Equities see modest gains with Crude under $100/bbl on second round negotiation hopes - Newsquawk US Market Open

- Next round of talks between US and Iran could take place this week or early next week, according to the Iranian embassy official in Pakistan.

- US VP Vance said we made some progress in Iran talks, and he wouldn't say things went wrong, while he added Iranians moved in our direction in talks, but not far enough.

- A US official said there is “continued engagement” with Iran and forward motion on trying to get to an agreement, while a senior US official also said talks between the US and Iran are continuing even now and there is progress in trying to reach an agreement, according to Axios.

- Energy eases amid continued reports of further US-Iran talks.

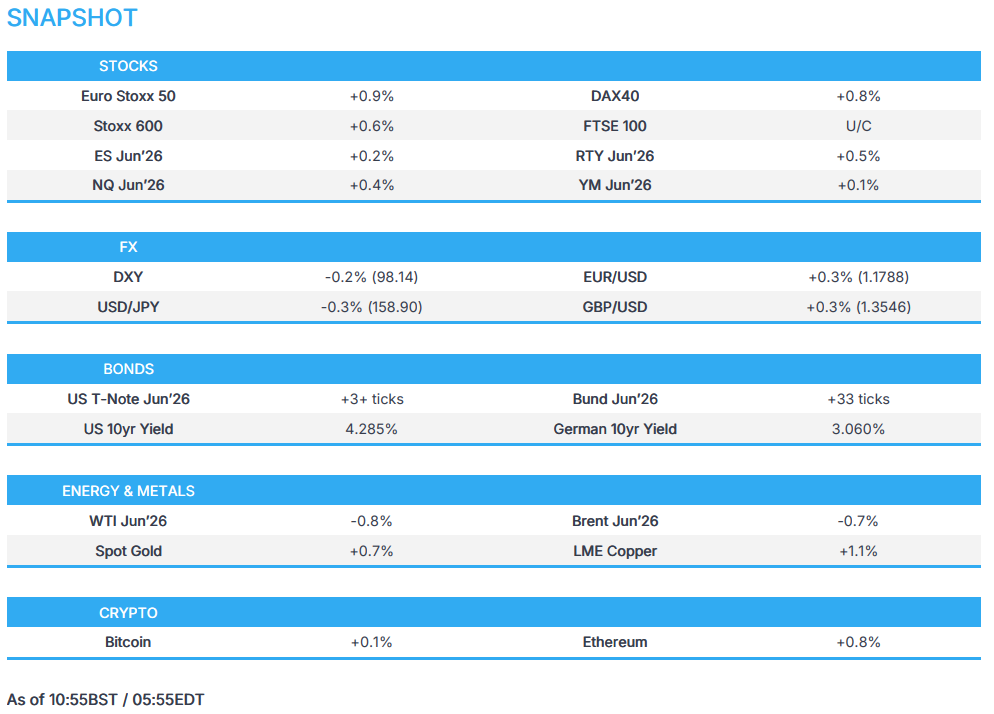

- Global equities gain on positive risk tone; US banks ahead.

- DXY soften, Kiwi continues to outperform while JPY helped modestly by reports BoJ is to increase price forecast.

- Fixed benchmarks gain, heavy speaker slate ahead.

- Looking ahead, highlights include US NFIB Business Optimism Index (Mar), ADP Weekly Change, PPI (Mar), South Korean Export/Import Prices (Mar), IMF World Economic Outlook Press Briefing (Apr). Speakers include BoE's Bailey & Greene, ECB's Lane, Cipollone & Lagarde, RBNZ's Breman, Fed's Goolsbee, Barr, Paulson, Collins & Barkin, Earnings from JPMorgan Chase, BlackRock, Citi, J&J, Wells Fargo & Kering.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- Next round of talks between US and Iran could take place this week or early next week, according to the Iranian embassy official in Pakistan. Further commentary by the Pakistan Foreign Ministry stating it offered to host a second round of US-Iran negotiations, no date or time has been set yet.

- Pakistani Journalist Mallick said "While Islamabad has offered to host the next round of in person talks between US and Iran, which could be held at a working level, to my understanding, date and venue for the next round has not been finalised as yet".

