Europe primed for a weaker open as energy benchmarks rally - Newsquawk EU Market Open

- The US continued to launch strikes for a third night, after President Trump stated that he would hit Iran “very hard” on Monday and Tuesday. Separately, Trump threatened to hit Iran’s “Pickaxe Mountain”, an underground nuclear facility; Brent Aug’26 +1.9%.

- US President Trump also announced a naval blockade, which is set to begin at 21:00 BST / 16:00 EDT.

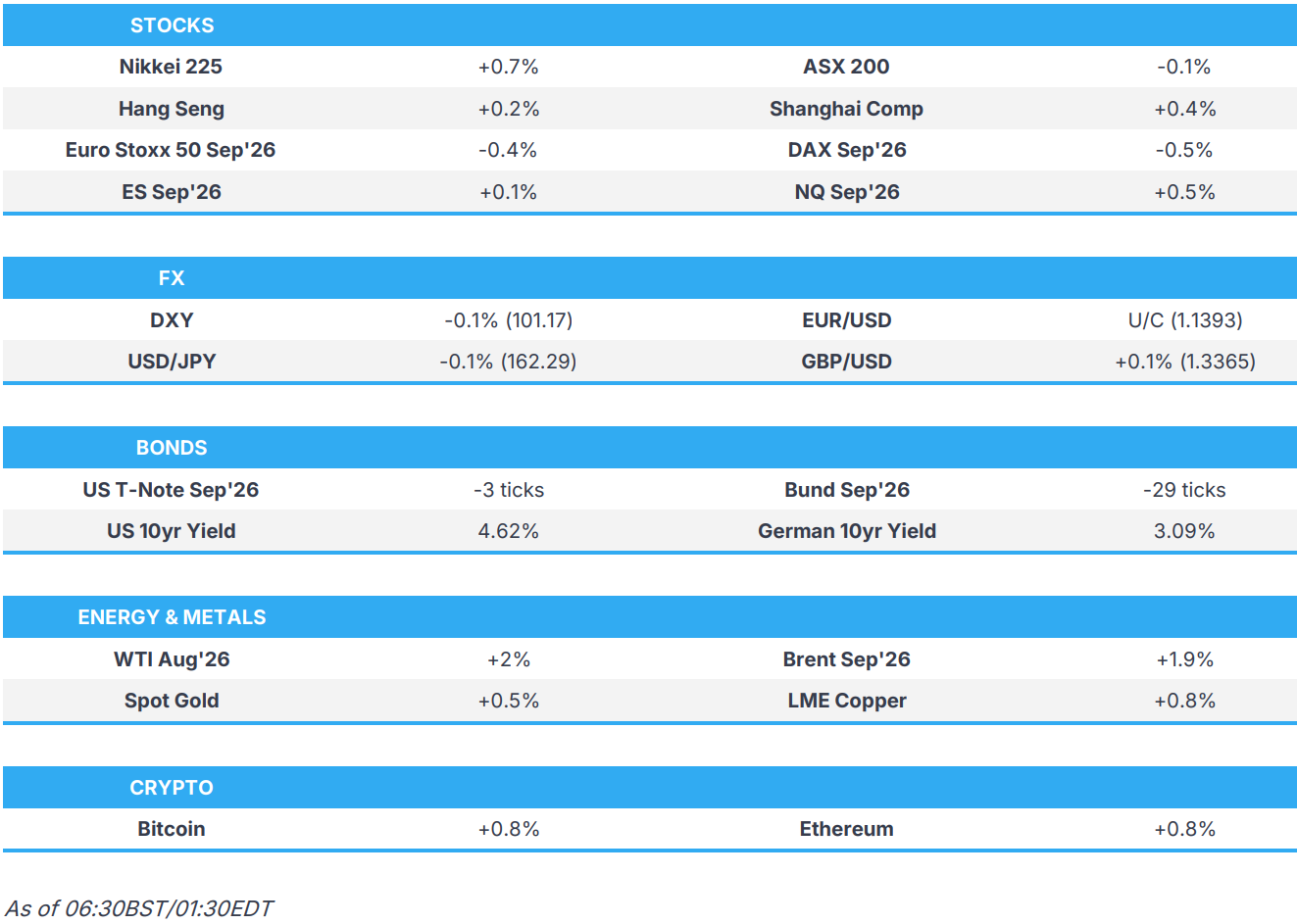

- APAC stocks were mostly in the red given the geopolitical environment and tech sell-off; European equity futures are indicative of a weaker open.

