Europe primed for a lower open amid lack of progress in US/Iran; hefty speaker slate + NVIDIA earnings due - Newsquawk EU Market Open

- Iran's position in talks with the US to end the war hasn't changed much from earlier iterations that failed to yield progress towards a deal, according to WSJ, citing mediators and US officials.

- US Vice President Vance said he had spoken with President Trump regarding Iran and stated that Tehran had two options: either reach an agreement or resume the war.

- A US intelligence assessment recently showed that US forces identified at least 10 mines in the Strait of Hormuz, according to CBS, citing US officials.

- Samsung Electronics’ (005930 KS) largest labour union will begin an 18-day strike on 21st May after wage talks broke down, Yonhap reported.

- APAC stocks declined following the weak handover from the US; European equity futures indicate a lower cash market open with Euro Stoxx 50 futures down 0.6%.

- Looking ahead, highlights include German PPI (Apr), UK Inflation Report (Apr), EU Inflation Final (Apr), New Zealand Trade Balance (Apr), and FOMC Minutes (Apr). Speakers include US President Trump, Fed's Paulson & Barr, BoE's Bailey, Breeden, Dhingra & Mann. Supply from Germany & US, Earnings from NVIDIA, Target & Intuit.

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- Iran's position in talks with the US to end the war hasn't changed much from earlier iterations that failed to yield progress towards a deal, according to WSJ citing mediators and US officials. Furthermore, it was reported that US and Israel had been preparing to carry out new attacks on Iran within days, and some said strikes could still happen as early as next week.

- US seized an Iran-linked ship in the Indian Ocean as US President Trump threatened to resume strikes, according to WSJ citing three US officials.

- US Vice President Vance said he had spoken with President Trump regarding Iran and stated that Tehran had two options: either reach an agreement or resume the war. Vance said significant progress had been made on Iran and noted that the military campaign could be restarted if necessary, but added that Trump did not want to pursue “option B” in Iran. Furthermore, Vance believes Iran wants to make a deal, but stated that “we won't know until they sign the deal”.

- US intelligence assessment recently showed that US forces identified at least 10 mines in the Strait of Hormuz, according to CBS citing US officials.

- US Senate voted 50-47 to advance war powers resolution that would end US strikes on Iran unless approved by Congress.

- Israeli assessments indicate that US President Trump has made the decision to attack Iran and that implementation is only a matter of time, according to Al Hadath citing Israel's Channel 12.

- Iranian Foreign Minister Araghchi said months after the start of the war on Iran, US Congress acknowledged the loss of dozens of aircraft worth billions, and Iran's powerful Armed Forces are confirmed as the first to strike down a touted F-35, while he added that with lessons learned and the knowledge they gained, a return to war will feature many more surprises.

- Iran said the claim by the US that an Iranian school, which was struck at the beginning of the war, was located within a cruise missile base is 'baseless'.

US TRADE

EQUITIES

- US stocks ended the day in the red amid the broader risk-off sentiment, although sectors closed more mixed. Sentiment was soured through the duration of the day, while further pressure was seen after WSJ reported that mediators see little progress in Iran-US talks and that Iran's position to end the war hasn't changed much from earlier iterations that failed to yield progress towards a deal.

- SPX -0.67% at 7,354, NDX -0.61% at 28,819, DJI -0.65% at 49,369, RUT -1.01% at 2,747.

- Click here for a detailed summary.

TARIFFS/TRADE

- Federal authorities are examining whether Chinese companies deliberately restricted the world's production of storage containers for the shipping trade just before the pandemic began six years ago, while several Chinese executives have been indicted, according to sources cited by CBS.

- China's MOFCOM confirmed China will purchase 200 Boeing (BA) jets and said the US is expected to provide engines and parts support for the China Boeing deal. MOFCOM announced a resumption of poultry imports from certain US states and said China reinstated qualified US beef exporter registrations, while it stated the US and China are seeking to extend the Kuala Lumpur trade agreement.

- EU lawmakers and member states reached a compromise early on Wednesday to implement a trade pact with the US, aiming to meet President Trump's July 4th deadline and avert tariff hikes.