- US and Iran discussing another round of face-to-face talks to secure longer-term ceasefire after Islamabad negotiations ended without a deal, while officials aim to meet again before two-week ceasefire expires next week, according to Clash report. AP also reported that US and Iran could be headed toward a second round of talks, while talks could happen on Thursday.

- US VP Vance said we made some progress in Iran talks and he wouldn't say things went wrong, adds Iranians moved in our direction in talks but not far enough. Ball is in Iran's court. We made it clear what US red lines are in Iran talks.

- US and Iran reportedly leave door open to dialogue after tense Islamabad talks, while a source stated that the parties came "very close" to an agreement and were "80% there", before running into decisions that could not be settled on the spot.

- Iranian President Pezeshkian said to French President Macron in a phone call on Monday that Iran will negotiate only under international law, while he claimed that unreasonable US demands prevented an agreement in weekend talks between US and Iran. He further told Macron that a lack of US good will and maximalist positions prevented finalising an agreement in Islamabad, IRNA reports; further states that diplomacy is the preferred path to resolving disputes.

- Iranian Spokesman for the National Security Committee said the end of the truce should not lead to its extension, Al Mayadeen reported.

- US aircraft carrier USS George H.W. Bush is sailing off the coast of Africa and is heading to the Middle East to join Operation Epic Fury, according to two US officials cited by WSJ.

- Saudi Arabia is pressing the US to drop its Hormuz blockade, with Gulf energy exporters worrying that Iran could escalate and close the Bab al-Mandeb, according to WSJ.

- Alarms have sounded in the Galilee Panhandle due to concerns over potential UAV penetration.

- Lebanese source said "The official mandate of Lebanon's ambassador in Washington is limited to pursuing a ceasefire with Israel", via Al Jazeera.

- Switzerland is reportedly ready to help diplomatic initiatives between the US and Iran.

- Russian Foreign Minister Lavrov tells Iranian counterpart Araghchi that it is important to ensure that no new fighting breaks out, and Moscow is on high alert to help in the settlement, while the latter warned warns of dangerous consequences of US actions.

- US Secretary of State Rubio is to host Israeli and Lebanese ambassadors for talks on Tuesday, while the talks aim for ceasefire, Hezbollah disarmament and peace deal, according to Axios.

- Meeting between the Israeli ambassador and the Lebanese ambassador Lebanon will be held on Tuesday at 18:00EDT/23:00BST, according to Al Jazeera citing Israeli Channel 15 citing sources.

- Chinese President Xi makes four proposals on maintaining peace in the Middle East, according to Chinese press.

- UK Deputy PM Lammy meets with US VP Vance in Washington and urges Iran ceasefire to hold, while he stresses free shipping through the Strait of Hormuz.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.6%) are rebounding from Monday’s losses as reports of a second round of US-Iran talks taking place as soon as Thursday brighten the risk tone. Outperformance is seen in the DAX, with gains of over 1%, while the FTSE 100 lags behind its peers. Imperial Brands (-8%) trades more softly after it delivered a trading update in which it kept its FY guidance unchanged as pricing in its tobacco business offset continued volume declines.

- European sectors are mainly in the green, with Utilities and Food, Beverage & Tobacco the only sectors with modest losses. Autos tops the sector pile, closely followed by Technology and Basic Resources.

- US equity futures continue to bid higher, with ES futures extending further beyond the 6,900 handle. Looking ahead, many of the US banks are set to report, including JPMorgan, Citi and Wells Fargo. As a reminder, Goldman Sachs reported its Q1 earnings, which were broadly positive, but shares slipped after FICC sales & trading revenue missed expectations.

- United Airlines (+1.9% pre-market), American Airlines (+4.8% pre-market) - United Airlines CEO pitched a possible merger with American Airlines to senior government officials, though it is unclear whether formal overture have been made, or a deal process is underway, according to Bloomberg. Any combination would face intense regulatory scrutiny even under the Trump administration, the report adds. (Bloomberg)

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX began the morning with a slight positive bias which was exacerbated by reports that US and Iran will return to negotiations later in the week. This report sparked a risk-on move, with crude falling USD 1.7/bbl, DXY marking fresh session lows, and high-beta currencies benefiting. It is worth noting that the outlet that ran this headline has since tweaked the headline to "could" resume talks, when it previously said "to" resume talks. With regards to date and time, that is not yet confirmed, though Pakistani Journalist Mallick writes "While Islamabad has offered to host the next round of in person talks between US and Iran, which could be held at a working level, to my understanding, date and venue for the next round has not been finalised as yet".

