Europe primed for lower open as energy adds to gains and US-Iran strikes continue - Newsquawk EU Market Open

- US struck Iran overnight, Trump said they will do so again on Wednesday night. Adding, they will hit power plants and bridges next week unless Iran negotiates.

- IRGC targeted weapons/storage in Bahrain and Kuwait, US positions in Jordan and the Fifth Fleet Command HQ. Iran said it is a mistake to think military action will force them to talk.

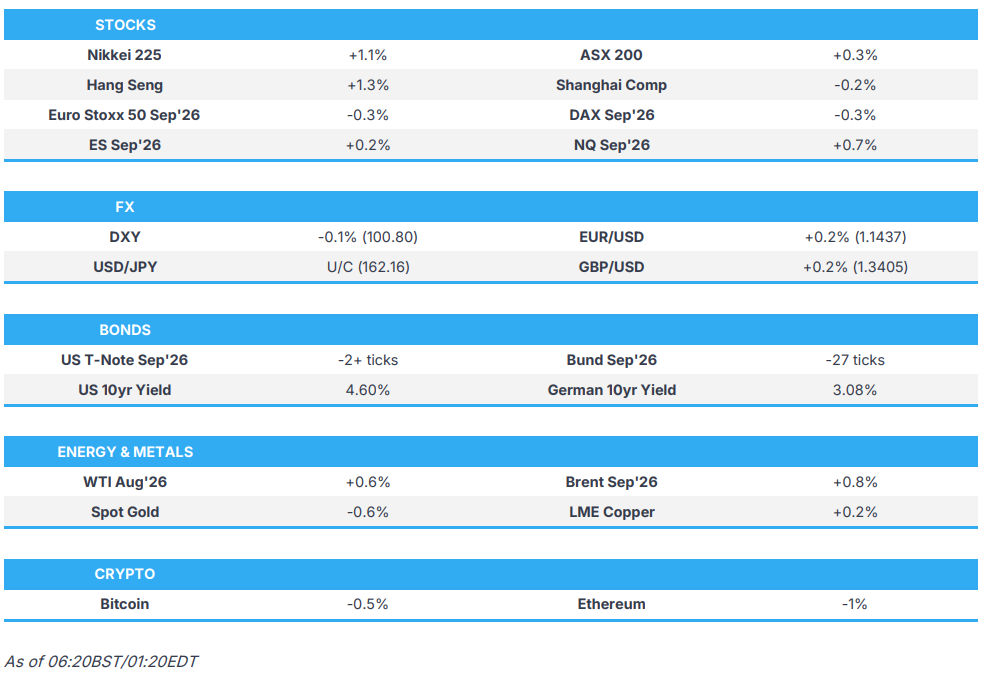

- Brent +0.8% on the above, USD failed to benefit with CPI continuing to weigh, USTs rangebound though Bunds came under modest pressure.

- APAC stocks were firmer as the US CPI read-across outweighed fresh US-Iran strikes, to the continued benefit of US futures, though Europe points lower, Euro Stoxx 50 -0.2%.

- GBP and EUR led on the softer USD, USD/JPY briefly moved below 162.00

- Looking ahead, highlights include Swedish CPIF Final (Jun), Spanish CPI Final (Jun), EZ Industrial Production (May), US PPI (Jun), BoC Policy Announcement (Jul), Fed Beige Book (Jul), Speakers including Fed’s Williams, Musalem, Warsh & Cook, BoC Governor Macklem, BoE's Pill, ECB's Nagel, Supply from Germany, Earnings from United Airlines, BlackRock, Elevance Health, Johnson & Johnson, Morgan Stanley, PNC Financial Services, BNY Mellon.

- Click for the Newsquawk Week Ahead.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US President Trump said in a pre-recorded Fox News interview that they are beating up Iran badly and Hormuz has to stay open, while he added that strikes will continue until he says it is enough, as well as stated they will save energy targets for last and will ultimately hit energy targets. Trump also said they will hit Iran hard on Wednesday night, and that next week will get really bad for Iran, in which they will hit Iran's power plants and bridges next week unless Iran comes to the negotiating table. Furthermore, he said US officials spoke to Iran on Tuesday and told Iran that it better make a deal.

