Global equities rise on plans of a Middle East ceasefire; President Trump to speak at a dinner - Newsquawk US Market Open

- US special envoy Witkoff and Jared Kushner are working on a mechanism which aims for a one-month ceasefire, while this would be very similar to understandings in Gaza and Lebanon, and a 15-point agreement will be negotiated during the month of a possible ceasefire.

- Iran has reportedly received the 15-point US ceasefire proposal, according to AP citing Pakistani officials.

- Crude slips as an Iranian ceasefire framework emerges.

- Global equities rise on plans of a Middle East ceasefire; ARM surging after the announcement of the sale of its own chips.

- USD slightly firmer but off best, AUD lags following a cooler inflation report while EUR unmoved following German Ifo.

- Fixed income firmer as softer energy prices dictates price action.

- Looking ahead, highlights include US Import/Export Prices (Feb), SNB Quarterly Bulletin (Q1). Speakers include ECB's Rehn & Kocher, BoE's Greene, Fed's Miran, US President Trump, Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

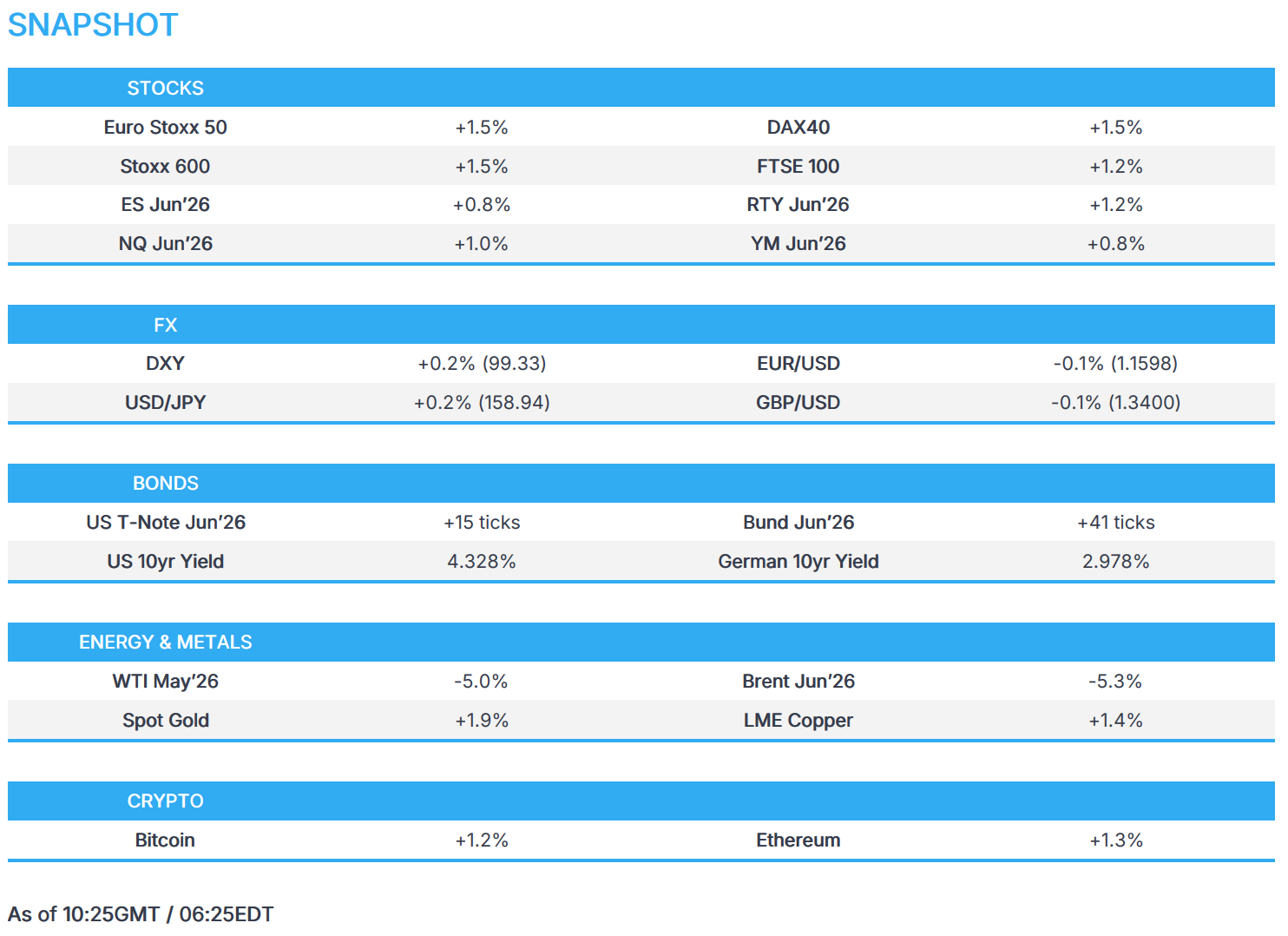

- European bourses (STOXX 600 +1.5%) are entirely in the green, benefiting from the reports that US is planning a one-month ceasefire and 15-point agreement, which has reportedly been received by Iran.

- European sectors, for the first time in a while, are all gaining. Industrial Goods and Services top the sector pile, closely followed by Technology. On the other hand, Telecoms lags.

- US equity futures (ES +0.8% NQ +1% RTY +1.2%) are following its European peers, trading with decent gains. Arm Holdings is surging in pre-market trade after the Co. announced that it will sell its own chips for the first time, forecasting annual revenue of around USD 15bln within 5 years.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is slightly firmer this morning, with the trough of the day coinciding with its 21 DMA at 99.07 (vs peak of 99.42). Geopols once again the main driver of action for the index this morning; to recap, a US-led 15-point ceasefire plan has been formed, whilst Iran has denied negotiations entirely. Earlier today, the index dipped off best levels on reports that Iran had received the 15-point plan, pointing to some initial progress to diplomacy. DXY fell from 99.36 to 99.25 within a few minutes, before then reversing much of that move thereafter.

- G10s are entirely lower vs USD this morning. The net-importers of energy regions (EUR, GBP, JPY) appear to be faring better vs peers, given the pressure in crude prices in recent trade. Antipodeans are underperforming, with underperformance in the Aussie in the aftermath of the slightly softer-than-expected Australian monthly inflation data.

