IEA set to announce oil reserve recommendation; DXY flat heading into CPI - Newsquawk US Market Open

- The IEA has proposed the largest ever release of oil from its strategic reserves, with Bloomberg reporting around 300-400mln barrels to be released.

- Separate reporting stated that the volume in the first month of the release of oil reserves would exceed 100mln barrels.

- Crude rises as geopolitics show no real signs of abating; copper falls as sentiment deteriorates.

- European equities entirely in the red, Rheinmetall disappoints despite increased need for defence; US equity futures continue to consolidate.

- DXY flat heading into CPI, AUD outperforms as more banks forecast a hike next week.

- Hawkish ECB speak drives EGBs lower; packed UK agenda ahead.

- Looking ahead, highlights include US CPI (Feb), OPEC MOMR, IEA recommendation, G7 call. Speakers include ECB's Schnabel & Fed's Bowman, Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

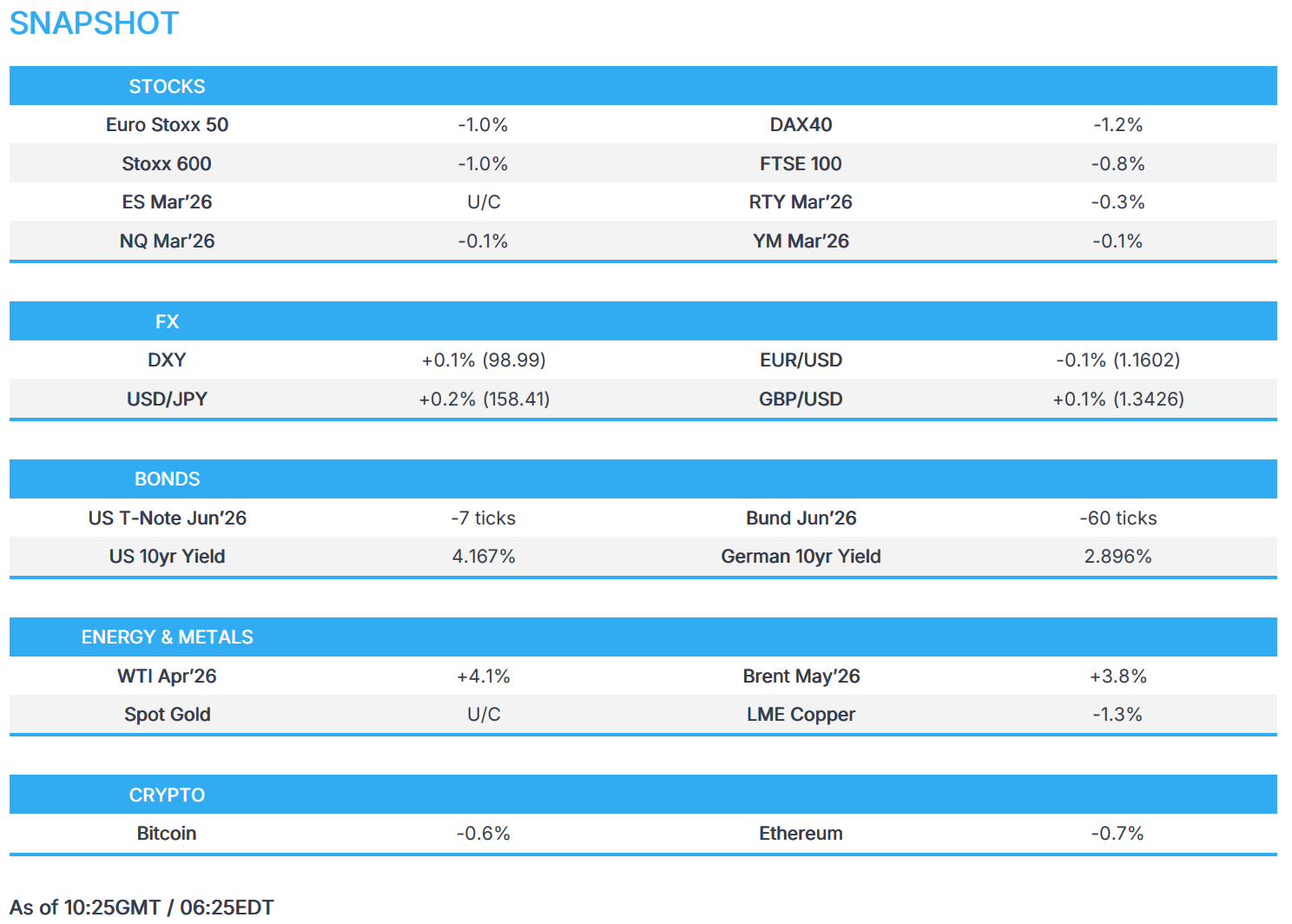

- European bourses (STOXX 600 -1.0%) are entirely in the red, as the Iran conflict intensifies. Losses in the IBEX 35 (-0.4%) have been limited after positive Inditex (+0.8%) earnings, which beat Q4 EBIT estimates and boosted capex following a strong start to 2026. The DAX 40 (-1.2%) underperforms after Rheinmetall (-6.2%) missed FY net income and guided softer 2026 revenue than analysts expected.