- The greenback looks to a busy day with US PPI and a packed calendar for Fed speak. Fed's Goolsbee (2027 voter, Dovish; no text expected) will speak to Yahoo Finance, He is also set to take part in a panel discussion and give remarks to media separately today. Barkin (2027 Voter, Neutral; no text), Barr (Voter, Neutral; text expected), Paulson (2026 Voter, Dovish; no text) and Collins (2028 Voter, Neutral; no text expected) are to speak on rural economic development.

- DXY continues to trade below all significant DMAs after falling below 100- and 200-DMAs in Monday's session. In terms of levels below, 97.87 marks the beginning of the war open, while today's session low was marked at 98.11.

- NZD stays the best performer in the G10FX space as markets price in further bps of hikes from the RBNZ. Overnight, ANZ revised its rate outlook for the RBNZ, now forecasting hikes in July, September and October. This follows moves from other domestic banks, ASB expecting the OCR to rise in September and December to a terminal of 3.25% next year (Terminal consensus), mid next year. ANZ Chief Economist Zollner said it is fair to interpret the recent media appearances from Governor Breman as deliberate. As a reminder, Breman conveyed hawkish marks a few times last week. Elsewhere in the ANZ note, Zollner said we don't have a strong view on July versus September. But we do have a pretty strong view that hikes will come before our previous call of December.

- JPY continues to be bound within 158-160 parameters. On Monday, remarks from BoJ Governor Ueda saw markets trim expectations of a hike in April's meeting, with the Japanese curve implying 4bp of hikes (prev. c. 15bp). As such, the haven remains in lockstep with a slightly weaker USD (DXY -0.2%). There was a Bloomberg source that just hit the wires, which suggested BoJ was considering a sharp increase to its price forecast this month, while weighing a possible growth outlook cut due to high oil prices. This report pushed USD/JPY lower by around 10 pips to mark a session low of 158.85.

FIXED INCOME

- Global fixed benchmarks were firmer overnight and continued to move a little higher as the European session progressed. Initial optimism was facilitated by reports that the US is reportedly eyeing a potential second round of in-person talks with Iran as the blockade takes hold, according to CNN. AP reported that the US and Iran could be headed toward a second round of talks, which could happen on Thursday. The complex then took another leg higher after Reuters reported that US and Iranian negotiation teams are to return to Islamabad for peace talks later this week. Markets will now await any official confirmation on if/when talks begin.

- USTs are higher by 4 ticks, and currently trade within a 111-07+ to 111-14+ range. Today’s action is encapsulated by the above, but later on, the domestic docket is packed with Fed speak and US data. In brief, weekly ADP employment stats (prev. +26k average per week over the four-week window), US PPI (expected to rise 1.2% M/M vs prev. 0.7%) and NFIB Business Optimism Index are all expected. On Fed speak, Fed’s Goolsbee (2027 Voter, Dovish; no text expected), Barr (Voter, Neutral; text expected), Paulson (2026 Voter, Dovish; no text expected), Collins (2028 Voter, Neutral) and Barkin (2027 Voter, Neutral) are all to provide comments later.

- Bunds and Gilts also follow the above, extending gains of around 40 ticks and 45 ticks, respectively. For the UK, BRC Retail Sales rose 3.1% (exp. 0.9% prev. 0.7%). The firm pointed towards warmer weather/Easter holidays boosting momentum, but highlighted risks surrounding the Middle East war, which is “is weighing heavily on both retailer and consumer confidence”. On the monetary policy front, BoE’s Mann highlighted that wage expectations could rise amidst the energy price shock.

- For Germany specifically, a large jump in Wholesale Prices in March weighed on Bunds at a time, though ultimately proved fleeting. Much of the jump in prices was associated with rises in “energy products and raw materials”, amid the Iranian conflict.