- EUR has had some ECB speak to digest this morning, and a few regional data points. ECB President Lagarde highlighted that “small, one-off and short-lived supply shocks can be looked through”, but noted that it “will not be paralysed by hesitation”. No move on her comments. Chief Economist Lane also provided some commentary, where he stated that market-based inflation expectations have risen since the start of the Iran conflict. Also, in the rearview, German Ifo metrics were fairly resilient, with Business Climate holding steady at 88.6 (topping expectations), whilst Expectations dipped to 86.0 (prev. 90.2). ING believes the recent Middle East conflict should only “delay, not derail” the rebound in Germany. EUR is currently a touch lower vs USD, and trades within a 1.1587-1.1630 range.

- GBP is also incrementally lower vs the USD, holding within a 1.3370-1.3436 range and trading in close proximity to its 100 DMA (1.3407), 21 DMA (1.3390) and 200 DMA (1.3433). Cable saw some fleeting upside on this morning’s inflation report, where headline printed a touch below expectations though core and services Y/Y figures topped expectations. Ultimately, the data lacks significance given it surveys the February period, before the Iran conflict began. Nonetheless, the series marginally adds to the stagflationary diagnosis the UK economy is currently subject to.

- Barclays FX month-end rebalancing: strong USD buying against most majors, and moderate buying against the EUR, JPY and GBP.

FIXED INCOME

- A bullish start to the day as the progress towards a ceasefire weighs on the energy space, allowing yields to ease from highs and in turn underpinning the fixed income space. Thus far, USTs have been as high as 110-30 with gains of 17 ticks at best. However, the benchmark remains shy of the WTD peak at 1110-04+ and by extension well off recent peaks.

- Elsewhere, EGBs and Gilts are bid, with gains of 43 and 53 ticks respectively, but off best levels by around 20 and 40 ticks.

- Bunds unreactive to remarks from ECB's Lagarde and Lane, which largely stuck to the script from last week. Elsewhere, the March German Ifo series was better than expected, though the readings did decline from the prior, with the exception of the Current Assessment. However, the series clearly shows that the economy is feeling the impact of the Middle East situation, but participants are yet to determine if the crisis is a lasting one or not, in terms of its economic impact. In short, further evidence of stagflation in the EZ.

