Global equities digest mixed reporting over US-Iran talks, oil firmer amid uncertainty - Newsquawk US Market Open

- Iranian Foreign Minister Araghchi is said to have secretly informed US Envoy Witkoff of Iranian Supreme Leader Mojtaba Khamenei’s agreement to negotiate, Al Arabiya reports citing Israeli press citing sources.

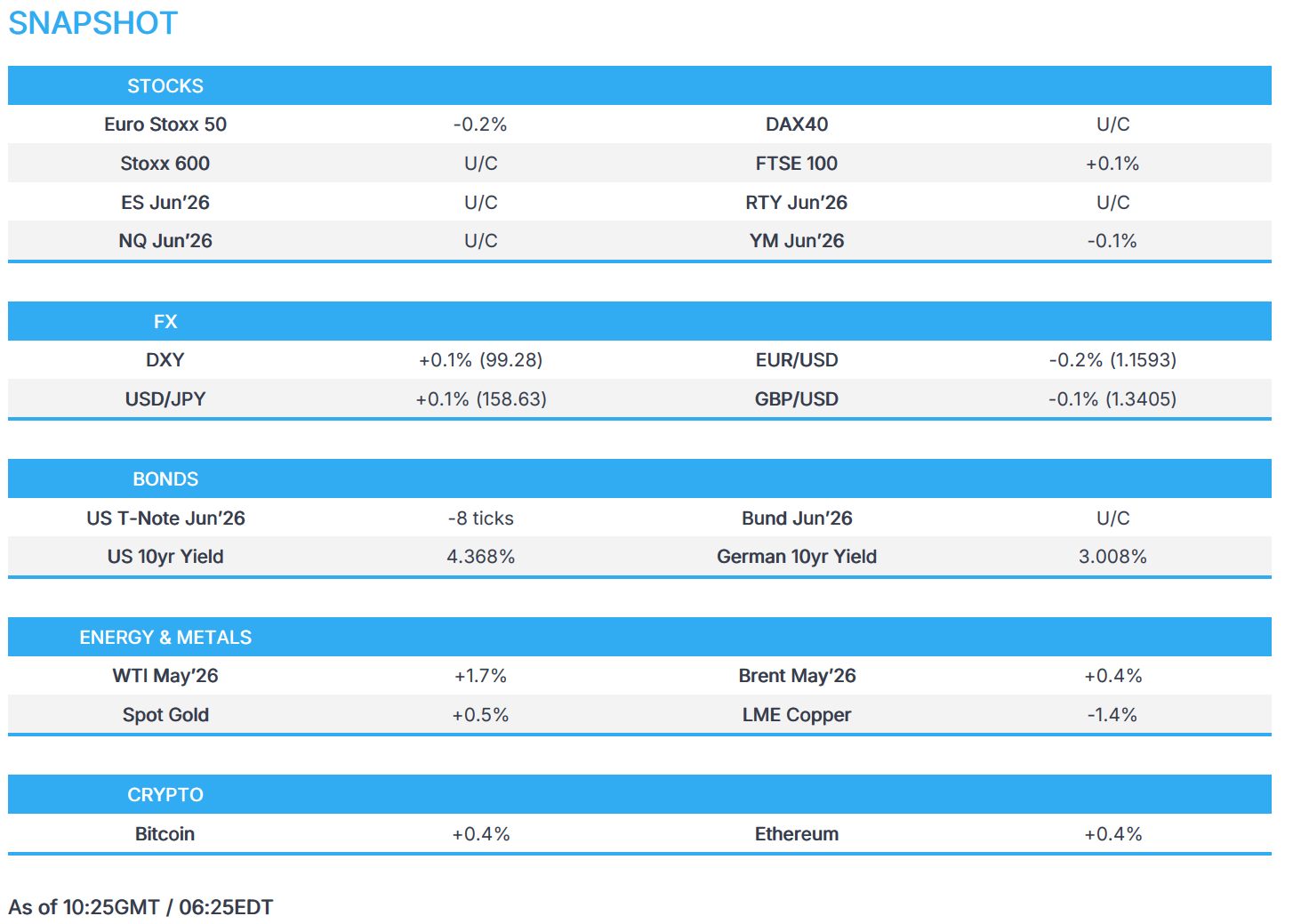

- European equities subdued while PUIG SM surges on EL merger; US equity futures pull back from Monday's highs.

- DXY finds its footing following recent losses, Antipodeans lag, EUR digests PMIs which indicate slowing growth.

