Equities under pressure as oil gains; US initiate 301 probe into key partners - Newsquawk US Market Open

- IEA OMR cut its 2026 global oil supply growth forecast by nearly half, stating the Middle East conflict as the largest oil supply disruption ever.

- USTR Greer said the US is initiating a Section 301 investigation into 16 trading partners, including China, the EU, Mexico, Vietnam, India and Japan, which could lead to responsive actions, including tariffs.

- European equities hit as Iran conflict continues, while Defence names benefit; Oil prices continue to weigh on US equities.

- DXY continues to benefit from geopols, JPY bucks the G10 trend and holds onto gains.

- Fixed income initially softer but coming off worst levels.

- Crude wanes off best levels after Brent briefly topped above USD 100/bbl, reports suggest that India is in discussions with Iran to secure passage for 20 tankers through Hormuz.

- Looking ahead, highlights include Canadian Trade Balance (Jan), US Trade Balance (Jan), Initial Jobless Claims, Housing Starts, Atlanta Fed GDP and CBRT Policy Announcement. Speakers include Fed's Bowman. Supply from the US, Earnings from Adobe.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

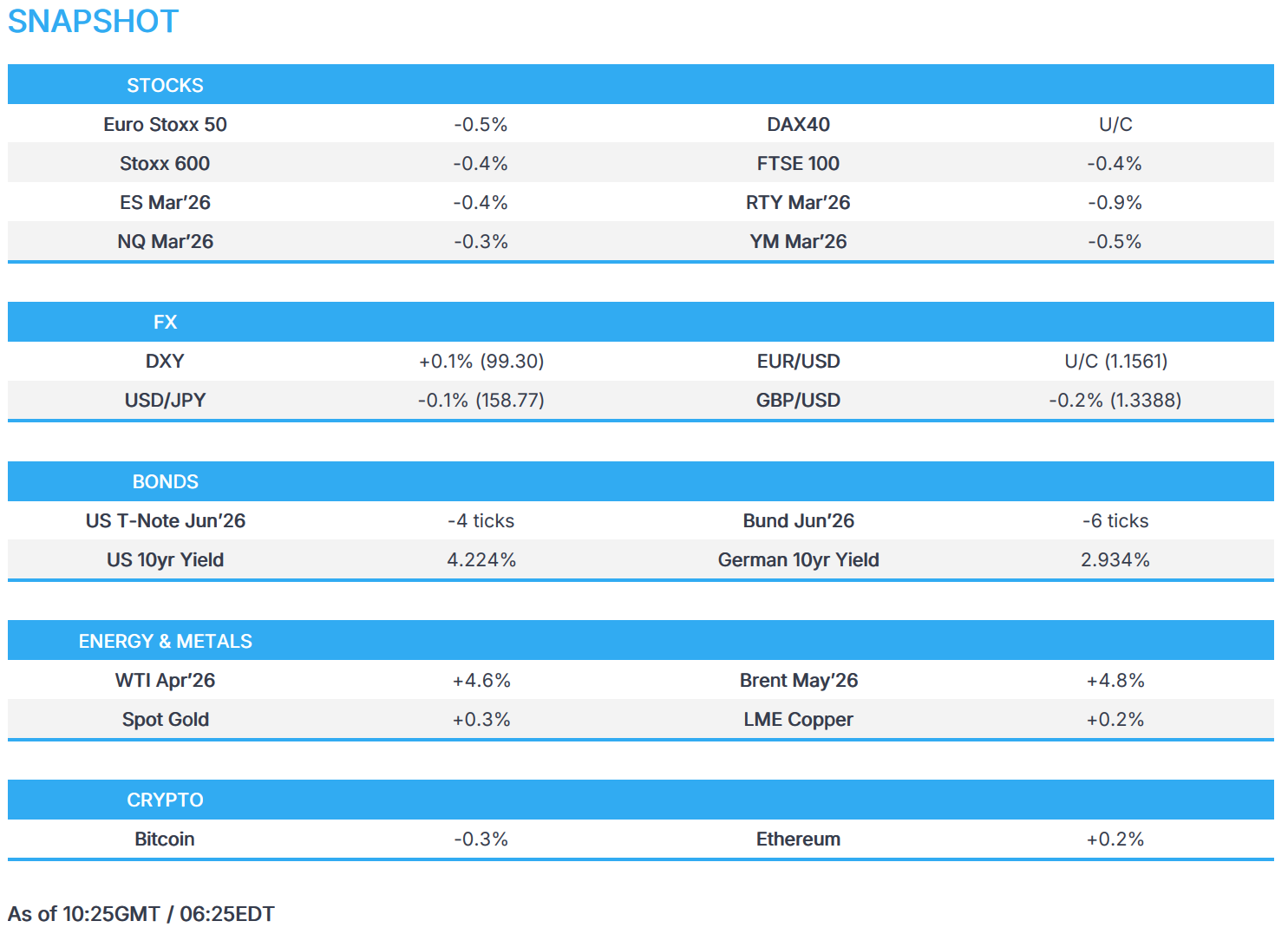

- European bourses (STOXX 600 -0.4%) have started the cash session on the backfoot, with higher oil prices continuing to weigh on growth prospects. Weakness in banks continues to affect the IBEX 35 (-0.9%), given its exposure. The DAX 40 (U/C) is modestly lower, but losses are limited due to gains in Zalando (+12.2%), Rheinmetall (+2.9%) and Hannover Re (+3.2%).

- European sectors are broadly in the red, with Banks (-2.1%) continuing to underperform. Automobiles (-0.9%) also sit near the bottom of the pile after BMW (-1.1%) missed Q4 sales estimates and forecast higher tariffs acting as a headwind on EBIT margin. Basic Resources (+0.7%) are benefiting from the rise in metals prices, while Chemicals (+0.8%) gain after K+S (+8.0%) beat Adj. EBITDA estimates.