- For Gilts, the bias was bullish given the above. However, the February CPI series marginally added to the stagflationary diagnosis the UK economy is currently subject to. Nonetheless, Gilts opened higher by around 35 ticks before climbing to an 88.62 peak with gains of 99 ticks at best. Ahead, BoE's Greene may weigh in on the UK's precarious economic situation.

- Germany sells EUR 1.726bln vs exp. EUR 2.0bln 2.60% 2041 and 0.00% 2052 Bund.

- Italy sells EUR 2.0bln vs exp. EUR 1.75-2.0bln 2.20% 2028 BTP & EUR 2.0bln vs exp. EUR 1.5-2.0bln 1.10% 2031, 1.80% 2036 BTPei.

- German KfW Head of Capital Markets said Euro Green bond issuance “likely to come early” in Q2; Issuance window is now shorter amid the conflict.

COMMODITIES

- WTI and Brent futures have pulled back this morning in a continuation of the premium unwind following reports the US is proposing a one-month ceasefire mechanism being developed by Witkoff and Kushner, similar to frameworks used in Gaza and Lebanon, whilst US also sent Iran a 15-point plan to end the war (full Newsquawk Analysis on the board). Iranian representatives reportedly told the Trump administration that the bar for returning to ceasefire talks remains high. There are also efforts to begin talks as soon as Thursday. The reports of US diplomatic drive have driven cautious optimism that the conflict may ease, helping lift equities and weigh on crude. Brent is trading below USD 96/bbl (in a USD 93.45-97.00/bbl range), while WTI trades a little beneath USD 89/bbl (in a USD 96.59-89.57/bbl range), despite the continued disruption in the Strait of Hormuz and additional US troop deployments to the Middle East.

- Nat gas prices meanwhile are weaker by some 7.5% at the time of writing, trading on either side of EUR 50/MWh, whilst reports suggested Dutch gas storage levels fall to the lowest point for this time of the year since 2010.

- Spot gold edged higher overnight and returned above the USD 4,500/oz level amid softer yields and lower oil prices, with the bullion currently within USD 4,456-4,602/oz. Analysts at ING suggest that “Near term, gold remains highly sensitive to Fed policy expectations, currency moves and geopolitical developments. Risks remain elevated as Iran retains control over the Strait of Hormuz and Israel continues operations against Iranian assets.”

- Copper futures benefit alongside the positive risk environment amid hopes for a ceasefire in the Iran conflict, with 3M LME copper in a USD 12,192.00- 12,348.35/t. Desks also suggest that positioning data points to a cautious rebound in risk appetite across base metals.

- Russia's Baltic Sea ports of Primorsk and Ust-Luga have reportedly suspended crude oil and oil products loadings after drone attacks.

- Russia is reviewing its energy supply chains amid Middle-East crisis to prioritise neighbouring nations, Tass reports.

- Hungarian PM Orban said gas flows to Ukraine will stop until oil flows through the Druzhba pipeline resumes.

- Japanese PM Takaichi requests the IEA to prepare additional oil release if needed, and met with IEA Executive Director Birol.

- IEA said it stands ready to release additional volumes from strategic oil reserves as required to support market stability.

- Valero (VLO) is said to be preparing its Port Arthur refinery to restart.

- Italian PM Meloni to meet top Algerian officials today in an effort to secure alternative gas supplies, according to FT.

- US President Trump's administration is expected to lift summer gasoline regulations to curb energy prices as soon as Wednesday, according to sources.

- Venezuela's opposition leader Machado said the country requires USD 150bln to boost oil output to 5mln bpd.

- Cosco (601919 CH / 1919 HK) have resumed new bookings for standard containers to the UAE, Saudi Arabia, Bahrain, Qatar, Kuwait and Iraq, effective immediately.

TRADE/TARIFFS

- China's Commerce Ministry, on Mexico's tariff increases on Chinese and non-FTA products, said it creates investment barriers; said China reserves the right to take measures.

NOTABLE EUROPEAN HEADLINES

- UK Business Secretary Kyle is to hold emergency talks with company bosses Wednesday morning about the impact of the Iran war on the UK economy, Sky News reported.

- Nigel Farage’s Reform UK abandoned pledge to nationalise water and energy companies, according to FT.

