Europe set for quiet open, JPY and AUD unreactive to as-expected policy meetings; Uchida ahead - Newsquawk EU Market Open

- US President Trump said the Hormuz deal is fully signed and that the Strait of Hormuz has already partially reopened, with a complete reopening expected on Friday.

- The US claim that Lebanon is not included in the memorandum of understanding is false, reports Fars, citing sources.

- Israeli artillery shelling was reported in southern Lebanon, while it was also reported that Hezbollah fired rockets at Israeli soldiers in the region.

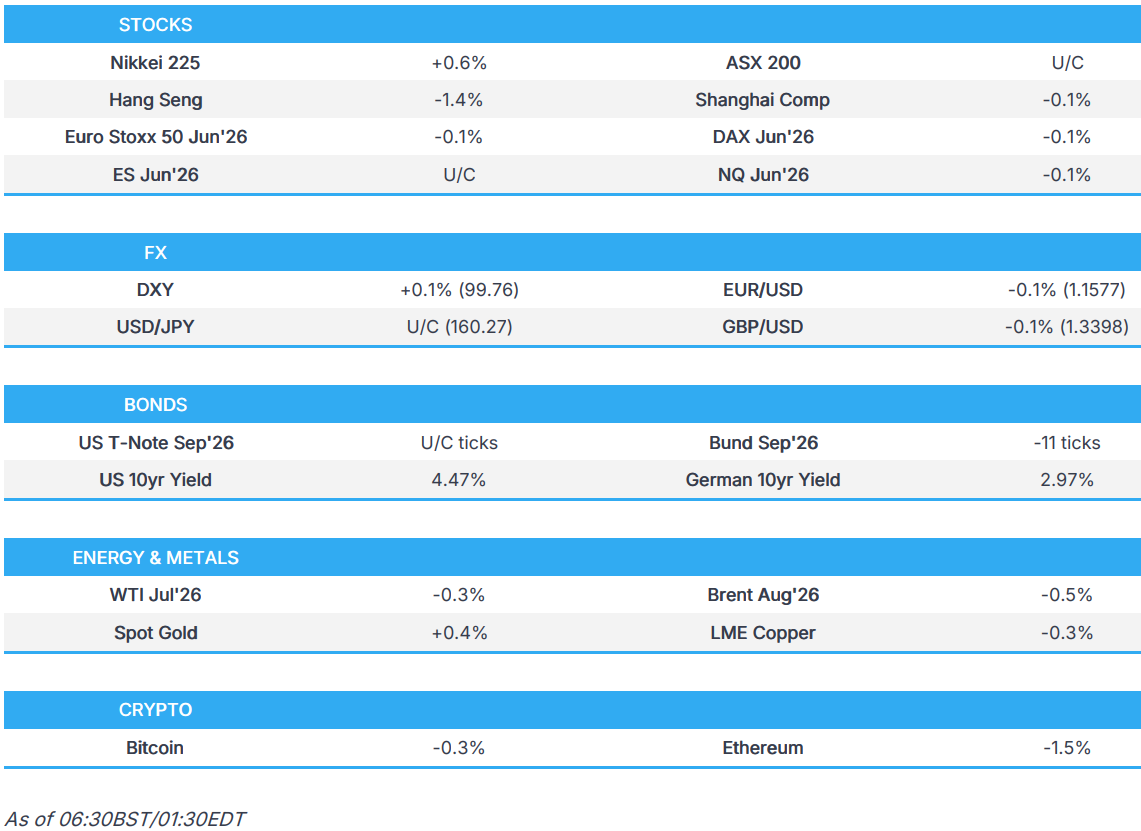

- APAC stocks were mixed, cooling from the relief rally seen on Monday; European equity futures are indicative of a slightly lower open.

- DXY is a touch firmer and trades around 99.70; JPY incrementally gains post-BoJ, which delivered a 25bps hike, as expected. The Aussie was little moved by the RBA's hawkish hold.