- European sectors are broadly weaker across the board, as Energy (+0.3%) continues to gain. Real Estate (-1.3%) and Financial Services (-1.3%), alongside Industrial Goods and Services (-1.8%), sit at the bottom of the pile, with higher yields and risk tone weighing on the sectors.

- US equity futures (ES U/C, NQ -0.1%, RTY -0.3%) are posting modest losses. In pre-market trade, Oracle (+10.5%) gains after-hours. The Co. reported earnings and revenue above expectations, and raised its FY revenue guidance as cloud revenue surged.

- Rheinmetall (RHM GY) – FY 2025 (EUR): Net Income 696mln (exp. 1.15bln), Revenue 9.9bln (prev. 9.75bln Y/Y), Backlog 63.8bln (prev. 49.9bln Y/Y). Raises dividend to EUR 11.50/shr (prev. EUR 8.10/shr).Guides initial FY26 Revenue 14-14.5bln (exp. 15bln), Op. Margin 19% (exp. 19.1%).

- Oracle (ORCL) - Q3 2026 (USD): Adj. EPS 1.79 (exp. 1.70), Revenue 17.2bln (exp. 16.92bln). Raises FY27 revenue view to USD 90bln (exp. 86.37bln) and said it expects to comfortably meet and likely exceed its FY27 revenue growth forecast.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is choppy this morning; currently trading around the unchanged mark, within a narrow 96.69-99.07 range. Little fresh from a European perspective, as focus remains on newsflow out of Iran. As it stands, the current conflict is showing few signs of ending, with reports now suggesting that Iran is taking steps to lay mines in the Strait of Hormuz. On the energy front, the IEA Governing Board is meeting today, whilst a separate G7 discussion on energy coordination is also scheduled for 14:00 GMT today. It was recently reported that the IEA proposed a 300-400mln barrel release of stockpiles – sources suggest that, should there be no objections, it could be announced as soon as today. Focus later will also be on US CPI, though it may lack signalling capacity given the current geopolitical situation.

- The Aussie extends on recent outperformance, as more banks now expect the RBA to hike rates at next week’s meeting. NAB and Westpac are the latest banks seen supporting a hike, joining the likes of Goldman Sachs and Bank of America. Delving into Westpac briefly, the bank previously forecast a hike in May, but the analysts now believe that the RBA will be “compelled to react” to the recent strength in oil prices. AUD/USD currently trades towards the upper end of a 0.71154 to 0.7185 range.

- Other G10s are trading modestly on either side of the unchanged mark vs the USD. The Loonie posts mild gains, given today’s strength in oil prices, whilst the JPY is the slight laggard, joined by the EUR. USD/JPY is venturing back into the touted “intervention zone”, beyond the 158.00 mark - though desks question the efficacy of intervening as the Iran war continues. GBP is essentially flat, awaiting cues from the Treasury Committee, which will question the Chancellor Reeves on the Spring Statement. BoE’s Breeden is also set to speak.

- For the EUR, currently trades just above the 1.1600 mark, within a 1.15904-1.1645 range. Today, there was a slew of ECB speakers, with particular focus on Kazimir who suggested that a rate hike on Iran may be closer than thought. This spurred some very modest upside in the EUR at the time, but was ultimately short-lived, given that he stated there is no reason to move rates at the next meeting.

FIXED INCOME

- APAC trade for fixed income was for the most part rangebound, with USTs and Bunds holding a handful of ticks in the red. JGBs also opened under pressure, with downside of 20 ticks at most. However, the move proved short lived as strong demand at the 5yr JGB tap underpinned the benchmark and lifted it to a 131.98 high, just shy of yesterday's 132.01 best.

- While relatively contained at first, EGBs came under renewed pressure early doors following ECB speak and a further uptick in energy benchmarks. Sending Bunds to a 126.55 trough over the course of the morning. On the former, Kazimir said an Iran-related rate hike could be closer than thought, though clarified that there is no reason to act in March. Near term market pricing has seen a very slight hawkish move this morning, but more pertinently end-2026 pricing implies around 25bps of tightening.

- In geopols, the UKMTO update seemingly spurred another leg higher in the crude space, with additional impetus potentially coming from the ongoing reporting around but lack of action on a reserve release.