- Fixed income mixed ahead of a busy speaker slate.

- Firmer trade across oil as markets digest conflicting reports while attacks continue.

- Looking ahead, highlights include US Flash PMIs (Mar), ADP Employment Change Weekly. Speakers include ECB's Sleijpen, Cipollone, Lane & Nagel, BoE's Pill, SNB's Schlegel & Tschudin, Fed's Barr. Supply from Germany & US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 U/C) trade mixed, with the AEX outperforming its peers while the FTSE MIB lags. The market reaction to the Flash PMIs were muted. However, the commentary within the PMIs gave the first glimpse at the effects of the Iranian war on businesses sentiment and the economy. The EZ release suggested the "eurozone GDP growth slowing to a quarterly rate of just below 0.1% in March with the forward-looking indicators pointing to a heightened risk of a downturn the coming months".

- European sectors show a positive bias. Energy tops the sector pile, closely followed by Chemicals following broker upgrades for BASF and Brenntag. At the bottom of the pile lies Banks and Basic Resources. In the Luxury space, Puig (+14%) soars after Estee Lauder confirmed it is in talks with the Spanish company, regarding a potential merger.

- US equity futures (ES/NQ/RTY U/C) are muted after a volatile start of the week. Despite the positive announcement of US-Iran talks by President Trump, the VIX still remains at elevated levels above its longer-term average, while the 20-, 200-SMA bearish cross for the NQ has been formed and the ES failed to convincingly close above 6,635 on Monday.

- Xiaomi (1810 HK) Q4 (CNY): Revenue 116.92bln (exp. 116.3bln). Adj. Net 6.35bln (exp. 5.78bln). In 2025, global smartphones reached 165.2mln units, smartphone revenue 186.4bln.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is firmer this morning and currently holds at the upper end of a 99.09-99.39 range. Action which appears to be a slight bounce back from the pressure seen in the prior session after US President Trump announced a five-day postponement to military strikes on Iranian power plants. Since, Iran has reportedly denied the notion that talks took place, whilst Israeli press suggested that Iranian Foreign Araghchi informed US envoy Witkoff that Mojtaba Khamenei agreed to negotiations. Markets will await more clarity on the matter in the near term, which may cap the index below recent highs (100.54). Geopols aside, focus later on will be on the weekly ADP jobs stats (last week, the series reported an average of +9k/week over the four-week window) and also Flash PMIs.

- G10s are entirely losing against the USD, with clear underperformance in the Antipodeans, which have been impacted by regional factors. For AUD/USD, the pair currently trades around 0.6955, but is still far from Monday’s trough of 0.6910; pressure which stems from weak flash PMIs. As for the Kiwi, RBNZ Governor Bremen highlighted that they would see higher inflation in the near term, which may have impacts on growth.

- Over in Europe, a number of PMI metrics have been released. In brief, Manufacturing appears to be remaining resilient whilst the Services component has deteriorated. However, markets looked to the figures for any early indications of the impact on the economy following the Iran conflict. Within the accompanying German report, analysts highlighted that “the service sector has seen an immediate negative impact”, whilst describing manufacturing resilience as a “surprise” – but potentially on “forward purchases over concerns about potential supply disruption in the coming months”. EUR/USD was ultimately little moved on these metrics, and currently trades within a 1.1575-1.1618 range, and around its 21 DMA at 1.1617.

- JPY is also a touch lower vs USD, with USD/JPY currently trading within a 158.27-158.79 range. Overnight, Japanese inflation was softer than expected, with headline Y/Y printing at 1.3% (exp. 1.5%). ING opines that the soft print will prove temporary and will not alter the BoJ’s rate hike cycle.

- Finally, the UK’s PMI metrics also indicated resilience in Manufacturing, whilst Services were weaker than expected. The accompanying release highlighted that “the war in the Middle East has hit the UK economy in March, stalling growth while driving inflation sharply higher”. Cable saw some fleeting pressure on the report itself, but this was ultimately short-lived; currently trading around its 200 DMA at 1.3434.

FIXED INCOME

- A bearish start to the day has given way to a slightly mixed session as the morning progresses and broader market benchmarks move.

- USTs in the red, lower by just under 10 ticks as it stands, but a few ticks off worst levels. Specifics for the space have been a little light in the early hours, with the market focused primarily on geopolitics and reporting around the Iranian Supreme Leader; see Commodities for a full breakdown.