- Germany sells EUR 3.953bln vs exp. EUR 5.0bln 2.50% 2031 Bobl: b/c 1.04x (prev. 1.1x), average yield 2.74% (prev. 2.72%), retention 20.9% (prev. 29.04%).

- The Netherlands sells EUR 2.81bln vs exp. EUR 2-3.0bln 2.50% 2031 DSL: avg. yield 2.795% (prev. 2.526%).

- Japan sold JPY 525bln 20-year JGBs; b/c 4.82x (prev. 3.25), average yield 3.327% (prev. 3.141%).

- Brazil to sell EUR-denominated 4yr, 7yr and 10yr debt via syndication.

- China's Finance Ministry to reportedly meet with underwrites on Thursday to discuss ultra-long special Treasury Bond issuance, according to Reuters sources.

- France opens book to sell EUR-denominated June 2037 Green Oat via syndicate; guidance seen at +13bps to May 2036 Oat.

COMMODITIES

- In geopolitics, President Trump said Iran had contacted the US and wanted a deal “very badly”, while a US official said talks were still continuing and progress was being made. The US and Iran are discussing a second round of talks, potentially in Islamabad on Thursday, though nuclear weapons and any Strait of Hormuz blockade remain key sticking points. More recently, an Iranian Embassy official in Pakistan said the next round of talks between US and Iran could take place this week or early next week.

- Elsewhere, the IEA completed the monthly trio of oil market reports. In its release, the IEA sees global oil supply exceeding demand by 410k BPD in 2026, (prev. 2.46mln BPD). IEA said crude, fuel, and NGL flows through Strait of Hormuz at 3.8mln BPD in early April (vs more than 20mln BPD pre-war), and added that resuming flows through the Strait of Hormuz is the single most important variable for easing pressure on energy supplies and prices.

- Brent Jun fell below USD 99/bbl (USD 96.50-99.45/bbl range), and WTI Jun resided in a USD 90.19-92.10/bbl parameter. Dutch TTF fell -2.5% in choppy trade. Natgas supply is seen as sufficient this summer despite Iran war-related disruption, with National Gas Transmission expecting domestic output and Norwegian flows to meet demand during the lower-consumption warmer months.

- Spot gold rose to levels just shy of USD 4,800/oz after a two-day decline, as signs of diplomatic engagement slightly eased inflation concerns. The yellow metal resides towards the top end of a USD 4,743-4,797/oz range at the time of writing.

- Copper hit a one-month high and other industrial metals also advanced on optimism around talks, though investors remain cautious over escalation risks. 3M LME copper resides in a USD 13,054.95- 13,201.93/t. In trade, China’s export growth slowed sharply to 2.5% Y/Y in March, missing forecasts after February’s near-40% gain, while imports surged amid energy-related disruption; analysts said Lunar New Year distortions and a high base likely exaggerated the slowdown. Elsewhere, the EU reached a prelim deal to cut tariff-free steel imports by 47% to 18.3mln metric tons per year and double out-of-quota duties to 50%, while also moving to phase out Russian steel imports, potentially by September 2028.

- Russian oil product exports from Black Sea port of Tuapse revised up to 1.27mln tons for April (vs 794k tons in prev. plan), according to traders cited by Reuters.

- IEA OMR: sees world oil demand falling by 80k in 2026 due to Iran (prev. forecast for a 640k BPD rise); sees world oil supply falling by 1.5mln BPD in 2026 (prev. forecast for 1.1mln BPD rise). SUPPLY/DEMAND IEA sees global oil supply exceeding demand by 410k BPD in 2026, (prev. 2.46mln BPD)MIDDLE EAST. IEA said crude, fuel, and NGL flows through Strait of Hormuz at 3.8mln BPD in early April (vs more than 20mln BPD pre-war). Resuming flows through the Strait of Hormuz is the single most important variable for easing pressure on energy supplies and prices. RUSSIA. Russia may struggle to produce oil above levels seen in early Q1 due to attacks on ports. Russia’s March crude production up to 8.96mln BPD from 8.67 mln BPD in February. Russia’s March crude exports up by 270k BPD from February to 4.6mln BPD.