- US President Trump held a Situation Room meeting on Tuesday regarding Iran strikes and discussed a wider scope of strikes on Iran, according to Axios.

- US President Trump said, on the change to the Hormuz toll proposal, that countries had called on him and Gulf countries had asked to handle the Hormuz fee in a different way. Trump also stated that countries had offered investments, and that he did not think anyone should charge a fee in the Strait, while he added that Gulf nation investment was better than imposing a fee, and that he had spoken to Saudi Arabia, the UAE, Qatar, Bahrain and Kuwait. Furthermore, Trump said he has no regrets regarding the Iran sanctions waiver and that they gave Iran a chance by lifting the blockade before, while he added that Iran shot first, which was a big mistake.

- US official said US forces carried out a few additional strikes on military targets in Iran earlier on Tuesday, while the latest US strikes in Iran were carried out to eliminate emerging threats.

- US Central Command forces began launching an additional round of strikes against Iran at 15:00EDT/20:00BST on Tuesday, to continue degrading Iranian capabilities used to attack commercial shipping in the Strait of Hormuz, while CENTCOM later announced the completion of strikes against Iran.

- US forces resumed the naval blockade against vessels transiting to and from Iranian ports.

- US struck Qeshm Island in southern Iran, and explosions were heard in the maritime area of eastern Hormozgan and Sirik, while explosions were heard in Bandar Abbas and Hengam Island. Explosions were also heard in Bampur and Chabahar in Iran, although Iran's semi-official news agency Tasnim noted officials denied reports of explosions in Chabahar, while explosions were reported in Iran's port city of Bandar Imam Khomeini, and a mineral water plant in Deloran was hit by three projectiles. Furthermore, reports noted that air defences around the Bushehr Nuclear Power Plant in Iran became active.

- IRGC said it targeted enemy weapons and parts storage in Bahrain and Kuwait, while it targeted a drone ramp in Kuwait's Ali Al Salem air base and targeted US positions at Jordan's Azraq base, as well as the US Fifth Fleet Command HQ, fuel facilities and equipment in Bahrain. IRGC said as long as the US evil stays in the region, not a drop of oil and gas will be exported from the region, and that US aggression will have no result other than delaying the opening of the Strait of Hormuz.

- Iran's Deputy Foreign Minister said Gharibabadi the US is making a mistake if it thinks its military attacks and blockade will force them to request negotiations, but also commented that Iran's return to negotiations and tolerance regarding the Strait of Hormuz is possible. Furthermore, he said the MoU effectively no longer exists and that no country should expect Iran to continue implementing the terms of the memorandum.

- US Treasury issued fresh Iran sanctions on entities, individuals, and vessels.

- UK Foreign Office summoned the Iranian charge d’affaires over proxy group assaults.

- The first day of Lebanese-Israeli negotiations in Rome was positive, although Israeli forces were also reported to have carried out massive explosions in Kafr Tibnit, Lebanon.

US TRADE

EQUITIES

- US stocks closed in the green and reversed earlier pressure seen following dismal prelim. Q2 IBM earnings, with a cooler-than-expected US CPI report helping unwind the initial downward move. Following the inflation metrics, which were cooler than expected across all gauges, immediate downside was seen in US yields and the dollar, to the benefit of FX peers, spot gold, and equities. Oil prices saw gains as the US and Iran continued to trade strikes, and the blockade restarted today, although Trump backed off his plan to charge a 20% fee for safe passage through the Strait of Hormuz, and will pivot to trade deals to cover the US costs of assuring safe passage through the Strait. Elsewhere, Fed Chair Warsh testified in front of the House, and speaking on today's inflation data, said it does not say mission accomplished, and he does not think that after today's CPI report, that everything is swell, while he stated it is one data point, and does not want to overread or cherry-pick data.

- SPX +0.38% at 7,544, NDX +1.10% at 29,586, DJI +0.02% at 52,513, RUT +0.39% at 2,965.

- Click here for a detailed summary.

