Global stocks mixed, crude firms and DXY lower after reports Iran communicated a three-stage negotiating process to the US - Newsquawk US Market Open

- Iran communicated a three-stage negotiating process to the US; 1) focus on ending the war and receiving guarantees, 2) then on the Strait of Hormuz, 3) and finally on nuclear issues.

- The US cancelled sending Witkoff & Kushner to Pakistan, suggesting it was a waste of time; Trump is to hold a situation room meeting on Monday, Axios.

- European bourses are modestly mixed, with US equity futures also holding around the unchanged mark; Qualcomm +12% on reports of an OpenAI partnership.

- DXY trundles below technical support, Antipodeans outperform, and GBP unfazed by potential PM referral.

- Fixed falters slightly as energy climbs into a packed week.

- Crude prices gain amidst a lack of US-Iran progress, but with focus on a three-stage plan.

- Looking ahead, highlights include US Dallas Fed Manufacturing Index (Apr), Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

MIDDLE EAST

- Iran has communicated a three-stage negotiation process to the US through intermediaries, according to Al Mayadeen citing Iranian reports. The first stage would focus on ending the war and receiving guarantees to prevent recurrence. Second stage is to be focused on the Strait of Hormuz while the third stage would lead to the nuclear issues. Axios later announced a similar report, adding that US President Trump is to hold a situation room meeting on Iran on Monday.

- US President Trump cancelled sending Steve Witkoff and Jared Kushner to Pakistan for talks with Iran, saying there would be “too much time wasted on travelling”. Trump said the US “has all the cards” and Iran “has none”, adding that “if they want to talk, all they have to do is call”. Trump later said the US would not travel “15, 16 hours” to meet “people nobody’s ever heard of”, adding that US envoys were not meeting Iran’s actual leader. Trump claimed Iran sent a “much better” offer within 10 minutes of him cancelling the envoys’ trip, but said Iran had offered “a lot but not enough”.

- US President Trump said Iran wants to talk and see if they can make a deal, US officials negotiating with Iran are dealing with the people who are in charge now. He also stated that Iran plans to make an offer aimed at resolving US demands, according to Reuters.

- Iran's Foreign Minister Araghchi posted on X that discussions in Oman included focusing on ways to ensure the safe transit through Hormuz and that neighbours are the priority. He later stated in Russia, ahead of his meeting with Russian President Putin, that the visit to Islamabad was very good, in which conditions were reviewed for US-Iran talks to continue.

- Iranian Foreign Minister Araghchi described his Pakistan visit as “very fruitful” and said Iran had shared a “workable framework to permanently end the war.” According to reports citing Pakistani officials, Araghchi laid out Tehran's negotiating demands as well as its reservations about US demands. In other talks, IRNA reported that the FM will travel to Muscat and Moscow to hold bilateral conversations, discuss current developments in the region, and the latest situation regarding the war.

- A trilateral meeting with the US, Iran and Pakistan will be considered only after Pakistan meet with Araghchi, a meeting between the US and Iran may not take place until Monday, Axios reported. US Special Envoy Witkoff and Kushner is to hold separate talks with Pakistan on Sunday.

- Axios reported that a US official and a source said Ghalibaf grew frustrated with the infighting in the Iranian leadership after the previous round of talks, and even threatened to step aside. It still remains unclear if he is the lead Iranian negotiator.

- Iran is reportedly "discussing the uranium and nuclear issue with friends and allies and is open for discussion at the negotiating table.", Journalist Mallick reported. Full post:"To my understanding, While Iran has proposed a structured operational mechanism for Strait of Hormuz which would lead to cessation of hostilities, at the same time, contrary to reported, Iran is discussing the uranium and nuclear issue with friends and allies and is open for discussion at the negotiating table.".

- Hezbollah outlines that they will be keeping their weapons, and dismisses the prospect of direct talks with Israel regarding Lebanon.

- Iran's proposal regarding Hormuz may be rejected by Washington because it excludes nuclear discussions, Al Hadath reported citing regional officials.