- DXY takes a breather; Kiwi outperforms following regional data and hawkish comments from RBNZ’s Conway.

- USTs and Bunds remain pressured amidst the elevated energy prices and after Fed’s Waller delivered hawkish remarks.

- Looking ahead, Highlights include German Wholesale Prices (Jun), Chinese M2 Money Supply (Jun), US NFIB Business Optimism Index (Jun), US CPI (Jun), Fed Discount Rate Minutes (Jul), ECB President Lagarde-US Treasury Secretary Bessent meeting.

- Speakers including Fed Chair Warsh, Goolsbee, Barr, Cook & Bowman, BoE Governor Bailey, Supply from the Netherlands & Germany.

- Earnings from Citi, Goldman Sachs, JPMorgan, Bank of America, Wells Fargo.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US President Trump reiterated that Iran has no air force, no navy and no military, while he said they will hit Iran very hard on Monday night and on Tuesday. Trump said they had a deal yesterday and that Iran breaks deals, as well as commented that the MoU was built to test Iran and that Iran didn't honour it. Trump also stated that they will hit 'Pickaxe Mountain' pretty soon and have their eyes on the site all the time, which is a good potential target

- US President Trump said he thinks the Iran war is going well and fast, as well as noted that they had a deal 2 days ago, but Iran turned around, while he added that they were attacking Iran on Monday night and taking out all their capabilities.

- US Central Command announced that it conducted and completed a third consecutive night of strikes against Iran, with US strikes reported in Bushehr, Bandar Abbas and Bandar Kangan, while explosions were also reported in Iran's Qeshm Island and Kish Island.

- US military has plans for several days of additional strikes in the Hormuz area and on Iran's southern coastline aimed at degrading the IRGC's ability to attack ships, according to Axios citing a US defence official, while it was reported that the US hasn't discussed the issue of possible tolls for securing the Strait of Hormuz with its allies in the region.

- US Navy-led JMIC said the US military will begin enforcement of a naval blockade of all Iranian ports and Iranian coastal areas at 20:00 GMT on 14th July, which will apply to all vessel traffic, regardless of the flag. It added that the blockade encompasses the entirety of the Iranian coastline, including but not limited to Iranian ports and oil terminals, although it will not impede neutral transit passage through the Strait of Hormuz to or from a non-Iranian destination.

- IRGC said it targeted weapons warehouses, satellite communications centre, and US forces' housing building at Bahrain's Juffair base. Iran's army also targeted US military facilities and equipment in Kuwait with drones, as well as targeted a 'hostile' US vessel with cruise missiles, while it was separately reported that a US military base in Jordan was hit by a missile attack and that a missile attack hit an Iranian Kurdish opposition group site east of Iraq's Erbil.

- Iran's Foreign Minister said whoever provides secure and safe passage of commercial vessels through Hormuz should be compensated, while he added that Iran has always been the Guardian of the Strait and will remain so forever. Furthermore, he said 20% is too much and that they will be fair.

- UKMTO received a report that a tanker was hit by an unknown projectile 40NM northeast of Qalhat, Oman, while the UAE Defence Ministry reported that two national tankers were targeted by Iranian cruise missiles in the southern Strait of Hormuz, with the incident occurring in Omani territorial waters, although the fires on both tankers were brought under control, and it reserved the right to respond to the escalation.

- Saudi Arabia conducted an assault on Yemen, while Houthis confirmed they targeted Saudi Arabia's Abha airport with ballistic missiles and warned airlines against flying over Saudi airspace.Furthermore, Houthi political bureau member Ali al-Bukhaiti said the group would target the "vital infrastructure" of Saudi Arabia in retaliation for the attack on Sanaa Airport.

- Sources reported that a Yemeni missile hit King Khalid Air Base near the Saudi city of Abha, and there were reports of an attack on Abha International Airport in southern Saudi Arabia. It was also reported that at least six missiles had been fired from Yemen towards Saudi Abha Airport, while the Saudi-led coalition said it dealt with ballistic missiles launched by Houthis towards the southern region, and sources reported the sound of an explosion in Jeddah.

