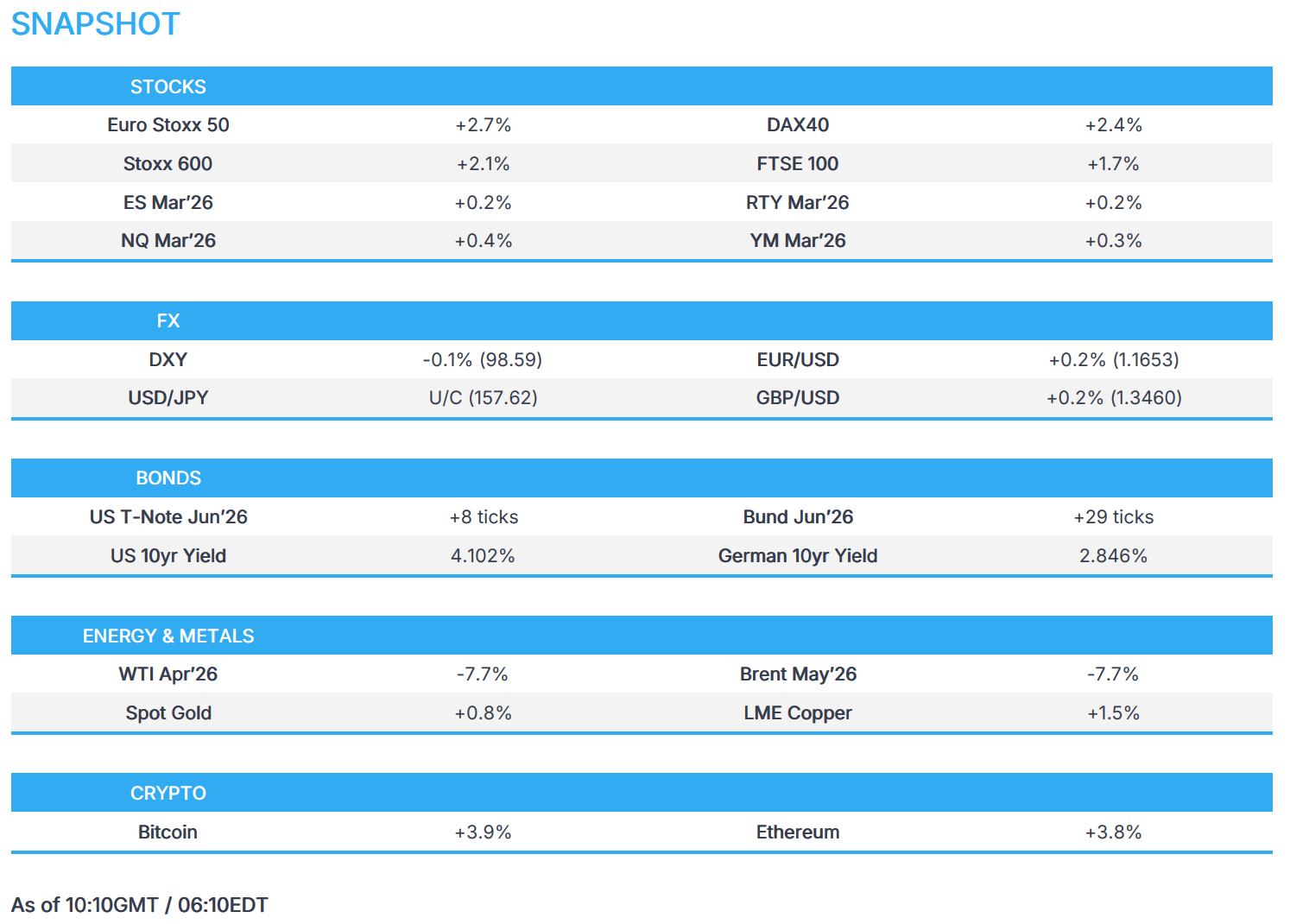

Equities supported on hopes of Iran conflict ending; Trump vows to keep the strait open - Newsquawk US Market Open

- US President Trump said it's going to be ended soon, and if it starts up again, Iran will be hit harder, while he responded 'no, but soon', when asked if the war will be done this week.