- Ukraine's Zaporizhzhia Nuclear power plant offsite power has been restored via one power line. This comes following reports by the IAEA saying Ukraine’s Zaporizhzhia nuclear power plant lost all off site power earlier in the morning.

- US Energy Secretary Wright said US energy prices will likely rise in the next few weeks and remain until meaningful ship traffic through the Strait of Hormuz resumes. Venezuelan oil production has surpassed 1.2mln bpd, representing a 25% increase over three months. 150mln barrels of Venezuelan oil sold since January 3rd. There is an announcement coming soon about a large American company with a history in Venezuela ramping up production. By this summer is an aggressive timeframe now for oil and gas prices to start coming down.

- Chevron (CVX) is signing a deal with Venezuela's PDVSA aimed at increasing production by joint ventures, according to state TV, while it agrees to asset swap with PDVSA.

- China is said to ease restrictions on certain BHP (BHP AT) iron ore cargoes.

- Petrobras (PBR) reportedly in early stage talks to buy back Brazil's Mataripe refinery from Abu Dhabi's Mubadala.

- SHFE said it will adjust price limits and margin requirements for certain gold and silver futures contracts from listing.

TRADE/TARIFFS

- Chinese President Xi said China and Spain should enhance cooperation and mutual trust, rejects the return to the law of the jungle, adds they are to jointly defend multilateralism and safeguard global development.

- China Foreign Ministry said if the US imposes tariffs on China over Iran related issues, China will take "firm" countermeasures.

- EU Chamber in China warns of expansion of China's export controls and said EU companies continue to suffer from China's export controls on rare earths, according to Handelsblatt.

- EU is considering flexibilities for methane regulation due to US pressure, while EU may ease forest protection law amid US pressure and the Trump administration is pressuring the EU to weaken Green Deal laws, according to Handelsblatt.

- EU reaches a provisional agreement on measures to limit steel imports.

NOTABLE EUROPEAN DATA RECAP

- German Wholesale Prices YoY (Mar) Y/Y 4.1% (Prev. 1.2%).

- German Wholesale Prices MoM (Mar) M/M 2.7% vs. Exp. 0.4% (Prev. 0.6%).

- Spanish Inflation Rate YoY Final (Mar) Y/Y 3.4% vs. Exp. 3.3% (Prev. 2.3%).

- Spanish Inflation Rate MoM Final (Mar) M/M 1.2% vs. Exp. 1.0% (Prev. 0.4%).

- Spanish Core Inflation Rate YoY Final (Mar) Y/Y 2.9% vs. Exp. 2.7% (Prev. 2.7%).

- Swedish CPIF YoY Final (Mar) Y/Y 1.6% vs. Exp. 1.6% (Prev. 1.7%).

- Swedish CPIF MoM Final (Mar) M/M -0.6% vs. Exp. -0.6%.

- Swedish Inflation Rate MoM Final (Mar) M/M -0.6% vs. Exp. -0.6% (Prev. 0.6%).

- Swedish Inflation Rate YoY Final (Mar) Y/Y 0.5% vs. Exp. 0.6% (Prev. 0.5%).

- UK BRC Retail Sales Monitor YoY (Mar) Y/Y 3.1% vs. Exp. 0.9% (Prev. 0.7%).

CENTRAL BANKS

- The BoJ is said to be considering a sharp increase to its price forecast this month, while weighing a possible growth outlook cut due to high oil prices, Bloomberg reports.

- BoE's Mann says concerned that a price shock could show up in wage expectations; inflation expectations are very volatile if CPI is above 3-3.5%.

- ECB's Rehn said it is unclear the war effect on medium term inflation, rate decisions not locked in beforehand. Monetary policy should not be based on a single price, such as oil; it should be based on the economy as a whole. Impact of the war on inflation is not straightforward.

- Fed's Miran (voter, dovish dissenter) said expects inflation to be close to target in a year. No reason to think oil prices will remain elevated. Thus far, seems wise to look through this oil shock.

- The ECB is urging EU governments to fast-track common deposit insurance to break the impasse in banking integration while warning against softening guardrails to boost competitiveness, the FT reported.