- As it stands, USTs in 110-16 to 110-29 confines, awaiting Flash PMIs for timely insight into how the Middle East situation is impacting the US economy; a point that may be of note as domestic focus turns increasingly to the midterms. Elsewhere, the docket features 2yr supply.

- Bunds are now nearly unchanged. Started the day lower by 21 ticks, hitting a 125.24 trough as yesterday's move retraced. Thereafter, the benchmarks lifted in the mid-morning alongside a modest bounce in peers. More recently, a bout of fresh pressure has been seen on Flash PMIs that point to a stagflation environment for the bloc, and one where price pressures are already evident.

- Gilts started on the front foot, got to an 88.17 high early doors, as while the benchmark hadn't fully acknowledged the bearishness in fixed seen late-US/early-APAC, the narrative had by the open reverted back to one of modest fixed upside as the energy space came under pressure once again. More recently, Flash PMIs for the UK also point to stagflation, as inflationary pressure "surged" while growth has "stalled". A dynamic that underscores the difficult balancing act the BoE has at the moment, given a desire to avoid a return to price upside, but the already precarious labour and growth narrative factor against tightening.

- UK sells GBP 2.25bln 4.75% 2035 Treasury Gilt: b/c 3.50x (prev. 3.63x), average yield 4.911% (prev. 4.585%), tail 0.2bps (prev. 0.2bps).

- Japan sold JPY 400bln in 40-year JGBs; b/c 2.54x (prev. 2.76x), highest accepted yield 3.600% (prev. 3.720%). Price at the highest accepted yield 89.57 (prev. 87.27).

- Australia sold AUD 1bln 3.75% April 2037 bonds, b/c 3.67, avg. yield 5.0650%.

COMMODITIES

- WTI and Brent futures are trimming some of the prior day's heavy losses that were triggered by US President Trump's announcement to postpone military strikes against Iranian power plants and energy infrastructure after the US and Iran had 'very good and productive conversations'. Nonetheless as it stands, Iran denied talks with the US and called it fake news, but said messages had been conveyed in recent days through several friendly countries, while the partial rebound in oil was also spurred by a report that some gas-related facilities were hit amid US-Israeli strikes on Isfahan. Price action this morning has been rather rangebound, although some downside was seen following reports that Iranian Foreign Minister Araghchi is said to have secretly informed US Envoy Witkoff of Iranian Supreme Leader Mojtaba Khamenei’s agreement to negotiate, Al Arabiya reported citing Israeli press Yedioth Ahronoth citing sources, although this remains unconfirmed. Prices clambered off those lows as Israeli official suggests that it is unlikely that Iran will agree to US demands. WTI resides in a current USD 88.50-92.29/bbl range, and Brent in a USD 101.93-101.93/bbl parameter.

- Spot gold is subdued amid a firmer USD as traders continue to weigh conflicting reports, with the yellow metal at the whim of the USD and oil prices, trading off lows in a current USD 4,305.94-4,448.33/oz range, but well within yesterday’s USD 4,099-4,536/oz range.

- Base metals are mixed with a softer bias. 3M LME copper futures hover on either side of USD 12k/t as concerns over the Iran war’s impact on global growth and inflation weighed on sentiment, with PMIs also pointing to stagflation. 3M LME copper resides in a USD 11,908.00-12,111.98/t range at the time of writing.

- Russia's agriculture ministry said the fertiliser export restrictions only concern ammonium nitrate. This comes following TASS reporting that Russia is introducing some limits on fertiliser exports until April 21st.

- India's Reliance (RIL IS) has reportedly purchased 5mln bbls of Iranian oil following the US sanctions waiver.

- The attacks on the gas pipeline in Khorramshahr did not affect its operations, Iran's Fars News agency reported.

- Mitsui O.S.K. Lines (9104 JT) denies reported its vessel passed through Strait of Hormuz.

- Japanese PM Takaichi said will start releasing joint oil storage with oil producing countries by end of March.

- Macquarie forecasts Brent hitting a floor of USD 85-90/bbl if the Iranian tensions decrease; said USD 150/bbl is still an option if the Strait of Hormuz remains shut until April.

TRADE/TARIFFS

- EU farmers see the concessions offered as part of the EU-Australia trade deal as 'unacceptable', AFP reported.

- EU and Australia agreed to a free trade deal, according to a joint statement.

- Chinese Commerce Minister Wang Wentao meets the US-China Business Council delegation; details light.

