry.

- US Private Inventory Data (bbls): Crude +10.3mln (exp. -1.3mln), Distillate -10.4mln (exp. -1.3mln), Gasoline -3.2mln (exp. -2.2mln), Cushing +0.8mln.

TRADE/TARIFFS

- India grants one-time customs duty relief for goods made in special economic zone and sold into domestic market.

- US is rushing to put in place a system to pay back USD 166bln it collected now after Trump tariffs were ruled to be unconstitutional, according to Nikkei.

NOTABLE EUROPEAN HEADLINES

- Germany's VDMA said German Engineering Orders -8% in Dec-Feb Y/Y (Domestic Orders -6%, Foreign Orders -8%).

- German Economic Institutes confirm cutting 2026 and 2027 GDP growth forecasts.

- UK government said new measures to ease cost of living pressure to come into force on April 1st. Increasing national living wage to £12.71. Energy bills are to be cut by average £117 a year for millions across the UK and locked in until end of June.

NOTABLE EUROPEAN DATA RECAP

- UK S&P Global Manufacturing PMI Final (Mar) 51.0 vs. Exp. 51.4 (Prev. 51.7, Low. 49.9, High. 51.9).

- EU S&P Global Manufacturing PMI Final (Mar) 51.6 vs. Exp. 51.4 (Prev. 50.8, Low. 51.4, High. 51.4).

- German S&P Global Manufacturing PMI Final (Mar) 52.2 vs. Exp. 51.7 (Prev. 50.9, Low. 50.9, High. 51.7).

- French S&P Global Manufacturing PMI Final (Mar) 50.0 vs. Exp. 50.2 (Prev. 50.1, Low. 50.2, High. 50.2).

- Italian S&P Manufacturing PMI (Mar) 51.3 vs. Exp. 50.8 (Prev. 50.6).

- Spanish S&P Manufacturing PMI (Mar) 48.7 vs. Exp. 50.5 (Prev. 50.0).

- Swedish Swedbank Manufacturing PMI (Mar) 56.3 (Prev. 56.1).

- Swiss procure.ch Manufacturing PMI (Mar) 53.3 vs. Exp. 47.1 (Prev. 47.4, Low. 46, High. 48).

- Swiss Retail Sales YoY (Feb) Y/Y 0.9% vs. Exp. 0.9% (Prev. -1.1%).

- Swiss Retail Sales MoM (Feb) M/M 0.4% vs. Exp. 0.1% (Prev. 1.1%).

CENTRAL BANKS

- BoJ new Board Member Asada does not comment on any specific stance. Rising oil prices put upward pressure on inflation while weighing on growth, creating a stagflationary trend.

- ECB's Stournaras said if oil prices rise over USD 150/bbl Europe could face a recession.

- ECB's Dolenc said ECB's adverse scenario is more likely to be the next baseline and current baseline is more like the best-case scenario.

NOTABLE US HEADLINES

- US President Trump signs executive order related to mail-in voting, said working on proof of citizenship and that voter ID and citizenship proof are subjects for another time.

- White House said US President Trump will sign a mail-in voting executive order (expected at 22:00BST/17:00EDT).

- US President Trump asks CPA for lists of insurers who were good to clients, and list who were bad in response to California fires.

GEOPOLITICS

MIDDLE EAST

- US President Trump said he is strongly considering pulling the US out of NATO after it failed to join his war on Iran, The Telegraph reported.

- US President Trump tells NBC News on Iran war "it is coming to an end".

- US advisers who speak regularly with the US President are reportedly uncertain about the mixed signals from Trump, according to Axios. "Some Trump aides and allies say he's mostly improvising rather than following any clear plan". "Aides have been convinced at various points that Trump was leaning toward a major escalation, and at others that he was eager for a swift resolution. "Nobody knows in the end what he's really thinking," a senior adviser said.".

- US Secretary of State Rubio said have largely destroyed Iran's air force and can see the finish line with Iran objectives, adds end to Iran war is not today, not tomorrow but it is coming. said:. There’s nothing any country is doing to help Iran that is in any way impeding our mission. There is potential for a direct meeting with Iran at some point. US is to re-examine NATO ties post-Iran war.

- Iranian Foreign Minister, when asked about the status of negotiations with the US, said "No decision has been made yet. We have many considerations. Our conditions for ending the war are very clear. We do not accept the ceasefire; We seek a complete end".

- Iranian Foreign Minister Araghchi reiterates Strait of Hormuz is closed to countries at war with Iran and said the US President must change his approach, also noted that a guarantee from 1-2 countries or from the UN Security Council is not enough. Iran has no plans for negotiations with the US. We are ready for any ground threat and are ready for at least six months of war.