- On the passage of oil, US President Trump said they will hit Iran harder if it attempts to stop world oil supply, while adding the Strait of Hormuz will be safe and getting close to finishing it regarding 'excursion'.

- Oil steadies after Monday's selloff after Trump signalled the Iranian war will end soon.

- European equities bounce out of correction territory, with Banks benefiting the most from the positive risk tone; US equity futures continue its reversal.

- Aussie outperforms on hawkish RBA rhetoric and Chinese trade data, DXY takes a breather after yesterday’s slide.

- Fixed income firmer as Monday's hawkish repricing unwinds.

- Looking ahead, highlights include US Weekly ADP, Existing Home Sales (Feb), G7 Energy Minister Meeting, EIA STEO, Supply from the US, Earnings from Oracle.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +2.1%) have rebounded from Monday's losses, with many of the indices returning out of correction territory (>10% pullback from ATHs). The IBEX 35 (+3.1%) is the outperformer, with gains in Santander (+5.9%) supporting the index after the Co.'s President bought 300,000 shares for almost EUR 3mln, as well as the improvement in overall risk tone. The brighter risk environment follows Monday's comments by US President Trump, who suggested that the Iran war could be coming to an end.

- European sectors are in the green, ex-Energy (-0.7%). Sectors that have been hit the hardest due to the Iran war have seemed to have bounced the highest this morning, with Banks (+4.1%), Basic Resources (+3.5%) and Travel and Leisure (+3.5%) sitting near the top of the pile.

- US equity futures (ES/RTY +0.4%, NQ +0.5%) continue to trade higher after reversing the losses posted at the start of Monday's cash session.

- Volkswagen (VOW3 GY) – FY 2025 (EUR): Op. Result 8.9bln (exp. 9.55bln, prev. 19.1bln Y/Y), Revenue 321.9bln (exp. 324.65bln, prev. 324.7bln Y/Y), guides initial FY26 Revenue flat to +3%, Op. RoS 4.0-5.5%. VOW3 shares +3.0%.

- TSMC (2330 TT) February (TWD) rev. rose 22% Y/Y 317.7bln (prev. 401.3bln M/M). TSM shares +0.9% pre-market

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY initially traded flat, before slipping a touch as the morning progressed. Today’s current range is contained within 98.492-98.939 at the time of writing. The day ahead of the US sees weekly ADP and Existing Home sales, although price action will likely be dictated by sentiment surrounding geopolitics.

- EUR/USD is flat with a mild upward bias, but consolidating after yesterday’s Trump-led slide in the USD, with the pair notching a 1.1507-1.1637 range on Monday, vs the current 1.1606-1.1636 range thus far on Tuesday. No move was seen to the German Trade Balance data. As above, price action will likely be dictated by geopolitical and/or energy updates.

- GBP/USD is among the better performers with Cable rising above its 200 DMA (1.3443) to a current high of 1.3483 (vs low 1.3413). This follows yesterday’s surge above its 100 DMA (1.3398) amid the aforementioned USD price action, with Tuesday’s range between 1.3282 and 1.3446.

- USD/JPY lacked direction overnight, and continues to trade sideways this morning after slipping beneath the 158.00 level yesterday, with little reaction to a batch of data releases from Japan, including Q4 GDP revisions that either matched or exceeded the preliminary numbers, while Household Spending surprisingly contracted. USD/JPY currently resides within 157.27-157.96 vs Monday’s 157.63-158.90 range.

- Antipodeans are mixed with AUD/USD outperforming amid firmer copper prices and better-than-expected Chinese trade data overnight, which showed double-digit percentage jumps in exports and imports for Australia and New Zealand's largest trading partner. AUD/NZD, meanwhile, has risen back above 1.1950 and edges closer to 1.2000.

- NOK weakened in the aftermath of softer-than-expected CPI data, with the pair, in a delayed reaction, lifting from 11.1350 to 11.1650 in the five minutes following the release, before hitting an 11.1825 peak around 20 minutes later. The pair made a session high at 11.2334, before pulling back towards the 11.1900 mark.

