European equities futures point to a positive open as ASML reports record orders - Newsquawk EU Market Open

- APAC stocks traded mixed with an early positive bias seen following the mostly constructive handover from Wall Street, although some cautiousness began to seep through ahead of looming key risk events.

- China is said to have approved the first batch of NVIDIA's (NVDA) H200 AI chips for import, with sources noting that China has granted approval for the import of several hundred thousand H200 AI chips, later reported to be over 400,000.

- ANZ shifted its RBA call, in which it now sees a 25bps hike at next week's RBA meeting following the mostly hotter Australian CPI report overnight.

- European equity futures indicate a firmer cash market open with Euro Stoxx 50 +0.6% following earnings from ASML. Euro Stoxx 50 cash finished with gains of 0.6% on Tuesday.

- Looking ahead, highlights include New Zealand Trade (Dec), Fed Policy Announcement, BoC Policy Announcement, BCB Policy Announcement. Speakers include ECB's Elderson & Schnabel, BoC's Macklem, Fed Chair Powell. Supply from Germany & US. Earnings from Microsoft, Meta, Tesla, Lam, ServiceNow, IBM, GE Vernova, AT&T, Starbucks, VF Corp, Danaher & AS.

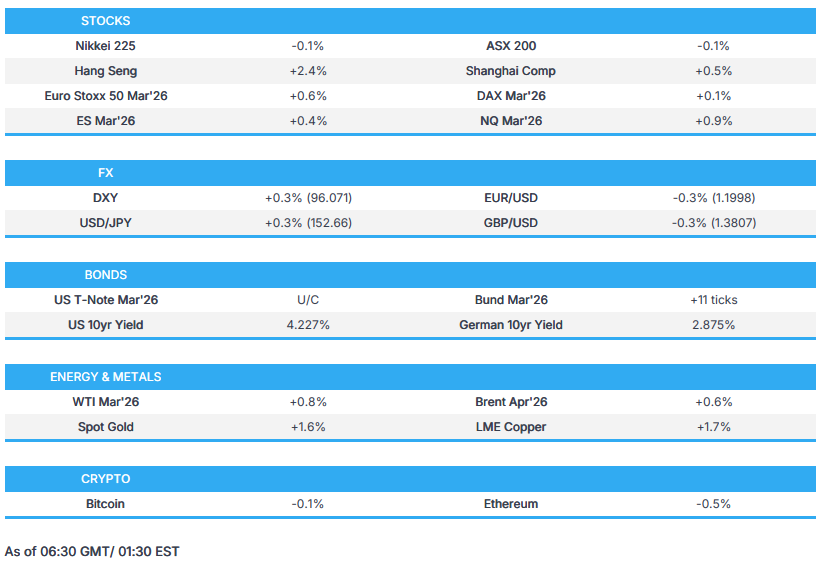

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks closed firmer, driven largely by mega-cap names as markets look towards MSFT, TSLA, and META earnings on Wednesday after the FOMC. Unsurprisingly, Healthcare was the worst performer, weighed by broad weakness in insurers (UNH -19.6%, CVS -14.2%, HUM -21.1%) after a WSJ report late on Monday that the Trump administration is proposing to keep the rates steady that Medicare pays insurers, lower than the Street's expectations of 5%.

- Financials also saw losses while Tech, Utilities, and Energy outperformed. The latter was supported by upside in crude prices as the winter storm in the US continues to curtail production, with analysts noting that US oil producers lost up to 15% of national production over the weekend. US data largely had little impact on FX, but did add to downside in US 2yr yields as US Consumer Confidence hit a 12-year low; Richmond Fed showed slight improvement, albeit still negative, while ADP weekly employment growth marginally eased.

- SPX +0.41% at 6,979, NDX +0.88% at 25,940, DJI -0.83% at 49,003, RUT +0.26% at 2,667.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said we will find a solution together with South Korea when asked about his announcement of raising tariffs against Korea, while he separately commented that they are making a lot of good deals.

- US President Trump’s admin is warning South Korea not to target tech companies with discriminatory regulations and investigations, while many discussions involve Coupang (CPNG), according to WSJ.

- USTR Greer said Chinese EVs won't enter the US from Canada without heavy levies, according to Fox Business. Greer also criticised South Korean digital services legislation, and stated the US is still imposing a 50% tariff rate on Indian goods, as well as noted that India has made a lot of progress weaning off Russian oil.

- China is said to have approved the first batch of NVIDIA's (NVDA) H200 AI chips for import, with sources noting that China has granted approval for the import of several hundred thousand H200 AI chips.

- China has reportedly approved imports of over 400,000 NVIDIA (NVDA) H200 chips, according to sources.

