European equity futures point to a positive open despite weakness in APAC equities; Trump leaning towards Warsh or Hassett for Fed Chair - Newsquawk EU Market Open

- APAC stocks were mostly pressured at the start of a risk-packed week and following on from the tech-led declines stateside amid a rotation out of AI, while participants digested economic releases, including the BoJ Tankan and Chinese activity data.

- The BoJ Tankan survey showed sentiment of Large Manufacturers was at the highest in four years, which supports the case for a rate hike.

- Hang Seng and Shanghai Comp were subdued after the latest Chinese activity data disappointed, and house prices continued to contract, with tech and biotech leading the declines in Hong Kong.

- US President Trump said on Friday that he is leaning towards Kevin Warsh or Kevin Hassett to lead the Fed and that the next Fed Chair should consult with him on interest rates.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.4% after the cash market closed with losses of 0.6% on Friday.

- Looking ahead, highlights include German Wholesale Price Index, EZ Industrial Production (Oct), Canadian CPI (Nov), US Advance Goods Trade Balance (Sep), and Australian PMI (Dec). Speakers include Fed’s Miran, Williams, & RBA’s Jones.

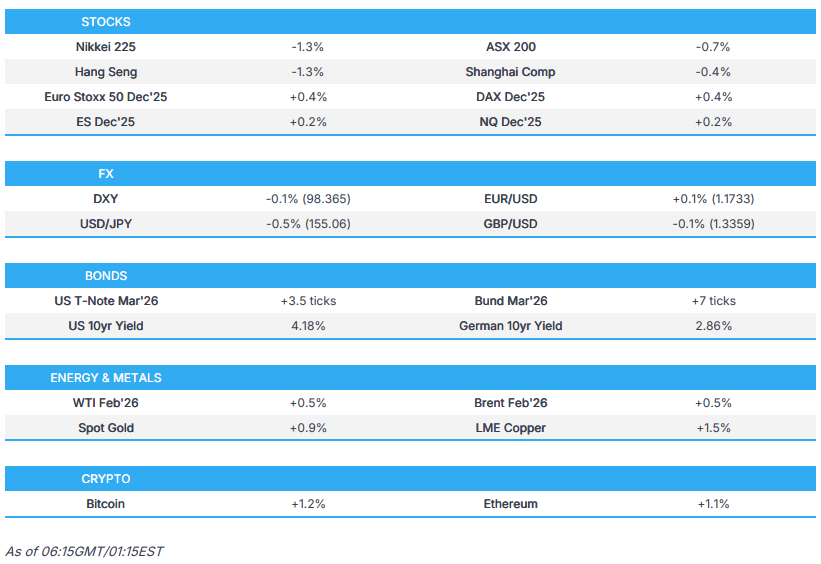

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks were sold on Friday with underperformance in the Nasdaq as Broadcom's (AVGO, -11.4%) Q4 earnings showed its AI order backlog fell short of expectations, adding to the AI concerns seen post-Oracle (ORCL, -4.6%) earnings. Oracle shares also declined after reports that data centres for OpenAI are reportedly delayed to 2028 from 2027; largely due to labour and material shortages, although Oracle denied the reports, which helped its shares pare some of the downside. Meanwhile, sectors were predominantly lower, with Tech slumping 3%, while energy and communication also lagged, albeit to a lesser extent.

- SPX -1.07% at 6,827, NDX -1.91% at 25,197, DJI -0.51% at 48,458, RUT -1.51% at 2,551.

- Click here for a detailed summary.

TARIFFS/TRADE

- US and Mexico reportedly struck a deal on Friday to settle the Rio Grande water dispute, which eases the bilateral tensions which had been stoked after US President Trump’s threat of an additional 5% tariff on Mexico if it did not provide additional water to help US farmers.

- White House crypto czar Sacks said on Friday that he sees China not accepting NVIDIA's (NVDA) H200 chip and that China wants to be semiconductor independent.

- China’s Central Financial and Economic Affairs Commission Deputy Director said they will expand exports and increase imports in 2026.