- Danish PM Frederiksen's bloc wins the election but lacks the majority with the left bloc winning 84 seats, right bloc gets 77 seats, and Danish moderate party wins 14 seats to become kingmaker, according to AFP.

- US President Trump endorses Hungarian PM Orban, stating he's a truly strong and powerful leader with a proven track record delivering of phenomenal results.

NOTABLE EUROPEAN DATA RECAP

- UK Inflation Rate MoM (Feb) M/M 0.4% vs. Exp. 0.4% (Prev. -0.5%, Low. 0.2%, High. 0.6%).

- UK Inflation Rate YoY (Feb) Y/Y 3.0% vs. Exp. 3% (Prev. 3%, Low. 2.8%, High. 3.2%); Services 4.3% vs. Exp. 4.2% (prev. 4.4%).

- UK Core Inflation Rate MoM (Feb) M/M 0.6% vs. Exp. 0.5% (Prev. -0.6%).

- UK Core Inflation Rate YoY (Feb) Y/Y 3.2% vs. Exp. 3.1% (Prev. 3.1%, Low. 3.0%, High. 3.3%).

- German Ifo Business Climate (Mar) 88.6 vs. Exp. 85.5 (Prev. 88.6, Low. 80, High. 88).

- German Ifo Expectations (Mar) 86.0 vs. Exp. 85.8 (Prev. 90.5, Low. 80, High. 90).

- German Ifo Current Conditions (Mar) 86.7 vs. Exp. 85.6 (Prev. 86.7, Low. 84.9, High. 87.6).

CENTRAL BANKS

- Fed's Goolsbee (2027 voter) said energy shocks can pose risks to both sides of the Fed mandate, while he doesn't know if they can cut rates again and it depends on how long the war will last. Possible that energy prices could stay high after the war ends. Likely to see a downturn in consumer sentiment. It's not an obvious playbook for what to do and it's a bad situation for a central bank.

- Fed's Barr (voter) sees rates holding steady for some time and wants evidence of sustainable inflation retreat. Labour market seems to be stabilising. Middle East conflict raises additional risk.

- ECB's Lagarde said "Small, one-off and short-lived supply shocks can be looked through. But as expected deviations from our inflation target grow larger and more persistent, the case for action becomes stronger.". "When the energy shock hit in 2021–22, several of these channels were operating simultaneously. But there are factors today which point to a lesser pass through."; namely, the initial shock has thus far been smaller, and today's macroeconomic backdrop is more benign. "We will not act before we have sufficient information on the size and persistence of the shock and its propagation. But we will not be paralysed by hesitation: our commitment to delivering 2% inflation over the medium term is unconditional."

- ECB's Lane said the central bank will at every meeting consider what the scenario is before setting policy.

- BoJ Minutes from the January 22nd-23rd meeting stated some members expressed the recognition that the Bank was currently at the stage of closely monitoring developments in economic activity and prices as well as financial conditions.

- Riksbank Minutes (Mar): Thedeen said "Our starting point with low inflation gives us some respite until we have a clearer picture of the economic consequences of the war...".

- RBA Assistant Governor Jones said RBA is shifting focus from if to how on digital tokens.

- RBNZ Chief Economist Paul Conway urged New Zealand's government to pursue structural reforms to lift productivity, saying monetary policy can’t solve the cost-of-living crisis alone.

GEOPOLITICS

MIDDLE EAST

- Iranian source says Pakistan has handed a US proposal to Iran, while the venue of talks is still being discussed, Reuters reports.

- Iran has reportedly received the 15-point US ceasefire proposal, according to AP citing Pakistani officials. The Pakistani officials described the proposal broadly as touching on sanctions relief, civilian nuclear cooperation, a rollback of Iran’s nuclear program, monitoring by the International Atomic Energy Agency, missile limits and access for shipping through the Strait of Hormuz.

- Iran's Ambassador to Pakistan said there were no talks between the US and Iran, either directly or indirectly, IRNA reported; said "friendly countries" seek to lay the ground for talks, "hopes these efforts can help in ending the war".

- Iran suspects US President Trump's peace talk push is a trick, while Iranian officials told countries attempting to mediate peace talks that they have been tricked twice by Trump and don't want to be fooled again, according to a source cited by Axios.