- Senior Israeli officials have told their American counterparts that if Hezbollah continues its attacks against IDF soldiers, Israel will not be able to respond in a measured manner, Journalist Stein reported citing sources.

- Israeli military reported hostile aircraft infiltration sirens sounded in northern Israel communities.

- Iranian Foreign Minister Araghchi said the visit to Islamabad was very good, in which conditions were reviewed for US-Iran talks to continue. Agreement has been made between Iran and Oman to continue consultations at an expert level.

- Israeli occupation forces are shelling Gaza beaches from the sea, according to Al Jazeer sources.

- Iran gave the US a new proposal through Pakistani mediators for reaching a deal on reopening the Strait of Hormuz and ending the war however postponing nuclear talks, Axios reported citing sources. US President Trump to hold a situation room meeting on Iran on Monday.

- Israeli artillery shelling targets eastern Gaza City, Al Mayadeen reported.

- Iran's Foreign Minister Araghchi posted on X that discussions in Oman included focusing on ways to ensure the safe transit through Hormuz and that neighbours are the priority.

- Lack of trust between Washington and Tehran hinders resumption of negotiations, Pakistani source tells Asharq.

- Iranian F-5 fighter jet reportedly breaches US air defences and hits a US military base in Kuwait, according to Press TV.

- US CENTCOM announces that the US has directed 38 ships to turn around or return to post since the start of the blockade.

- UKMTO reported of an incident occurring 6NM northeast of Somalia, where unknown persons seized the cargo ship and diverted it into territorial waters.

EQUITIES

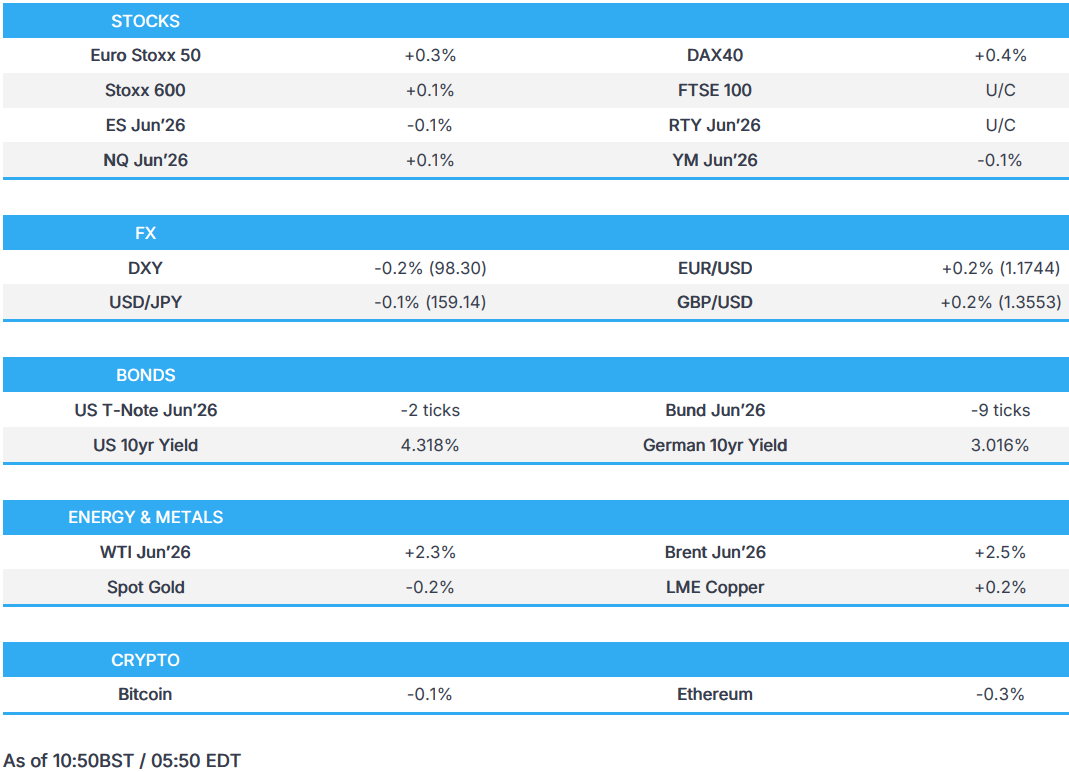

- European bourses are mostly firmer this morning, albeit modestly so. The DAX 40 (+0.4%) leads vs peers, whilst the AEX (-0.3%) lags a touch.