- Looking ahead, highlights include Italian Inflation Final (May), EU/German ZEW (Jun), US ADP Weekly, Import/Export Prices (May), Housing Starts (May), Atlanta Fed GDP (Q2), Speakers including RBA's Bullock, BoJ's Uchida & ECB's Lane, Supply from UK, Germany & US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US President Trump said the Hormuz deal is fully signed and that the Strait of Hormuz has already partially reopened, with a complete reopening expected on Friday, while he also stated that oil prices will plummet and lots of great things will happen in the Middle East. Furthermore, Trump said the text will come in the very near future and reiterated there will be no sanctions relief for Iran until it does what it is supposed to do.

- A US senior official said the US has signed the memorandum of understanding with Iran, with President Trump, Vice President Vance and Iranian Parliamentary Speaker Ghalibaf all signing the document. The official reiterated that the deal provides for the immediate opening of Hormuz and the lifting of the US blockade on Iran, while traffic through the Strait will increase significantly, although reopening will take time due to mines, and anticipated traffic volumes would rise within one to two weeks. The official also stated that a formal signing ceremony is scheduled for Friday, and details of the agreement will be released within the next 24-48 hours, while technical discussions will begin later this week.

- US President Trump posted on Truth Social "Iran has agreed to never have a Nuclear Weapon! Also, the story that the U.S. is paying Iran 300 million Dollars is Fake News, put out by the Dumocrats!!!"

- US President Trump's administration considers USD 300bln fund for Iran if deal is upheld, and incentives would be tied to Tehran's performance, including over opening up the Strait of Hormuz and nuclear talks, according to FT.

- US President Trump's close aide Bruesewitz clarified that the USD 300bln Iran reconstruction plan will only be established after Iran completely dismantles its nuclear program, ceases support for terrorist organisations and conducts significant internal reforms.

- US Vice President J.D. Vance said the memorandum of understanding between the US and Iran is a brief, one-and-a-half-page document serving as a broad framework rather than a detailed agreement, and is a very general document that requires technical talks. Vance also stated that Trump may release the US-Iran agreement before Friday and affirmed the agreement is expected to be signed on Friday.

- CIA Director Ratcliffe told US President Trump and senior administration officials that information gathered by US intelligence agencies raises serious doubts about Iran's willingness to make the concessions the US seeks in a final nuclear deal, according to Axios. Sources also stated that Trump and his team discussed intelligence gathered by US intelligence agencies, which showed the way Iranian officials were discussing the deal among themselves was inconsistent with what they were telling mediators and the US. Furthermore, Ratcliffe was not the only sceptic on Trump's senior team, as Secretary of State Rubio and Defence Secretary Hegseth expressed concerns and raised questions about the deal in internal discussions, while VP Vance and envoys Witkoff and Kushner supported it.

- Iranian President Pezeshkian said the majority of the IRGC supported the text regarding the MoU, and "What has been understood is an important step towards stopping the war and starting negotiations, and a final agreement has not yet been reached".

- IRGC Brigadier General Qaani said Bab al-Mandab is just one of the strategic points in the hands of the resistance and there are other places that will be activated if necessary, according to Fars News.

- Iranian army spokesperson said they will increase their defensive power during the agreement period with the US, and keep their readiness more than before.

- Iranian media reported that three oil tankers and two ships carrying essential Iranian goods 'passed through' the US naval blockade.

- Three explosions were reportedly heard south of Qeshm Island in the Strait of Hormuz, while Iranian state media said the blasts were possibly linked to traffic management.

- Israeli PM Netanyahu said with or without a deal, Iran will not have a nuclear weapon, while he added Israel will remain in security zones as long as needed and will continue to thwart threats in the region. Netanyahu also stated that sometimes he and US President Trump do not see eye to eye.

- Israeli PM Netanyahu and US VP Vance reportedly had a tense conversation regarding Israel's presence in Lebanon, according to Al Jazeera citing Israeli Channel 13 sources.

- An informed source said the US claim that Lebanon is not included in the memorandum of understanding is false, according to Fars News Agency.

- Israeli artillery shelling was reported in the Nabatieh district of southern Lebanon. It was separately reported that Hezbollah fired rockets and artillery at Israeli soldiers, while the Israeli military said it intercepted numerous rockets launched by Hezbollah towards troops in southern Lebanon.