- EU plans a crackdown on very dangerous Chinese products sold on online platforms, including Alibaba (9988 HK) and Shein, according to FT.

- France said conditions for an EU vote on a Mercosur deal are not yet met, despite recent progress, while France calls for the EU-Mercosur December meeting to be pushed back to continue work on mirror clauses.

NOTABLE HEADLINES

- US President Trump is reportedly not certain his economic policies will translate to midterm wins, while he said his US investments haven’t fully taken effect and stated that by the time they have to talk about the election, which is in another few months, he thinks their prices are in good shape.

- US President Trump said on Friday that he is leaning towards Kevin Warsh or Kevin Hassett to lead the Fed and that the next Fed Chair should consult with him on interest rates. Trump added it is not typically done anymore, but used to be done routinely and should be done, while he stated interest rates should be 1% or lower a year from now, according to WSJ.

- White House economic adviser Hassett said he would consider US President Trump’s policy opinions, but added that the central bank would remain independent if he were to become the next Fed chair.

- Fed's Daly (2027 voter) said on Friday that she favoured a cut at last week's Fed meeting and that the FOMC decision was not an easy choice, while she added that goals are in conflict as inflation is above target and the labour market is softening. Furthermore, she said Congress gave them two goals, and their job is to meet both of them, and the recent policy decision puts them in a good place to achieve that.

- Apollo Management took bets against technology companies vulnerable to AI, in which it is betting against several large loans to software makers and cutting exposure to the sector, according to FT.

APAC TRADE

EQUITIES

- APAC stocks were mostly pressured at the start of a risk-packed week and following on from the tech-led declines stateside amid a rotation out of AI, while participants digested economic releases, including the BoJ Tankan and Chinese activity data.

- ASX 200 retreated with the declines led by mining, materials, resources and tech sectors, with the mood in Australia also sombre following a terror attack on Bondi Beach targeting a Jewish celebration.

- Nikkei 225 underperformed ahead of a widely anticipated BoJ rate hike later this week, while the quarterly BoJ Tankan survey showed sentiment of Large Manufacturers was at the highest in four years, which supports the case for a rate hike.

- Hang Seng and Shanghai Comp were subdued after the latest Chinese activity data disappointed and house prices continued to contract, with tech and biotech leading the declines in Hong Kong, while losses in the mainland were contained after reports that China is to issue ultra-long-term special government bonds in 2026 to fund major national strategies and security initiatives, as well as large-scale equipment upgrades and consumer goods trade-in programs.

- US equity futures nursed some of Friday's losses, but with the recovery contained ahead of this week's main risk events.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.4% after the cash market closed with losses of 0.6% on Friday.

FX

- DXY was little changed to start the week with price action contained to within a narrow range amid light weekend catalysts and as participants await tomorrow's Non-Farm Payrolls data, while there were comments last Friday from US President Trump who said he is leaning towards Kevin Warsh or Kevin Hassett to lead the Fed, as well as noted that the next Fed Chair should consult with him on interest rates, and that interest rates should be 1% or lower a year from now.

- EUR/USD traded sideways amid quiet newsflow from the bloc and with Eurozone Industrial Production due later.

- GBP/USD struggled for direction, and with little reaction seen from the latest UK Rightmove House Price data, which continued to show contractions.

- USD/JPY trickled lower amid wide expectations for the BoJ to increase rates later in the week, while the BoJ Tankan survey showed nearly all components of the release either matched or topped estimates.

- Antipodeans were subdued following the disappointing Chinese activity data, and with NZD underperforming after comments from RBNZ Governor Breman, who said the forward path for the official cash rate published in the November monetary policy statement indicates a slight probability of another rate cut in the near term.

- PBoC set USD/CNY mid-point at 7.0656 vs exp. 7.0569 (Prev. 7.0638)

FIXED INCOME

- 10yr UST futures eked mild gains in quiet trade in the absence of pertinent drivers, while participants await comments from Fed officials Miran and Williams due later, ahead of tomorrow's NFP jobs report.

- Bund futures traded rangebound following on from last week's choppy mood and ahead of German wholesale prices.