- Moving to Gilts, the benchmark opened lower by over 50 ticks and has since slipped another 30 or so to a 90.27 base. Currently lagging, posting downside of 78 ticks vs 63 for Bunds. Action is very much occurring in tandem with the EGB move. Additionally, the UK has a packed agenda with Chancellor Reeves discussing her Spring Statement with the TSC, the release of Mandelson-related files by the government (around 12:30GMT) and then an appearance from BoE's Breeden, however this is scheduled to be on stablecoins.

- Vnet (VNET) , China's largest data centre operator, is considering a dollar bond sale to fund expansion, Bloomberg reported citing sources.

- Amazon (AMZN) opens books on eight-part EUR denominated bond offering.

- Japan sold JPY 1.9tln 5yr JGBs; b/c 3.69x (prev. 3.10x), average yield 1.633% (prev. 1.640%).

- Australia sold AUD 1bln 4.25% October 2036 bonds, b/c 3.87, avg. yield 4.9002%.

COMMODITIES

- WTI and Brent front-month futures have been grinding higher since early European hours following a choppy APAC session and the declines seen during the prior session. Yesterday, there was a bout of selling pressure after US Energy Secretary Wright mistakenly posted that the US Navy escorted an oil tanker through the Strait of Hormuz, although oil then pared some of the losses as the post was deleted shortly after, and the White House confirmed that this was false.

- Note, the IEA Governing Board is meeting today, whilst a separate G7 discussion on energy coordination is also scheduled for 14:00 GMT today. It was recently reported that the IEA proposed a 300-400mln barrel release of stockpiles – sources suggest that, should there be no objections, it could be announced as soon as later today.

- Spot gold holds an upward bias on either side of the USD 5,200/oz level, with the precious metal kept afloat alongside the recent easing in oil price pressures, although DXY has clambered off worst levels as eyes remain on flows in the Strait of Hormuz. A deterioration in sentiment in early European hours cushions downside for the yellow metal for now, which resides in a narrow USD 5,175.35-5,223.38/oz at the time of writing.

- Copper futures traded rangebound overnight but then slipped in early European hours amid a broader deterioration of sentiment as the Iranian war shows no signs of ending despite recent commentary from US President Trump. 3M LME copper is back under USD 13,000/t and resides towards the bottom end of a USD 12,993.00-13,151.53/t at the time of writing.

- G7 statement said the group is vigilantly monitoring the energy market, and G7 supports in principle the use of strategic oil reserve.

- IEA to recommend the release of strategic reserves, according to sources; volume in the first month would reportedly exceed 100mln barrels.

- IEA reportedly proposed oil stockpile release of around 300-400mln barrels, according to Bloomberg; decision is possible later on Wednesday, said a source.

- IEA has proposed the largest ever release of oil from strategic reserves to bring down the price of crude, according to WSJ. "Countries would decide Wednesday whether to release oil stocks in an attempt to tame crude prices". "The release would exceed the 182 million barrels of oil that IEA member countries put onto the market in two releases in 2022 when Russia launched its full-scale invasion of Ukraine".

- As part of a potential 400mln barrel IEA crude release, Germany would release around 19.5mln barrels, Handelsblatt reports citing sources; equating to around 20% of Germany's reserves

- Black Sea CPC blend oil exports were reportedly revised down to around 1.4-1.5mln BPD for March (prev. 1.7mln BPD)

- White House reportedly believes it can "withstand a brief spike in oil prices — for as many as four weeks... before the political hit does lasting damage", according to Politico citing sources.

- Iraq's oil ministry has sent a letter to the Kurdistan regional government for the export of at least 100k BPD via the Kurdistan pipeline to Turkey's Ceyhan, according to oil officials.

- EU Commission President von der Leyen said Europe's dependency on fossil fuels have cost it EUR 3bln in extra costs in the first 10 days of the Iran war, returning to Russian fossil fuels in the current crisis would be a strategic blunder. EU is preparing options to lower energy prices, which include better use of purchase power agreements and CFDs, state aid measures, gas price subsidies or caps.

- Maersk (MAERSKB DC) CEO tells the WSJ that 10 ships are trapped in the Persian Gulf and would need at least 10 days to resume normal operations if a ceasefire was to occur.

- Glencore (GLEN LN) workers reportedly set to conduct a strike at Australian copper refinery, according to Bloomberg.

TRADE/TARIFFS

- Ireland Prime Minister is planning to talk about EUR 6.1bln in investment into the US during the visit on March 17th, WSJ reported.

NOTABLE EUROPEAN HEADLINES

- European Commission draft Citizens' Energy Package recommends concrete measures to lower household energy prices, Handelsblatt reported; aim is to lower electricity taxes to a minimum.

NOTABLE EUROPEAN DATA RECAP

- German Inflation Rate YoY Final (Feb) Y/Y 1.9% vs. Exp. 1.9% (Prev. 2.1%, Low. 1.9%, High. 1.9%).