FIXED INCOME

- A bullish start for fixed, as the complex continues to unwind the energy-induced sell-off from the start of the week.

- USTs are firmer by 10 ticks and at the top of a 112-14+ to 112-24+ band. Continuing to grind higher as energy benchmarks remain under pressure. The US day ahead is primarily a waiting game for any further administration updates on the timeline of the conflict, in addition to a 3yr tap.

- The upside today is most pronounced in Gilts as they catch up to the late Monday commentary from Trump, that the Middle East conflict could be over soon. Gilts gapped higher by 57 ticks, eclipsing the 91.00 handle before continuing to a 91.39 peak, taking out Friday's 91.25 best. If the move continues, there is a bit of a gap before the 92.00 mark and then a cluster of levels just above. Given this, yields have pared notably. The UK 10yr notched a 4.79% peak yesterday, its highest since 4.86% from the 3rd of September 2025. This morning, the 10yr has been as low as 4.53%.

- Bunds are bid, even though the benchmark lifted by over 50 ticks late Monday on the Trump interview. Currently, firmer by 33 ticks but around 25 off a 127.53 peak. Similarly to Gilts, a bit of a gap now before the 128.00 mark and then a cluster of recent levels above. For the ECB, the action has helped markets to calm from the extreme pricing adjustments on Monday. Where, at one point, two 25bps hikes were priced. Currently, around 20bps of tightening is implied by end-2026, vs. c. 7bps this time last week.

COMMODITIES

- Crude futures declined and have completely retraced this week's opening surge. Downside follows comments from US President Trump, who suggested that the war with Iran will end soon. However, comments from the Iranian side this morning has shown little sign of constructive relations, as the Iranian Parliament Speaker said they do not seek a ceasefire. WTI Apr resides towards the middle of USD 84.43-91.48/bbl, while Brent May similar trades mid-range of USD 88.05-98.04/bbl.

- Nat Gas futures were similarly hit, with Dutch TTF this morning -15% and under EUR 50/MWh once again, with the market aggressively "pricing out" the previous risk premium amid US President Trump’s comments.

- Spot gold continues to edge higher, with the metals complex helped by recent dollar softening and as buying resumed amid hopes of a nearing conclusion to the hostilities and disruption in the Middle East. Spot gold trades towards the upper end of a USD 5,117.51-5,195.40 /oz range vs Monday’s hefty USD 5,014.58-5,192.04/oz parameter, in which gold closed at USD 5,136.60/oz.

- Copper futures advanced alongside the improvement in risk appetite, with little initial reaction seen to the latest trade data from the red metal's largest buyer, China. To recap, Trade Balance, Imports, and Exports smashed expectations. China combined its Jan-Feb data to account for the Lunar New Year holiday distortions. 3M LME copper resides in a USD 12,992.00- 13,129.00/t.

- G7 Energy Ministers to meet at 12:45GMT / 08:45EDT.

- Saudi Aramco CEO sees global oil demand to reach record high of 107.3mln BPD in 2026.

- Saudi Aramco CEO said there is a disruption of around 180mln barrels so far; there are no problems related to storage capacity locally or internationally; CEO declines to comment on current oil production levels. "We will operate the East-West Pipeline at full capacity within two days". Have 2mln BPD of spare capacity, so if there are any shutdowns amid the current situation, bringing that spare capacity back will take a matter of days.

- Saudi Aramco plans to increase refining capacity in strategic regions.

- Saudi Arabia, UAE, Iraq and Kuwait reportedly cut oil output by as much as 6.7mln BPD in total, Bloomberg reported citing sources.

- Shanghai Futures Exchange announced the adjustment of price limits and margin ratios for some fuel oil, petroleum asphalt and butadiene rubber futures.

- Taiwan's Formosa Petrochemical (6505 TT) declares a force majeure on some supplies.

- Taiwan's Cabinet said it is to further cut the commodity tax on gasoline and diesel to 50%.

- Japan's Trade Minister Akazawa said Japan supports the IEA-led coordinated release of strategic oil reserves.