- 10yr JGB futures were indecisive with demand hampered heading into a widely anticipated BoJ rate hike on Friday, while the latest BoJ Tankan data showed all components either matched or improved on their previous readings, which further supported the case for the BoJ to resume its policy normalisation.

COMMODITIES

- Crude futures were marginally higher but with gains capped by a lack of major energy specific catalysts and following mixed geopolitical headlines from late last week including reports of Iran seizing a foreign tanker carrying 6mln litres of smuggled diesel in the Gulf of Oman, while a lot of progress was said to have been made during talks between Ukraine and the US on peace proposals, with discussions to continue on Monday.

- Kuwait sees a fair oil price at USD 60-65/bbl under current conditions, and they had expected prices to remain at least as they were, if not better, but were surprised by the drop, according to the Kuwaiti Oil Minister. He added they are searching for a partner in a petrochemical project in Oman’s Duqm, but are ready to move ahead with Oman if no investor is found.

- Egypt proposed a unified Arab emergency oil and gas purchases mechanism, according to the Petroleum Ministry.

- Spot gold returned to above the USD 4,300/oz level amid a broad recovery in the metals complex from last Friday's trough.

- Copper futures nursed some of last week's late losses, but with the rebound contained ahead of this week's key risk events and as participants digested the latest activity data from the red metal's largest buyer, which missed expectations.

CRYPTO

- Bitcoin rebounded from Sunday's losses and returned to above the USD 89,000 level.

NOTABLE ASIA-PAC HEADLINES

- China is to issue ultra-long-term special government bonds in 2026 to fund major national strategies and security initiatives, as well as large-scale equipment upgrades and consumer goods trade-in programs.

- China stats bureau spokesperson said China’s economy stabilised and improved in November, but the impact of changes in the external environment has deepened, and the conflict between strong domestic supply and weak demand is prominent. The spokesperson also noted that some industries and firms face difficulties, while authorities will step up counter-cyclical and cross-cyclical adjustments. Furthermore, it was stated that household consumption capability and confidence need to be further improved, with efforts to be made to stabilise jobs, boost income growth, and release consumption potential.

- China Vanke’s (2202 HK) proposal for a one-year delay of repayment for a bond due December 15th was rejected by bondholders, which leaves a five-day grace period to make the CNY 2bln bond payment and avoid a potential default.

- Hong Kong’s Democratic Party voted on Sunday to dissolve amid pressure from Beijing and previous alleged threats of severe consequences, including possible arrest if they did not disband, according to The Guardian.

- BoJ is likely to begin selling its ETF holdings as soon as January, according to Bloomberg.

- RBNZ Governor Breman said the economic outlook has evolved broadly in line with expectations, and the forward path for the Official Cash Rate published in the November monetary policy statement indicates a slight probability of another rate cut in the near term. However, she added that if economic conditions evolve as expected, the official cash rate is likely to remain at its current level of 2.25% for some time. Breman also commented that there continues to be signs that growth is recovering and financial market conditions have tightened since the November decision, beyond what is implied by the central projection for the OCR.

DATA RECAP

- Chinese Industrial Output YY (Nov) 4.8% vs. Exp. 5.0% (Prev. 4.9%)

- Chinese Retail Sales YY (Nov) 1.3% vs. Exp. 2.8% (Prev. 2.9%)

- Chinese Urban Investment (YTD)YY (Nov) -2.6% vs. Exp. -2.3% (Prev. -1.7%)

- Chinese Unemployment Rate Urban Area (Nov) 5.10% (Prev. 5.10%)

- Chinese China House Prices MM (Nov) -0.40% (Prev. -0.50%)

- Chinese China House Prices YY (Nov) -2.4% (Prev. -2.2%)

- Japanese Tankan Large Manufacturing Index (Q4) 15.0 vs. Exp. 15.0 (Prev. 14.0)

- Japanese Tankan Large Manufacturing Outlook (Q4) 15.0 vs. Exp. 13.0 (Prev. 12.0)

- Japanese Tankan Large Non-Manufacturing Index (Q4) 34.0 vs. Exp. 35.0 (Prev. 34.0)

- Japanese Tankan Large Non-Manufacturing Outlook DI (Q4) 28.0 vs. Exp. 28.0 (Prev. 28.0)

- Japanese Tankan Large All Industry Capex Estimate (Q4) 12.6% vs. Exp. 12.0% (Prev. 12.5%)

GEOPOLITICS

MIDDLE EAST

- Israel’s military conducted a strike on Gaza, which killed senior Hamas commander Raed Saed, while the Israeli military said it put a planned strike on a southern Lebanon site on hold after the Lebanese Army requested access.