TARIFFS/TRADE

- Japan considers lifting the ban on US potato imports, according to Nikkei.

NOTABLE HEADLINES

- Fed Chair Warsh said today's inflation data did not mean mission accomplished and that he did not think everything was swell after the CPI report, while he added it was one data point and cautioned against overreading or cherry-picking the data. Warsh reiterated the Fed's commitment to the 2% inflation target, saying the central bank would deliver 2% inflation, and stated that June CPI was softer than expected, but stressed he was not cherry-picking the data and noted there was still plenty of work to do.

- Fed's Goolsbee (2027 voter) said June CPI inflation was surprisingly benign and that was encouraging, but cautioned against overreacting to one month's data, while he added that if the Fed received several months of similar inflation readings, he would feel better. Goolsbee also stated that services inflation was encouraging, and that if several months of PCE inflation mirrored the CPI data, he would feel much more confident, as well as commented that the labour market was stable without being strong.

- Fed's Barr (voter) published a paper titled, "Will AI Broadly Raise Living Standards or Drive Income and Wealth Inequality?", saying scenarios for AI adoption varied widely regarding how AI might affect inequality. Barr said AI, like past major technological advances, would shape the labour market and the broader economy in myriad ways, while adding that it remained unclear whether AI would reduce or increase income and wealth inequality.

- US President Trump said he thinks the inflation trend will hold and noted inflation is down, while he stated the report was incredible and to remember that for the midterms. Furthermore, he said they will bring prices much lower yet.

- US House voted to make daylight saving time permanent and sent the bill to the Senate.

APAC TRADE

EQUITIES

- APAC stocks traded with a positive bias as most major indices took impetus from the gains on Wall St, where sentiment was underpinned, and Fed rate hike bets were trimmed following softer-than-expected CPI data, while US President Trump also abandoned plans for a 20% Hormuz fee.

- ASX 200 eked out marginal gains with outperformance in miners following Rio Tinto's quarterly update, although the upside in the index was capped as defensives lag.

- Nikkei 225 rallied amid tech strength, but with further upside limited following weak Machinery Orders.

- KOSPI was boosted by the tech-related momentum and with SK Hynix shares up by a double-digit percentage as it played catch-up to the 27% surge in its ADRs.

- Hang Seng and Shanghai Comp diverged with the mainland lagging after a slew of mixed data releases, including Chinese GDP and activity data.

- US equity futures kept afloat following softer US CPI data and the start of earnings season.

- European equity futures indicate a lower cash market open with Euro Stoxx 50 futures down 0.2% after the cash market closed with gains of 0.2% on Tuesday.

FX

- DXY remained subdued after weakening in the aftermath of the softer-than-expected CPI data, which resulted in some unwinding of Fed rate hike bets, although Fed Chair Warsh noted that the inflation data did not mean the mission was accomplished and cautioned against overreading or cherry-picking the data, while participants also look ahead to PPI data and more Fed speakers, including Warsh's testimony to the Senate.

- EUR/USD benefited from the softer buck and reclaimed the 1.1400 status, while catalysts remained light for the bloc, although there were reports that the EU was set to propose easing banks' capital requirements.

- GBP/USD returned to above the 1.3400 level as cyclical currencies are underpinned by the positive risk environment, while previous comments from BoE Governor Bailey had little impact, in which he noted that the core banking system in the UK was resilient and debt levels were not stretched.

- USD/JPY retested the 162.00 level to the downside after US yields retreated post-CPI, but with downside limited amid higher oil prices and disappointing Machinery Orders data from Japan.

- Antipodeans marginally edged higher owing to their high-beta statuses, but with the upside capped as participants also digested mixed Chinese GDP and activity data.

- PBoC set USD/CNY mid-point at 6.7910 vs exp. 6.7695 (prev. 6.7990).

FIXED INCOME

- 10yr UST futures struggled for direction after reversing the post-CPI spike and with Fed Chair Warsh noting the inflation data did not mean mission accomplished, while he cautioned against overreading the data.

- Bund futures were subdued amid higher energy prices and with EUR 3bln of Bund issuances due later.