- European sectors opened with a positive bias, but the leaderboard now looks mixed. Topping the pile is Retail, led by Adidas, +1.6%, where two runners wore its new ultra-light racing shoe to break the two-hour barrier at the 2026 London Marathon. Also performing well is the Energy sector, with oil benchmarks firmer on the day. At the bottom of the pile are the consumer-sensitive Optimised Personal Care and Food Beverage & Tobacco.

- US equity futures are modestly mixed on either side of the unchanged mark; ES -0.1%, NQ +0.1%. The US-specific docket is light ahead of this week's FOMC meeting, with just 2 and 5yr supply, and Dallas Fed Manufacturing scheduled.

- OpenAI is working with MediaTek (2454 TW) and Qualcomm (QCOM) on mobile processors, and with Luxshare as exclusive system design and manufacturing partner, for AI agent phones, according to Ming-Chi Kuo.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX shows a risk-on picture not seen across other asset classes, in a move seemingly driven by a weaker greenback, with antipodeans and generally high-beta FX outperforming.

- DXY is lower by 0.2%, well off highs of 99.34 made at the Asia re-open and below both 100 and 200 DMAs, which offered support last week. This comes as Axios reported that Iran gave the US a new proposal for reaching a deal on reopening the Strait of Hormuz, news which has helped the risk complex. The plan calls for an extension of the ceasefire so parties can work on a three-stage plan, with nuclear negotiations the final stage. The report noted that Pakistani mediators had given the proposal to the US, though it was unclear if the US would cooperate. The US-specific docket is light ahead of this week's FOMC meeting, with just 2 and 5yr supply, and Dallas Fed Manufacturing scheduled.

- Away from geopolitics, and perhaps another story which has offered the USD: Senator Tillis said he was dropping his decision to block the nomination of Kevin Warsh as Fed Chair following the DoJ's decision to drop the criminal case against Fed Chair Powell. The vote on Warsh's confirmation is scheduled for 29th April.

- Antipodeans outperform, the cross is choppy and around the unchanged mark as both currencies benefit against the weaker Buck following that Axios report. NZD/USD, AUD/USD +0.6%/+0.5%. CAD also does well, helped by the risk environment alongside Crude benchmarks, which are firmer on the session.

- EUR/GBP is a touch firmer after it bounced off a 0.8654 low to try to recoup last week's modest losses following strong UK data. Both currencies look to expected holds from the ECB and BoE. In the UK, political angst persists, with the Daily Mail reporting that former Deputy PM Rayner told Labour MPs the time to oust the PM was “now or never”.

FIXED INCOME

- A softer start to the week, as energy upside lifts yields and weighs on fixed benchmarks. However, the magnitude of fixed action is relatively limited amid mixed geopolitical reporting, awaiting supply and the week's packed central bank agenda, which includes the BoE, ECB & Fed.

- USTs as low as 111-01, with downside of 5+ ticks at most. If the move extends, we look to 110-27+ and 110-26+ from Friday and Thursday, before attention then turns to 110-22+, 110-17+ and the 110-16 MTD low from earlier in April. The US agenda is, aside from geopolitical updates, headlined by 2yr & 5yr note supply ahead of Wednesday's Fed.

- Gilts gapped lower by 23 ticks and then slipped another 12 to an 87.13 low. Modestly underperforming peers, given the above. Elsewhere for the UK, we count down to Thursday's BoE, a hold is expected and priced, with attention on any clues via the statement, forecasts, or individual Committee members' remarks as to when a move might occur. Currently, markets imply 25bps hikes in July (+30bps) and December (+54bps).