- Iran's Foreign Minister Araghchi said Iran has zero trust in the US and dismisses the effectiveness of any potential ground operation targeting Iran.

- Iranian Deputy Speaker of Parliament said "Strait of Hormuz will never be opened, there has been no negotiation and there will be no negotiation", Fars reported.

- Iran began a new round of missile attacks against Israeli positions, according to SNN.

- Yemeni Houthi spokesperson claims a joint attack with Hezbollah against Israel, said the escalations will only drive Yemen "to further escalation in the coming period until the aggression stops and the blockade is lifted".

- Daily Mail columnist Andrew Neil posted "I am told by White House sources that Trump is seriously considering taking Kharg Island".

- Iran began a new round of missile attacks against Israeli positions, according to SNN.

- Iranian drone reportedly strikes US Victoria base in Baghdad, according to Fars news agency.

- Israeli military identified launch of missile from Yemen towards Israel.

- US and Israel attacked weather facilities of Bushehr again, via ISNA.

- Reports of a drone attack on an oil field in the "Chamanke" region, located in the north of Dohuk province in Iraqi Kurdistan; attack caused a fire in this oil field. The field is managed by an American company, Fars News reported.

- Reports of explosions in Saudi Arabia; reporting in proximity to Saudi announcing the interception of two drones in the last few hours.

- Qatari Defence said a cruise missile struck an oil tanker chartered for QatarEnergy in the economic waters, Al Arabiya reported.

- United Arab Emirates is preparing to help the US and other allies open the Strait of Hormuz by force, according to WSJ.

- Powerful explosion rocks American base in Erbil, according to Press TV.

- Iran's Mobarakeh steel plant hit in US-Israel strike and Khuzestan steel plant also targeted, Mehr News reported.

- UK PM Starmer reaffirmed that the war in the Middle East is not our war and will not be dragged into the conflict. Exploring every diplomatic avenue to reopen Hormuz.

RUSSIA-UKRAINE

- Russia's Deputy Foreign Minister Galuzin told TASS that talks on Ukraine are on pause.

CRYPTO

- Bitcoin tops above USD 69k, Ethereum extends above USD 2.1k.

APAC TRADE

- APAC stocks mostly rallied with global risk sentiment buoyed by hopes for an end to the Iran conflict following encouraging comments from the US and Iran, while President Trump also suggested that the war could end in 2 or 3 weeks, and he will deliver a nationwide address on Wednesday evening to give an important update regarding Iran.

- ASX 200 gained at the open and was led by outperformance in mining, materials, resources and tech, with nearly all sectors in the green aside from some defensives, while the index also shrugged off weak PMIs.

- Nikkei 225 surged back above the 53,000 level amid hopes of a nearing end to the conflict and after the latest BoJ Tankan survey mostly topped forecasts, with the headline large manufacturing index at its highest in more than five years.

- Hang Seng and Shanghai Comp conformed to the broad upbeat mood across the region with notable strength seen in mining, tech and biopharmaceuticals, while a miss on Chinese RatingDog Manufacturing PMI and the smallest PBoC injection in more than a decade failed to derail the momentum.

NOTABLE APAC DATA RECAP

- Chinese RatingDog Manufacturing PMI (Mar) 50.8 vs. Exp. 51.6 (Prev. 52.1, Low. 50.5, High. 53).

- Japanese Tankan Large Manufacturers Index (Q1) 17 vs. Exp. 16 (Prev. 15, Low. 8, High. 18).

- Japanese Tankan Large Non-Manufacturing Index (Q1) 36 vs. Exp. 33 (Prev. 34, Low. 28, High. 36)

- Japanese Tankan Small Manufacturers Index (Q1) 7 vs. Exp. 7 (Prev. 6, Low. -1, High. 9)

- Japanese Tankan Large Manufacturing Outlook (Q1) 14 vs. Exp. 13 (Prev. 15, Low. 5, High. 15)

- Japanese Tankan Large Non-Manufacturing Outlook (Q1) 29 vs. Exp. 28 (Prev. 28, Low. 24, High. 34)

- Japanese Tankan Large All Industry Capex (Q1) 3.3% vs. Exp. 13% (Prev. 12.6%)

- South Korean S&P Global Manufacturing PMI (Mar) 52.6 (Prev. 51.1).

- South Korean Balance of Trade (Mar) 25.74B (Prev. 15.5B).

- South Korean Imports YoY (Mar) Y/Y 13.2% (Prev. 7.5%).

- South Korean Exports YoY (Mar) Y/Y 48.3% (Prev. 29%).

Loading...