- US equity futures (ES -0.4% NQ -0.3%, RTY -0.9%), similar to their European peers, continue to be weighed on by higher oil prices. Correlation between the ES and WTI has become increasingly inverse, now lying at c. -0.8.

- BMW (BMW GY) – Q4 2025 (EUR): EBIT 2.12bln (exp. 1.92bln), Revenue 33.5bln (exp. 37.4bln). FY 2025: Revenue 133.45bln (prev. 142.38bln Y/Y), EBIT 10.18bln (prev. 11.50bln Y/Y).

- Dollar General (DG) Q4 2025 (USD): Adj. EPS 1.65 (exp. 1.64), Revenue 10.82bln (exp. 10.80bln).

- Honda Motor (7267 JT) revises guidance: now projects a FY25/26 loss of JPY 420bln-690bln (vs prior exp. JPY 300bln profit); losses amid asset write-offs on cancelled EV models.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is slightly firmer this morning and trades within a 99.31-99.52 range, and now heading back to the YTD high at 99.69 (March 9th). Upside on Wednesday was facilitated by higher yields as the energy prices continue to trudge higher as the geopolitical situation in Iran is showing little signs of abating any time soon, as an overnight attack on Omani export terminals led Brent back above USD 100/bbl. The recent IEA 400mln barrel reserve release has ultimately had little impact on prices, given the lengthy timeline for the barrels to enter the market and ING rightly points out, it still works out to be “far short of the supply losses we are seeing from the Persian Gulf”. Domestically, weekly jobless claims, trade data and Fed speak via Bowman - though she will not touch on monetary policy.

- G10s are broadly flat to lower against the USD. The JPY and CAD hold afloat, though the former remains within the touted intervention zone beyond 158.00. As mentioned in previous FX pieces, intervention seems unlikely given, a) intervention would prove to be ineffective given the current geopolitical environment, b) low volume short positions on the JPY, c) the move is fundamentally driven by higher energy prices d) the recent lack of verbal intervention suggests potentially higher bar for USD/JPY to rise. Nonetheless, markets will be cognizant of any jawboning heading into the BoJ meeting and wage negations next week.