US TRADE

EQUITIES

- US stocks closed firmly in the green, albeit slightly off intraday highs, as risk sentiment took its cue from the US and Iran reaching a peace agreement that is expected to be formally signed in Switzerland on Friday. While full details of the agreement have yet to be released, reports suggest the US will lift its naval blockade while Iran will reopen the Strait of Hormuz. The positive developments surrounding the US-Iran agreement drove a broad risk-on move across asset classes, while sector performance reflected the improved risk backdrop in which Technology, Communication Services, and Consumer Discretionary led the gains, while Energy was the clear laggard amid the sharp decline in oil prices, as traders removed much of the geopolitical risk premium embedded during the conflict.

- SPX +1.65% at 7,554, NDX +3.06% at 30,544, DJI +0.92% at 51,676, RUT +0.72% at 2,965.

- Click here for a detailed summary.

NOTABLE HEADLINES

- California Governor Newsom said US President Trump has directed the DoJ to investigate him.

APAC TRADE

EQUITIES

- APAC stocks traded mixed as the prior day's rally and US-Iran peace deal euphoria petered out amid a continued lack of concrete details regarding the interim agreement and as market participants turn their attention to this week's busy slate of central bank policy decisions.

- ASX 200 was led lower by weakness in tech, consumer discretionary and industrials, while participants also digested the RBA rate decision in which the central bank paused after three consecutive rate hikes, but warned of potential future hikes if necessary and remained hawkish regarding inflation.

- Hang Seng and Shanghai Comp were choppy as participants digested mixed activity data in which Industrial Production topped forecasts, but Retail Sales missed and printed in contraction territory, while the PBoC continued its increased liquidity efforts.

- US equity futures took a breather after the recent rally on Wall St, where the Nasdaq outperformed on tech strength, and the Dow printed fresh all-time intraday highs and a record close.

- European equity futures indicate a slightly lower cash market open with Euro Stoxx 50 futures down 0.1% after the cash market closed with gains of 0.7% on Monday.

FX

- DXY attempted to nurse some losses after weakening yesterday as risk sentiment was boosted by the US and Iran reaching a framework peace agreement, which is expected to be formally signed in Switzerland on Friday. The full details have yet to be released, although reports suggested the US would lift its naval blockade and Iran would reopen the Strait of Hormuz, while there were discrepancies, such as surrounding the release of funds, with US President Trump refuting reports of a potential USD 300bln reconstruction fund for Iran. Nonetheless, the focus now turns to the slew of rate decisions, including from the FOMC on Wednesday.

- EUR/USD took a breather after it recently benefited from a softer dollar, but ultimately failed to sustain the 1.1600 status despite several ECB comments yesterday, which were mostly hawkish-leaning.

- GBP/USD faded this week's initial gains and returned to flat territory amid quiet newsflow, while the calendar remained light for the UK, but will pick up from Wednesday with the release of CPI data, followed by the BoE policy meeting and the key Makerfield by-election, which are both scheduled on Thursday.

- USD/JPY continued to pull back from Monday's peak, but retained the 160.00 handle as attention turned to the BoJ policy decision, which unsurprisingly lifted rates to the highest in more than three decades, and also announced to pause the future tapering of bond purchases from FY27.

- Antipodeans retreated as the risk sentiment in Asia waned and following mixed activity data from China, which showed a contraction in Retail Sales, while attention then turned to rate decisions, including from the RBA, which stood pat after having delivered three consecutive rate hikes so far this year.

- PBoC set USD/CNY mid-point at 6.8108 vs exp. 6.7605 (prev. 6.8088).

FIXED INCOME

- 10yr UST futures paused overnight after bull steepening yesterday as the front-end outperformed on lower oil prices following the US-Iran MoU, while demand was contained ahead of a US 20yr auction due later today and with the FOMC announcement scheduled on Wednesday.

- Bund futures trickled lower amid incoming supply, including EUR 5bln in Bobls today, followed by tomorrow's EUR 2.5bln of Bund offerings, while German ZEW data also looms.

- 10yr JGB futures declined heading into the BoJ policy decision and extended on losses after the central bank hiked rates by 25bps to 1.00%, as widely expected, with rates now at their highest level since 1995.