- Japan's Chief Cabinet Secretary Kihara reiterates no decision has been made on releasing strategic oil reserves.

- Iran plans to impose duties on tankers and ships in Persian Gulf, according to a source cited by CNN.

TRADE/TARIFFS

- Indian Trade Minister Goyal said there will be no tariff concessions on sugar imports under any trade deal.

- Small businesses sue the Trump administration regarding the new 10% global tariffs, according to the New York Post.

NOTABLE EUROPEAN DATA RECAP

- French Balance of Trade (Jan) -1.8B vs. Exp. -4.6B (Prev. -4.3B, Rev. From -4.8B).

- French Exports (Jan) 53.4B (Prev. 53.0B, Rev. From 53.1B).

- French Imports (Jan) 55.3B (Prev. 57.3B, Rev. From 57.9B).

- German Balance of Trade (Jan) 21.2B vs. Exp. 15.2B (Prev. 17.1B, Rev. From 17.1B).

- German Imports MoM (Jan) M/M -5.9% (Prev. 1.4%).

- German Exports MoM (Jan) M/M -2.3% vs. Exp. -2% (Prev. 4.0%, Rev. From 4%, Low. -2%, High. -1.5%).

- Italian PPI YoY (Jan) Y/Y -1.6% (Prev. -1.4%).

- Italian PPI MoM (Jan) M/M 1.5% (Prev. -0.7%).

- Norwegian Core Inflation Rate MoM (Feb) M/M 0.7% (Prev. 0.3%).

- Norwegian Core Inflation Rate YoY (Feb) Y/Y 3.0% vs. Exp. 3.0% (Prev. 3.4%).

- Norwegian Inflation Rate MoM (Feb) M/M 0.6% (Prev. 0.6%).

- Norwegian Inflation Rate YoY (Feb) Y/Y 2.7% vs Exp. 2.8% (Prev. 3.6%).

- Swedish GDP MoM (Jan) M/M -1.1% (Prev. -0.7%, Rev. From -0.6%).

- UK BRC Retail Sales Monitor YoY (Feb) Y/Y 0.7% vs. Exp. 2.4% (Prev. 2.3%).

CENTRAL BANKS

- ECB's Muller said the chance of rate hit has increased but should not rush, need to see if the surge in energy prices is transitory or not.

- ECB's Simkus said it is important to stay calm until the next policy decision and not to over react, we are aware of the recent changes in market pricing but should stay the course for now.

- RBA Deputy Governor Hauser said Australia's economy is overall in good shape and there will be a very genuine policy debate at the board meeting, with arguments on both sides. A 5% peak for inflation probably looks a little on the pessimistic side; our response depends on size and persistence of the price shock, which is very uncertain. Inflation is too high. Oil price rise clearly an upside risk to the inflation projection but still in flux. Recent data seem to confirm even more decisively that the economy has limited spare capacity. Not all domestic data came in as strongly as expected, including consumption. Uncertainty over developments in Iran is extremely high. Data seems to confirm the economy has limited spare capacity.

GEOPOLITICS

MIDDLE EAST

- Iranian Parliament Speaker said we do not seek a ceasefire and believe in the necessity of teaching the aggressor a harsh lesson.

- Iranian Army said we attacked the oil and gas refinery and fuel tanks in Haifa with drones, Al Hadath reported.

- Iranian military said heavy fire will continue to rain down on aggressors.

- Iranian Foreign Minister Araghchi said negotiations with the US are no longer on the agenda.

- Iran's ambassador to China said that passage through the Strait of Hormuz will be controlled, but the Strait will not be closed.

- Iran's Revolutionary Guards say they will not allow a single litre of oil to be exported from the region if the US and Israeli attacks continue, adds that they will determine how and when the war ends.

- IRGC said the Strait of Hormuz will be open to any state that expels US and Israeli diplomatic envoys from its territory starting tomorrow.

- Iran targeted US sites and depots in Kuwait in recent hours, according to Tasnim.