- AUD underperforms vs USD this morning, scaling back some of this week’s gains. RBA hike bets continue to be taken by sell-side banks, with ANZ the latest see a 25bps increase at next week’s meeting; money markets now assign a circa 80% chance of such a move.

FIXED INCOME

- Another bearish session for fixed as, despite the IEA stockpile announcement, energy benchmarks are on the front foot once again with Brent eclipsing USD 100/bbl in APAC trade and Dutch TTF as high as EUR 53.80/MWh. In brief, energy strength comes as the market digests the time it will take for the IEA flows to hit the market, the Middle East conflict showing no immediate signs of stopping, and the associated ongoing Strait of Hormuz block.

- Given this, USTs are lower by a handful of ticks and holding just off a 111-21 base. If the move continues, we look to support at 111-19+, 111-10 and 111-08+ from earlier in the year. The US docket is headlined by Fed speak and then a 30yr auction to round off the week, after a poor 3yr and a 10yr that was an improvement from the last outing, but softer than the average tap.

- Gilts lower by around 40 ticks at most, hitting a 89.36 trough, which, while notable is still some way clear of the 88.80 MTD low and the 88.52 contract base. Pressure a function of the referenced energy moves and a return towards some of the hawkish BoE pricing seen at the start of the week, with around a 20% chance of a hike by end-2026 currently implied.

- Finally, Bunds followed suit at first and hit a 125.91 base, taking the German 10yr yield to another multi-year high. Amidst this, market pricing got to around an 80% chance of two 25bps hikes by the ECB in 2026; reminder, at most we have seen two hikes fully priced in recent sessions. However, this pared across the mid-morning with the benchmark briefly, but only marginally, moving into the green. No clear or overt fundamental behind the gradual turnaround, but the action is potentially a function of energy benchmarks easing from overnight peaks.

- Italy sells EUR 6.0bln vs exp. EUR 4.75-6.0bln 2.40% 2029, 3.15% 2033 and 3.25% 2038 BTP

- UK sells GBP 500mln 1.825% 2049 I/L Gilt: b/c 3.57x (prev. 3.39x), real yield 2.019% (prev. 2.360%)

- EQT's (EQT SS) EdgeConneX plans a EUR 600mln data centre-backed debt sale.

- Australia sold AUD 150mln in 2032 indexed bonds, b/c 3.97, avg. yield 2.3433%.

COMMODITIES

- WTI and Brent futures trade firmer but off best levels after Brent futures briefly rose above USD 100/bbl in APAC hours, with the former currently in a USD 88.61-95.97/bbl range and the latter in a USD 96.69-101.59/bbl parameter. The gains come amid a war that seems to be escalating rather than abating (full Newsquawk Analysis available on the headline feed).

- European natgas prices are firmer but off their best levels after rising almost 8% in sympathy with crude prices. The EU’s Dombrovskis warned that inflation could exceed 3% this year if the Middle East war keeps Brent around USD 100/bbl and gas prices elevated for a prolonged period; under that scenario, 2026 growth would be up to 0.4ppts below the 1.4% pace forecast late last year.

- Spot gold is mildly firmer this morning and largely moves in tandem with the USD, which in turn tracks oil prices. Gold retreated overnight following US CPI data, which reduced expectations for any near-term Fed rate cuts, and as the Middle East conflict lifted crude prices. XAU/USD resides in a USD 5,125.64-5,189.86/oz range within Tuesday’s USD 5,117.35-5,238.75/oz.

- 3M LME copper ekes mild gains on either side of USD 13,000/t as the red metal largely tracks the USD and oil for any impact on the growth narrative, with further upside likely capped by the US initiating a Section 301 investigation into 16 trading partners, including China, the EU. 3M LME copper currently resides in a narrow USD 12,920.60-13,055.88/t range at the time of writing.