US TRADE

EQUITIES

- US stocks were pressured with the Nasdaq the clear underperformer as Technology led the broader market lower, while the weakness in Tech was driven by sharp losses in memory names (DRAM -c. 9%) and semiconductor stocks (SOXX -5%) amid concerns surrounding SK Hynix's upcoming earnings, with the stock also giving back some of Friday's gains following its US listing. Broader risk sentiment was also weighed down by ongoing geopolitical tensions between the US and Iran after further military strikes over the weekend. President Trump announced that the US would reinstate the blockade on Iran and assume control of the Strait of Hormuz, adding that the US would impose a 20% charge on cargo vessels transiting the Strait in exchange for safe passage.

- SPX -0.78% at 7,517, NDX -1.88% at 29,264, DJI -0.26% at 52,499, RUT -0.78% at 2,955.

- Click here for a detailed summary.

NOTABLE HEADLINES

- Fed's Waller (voter) said that if there was another hot reading on core inflation this week, the Fed would need to consider a rate hike in the near term, while he would need to see several months of lower core inflation to feel inflation was moving in the right direction, and expressed concern about the elevated pace of core inflation. Waller said there was still a credible case for inflation to fall back to the 2% target without higher rates, but noted there was an equally plausible case that tighter policy would be needed. Waller stated he remained committed to returning inflation to the 2% target while also avoiding over-tightening policy and risking recession, while he expects a deceleration in headline inflation beginning with this week's inflation data, but said his focus would remain on core inflation. Furthermore, he had been sceptical of the Fed's dot plot for a long time and would remove the long-run estimates, not extend projections beyond 18 months and would release the dots a day after the meeting.

- US President Trump said he will be making a speech to the nation on Thursday evening at 21:00EDT/02:00BST. It was separately reported that Trump's Thursday speech is slated to address newly declassified intelligence reports that the White House asserts reveal plans by foreign nations to interfere in the 2020 election.

- US House budget committee will mark up a budget resolution on Wednesday, according to Punchbowl's Sherman.

APAC TRADE

EQUITIES

- APAC stocks were mostly in the red following the weak lead from the US, where risk sentiment was weighed on by tech selling and geopolitical escalation, while US-Iran strikes persisted for the third consecutive night and Trump announced to reinstate the naval blockade on Iran, as well as touted a 20% Hormuz shipping fee.

- ASX 200 was dragged lower by weakness in tech, industrials, consumer staples and financials, but with the downside stemmed by resilience in energy and utilities, while there was also an improvement in Westpac Consumer Sentiment.

- Nikkei 225 initially dropped below the 67,000 level amid tech weakness and higher oil prices, but then gradually nursed its losses and returned to flat territory as domestic yields softened.

- Hang Seng and Shanghai Comp conformed to the tech-related weakness and ultimately failed to benefit from the better-than-expected Chinese trade data.

- US equity futures were choppy amid cautiousness as US-Iran strikes continued and with participants awaiting the start of earnings season.

- European equity futures indicate a lower cash market open with Euro Stoxx 50 futures down 0.6% after the cash market closed flat on Monday.

FX

- DXY took a breather after gaining yesterday alongside the broad-based risk-off sentiment and hawkish comments from Fed's Waller. He stated that if there is another hot reading on core inflation this week, the Fed will need to consider a rate hike in the near term, and that they would need to see several months of lower core inflation to feel inflation is moving in the right direction. Furthermore, price action is contained overnight as participants await US CPI data and Fed Chair Warsh's testimony to Congress.

- EUR/USD attempted to recoup some lost ground, although the rebound was limited with the single currency lingering beneath the 1.1400 handle amid the lack of pertinent FX-specific drivers.

- GBP/USD bounced off the prior day's lows but lacked meaningful conviction after sliding from resistance at the 1.3400 level, while focus in the UK is on politics, with Andy Burnham to be crowned the leader of the ruling Labour party on Friday after winning 349 nominations out of 403 MPs, making it mathematically impossible for any rival to launch a challenge.

- USD/JPY slightly pulled back after advancing yesterday in tandem with rising US yields and oil prices.

- Antipodeans clawed back some of their recent losses with NZD the outperformer after the improvement in quarterly NZIER Business Confidence, while RBNZ Chief Economist Conway noted that a further reduction in monetary stimulus is likely to be required.

- PBoC set USD/CNY mid-point at 6.7990 vs exp. 6.7927 (prev. 6.7972)

FIXED INCOME

- 10yr UST futures were subdued after retreating yesterday amid rising oil prices and hawkish comments from Fed's Waller, while participants await US CPI data and Fed Chair Warsh's testimony.