NOTABLE EUROPEAN DATA RECAP

- UK S&P Global Composite PMI Flash (Mar) 51.0 vs. Exp. 52.8 (Prev. 53.7, Low. 51.3, High. 53.6). “The war in the Middle East has hit the UK economy in March, stalling growth while driving inflation sharply higher.". “Inflationary pressures have surged higher on the back of rising energy prices and fractured supply chains. The acceleration in cost growth in the manufacturing sector was especially severe, being the sharpest since the depreciation of sterling following Black Wednesday in 1992."

- UK S&P Global Manufacturing PMI Flash (Mar) 51.4 vs. Exp. 50.5 (Prev. 51.7, Low. 48.0, High. 51.6).

- UK S&P Global Services PMI Flash (Mar) 51.2 vs. Exp. 53 (Prev. 53.9, Low. 50.0, High. 53.8).

- EU S&P Global Composite PMI Flash (Mar) 50.5 vs. Exp. 51 (Prev. 51.9, Low. 49.7, High. 51.5). “The survey data are indicative of eurozone GDP growth slowing to a quarterly rate of just below 0.1% in March with the forward-looking indicators pointing to a heightened risk of a downturn the coming months. The survey’s price gauge is meanwhile indicative of consumer price inflation accelerating close to 3%, with cost pressure likely to add still further to selling price inflation in the coming months."

- EU S&P Global Manufacturing PMI Flash (Mar) 51.4 vs. Exp. 49.4 (Prev. 50.8, Low. 48.2, High. 50.3).

- EU S&P Global Services PMI Flash (Mar) 50.1 vs. Exp. 51 (Prev. 51.9, Low. 50.2, High. 51.9).

- German S&P Composite PMI Flash (Mar) 51.9 vs. Exp. 51.8 (Prev. 53.2, Low. 50.7, High. 52.7). "The service sector has seen an immediate negative impact. Growth in business activity has slowed sharply to its weakest since the current upturn began last September, weighed down by a drop in inflows of new work that reflects a combination of increased uncertainty and rising price pressures.". "The big surprise is perhaps the acceleration in growth in the manufacturing sector. Reports from goods producers indicate that demand has in some cases been boosted by companies reacting to the disruption and uncertainty brought on by the war in the Middle East."

- German S&P Manufacturing PMI Flash (Mar) 51.7 vs. Exp. 49.4 (Prev. 50.9, Low. 48.0, High. 52.0).

- German S&P Services PMI Flash (Mar) 51.2 vs. Exp. 52 (Prev. 53.5, Low. 49.5, High. 53.2).

- French S&P Composite PMI Flash (Mar) 48.3 vs. Exp. 49.9 (Prev. 49.9, Low. 48.9, High. 49.8)."Soaring oil and oil-product prices, rising fuel costs and disrupted maritime supply chains have led to the worst delivery delays from vendors in over three years and pushed up input prices for French companies to an extent not witnessed since late-2023."

- French S&P Manufacturing PMI Flash (Mar) 50.2 vs. Exp. 49.5 (Prev. 50.1, Low. 48.4, High. 49.8).

- French S&P Services PMI Flash (Mar) 48.3 vs. Exp. 49 (Prev. 49.6, Low. 48.6, High. 49.8).

CENTRAL BANKS

- BoJ Governor Ueda said he expects underlying inflation to accelerate moderately and price trend is to rise gradually. Tight labour market, firms' active wage, price-setting behaviour will keep in place a cycle in which wages and prices rise in tandem. Temporary freeze on food sales tax may briefly push down inflation, but is likely to have a limited impact on inflation expectations. Will guide monetary policy appropriately to stably achieve the inflation target, accompanied by wage gains. To conduct policy for stable prices with wage growth.

- ECB's Kazaks says it is clear prices will be higher, and growth will be slower.

- ECB's Vujcic said ECB must be vigilant facing stagflation risk and officials will know soon whether they must act, adds if hikes are needed, better to start with a small move.

- RBNZ Governor Bremen said will see higher inflation over the near term and some growth impacts, adds will be looking if firms are passing on costs or absorbing them, also looking for second round effects and will act if inflation expectations shift.

NOTABLE US HEADLINES

- US GOP senators see a path to ending the Department of Homeland Security shutdown after a Trump meeting on Monday, according to POLITICO.

- Four Senate Republicans meeting with US President Trump at the White House and discuss funding for the Department of Homeland Security, according to POLITICO.