- Bunds in-fitting with the above. Somewhere between USTs and Gilts in magnitude. As low as 125.48, posting losses of 17 ticks at most. Driven by the above geopolitical developments. No move to a weak GfK survey for May, as consumer sentiment was hit again by the Middle East conflict, resulting in a sharp decrease in income expectations and the 12-month view moved to a level similar to April 2022, at the start of the Ukraine conflict.

- China delays foreign debt sales with USD 100bln of bonds due, Bloomberg reported.

- EU sells EUR 6bln vs exp. EUR 7bln 2.50% 2031, 3.25% 2036, and 4.00% 2044 Bonds.

COMMODITIES

- WTI and Brent are both firmer this morning by circa. 2.6%, as the complex digests several geopolitical updates, with the overarching theme overall a lack of progress between US-Iran.

- To recap, US President Trump cancelled his envoy’s trip to Pakistan, suggesting that it would be a waste of time. He claimed that Iran sent a “much better” offer within 10 minutes of him cancelling the trip, but it was “not enough”. Since, Axios reported that Iran had communicated a three-stage negotiation process to the US through intermediaries. A first stage would involve securing guarantees to prevent another war, with the next stage to focus on the Strait and then finally on nuclear issues. Given that this proposal pushes the nuclear issue to the back of the agenda, it is not likely that the US will accept the proposal. The focus ahead will be on Trump, who is reportedly to hold a situation room meeting on Iran.

- WTI and Brent climbed higher throughout the European morning; Brent Jun’26 sits at the upper end of a USD 106.19/bbl to USD 108.24/bbl range, with WTI Jun’26 also at highs within a USD 94.99/bbl to USD 96.87/bbl band. Both contracts jumped at the open as markets digested Trump’s cancellation of talks, but then slipped on the aforementioned Axios report. The proposal indicates some openness to negotiations, but given that the nuclear issue has been pushed to the back of the agenda, it is unlikely to be accepted by the US. A factor which likely explains the complete reversal of the initial downside following the report.

- Spot gold is essentially flat this morning and currently trades within a USD 4,672-4,729/oz range. It currently oscillates around its 21 DMA (4,718/oz), with the high of the day a touch short of its 100 DMA (4,746/oz). Elsewhere, base metals hold a slight negative bias, but with slight strength in Aluminium prices, given the elongated disruption of supplies from the Middle East region. As for 3M LME Copper, it is currently a little lower within a USD 13,259-13,376.03/t range.

- Iran suspends exports of steel slabs and sheets until 30th May, Iranian media reported.

- Citi raises its base case average Brent price forecasts to USD 110/bbl for Q2, USD 95/bbl for Q3, USD 80/bbl for Q4. Flows could easily remain disrupted through the end of June, which could see Brent reach USD 150/bbl.

- Goldman Sachs raises its Brent forecast to USD 100/bbl this quarter and USD 90/bbl in Q4, due to prolonged disruption in the Strait of Hormuz and extreme inventory draws.

- Japanese PM Takaichi said Japan has secured stable oil supply into next year, closely watching the Middle East impact on the economy.

TRADE/TARIFFS

- India and New Zealand have signed a FTA, lowering and eliminating tariffs across a range of goods, and granting 100% duty-free access for Indian exporters.

- China's Commerce Ministry is to hold a press conference on Thursday 30th at 08:00BST/03:00EDT to brief on recent key trade and commerce developments.

- China's MOFCOM issues a statement on the EU Industrial Accelerator Act, calling it discriminative for trade; will closely monitor and engage in dialogue with the EU but threatens countermeasures if the EU presses ahead.

NOTABLE EUROPEAN HEADLINES

- ECB SAFE Survey: Firms reported further net tightening of bank loan interest rates and other loan conditions related to price and non-price factors. Firms reported further net tightening of bank loan interest rates and other loan conditions related to price and non-price factors. Financing needs remained stable, but availability of bank loans deteriorated marginally. Firms expected stronger increases in selling prices and non-labour input costs, whereas wage expectations moderated slightly. Short-term inflation expectations increased markedly, with medium-term inflation expectations remaining stable.