NOTABLE HEADLINES

- Fed's Paulson (2026 voter) said inflation remains too high and interest rate cuts may only happen after inflation is controlled, while he also commented that current policy is appropriate and it is healthy for markets to consider an extended hold or hikes. Paulson stated the US labour market is stable and consumption is slowing, but is resilient, and a rate hike may be considered if growth moves above potential or other inflation risks emerge. Furthermore, he reiterated that he did not see a need to change language at the last policy meeting, as well as noted that risks are 'super-elevated' right now to both inflation and the outlook.

- US President Trump is to attend the G7 summit in France in June and is to talk about artificial intelligence, trade and crime-fighting, according to Axios.

- US President Trump signed a fintech Executive Order to protect the US financial system from illicit activity, while it was reported that the White House plans to release an Executive Order on cybersecurity and AI safety as soon as this week, which seeks early government access to advanced models.

APAC TRADE

EQUITIES

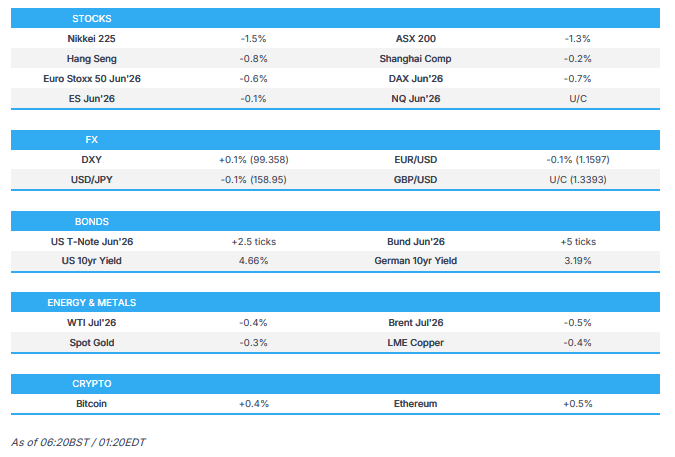

- APAC stocks declined following the weak handover from the US, with sentiment dampened amid headwinds from a higher yield environment and the uncertain geopolitical backdrop.

- ASX 200 retreated with the declines led by underperformance in the mining and materials sectors, while a lack of data and firmer yields contributed to the uninspired mood.

- Nikkei 225 fell beneath the 60,000 level with notable pressure in machine tool and electrical equipment manufacturers, while recent comments from Japan's Finance Minister, and current FX levels were seen to stoke intervention risks.

- Hang Seng and Shanghai Comp conformed to the downbeat sentiment amid bond and inflation woes, with the declines in Hong Kong led by mining, solar and property stocks, while there was a lack of surprises from the PBoC announcement to maintain the benchmark Loan Prime Rates for the 12th consecutive month.

- US equity futures were lacklustre following the recent inflationary concerns and bond selling, while participants look ahead to NVIDIA earnings after-market on Wednesday.

- European equity futures indicate a lower cash market open with Euro Stoxx 50 futures down 0.6% after the cash market closed flat on Tuesday.

FX

- DXY paused overnight after gaining against its major peers yesterday as global government bond yields continued to march higher amid inflationary concerns and the ongoing geopolitical backdrop, with US President Trump suggesting a 2-3 day timeline on Iran, or "maybe until early next week", and it was also reported that Iran's position in talks with the US to end the war hasn't changed much from earlier iterations that failed to yield progress towards a deal. Participants now look ahead to FOMC Minutes and NVIDIA earnings, while there were recent comments from Fed's Paulson who said that inflation remains too high and interest rate cuts may only happen after inflation is controlled, as well as stated that current policy is appropriate and that it is healthy for markets to consider an extended hold or hike.

- EUR/USD lacked conviction after retreating throughout the prior day amid a firmer buck to breach 1.1600 to the downside, with little help in the single currency from comments by ECB Nagel, who stated the ECB is moving away from the baseline scenario, and will take the next rate decision based on data in June.

- GBP/USD trickled beneath the 1.3400 handle in a somewhat choppy fashion following mixed employment and average earnings data, while the latest UK inflation figures are scheduled for today.

- USD/JPY pulled back beneath the 159.00 level in the absence of any key data releases and with participants mindful of increased intervention risks amid the nearby, critical 160.00 threshold.

- Antipodeans were contained amid the downbeat risk sentiment and sparse overnight calendar.

- PBoC set USD/CNY mid-point at 6.8397 vs exp. 6.8072 (prev. 6.8375).