- Two US Army soldiers and a civilian US interpreter were killed in Syria, while the Syrian government said the attacker was a member of Syrian security forces with extremist views. It was later reported that US President Trump said they will retaliate against ISIS and that there will be a lot of damage done to the people who attacked the troops in Syria.

- US CENTCOM will host a Doha conference on 16th December with partner nations to plan the international stabilisation force for Gaza, according to US officials.

- US forces raided a ship and seized cargo headed to Iran from China, according to WSJ.

- Iran was reported on Friday to have seized a foreign tanker carrying 6mln litres of smuggled diesel in the Gulf of Oman, according to state media.

RUSSIA-UKRAINE

- US President Trump said a lot of progress is being made on Russia and Ukraine, while he responded that they don’t want it now, and it would be complex when asked about the idea of a free economic zone in the Donbas region.

- Ukrainian President Zelensky said services have been working to restore electricity, heating and water supply to regions following Russian strikes on energy infrastructure. Zelensky also commented that there won’t be a peace plan that everyone will like and there will be compromises, while he also stated that US and European security guarantees, instead of NATO membership, are a compromise from Ukraine’s side and that security guarantees should be legally binding.

- Ukrainian presidential adviser said Ukraine and US teams meeting on peace proposals in Berlin lasted more than five hours on Sunday and will continue on Monday, while US special envoy Witkoff said a lot of progress was made during the talks.

- Ukrainian military said it struck a Russian oil refinery in the Krasnodar region and a Russian oil depot in the Volgograd region, while Ukraine’s Navy said a Russian drone attack hit a Turkish civilian vessel carrying sunflower oil to Egypt on Saturday.

- Russian Defence Ministry said Russian forces captured Varvarivka in Ukraine’s Zaporizhzhia region, according to RIA.

OTHER

- US envoy John Coale said Belarusian President Lukashenko agreed to do all he can to stop weather balloons flying into Lithuania, while Coale also stated that the US will remove sanctions on Belarusian potash and that around 1,000 remaining political prisoners in Belarus could be released in the coming months.

- US President Trump said land strikes against Venezuela will start happening and don’t necessarily have to be in Venezuela.

- US President Trump said on Friday that he had a very good conversation with the Thai and Cambodian PMs, while he added that they agreed to cease all shooting effective that evening and go back to the original peace accord. However, it was reported over the weekend that Thailand’s PM Charnvirakul said his country has not reached a ceasefire agreement with Cambodia and the Thai military will continue fighting on the disputed border.

- Philippine Coast Guard said three Filipino fishermen were wounded and two fishing boats suffered significant damage from high-pressure water cannon blasts by Chinese Coast Guard ships in the South China Sea, while it called on China’s Coast Guard to adhere to internationally recognised standards of conduct.

- China sanctioned the former chief of staff of the Japan Self-Defense Forces, in which it froze properties, prohibiting transactions with, and barring visas for former Japanese official Iwasaki.

GLOBAL NEWS

- At least 16 people were killed, and 40 were injured in a targeted, mass shooting terror attack against a Jewish celebration of Hanukkah held at Bondi Beach in Sydney on Sunday, while it was reported that Israeli PM Netanyahu said he warned Australia about anti-Semitism and told Australia's PM that anti-Semitism spreads when leaders stay silent.

EU/UK

DATA RECAP

- UK Rightmove House Prices MM (Nov) -1.8% (Prev. -1.8%)

- UK Rightmove House Prices YY (Nov) -0.6% (Prev. -0.5%)

Loading...