- EU Commission official said Shein could face an EU investigation regarding the sale of illegal products on its platform, but is unlikely to be hit with an order to suspend its website.

NOTABLE HEADLINES

- US President Trump said under his leadership, economic growth is exploding to numbers not seen before, while he reiterated that he wants interest rates to go down and affirmed that he will announce his Fed chair pick soon.

- US President Trump said he doesn't think the dollar declined too much and noted that the dollar is doing great and the value of the dollar is great, while he stated that China and Japan always want to devalue their currencies. Trump also said the dollar is seeking its own level, which is fair and he can have it up or down like a yo-yo.

APAC TRADE

EQUITIES

- APAC stocks traded mixed with an early positive bias seen following the mostly constructive handover from Wall Street, although some cautiousness began to seep through ahead of looming key risk events.

- ASX 200 was subdued with the index dragged lower by weakness in tech and consumer stocks, while the predominantly firmer-than-expected inflation data from Australia supports the case for a hike at next week's RBA meeting.

- Nikkei 225 underperformed from the open, following the recent currency strength spurred by intervention speculation and US President Trump's FX-related rhetoric.

- Hang Seng and Shanghai Comp were in the green with energy and telecom stocks among the index leaders in Hong Kong, while the mainland was kept afloat after developer China Vanke won creditor approval to extend another two CNY bonds and with a report noting that China approved the first batch of NVIDIA's H200 AI chips for import involving several hundred thousand H200 AI chips.

- US equity futures mostly extended on gains but with the upside capped as the FOMC and Mag 7 earnings loom.

- European equity futures indicate a firmer cash market open with Euro Stoxx 50 +0.6% following earnings from ASML. Euro Stoxx 50 cash finished with gains of 0.6% on Tuesday.

FX

- DXY nursed some of the prior day's losses after suffering from the ongoing de-dollarisation theme, and with the greenback not helped by weak US Consumer Confidence, while selling pressure was exacerbated late on Tuesday after President Trump said he doesn't think the dollar declined too much and that he can have it up or down like a yo-yo. The attention now turns to the conclusion of the FOMC meeting later, where the Fed is expected to pause on rates.

- EUR/USD pared some of its spoils after having benefitted yesterday from the dollar's demise, which saw the single currency briefly reclaim the 1.2000 status, while several recent ECB comments did little to shift the dial.

- GBP/USD pulled back after climbing to its highest level in more than four years and failed to sustain a brief return to the 1.3800 territory, with very light newsflow from the UK.

- USD/JPY rebounded from a 3-month low after slumping on intervention speculation and rhetoric from US President Trump, who doesn't think the dollar declined too much and said China and Japan always want to devalue their currencies.

- Antipodeans mildly softened as the dollar regained poise and with only brief support seen in AUD/USD following Australian CPI data in which the monthly reading for December printed firmer-than-expected, while the headline quarterly figures matched estimates, although the quarterly RBA-preferred Trimmed Mean Inflation topped forecasts and remained above the RBA's 2%-3% inflation goal. This prompted ANZ to shift its RBA call, in which it now sees a 25bps hike at next week's RBA meeting and views this as a single insurance tightening and not the start of a series of hikes.

- PBoC set USD/CNY mid-point at 6.9755 vs exp. 6.9231 (Prev. 6.9858)

FIXED INCOME

- 10yr UST futures were choppy following US-South Korea tariff frictions, weak US Consumer Confidence and an average 5-year auction stateside, while the attention turns to FOMC, where the Fed is widely expected to stand pat.

- Bund futures struggled for direction after yesterday's choppy performance, while GfK data and Bund supply loom.

- 10yr JGB futures climbed amid a softer yield environment in Japan with risk appetite sapped by a firmer currency, while stale minutes from the BoJ's December meeting provided very little to shift the dial in which members reiterated that it is appropriate to keep raising rates if the outlook is met, although prices were briefly supported in the aftermath of the latest 40yr JGB offering which resulted in a slightly higher-than-previous coverage ratio.

COMMODITIES

- Crude futures remained elevated after rallying throughout the prior session despite the absence of any major energy-specific catalysts, although the moves had coincided with recent dollar selling and weather-related output disruptions, while the latest weekly private sector inventory data was mixed and had little impact on price action.

- US Weekly Private Inventory Data (bbls): Crude -0.2mln (exp. +1.8mln), Distillate +2.0mln (exp. -0.6mln), Gasoline -0.4mln (exp. +1.0mln), Cushing -0.0mln.

- US is reportedly to issue a general license soon lifting some sanctions on the Venezuelan oil industry.