- US President Trump said it's going to be ended soon, and if it starts up again, Iran will be hit harder, while Trump responded 'no, but soon', when asked if the war will be done this week. said:. Big risk on Iran has been over for three days. We can leave it here but we are going to go further.

- US President Trump said will hit Iran harder if it attempts to stop world oil supply, adds Strait of Hormuz will be safe and getting close to finishing it regarding 'excursion'. said:. Waiving some oil-related sanctions and will take some sanctions off until this straightens out. Winning very decisively and way ahead of schedule.

- US President Trump said we're making major strides towards completing military objective and people could say they're pretty well complete, left some of the most important Iran targets for later. said:. Iran's missile capabilities are down to 10% or maybe less. Could hit Iran's electric production, but don't want to. We're ahead of our initial timeline by a lot. Thinks Iran should put in a head that will be peaceful.

- US President Trump's advisors urged him to find an Iran exit ramp, fearing political backlash, according to WSJ.

- US-Israel aggression targets houses in the Mehrshahr area of Karaj, western Iran, according to Mehr News Agency.

RUSSIA-UKRAINE WAR

- Russia's Kremlin says the trilateral format of the Ukraine talks need to be continued, but no specific dates or locations have been agreed for the next round

CRYPTO

- Bitcoin returns above USD 70k, Ethereum regains the USD 2k handle as risk tone improves.

APAC TRADE

- APAC stocks rose with global risk sentiment underpinned after oil price pressures eased on a potential G7 joint release of emergency reserves, and with relief seen after US President Trump said the war in Iran could end very soon.

- ASX 200 rallied with gains led by outperformance in miners, materials, tech and healthcare, while there was little reaction seen to the improved consumer sentiment and mixed business surveys.

- Nikkei 225 reclaimed the 54,000 status amid softer yields and as exporters cheered the pullback in energy prices. There were also several data releases, including the final Q4 GDP, which either matched the preliminary numbers or were revised upwards, although Household Spending disappointed.

- Hang Seng and Shanghai Comp were in the green, although the mainland bourse lagged behind its regional peers after reports that the US and China clashed over fentanyl and tariffs at a global drugs meeting, while the Trump administration told Beijing it expects to reimpose the fentanyl-related levy under a different law.

NOTABLE APAC DATA RECAP

- Chinese Balance of Trade (Jan-Feb) 213.62B vs. Exp. 179.6B (Prev. 114.10B, Rev. From 114.1B).

- Chinese Exports YoY (Jan-Feb) Y/Y 19.2% vs. Exp. 7.1% (Prev. 6.6%).

- Chinese Imports YoY (Jan-Feb) Y/Y 19.8% vs. Exp. 6.3% (Prev. 5.7%).

- Japanese GDP Growth Rate QoQ Final (Q4) Q/Q 0.3% vs. Exp. 0.3% (Prev. -0.6%, Rev. From -0.7%, Low. 0.1%, High. 0.4%).

- Japanese GDP Growth Annualized Final (Q4) 1.3% vs. Exp. 1.2% (Prev. -2.3%, Rev. From -2.6%, Low. 0.3%, High. 1.5%).

- Japanese Household Spending YoY (Jan) Y/Y -1.0% vs. Exp. 2.5% (Prev. -2.6%, Low. -0.3%, High. 5.2%).

- Japanese Household Spending MoM (Jan) M/M -2.5% vs. Exp. 0.8% (Prev. -2.9%, Low. -0.4%, High. 3.5%).

- Japanese Average Cash Earnings YoY (Jan) Y/Y 3% vs. Exp. 2.5% (Prev. 2.4%).

- Australian NAB Business Confidence (Feb) -1 (Prev. 3).

- Australian Westpac Consumer Confidence Change (Mar) 1.2% (Prev. -2.6%).

- Australian Westpac Consumer Confidence Index (Mar) 91.6 (Prev. 90.5).

- South Korea GDP Growth Rate QoQ Final (Q4) Q/Q -0.2% vs. Exp. -0.3% (Prev. 1.3%).

- South Korea GDP Growth Rate YoY Final (Q4) Y/Y 1.6% vs. Exp. 1.7% (Prev. 1.8%).

Loading...