- Iranian officials have told the Trump administration via channels that they do not want to resume negotiations with Envoy Steve Witkoff and Jared Kushner, while it prefers to negotiate with VP JD Vance.

- Iranian representatives have communicated to the Trump administration a high bar for re-entering ceasefire negotiations, according to people familiar with the matter cited by WSJ/Dow Jones.

- United Command of Iranian Armed Forces spokesperson said US is negotiating with itself, according to IRNA.

- Iranian Foreign Ministry spokesperson said there is no dialogue or negotiations with the US; no one trusts US diplomacy. Forces are focussed on defense.

- Iranian Navy Commander says USS Lincoln strike group is under constant Iranian monitoring and will be targeted as soon as it comes within range of missile systems, SNN reports.

- A senior analyst with knowledge of the ongoing ceasefire talks said that discussions between the US and Iran were making quiet but swift progress.

- Israel's UN envoy said Israel is not part of negotiations between the US and Iran.

- US and Arab officials say mediators from Turkey, Egypt and Pakistan are pushing to have a meeting arranged between US and Iran in the next 48 hours, but both sides remain far apart, according to WSJ.

- Trump administration increasingly using US Treasury Secretary Bessent to communicate its case on Iran as it seeks to contain market fallout, Semafor reported. Some critics called the choice unusual and a sign of dysfunction, while others said his standing in economic circles made him a credible spokesman. White House officials said he was key to reassuring markets and the public.

- US orders 82nd Airborne army paratroopers to the Middle East as earlier flagged, according to Washington Post. US officials said that seizing Kharg Island is among the plans the administration is considering.

- US Senate voted 53-47 to block resolution that would limit President Trump's Iran war power.

- Israel hit a Russian-Iranian weapons smuggling route in the Caspian Sea, according to WSJ.

- IDF said it has started a new wave of strikes targeting Iranian regime's infrastructure in Tehran.

- Five explosions at a missile site in Isfahan this morning, Al Hadath reported citing Iranian media.

- IAEA Chief Grossi said talks between Washington and Tehran on the nuclear program and other issues may be held in Islamabad in the coming days.

- Kuwait's General Authority of Civil Aviation said drones targeted fuel tanks at Kuwait's international airport, causing a fire, although there were no casualties reported.

- UK PM Starmer said UK is now working with partners on a plan to ensure flows of goods through key maritime routes, following a call with the Saudi Crown Prince.

CRYPTO

- Bitcoin returns above USD 71k amid the positive risk tone, Ethereum nears USD 2.2k.

APAC TRADE

- APAC stocks traded higher with risk sentiment spurred by hopes of a halt to the Iran conflict after optimistic comments from US President Trump regarding negotiations, while it was reported that the US was working on a 1-month ceasefire and offered a 15-point plan to Iran for ending the conflict.

- ASX 200 rallied with gains led by outperformance in mining stocks as gold producers cheered a rebound in the precious metal, while the federal and Queensland governments announced a AUD 2bln bailout for Rio Tinto's Boyne aluminium smelter.

- Nikkei 225 outperformed and returned to above the USD 53,000 level as Iran ceasefire hopes to alleviate the recent oil and inflation-related pressures.

- Hang Seng and Shanghai Comp were positive, albeit to varying degrees throughout the day, as participants digested a slew of earnings releases, while the PBoC conducted a CNY 500bln on 1yr MLF operation.

NOTABLE APAC DATA RECAP

- Australian Inflation Rate YoY (Feb) Y/Y 3.7% vs. Exp. 3.8% (Prev. 3.8%, Low. 3.5%, High. 4.0%).

- Australian Inflation Rate MoM (Feb) M/M 0.0% vs. Exp. 0% (Prev. 0.4%, Low. -0.2%, High. 0.4%).

- Australian RBA Weighted Median CPI YoY (Feb) Y/Y 3.5% vs. Exp. 3.6% (Prev. 3.6%).

- Australian RBA Weighted Median CPI MoM (Feb) M/M 0.2% vs. Exp. 0.3% (Prev. 0.3%).

- Australian RBA Trimmed Mean CPI YoY (Feb) Y/Y 3.3% vs. Exp. 3.4% (Prev. 3.4%, Low. 3.3%, High. 3.4%).

Loading...