- RBA Deputy Governor Hauser said not sure interest rates are at the right level to tame inflation, adds rates need to bring inflation to the 2-3% target and that Q2 headline inflation is around 5% due to fuel costs. Further, RBA's Deputy Governor Hauser said inflation in Australia is too high and Australia's supply capacity is constrained, adds energy price spikes has been a big income shock for Australia.

- Monetary Authority of Singapore tightens policy as expected by slightly raising the rate of appreciation of the SGD NEER policy band, while it made no change to the width and level the band is centred. In an appropriate position to respond effectively to any risk in medium-term price stability. Stands ready to curb excessive volatility in SGD NEER. MAS Core inflation will pick up and remain elevated over next few quarters. GDP growth will slow over the course of the year.

GEOPOLITICS

RUSSIA-UKRAINE

- Russian drones attacked Ukraine's Izmail port and damaged a Panama-flagged vessel, according to Ukraine's Deputy PM cited by Reuters.

OTHERS

- North Korea test fires a cruise missile and anti-warship missiles from a naval destroyer, according to KCNA.

CRYPTO

- Bitcoin nears USD 75k on improved risk sentiment, Ethereum bids towards USD 2.4k.

APAC TRADE

- APAC stocks traded higher as risk sentiment was underpinned by hopes regarding US-Iran peace talks after President Trump suggested Iran called the US and wants to make a deal very badly, while a US official said that talks between the sides are continuing even now and there is progress, with some reports also noting that the second round of face-to-face talks could take place this Thursday, although there hasn't been any confirmation.

- ASX 200 was lifted by outperformance in tech and miners, but with the upside capped following a deterioration in Australian Consumer Sentiment and Business Confidence surveys.

- Nikkei 225 rallied to just shy of the 58,000 level with tech-related stocks dominating the list of best performers, including SoftBank, Advantest, NEC Corp and Renesas, all in the top five biggest gainers.

- Hang Seng and Shanghai Comp gained, but with the advances limited as participants also digested mixed Chinese trade data, in which exports disappointed and imports surged, while China Customs Vice Minister said the international situation is currently turbulent, geopolitical conflicts are intensifying and global oil prices fluctuate sharply.

NOTABLE ASIA-PAC HEADLINES

- South Korean Pension Fund allows more FX hedging to bolster KRW, Bloomberg reported.

- China will refine its drug pricing system with 14 measures, Xinhua reported.

- China Customs Vice Minister said China foreign trade situation had a good start.

- Japanese Finance Minister Katayama said to discuss financial markets and energy conditions with counterparts at meetings and ready to roll out measures to support Asian nations. Will maintain close dialogue with JGB market participants amid rising yields. Specific monetary policy operations are for the BoJ to determine.

NOTABLE APAC DATA RECAP

- Chinese Yuan-Denominated Balance of Trade (Mar) 354.8B (Prev. 1503.49B).

- Chinese Yuan-Denominated Exports YY (Mar) -0.7% (Prev. 36.1%).

- Chinese Yuan-Denominated Imports YY (Mar) 23.8% (Prev. 10.9%).

- Chinese Balance of Trade (Mar) 51.13B vs. Exp. 112B (Prev. 213.62B).

- Chinese Imports YoY (Mar) Y/Y 27.8% vs. Exp. 11.1% (Prev. 19.8%).

- Chinese Exports YoY (Mar) Y/Y 2.5% vs. Exp. 8.3% (Prev. 21.8%).

- Australian NAB Business Conditions (Mar) 6 (Prev. 7).

- Australian NAB Business Confidence (Mar) -29 (Prev. -1).

- Australian Westpac Consumer Confidence Change (Apr) -12.5% (Prev. 1.2%).

- Australian Westpac Consumer Sentiment (Apr) 80.1 (Prev. 91.6).

- Japanese Industrial Production MoM Final (Feb) M/M -2.0% vs. Exp. -2.1% (Prev. 4.3%).

- Japanese Industrial Production YoY Final (Feb) Y/Y 0.4% (Prev. 0.7%).

- Japanese Capacity Utilization MoM (Feb) M/M -0.1% (Prev. 2.9%).

Loading...