COMMODITIES

- Crude futures were contained after tumbling yesterday on the US-Iran interim peace agreement to end the hostilities and open up the Strait of Hormuz. While the full document itself hasn't been released yet, officials have been revealing some details, but there are some discrepancies. Nonetheless, the MoU was reportedly signed virtually by US President Trump, VP Vance and Iranian Parliamentary Speaker Ghalibaf, with an official signing to take place in Switzerland on Friday.

- US Strategic Petroleum Reserve crude oil stocks fell to the lowest since 1983 at 340.3mln barrels.

- Spot gold eked slight gains in rangebound trade after Monday's intraday pullback was stemmed by support at the USD 4,300/oz level, and as the focus turns towards central bank policy announcements.

- Copper futures continued to fade recent gains as the euphoria surrounding the US-Iran agreement began to wear thin amid the lack of concrete details and with Trump refuting reports regarding a potential USD 300bln reconstruction fund for Iran, which he called fake news.

CRYPTO

- Bitcoin is marginally lower after rebounding from a brief dip beneath the USD 66,000 level.

CENTRAL BANKS

- BoJ raised its short-term interest rates by 25bps to 1.00%, as expected, while it announced to pause tapering of bond buys, in which it will keep the monthly pace of JGB buying at around JPY 2tln from April 2027. BoJ said it will continue to raise the policy rate in response to developments in economic activity, prices and financial conditions, while it will examine the likelihood of realising the baseline scenario as well as risks in considering the timing and pace of policy adjustment. The decision on rates was made by a 7-1 vote, as board member Asada dissented against a hike, while board member Tamura proposed tapering bond purchases by JPY 200bln per quarter from April 2027 onward, but the proposal was rejected by a majority vote. BoJ stated there is no change in the current plan to reduce monthly JGB buying by JPY 200bln yen each quarter until January-March 2027 and it is prepared to amend the bond-taper plan at future policy meetings if necessary, but will discontinue the practice of conducting an interim assessment of the bond-taper plan. Furthermore, it said it will respond nimbly, including by increasing JGB buying and conducting fixed-rate purchase operations, in the event of a rapid rise in long-term rates.

- RBA kept the Cash Rate unchanged at 4.35%, as expected and with the decision unanimous, but warned of potential further hikes if necessary, citing persistent inflation and oil supply disruptions. RBA said the latest data indicates that headline and underlying inflation remain too high, and the board will monitor incoming data and the evolving assessment of the outlook and risks to guide its decisions, while it noted short-term inflation expectations have eased but remain above levels seen earlier this year. Furthermore, it stated that monetary policy is well placed to respond to developments and the Board is focused on its mandate to deliver price stability and full employment, while it will do what it considers necessary to achieve that outcome, including increasing the cash rate target further if required.

NOTABLE ASIA-PAC HEADLINES

- China's National Bureau of Statistics spokesperson said China's economic foundation needs to be strengthened, and that the external situation is complex and volatile, while China is to strengthen counter-cyclical adjustments, and will stabilise employment and the market. NBS also stated that China is to expand domestic demand and that some companies face relatively big pressure. Furthermore, the stats bureau spokesperson said there is still ample space for China to expand investment and that stronger employment and income growth are needed to boost consumption, as well as stated that China has ample policy space, reserves and flexible tools available to ensure stable economic growth, but also acknowledged that China's foreign trade faces some pressure due to external uncertainties.

DATA RECAP

- Chinese Industrial Production YY (May) 4.5% vs. Exp. 4.2% (Prev. 4.1%)

- Chinese Retail Sales YY (May) -0.6% vs. Exp. 0% (Prev. 0.2%)

- Chinese Fixed Asset Investment YTD YY (May) -4.1% vs. Exp. -2% (Prev. -1.6%)

- Chinese Unemployment Rate (May) 5.1% vs. Exp. 5.2% (Prev. 5.2%)

- Chinese House Price Index YY (May) -3.5% (Prev. -3.5%)

GEOPOLITICS

RUSSIA-UKRAINE

- UK is to announce new Russian shadow fleet sanctions on Tuesday, with the UK to target Russian LNG vessels and finance networks.

EU/UK

NOTABLE HEADLINES

- EU officials are drafting a blueprint to manage banking crisis liquidity, according to POLITICO.

Loading...