- IEA OMR: cuts 2026 global oil supply growth forecast to 1.1mln BPD (prev. 2.4mln BPD), total 2026 supply forecast 107.2mln BPD (prev. 108.6mln BPD). Middle East conflict is the largest oil supply disruption ever. Demand Forecasts. 2026, total: 104.8mln BPD. 2026, growth: 640k BPD (prev. 850k BPD). OPEC+ production decreased by 210k BPD in February.

- US is to release 172mln barrels of crude from strategic petroleum reserve, according to Energy Department. The release will begin next week, with delivery expected to take around 120 days based on planned discharge rates, while the US will replace reserves by 20% more than what will be withdrawn. SPR release is part of the broader coordinated crude oil release from IEA member countries in response to the Iran war.

- US President Trump said IEA decision to release oil from reserves will substantially reduce oil prices.

- Oman’s Mina Al Fahal crude export terminal has resumed normal operations after a temporary halt earlier Thursday, with loading activities now proceeding as usual, according to reported.

- Iraqi official said oil ports have completely stopped operations, while commercial ports continue to operate following attack on two fuel tankers.

- India is in discussions with Iran to secure passage for 20 tankers through the Strait of Hormuz, Bloomberg reported citing sources.

- US Energy Secretary Wright said hope to see ships through the Strait of Hormuz in a few weeks.

- China reportedly expands BHP's (BHP AT) iron ore ban to new products, asking domestic steel mills not to take delivery from BHP's Portside Newman fines from next week.

TRADE/TARIFFS

- USTR Greer said US is initiating Section 301 investigation into 16 trading partners, including China, EU, Mexico, Vietnam, India and Japan, adds the investigation could lead to responsive actions, including tariffs. Said the EU has done approximately 0% of what was agreed in the bilateral trade deal.

- South Korea parliament passes US investment bill, as expected.

NOTABLE EUROPEAN HEADLINES

- Germany's IFW institute sees 2026 inflation at 2.5% (prev. 1.8%), GDP at 0.8% (prev. 1.0%), 2027 GDP at 1.4% (prev. 1.3%).

NOTABLE EUROPEAN DATA RECAP

- Swedish CPIF MoM Final (Feb) M/M 0.6% vs. Exp. 0.6% (Prev. 0.3%).

- Swedish CPIF YoY Final (Feb) Y/Y 1.7% vs. Exp. 1.7% (Prev. 2.0%); XE 1.4% (exp. 1.4%).

- Swedish Inflation Rate MoM Final (Feb) M/M 0.6% vs. Exp. 0.6% (Prev. 0.1%).

- Swedish Inflation Rate YoY Final (Feb) Y/Y 0.5% vs. Exp. 0.5% (Prev. 0.5%).

- UK RICS House Price Balance (Feb) -12% vs. Exp. -9% (Prev. -10%).

CENTRAL BANKS

- Bank of Japan Governor Ueda said foreign exchange is an important factor affecting the economy and prices, during parliamentary testimony. Need to be mindful that Forex has larger impacts on prices than in the past and could affect inflation expectations. Will conduct appropriate monetary policy while assessing how Forex affects the likelihood of our forecasts.

- ANZ Bank and Goldman Sachs now see the RBA hiking the Cash Rate at next week's meeting.

- NBP's Janczyk said the current base rate is at an appropriate level for the coming quarters.

- BoK member Hwang said need to make rate decision with greater caution.

NOTABLE US HEADLINES

- US President Trump is to signs orders on housing in the coming days, according to Punchbowl citing a White House spokesperson.

- BofA Card Spending (w/e March 7th): +4.6% Y/Y, vs 3.2% in February. Y/Y spending appears to be robust in the early part of March.