- German Inflation Rate MoM Final (Feb) M/M 0.2% vs. Exp. 0.2% (Prev. 0.1%).

- Spanish Retail Sales MoM (Jan) M/M 0.1% (Prev. -0.8%).

- Spanish Retail Sales YoY (Jan) Y/Y 4.0% (Prev. 2.9%).

CENTRAL BANKS

- ECB's de Guindos said risks are tilted to the downside, macroeconomic projections will be much more complicated now.

- ECB's Kazaks said the ECB could act if war raises inflation expectations.

- ECB's Kazimir said a rate hike on Iran may be closer than thought; no reason to act at next week's meeting.

- ECB’s Villeroy said he does not expect a rate hike at next week's ECB meeting, said energy costs are a minor part of consumer spending, said banks should stay calm amid the Iran crisis.

- ECB's Nagel said the ECB will act decisively if an energy spike feeds into durably higher inflation; the risk of higher inflation has risen, economic outlook has deteriorated; the latest US statements on Iran war offer cause for hope.

- Westpac and National Australia Bank now expect the RBA to hike rates in March and May.

NOTABLE US HEADLINES

- Senators Warner (D) and Rounds (R) are to introduce new legislation focused on AI and the workforce, Axios reported citing an announcement.

GEOPOLITICS

MIDDLE EAST

- Iran's Joint Command Spox said US and Israeli banks will be hit after an attack on an Iranian bank, via IRNA.

- Iran’s IRGC said it carried out its heaviest and most intense attacks since the start of the war, targeting US and Israeli assets across the region, according to WSJ.

- IRGC said it launched missiles carrying 2-ton warheads in a new wave of heavy, multi-warhead strikes targeting US bases in Iraq and Bahrain as well as Israel.

- Iran's police chief said anyone taking to the streets at the enemy's request will be confronted as an enemy and not a protester, adds security forces are prepared to respond and have their fingers on the trigger.

- Iran launches new wave of missiles on occupied territories.

- Iranian armed forces spokesperson vows retaliation for Israeli and US strikes on residential areas.

- US officials said Iran has laid less than 10 mines in the Strait of Hormuz and it is unclear if it intends to lay more in the near term, according to WSJ.

- Drone reportedly hits a US diplomatic facility in Iraq, according to Washington Post.

- US Central Command said US forces eliminated multiple Iranian naval vessels on March 10th, including 16 mine layers near the Strait of Hormuz.

- Air defenses shoot down a drone targeting a US military base near Erbil Airport in Iraqi Kurdistan.

- Israeli army announces massive wave of raids on Tehran, targeting Iranian regime infrastructure.

- UAE Defence Ministry reported air defences are currently intercepting missiles and drones from Iran.

- Israel rejects Lebanon's request for a halt in fighting to allow for talks, according to FT.

- UKMTO said it has received a report of an incident 50NM north-west of Dubai, with a bulk carrier hit by an unknown projectile.

RUSSIA-UKRAINE

- Russia's Kremlin said Istanbul is an possible location for talks next week but there is no specific clarity yet.

OTHERS

- North Korea conducted strategic cruise missile tests on Tuesday for a naval destroyer, while Leader Kim said destroyers must be equipped with supersonic weapons, according to KCNA.

CRYPTO

- Bitcoin returns below USD 70k while Ethereum continues to trade above USD 2k.

APAC TRADE

- APAC stocks traded higher as the recent easing of oil prices helped the region shrug off the lacklustre lead from Wall Street and reports of Iran beginning to lay mines in the Strait of Hormuz.

- ASX 200 gained with strength in mining, resources, materials and financials, front-running the advances, but with upside capped amid increased bets for the RBA to hike rates at next week's meeting following recent central bank rhetoric and calls by some of Australia's largest banks for consecutive rate increases in March and May.

- Nikkei 225 rallied following the recent easing of oil price pressures and as softer-than-expected PPI data, which showed a surprise monthly deflation, supports the case for a delay in BoJ policy normalisation.

- Hang Seng and Shanghai Comp lagged amid quiet catalysts and with Chinese officials said to be frustrated by what they see as insufficient US preparation for the Trump-Xi summit later this month, while China also moved to curb the use of OpenClaw AI by banks and state agencies.

NOTABLE ASIA-PAC HEADLINES

- Japan's government is considering measures amid Middle East tensions and will announce gas and utility price measures at an appropriate time, according to Nikkei.

NOTABLE APAC DATA RECAP

- Japanese PPI MoM (Feb) M/M -0.1% vs. Exp. 0.1% (Prev. 0.2%, Low. -0.2%, High. 0.4%).

- Japanese PPI YoY (Feb) Y/Y 2.0% vs. Exp. 2.1% (Prev. 2.3%, Low. 1.9%, High. 2.5%).

Loading...