GEOPOLITICS

MIDDLE EAST

- Iranian Foreign Minister Araghchi is said to have secretly informed US Envoy Witkoff of Iranian Supreme Leader Mojtaba Khamenei’s agreement to negotiate, Al Arabiya reported citing Israeli press Yedioth Ahronoth citing sources.

- Senior Iranian Foreign Ministry official said Iran received points from the US through mediators and that they are being reviewed, according to CBS News.

- Iranian Revolutionary Guard said it is launching the 78th wave of Operations Al-Waad Al-Sadiq 4 towards the occupied territories and American bases.

- The chances of an agreement between the US and Iran are “very small,” Israeli officials told The Jerusalem Post; sources said the deployment of American forces in the Middle East is continuing as usual. Israeli officials also said there has been no change in coordination with the US military or in operational plans.

- Israeli official suggests that it is unlikely that Iran will agree to US demands; said US President Trump is determined to reach a deal with Iran.

- Israel's Air Force is launching raids on military infrastructure and production sites near Isfahan,, Israel's Channel 12 reports.

- Israeli Defence Minister Katz says Israel will establish a buffer zone in southern Lebanon, modelled on what was implemented in Rafah, Al Jazeera reports; the army is now carrying out ground operations in Lebanese territory to control the front line.

- Gas-related facilities said to be hit in strikes on Isfahan in central Iran, in which offices belonging to a gas company and a gas pressure reduction station were damaged in a US-Israeli attack on Isfahan in central Iran, according to Fars News Agency.

- A projectile fell on a gas pipeline feeding a power station in Khorramshahr, Iran, while there were no casualties.

- Saudi Arabia reportedly told the US it was ready to strike Iran if its own power and water facilities were targeted by Iran, according to reported citing sources.

- US President Trump's admin is eyeing Iran’s parliament speaker Ghalibaf as US-backed leader, according to POLITICO.

RUSSIA-UKRAINE

- The US is ready to provide real security guarantees if Ukraine withdraws from Donbas, according to Ukrainian press citing sources. According to the interlocutors, in the absence of progress, the American side is allegedly considering the possibility of withdrawing from the negotiations and switching attention to other areas, in particular Iran.

CRYPTO

- Bitcoin holds above USD 71k, while Ethereum trades around USD 2150.

APAC TRADE

- APAC stocks took their cues from the positive performance on Wall Street, where the major indices rallied, and oil dropped after US President Trump announced US-Iran conversations and a five-day halt of strikes against Iranian energy infrastructure, while Iran denied the talks and called it fake news. Nonetheless, stocks gained in Asia but are well off their earlier highs as the conflict persisted overnight, while oil prices also partially rebounded amid news that gas-related facilities were hit in strikes on Isfahan in central Iran, where offices belonging to a gas company and a gas pressure reduction station were damaged.

- ASX 200 climbed at the open with outperformance in mining, materials and resources, although the index eventually pared the majority of gains with losses seen in tech and financials, while flash PMI data weakened.

- Nikkei 225 traded higher but had given back a chunk of the earlier spoils and briefly returned to beneath the 52,000 level with headwinds seen as oil prices partially rebounded from yesterday's slump.

- Hang Seng and Shanghai Comp gained with outperformance in Hong Kong amid tech strength and with attention on earnings.

NOTABLE APAC DATA RECAP

- Japanese Inflation Rate YoY (Feb) Y/Y 1.30% vs. Exp. 1.50% (Prev. 1.50%).

- Japanese Core Inflation Rate YoY (Feb) Y/Y 1.60% vs. Exp. 1.70% (Prev. 2.00%, Low. 1.50%, High. 1.80%).

- Japanese Inflation Rate MoM (Feb) M/M -0.2% (Prev. -0.1%).

- Japanese Inflation Rate Ex-Food and Energy YoY (Feb) Y/Y 2.50% vs. Exp. 2.70% (Prev. 2.60%).

- Japanese S&P Global Services PMI Flash (Mar) 52.8 vs. Exp. 51.8 (Prev. 53.8).

- Japanese S&P Global Manufacturing PMI Flash (Mar) 51.4 vs. Exp. 52.8 (Prev. 53).

- Japanese S&P Global Composite PMI Flash (Mar) 52.50 vs. Exp. 51.3 (Prev. 53.90).

- Australian S&P Global Services PMI Flash (Mar) 46.6 (Prev. 52.8).

- Australian S&P Global Composite PMI Flash (Mar) 47.0 (Prev. 52.4).

- Australian S&P Global Manufacturing PMI Flash (Mar) 50.1 (Prev. 51.0).

Loading...