GEOPOLITICS

MIDDLE EAST

- A senior US administration official, on the Middle East conflict and President Trump's view, said "The Iranians fcking around with the Strait makes him more dug in". An advisor said that Trump is bullish on the success of the operation thus far and believes the American people will believe it was the right approach once it is over. Advisor adds that Trump, and others in the administration, genuinely believe that gas prices will substantially fall when the Middle East conflict concludes, and long enough before the midterms to not be a problem.

- US President Trump was reportedly "ambiguous and noncommittal" during the G7 leaders call, Axios reported; with some participants thinking POTUS wants to end the war, while other attendees left with the opposite view.

- US President Trump said we knocked out Iran's navy and mine layers, adds oil prices will come down, but we won't leave early. said the job on Iran must be finished and don't want to return every two years.

- US President Trump said we know where Iranian sleeper cells are and have eyes on all of them, adds we are going to look very closely at the Straits.

- Reports of a drone attack on a US military base in Kuwait, Tasnim reported.

- According to Lebanese newspaper citing diplomatic sources, Iran clarified that they defend itself against American and Israeli aggression and that it will not agree to a ceasefire that is not accompanied by clear guarantees, via N12 News reporter Lipkin.

- Officials from four nations are attempting to persuade Iran to begin talks with the US, Jerusalem Post reported citing sources; however, thus far, Iran has refused to engage and is maintaining a hardline position.

- Reports suggests that Iran says it struck a US oil tanker in the Strait of Hormuz.

- Iran said it gives permission for Indian oil tankers to pass through the Strait of Hormuz. This was later denied by an Iranian source.

- "The campaign against Hezbollah will not be short and will not adhere to a specific timetable", according to Sky News Arabia citing Israeli officials.

- Iranian explosive-laden boats hit two fuel tankers in Iraqi waters.

- Iran military-affiliated outlet Defa press cites informed sources that note Yemeni resistance and some other resistance groups are fully prepared to join the battle in the coming days. According to predictions, with the entry of these groups, there is a risk of closing the strategic Bab-al-Mandab Strait which would disrupt transit in the Suez Canal.

- UKMTO received a report of an incident 35 nautical miles north of Jebel Ali in United Arab Emirates, in which a container ship was struck by an unknown projectile causing a small fire, while all crew are safe.

- Saudi Ministry of Defence said they are intercepting a drone heading to the Shaybah oil field, Sky News Arabia reported; reported suggest the interception was successful.

- Qatar residents reportedly receive mobile alert for missile threat.

RUSSIA-UKRAINE

- Ukrainian President Zelensky will meet with French President Macron in Paris on Friday.

CRYPTO

- Bitcoin holds below USD 70k while Ethereum continues to trade above 2k.

APAC TRADE

- APAC stocks declined as rising oil prices dampened sentiment and stoked inflationary concerns, while the announcement of a record joint emergency reserves release failed to drag energy prices lower, due to likely slow deliveries and with further disruptions in the Middle East from the ongoing hostilities.

- ASX 200 was dragged lower by losses in nearly all sectors aside from energy, and with further calls by large banks for the RBA to deliver a back-to-back rate hike next week.

- Nikkei 225 briefly slumped below the 54,000 level as the higher oil prices lifted yields and weighed on manufacturer and exporter sentiment.

- Hang Seng and Shanghai Comp conformed to the broad downbeat mood in the region, with risk appetite also not helped by the announcement that the US is initiating a Section 301 investigation into 16 trading partners, including China, the EU, Mexico, Vietnam, India and Japan.

NOTABLE ASIA-PAC HEADLINES

- Japanese PM Takaichi said won't rule out using FY25 reserve funds for fuel and the existing fund has JPY 280bln remaining, adds no additional budget for fuel subsidies now and will use existing fund for fuel price measures.

NOTABLE APAC DATA RECAP

- Australian Consumer Inflation Expectations (Mar) 5.2% (Prev. 5.0%).

- Japanese Foreign Bond Investment (Mar/07) 399.8 (Prev. -673.1).

- Japanese Stock Investment by Foreigners (Mar/07) 385.5 (Prev. 973.9).

Loading...