- Spot gold extended on record highs and climbed above the USD 5,200/oz level for the first time, with recent dollar pressure and uncertainty, supporting demand for the precious metal.

- Copper futures rallied alongside the mostly constructive mood, but with further upside capped ahead of looming key events and with resistance at the USD 6.00/lb level.

- Citadel is moving into industrial metals, shifting its stance after years of avoiding the sector as prices from copper to tin hit record highs, Bloomberg reported citing sources. The hedge fund hired Ylan Adler as a portfolio manager with a cross-commodities mandate, of which metals will be a key part, according to sources.

CRYPTO

- Bitcoin was lacklustre and eventually trickled lower to below the USD 89,000 level.

NOTABLE ASIA-PAC HEADLINES

- BoJ Minutes from the December 18th-19th Meeting noted that members said it is appropriate to keep raising rates if the outlook is met, while most members said BoJ should not have a preset idea on rate hike pace and must scrutinise the economy, prices and markets in making decisions at each meeting. A few members said adjusting the degree of monetary support would help stabilise markets and have merits to the economy, while a member said waiting for another meeting to raise rates would be risky given the impact of FX on inflation, and a member also warned that divergence of real rates from equilibrium may impair long-term economic growth.

- UK PM Starmer delayed the decision on a Chinese-built wind farm factory after security fears.

DATA RECAP

- Australian CPI YY (Dec) 3.8% vs. Exp. 3.6% (Prev. 3.4%)

- Australian Trimmed Mean CPI YY (Dec) 3.3% vs. Exp. 3.3% (Prev. 3.2%)

- Australian CPI QQ (Q4) 0.6% vs Exp. 0.6% (Prev. 1.3%)

- Australian CPI YY (Q4) 3.6% vs Exp. 3.6% (Prev. 3.2%)

- Australian RBA Trimmed Mean CPI QQ (Q4) 0.9% vs. Exp. 0.8% (Prev. 1.0%)

- Australian RBA Trimmed Mean CPI YY (Q4) 3.4% vs. Exp. 3.3% (Prev. 3.0%)

- Australian RBA Weighted Median CPI QQ (Q4) 0.9% vs. Exp. 0.8% (Prev. 1.0%)

- Australian RBA Weighted Median CPI YY (Q4) 3.2% vs. Exp. 3.1% (Prev. 2.8%)

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu said if Iran attacks them, it will respond with a force it has never seen before. It was separately reported that the Israeli military said it identified "suspected infiltration" into Israel from Jordan.

- IRGC said Iran will treat neighbours as hostile if their territory is used to launch an attack.

- US President Trump said he is hearing that Iraq might make a very bad choice by reinstalling Nouri al-Maliki as Prime Minister, while he added that it should not be allowed to happen again and if elected, the US will no longer help Iraq.

RUSSIA-UKRAINE

- US President Trump said very good things are happening on Ukraine and Russia.

OTHERS

- North Korea said it had tested a large calibre multiple rocket launch system, according to KCNA.

EU/UK

NOTABLE HEADLINES

- ECB's Nagel said there is no reason to change rates anytime soon, and he agrees with Chief Economist Lane that there is no good argument for changing rates in either direction.

- ECB's Kocher said officials must be ready to act if needed. It was separately reported that ECB's Kocher said the central bank would need to act if the euro keeps gaining, according to FT.

- Dutch political party leaders reached an agreement on forming a minority government.

- French government survived no-confidence votes in parliament.

NOTABLE EUROPEAN EQUITY NEWS

- ASML (ASML NA) - Q4 2025 (EUR): Sales 9.72bln (exp. 9.26bln, guided 9.2-9.8bln), Orders 13.2bln (exp. 6.95bln), guides Q1 2026 Revenue 8.2-8.9bln (exp. 8.11bln), guides FY26 sales 34-39bln (exp. 36.5bln); Announces up to EUR 12bln share buyback. CEO: "many of our customers have shared a notably more positive assessment of the medium-term market situation, primarily based on more robust expectations of the sustainability of AI-related demand."

- LVMH (MC FP) - Q4 2025 (EUR): Revenue 22.7bln (exp. 22.6bln), Organic growth +1% (exp. -0.3%); FY revenue 80.81bln (exp. 80.65bln), Profit from recurring operations 17.76bln (exp. 17.15bln), Net profit 10.88bln (exp. 10.55bln). Q4 fashion & leather organic sales -3% (exp. -2.94%) Q4 wines & spirits revenue -9% (exp. -1.1%). Q4 sales -2% in Europe, +1% in US, and +1% in Asia. Will propose dividend of EUR 13 (exp. EUR 12.04).

Loading...