- UK Chancellor Reeves is to deliver speeches to set out a responsible plan to see households and businesses through the Iran war fallout, according to the FT citing sources; the Chancellor will also set out measures in June to boost growth.

- UK ministers have voiced concerns about the damage to the tech sector and its alliance with the US as the PM plans for closer relations with the EU, FT reported citing sources.

NOTABLE EUROPEAN DATA RECAP

- German GfK Consumer Confidence (May) -33.3 vs. Exp. -29.5 (Prev. -28.0).

CENTRAL BANKS

- BoJ Deputy Governor Uchida to join policy meeting by phone due to health reasons.

- Swiss Sight Deposits (CHF) (w/e Apr 24th): total 455.91bln (prev. 453.55bln), of domestic banks 433.01bln (prev. 433.27bln).

NOTABLE US HEADLINES

- The US Secret Service, is at risk of not being not being able to pay its employees by the end of the week, Semafor reported citing sources; suggesting that a shutdown nears its breaking point.

- The US and Japan plan a dual-use partnership to counter China in the drone market, Kyodo reported.

- US State Department has reportedly ordered a global warning over alleged AI IP theft involving DeepSeek and other Chinese firms, according to Reuters citing sources.

- US President Trump said he does not know if he was the target at the DC Gala.

NOTABLE US EQUITY HEADLINES

- OpenAI is working with MediaTek (2454 TW) and Qualcomm (QCOM) on mobile processors and with Luxshare as exclusive system design and manufacturing partner for AI agent phones, according to Ming-Chi Kuo. Mass production is expected in 2028, with specifications and suppliers due by end-2026 or Q1 2027. Kuo said OpenAI may bundle subscriptions with hardware.

- Southwest Airlines (LUV) said the Co. is not part of the US budget carriers seeking government aid.

- A group of budget airlines have requested USD 2.5bln in federal assistance in exchange for convertible warrants, WSJ reported citing sources.

GEOPOLITICS

RUSSIA-UKRAINE

- A drone has hit the transportation department of Ukraine's Zaporizhzhia plant, according to reported.

- Iranian FM Araghchi has arrived in Russia ahead of his meeting with Russian President Putin, Tasnim reported.

- North Korea's Supreme Leader Kim Jong-un said that North Korea will continue to support Russia, KCNA reported.

- Russia's Foreign Minister reportedly said Russia is willing to hold talks with the US on a Ukraine settlement.

CRYPTO

- Bitcoin is a little lower and trades around USD 78k; Ethereum also moves a touch lower and holds just above USD 2.3k.

APAC TRADE

- Asia-Pac stocks pointed to a broadly positive start of the week, mainly spurred by an Axios report detailing that Iran gave the US a new proposal, through Pakistani mediators, for reaching a deal on reopening the Strait of Hormuz and ending the war. It is a three-stage proposal, with the halting of the war and focus on the Strait of Hormuz highlighted as the key points before the third stage of nuclear issues.

- ASX 200 was the underperformer, being weighed on by losses in Energy and Utilities following Friday’s risk-on sentiment hitting energy prices. Among the weakness, Atlas Arteria outperformed after IFM investors offers to buy the Co. for AUD 4.75/security.

- Nikkei 225 initially traded with a lack of direction before being boosted following the Axios report. The index has regained the 60,000 handle and continued to gain towards 61,000.

- KOSPI was the clear outperformer as it tracks its peers’ stateside. This was spearheaded by Intel (INTC) after the Co. reported positive Q1 earnings and beat forecasts.

- Hang Seng and Shanghai Comp. traded with mild gains. Chips across Asia are performing well, with China’s SMIC also benefiting from the announcement that DeepSeek’s V4 is adapted to run on Huawei chips.

NOTABLE APAC DATA RECAP

- Japanese Coincident Index Final (Feb) 116.3 (Prev. 117.9).

- Japanese Leading Economic Index Final (Feb) 113.3 vs. Exp. 112.4 (Prev. 112.1).

- Chinese Industrial Profits (YTD) YoY (Mar) Y/Y 15.5% (Prev. 15.2%).

Loading...