- Bund futures remained pressured as higher energy prices stoked inflationary concerns, while demand was not helped by incoming data and looming supply, including a EUR 6bln Schatz issuance today, followed by EUR 3bln of Bunds tomorrow.

- 10yr JGB futures rebounded from the prior day's trough with the recovery facilitated by comments from Japan's Finance Minister Katayama, who said it is time to consider including JGBs in NISA and that if the environment surrounding asset management changes sharply, a change to GPIF's portfolio could be examined. Furthermore, she hopes to quickly establish details on steps to make JGBs more attractive, while support was also seen following a stronger 20yr auction, which resulted in a zero tail.

COMMODITIES

- Crude futures extended on gains after rallying yesterday by more than 9% owing to the US-Iran geopolitical escalation, with the US military conducting a third consecutive night of strikes against Iran. Furthermore, Trump announced to reinstate the blockade against Iran, touted a 20% Hormuz shipping fee and said they would hit Iran very hard on Monday night and Tuesday. Elsewhere, recent strikes between Saudi Arabia and Yemen also highlighted the risks of the conflict broadening across the region.

- US Strategic Petroleum Reserve crude oil stocks fell by about 3mln bbls to 316.5mln bbls last week, which was the lowest since 1983.

- Spot gold nursed some losses after briefly slipping beneath the USD 4,000/oz level amid recent dollar strength, upside in yields and higher oil prices.

- Copper futures steadily gained amid stronger-than-expected Chinese trade data.

CRYPTO

- Bitcoin marginally gained in choppy trade above the USD 62,000 level.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama suggested it is time to consider including JGBs in NISAs, and stated that if the environment surrounding asset management changes sharply, a change to GPIF's portfolio could be examined, while she hopes to quickly establish details on steps to make Japanese government bonds more attractive.

- RBNZ Chief Economist Conway said the Middle East conflict complicates monetary policy like all supply shocks, while he added that understanding how firms respond to cost shocks is crucial in maintaining low and stable inflation. Furthermore, he said that despite easing prices, the effects of the shock are expected to continue impacting the economy for some time, and that a further reduction in monetary stimulus is likely to be required.

- China Customs Vice Minister said this year's increase in China's trade has been strong and the momentum is stable.

DATA RECAP

- Chinese Balance of Trade (Jun) 125.8B vs. Exp. 121B (Prev. 105.43B)

- Chinese Exports YY (Jun) 27% vs. Exp. 18.2% (Prev. 19.4%)

- Chinese Imports YY (Jun) 36% vs. Exp. 24% (Prev. 27.4%)

- Chinese Balance of Trade (CNY)(Jun) 859B vs. Exp. 820B (Prev. 724B)

- Chinese Exports YY (CNY)(Jun) 20.8% (Prev. 13.8%)

- Chinese Imports YY (CNY)(Jun) 29.4% (Prev. 21.5%)

- Singaporean GDP Growth Rate QQ (Q2 A) 1.1% vs. Exp. 1.1% (Prev. 1.0%)

- Singaporean GDP Growth Rate YY (Q2 A) 5.7% vs. Exp. 5.3% (Prev. 6.0%)

- Australian Westpac Consumer Confidence Index (Jul) 83.9 (Prev. 80.6)

- Australian NAB Business Confidence (Jun) -5 (Prev. -14)

- Australian NAB Business Conditions (Jun) 3 (Prev. 3)

- New Zealand NZIER Business Confidence (Q2) 8% (Prev. -4%)

GEOPOLITICS

RUSSIA-UKRAINE

- Russian ballistic missiles targeted Ukraine's capital of Kyiv, with sirens and explosions heard across the Ukrainian capital, according to FT.

- Ukrainian President Zelensky noted an urgent need for defence systems, while he is requesting 100 Patriot interceptors per month and a total of 300 by winter to deter further Russian aggression.

- US President Trump will support the Russia sanctions bill, while it was separately reported that Senate Majority Leader Thune expressed hope for progress on the Russia sanctions bill.

OTHER

- US President Trump said they're looking into whether Cuba is storing Iranian drones, while he added that they will take care of it if Cuba has Iranian drones.

EU/UK

NOTABLE HEADLINES

- UK's Burnham will be crowned Labour leader on Friday as he won 349 nominations from MPs out of 403, which makes it mathematically impossible for any rival to launch a challenge.

DATA RECAP

- UK BRC Retail Sales Monitor YoY (Jun) Y/Y 1.7% vs. Exp. 2.9% (Prev. 3.4%)

Loading...