FIXED INCOME

- 10yr UST futures were contained following the prior day's losses amid inflationary concerns and as the Middle East conflict drags on with no clear end in sight, despite US President Trump reiterating that the war will end very quickly and that Iran wants to make a deal badly.

- Bund futures are off the prior day's trough but with the rebound limited following the recent global bond rout, while participants await German PPI data and a Bund issuance.

- 10yr JGB futures were indecisive following the recent losses in global peers and amid a quiet overnight calendar, while some pressure was seen after a weaker 20yr JGB auction and with sources noting that Japan may introduce new JGBs targeting retail buyers.

COMMODITIES

- Crude futures were rangebound overnight following the recent choppy performance and as the geopolitical landscape remained uncertain with US President Trump warning that they could hit Iran again, but is not yet sure, and that Iran is begging to make a deal, while he suggested a timeline for Iran could be 2-3 days or early next week. Furthermore, it was reported that the US seized an Iran-linked ship in the Indian Ocean, and Iran's position in talks with the US to end the war was said not to have changed much from earlier iterations that failed to yield progress towards a deal.

- US Private Inventory Data (bbls): Crude -9.1mln (exp. -3.4mln), Distillates -1.0mln (exp. -1.3mln), Gasoline -5.8mln (exp. -2.1mln), Cushing -1.4mln.

- US Energy Secretary Wright said the US is not going to run out of gas and that high gas prices are a price the US has to pay.

- Two Chinese supertankers, carrying 4mln barrels of oil, exited the Strait of Hormuz on Wednesday, according to tracking data. It was later reported that India was preparing to send oil tankers through the Strait of Hormuz following prior reports regarding the Chinese tankers.

- UK government permits the provision of certain services and actions related to the import of diesel and jet fuel processed in third countries from Russian crude oil.

- Spot gold mildly retreated after failing to sustain a brief return to above the USD 4,500/oz level.

- Copper futures were subdued amid the mostly negative risk sentiment following the recent global bond rout.

CRYPTO

- Bitcoin was choppy and kept to within a tight range above the USD 76,000 level.

NOTABLE ASIA-PAC HEADLINES

- Chinese Loan Prime Rate 1Y (May) 3.0% vs. Exp. 3.0% (Prev. 3.0%)

- Chinese Loan Prime Rate 5Y (May) 3.5% vs. Exp. 3.5% (Prev. 3.5%)

- Chinese President Xi met Russian President Putin in Beijing and said that relations have reached their current level due to deepened political mutual trust and strategic cooperation, while Putin said ties between Russia and China support broader international stability. Furthermore, China and Russia plan to deepen continuous strategic coordination, and Putin invited Chinese President Xi Jinping to travel to Russia next year, while Xi told Putin that the world faces the risk of regressing into a “law of the jungle.”

- BoJ Governor Ueda said the latest GDP data is mostly in line with its forecast, and the Middle East situation has begun to have an impact, while they need to closely monitor signs of upward price pressures. Ueda said he is aware that long-term interest rates are rising rapidly and responded that they will assess the market situation and functionality when asked about BoJ tapering plans, while he reiterated that they will take appropriate monetary policy to achieve the inflation target.

- Japanese Finance Minister Katayama said they are ready to take decisive action on FX.

- Samsung Electronics’ (005930 KS) largest labour union will begin an 18-day strike on 21st May after wage talks broke down, Yonhap reported.

GEOPOLITICS

RUSSIA-UKRAINE

- EU governments are discussing whether former ECB President Draghi or former German Chancellor Merkel could represent the bloc in potential negotiations with Russian President Putin, according to FT.

OTHER

- US President Trump said Cuba is a failed nation that needs help from the US, while he believes a diplomatic deal can be made, according to Semafor.

- US indictment of former Cuban president Raúl Castro is expected to be announced today, according to two federal sources familiar with the investigation cited by NBC News.

EU/UK

NOTABLE HEADLINES

- BoE's Breeden said plans for a digital gilt will make Britain’s sovereign debt more appealing to a wider pool of investors and help lower government borrowing costs, according to City AM.

- UK’s Andy Burnham won’t commit to keeping Labour’s manifesto promises on tax and has opened the door to new tax rises if he becomes PM, while his decision to back the current fiscal rules wins him a reprieve from markets, but it limits his options to fund policies like council house-building, and raises the prospect of tax hikes, according to Bloomberg's Wickham.

Loading...