- 10yr JGB futures held on to recent spoils, albeit with price action choppy overnight following disappointing Machinery Orders data and the mostly positive risk environment.

COMMODITIES

- Crude futures kept afloat after gaining yesterday as strikes continued across the Middle East in the ever-widening conflict, while attacks persisted overnight, and Trump said they will hit Iran hard tonight, as well as threatened to target Iranian power plants and bridges next week unless Iran comes to the negotiating table, although he abandoned plans to impose a 20% Strait of Hormuz fee.

- US Private Inventory Data (bbls): Crude -0.6mln (exp. -2.7mln), Distillates +2.3mln (exp. +1.0mln), Gasoline -1.7mln (exp. +0.6mln), Cushing +0.2mln.

- US President Trump said Iraq had tremendous oil reserves and significant wealth potential, adding that he would announce oil partnerships with Iraq this week or next. Trump also said that oil companies were now entering Iraq for partnerships, that oil firms were all going in and getting along with Iraq, and that while the US would be there for Iraq if it needed protection, Iraq did not need the US military.

- Spot gold faded post-CPI moves and continued to pull back from resistance at USD 4,100/oz.

- Copper futures were rangebound as participants digested Chinese GDP, Industrial Production and Retail Sales data.

CRYPTO

- Bitcoin retreated beneath the USD 65,000 level but with downside stemmed by an intraday bounce.

NOTABLE ASIA-PAC HEADLINES

- China's stats bureau deputy head said China's CPI and PPI are in reasonable ranges and hard won given most countries face big price increases, while the official added that China's energy supplies are sufficient, production is stable, and imports are under control. Furthermore, it was stated that the Q2 GDP growth slowdown is due mainly to short-term factors and external factors, while H1 GDP growth lays a good foundation for achieving the full-year growth target.

DATA RECAP

- Chinese GDP Growth Rate QQ (Q2) 0.9% vs. Exp. 0.9% (Prev. 1.3%, Low. 0.8%, High. 1.2%)

- Chinese GDP Growth Rate YY (Q2) 4.3% vs. Exp. 4.4% (Prev. 5%, Low. 2.7%, High. 4.8%)

- Chinese Industrial Production YY (Jun) 5.3% vs. Exp. 4.7% (Prev. 4.5%, Low. 4.3%, High. 5.5%)

- Chinese Retail Sales YY (Jun) 1.0% vs. Exp. -0.1% (Prev. -0.6%, Low. -1.2%, High. 0.7%)

- Chinese Fixed Asset Investment YTD YY (Jun) -5.7% vs. Exp. -5.0% (Prev. -4.1%, Low. -6.0%, High. -2.5%)

- Chinese Unemployment Rate (Jun) 5.0% vs. Exp. 5.1% (Prev. 5.1%)

- Chinese House Price Index YoY (Jun) Y/Y -3.3% (Prev. -3.5%)

- Japanese Machinery Orders MM (May) -12.4% vs. Exp. -4.2% (Prev. 8.7%, Low. -6.7%, High. 0.4%)

- Japanese Machinery Orders YY (May) -1.9% vs. Exp. 12.9% (Prev. 15.6%, Low. 0.6%, High. 17%)

GEOPOLITICS

RUSSIA-UKRAINE

- US President Trump, when asked on the Russia sanctions bill, said that he thinks they might add Iran and Hezbollah to it, as well as stated that secondary sanctions on China and India have not yet been discussed, but they will have to have a look.

- US Senators released the text of the updated Russia sanctions bill negotiated by President Trump and late Senator Graham, which eases tariffs that could be placed on buyers of Russian oil and gas. Tariffs for Russian oil and gas buyers would be reduced to a maximum of 100% on the top 5 purchasers, from a blanket 500%, while the bill lets Trump waive sanctions if he deems it in the US national interest to do so.

EU/UK

NOTABLE HEADLINES

- Ed Miliband's opponents in the Labour Party believe he has failed in his bid to become Chancellor, with current Home Secretary Mahmoud seen by some MPs as the favourite to take the Chancellor role in Andy Burnham's new government, according to FT.

Loading...