Indian tanker moves out the strait; DXY breaches 100 ahead of busy data schedule - Newsquawk US Market Open

- US has issued a new Russia-related general license permitting the sale of Russian crude oil and petroleum products loaded on vessels as of March 12.

- ByteDance reportedly plans to tap NVIDIA (NVDA) Blackwell processors that are barred for export to China, with the Co. working with Aolani Cloud on plans to use some 500 Blackwell computing systems in Malaysia, according to WSJ.

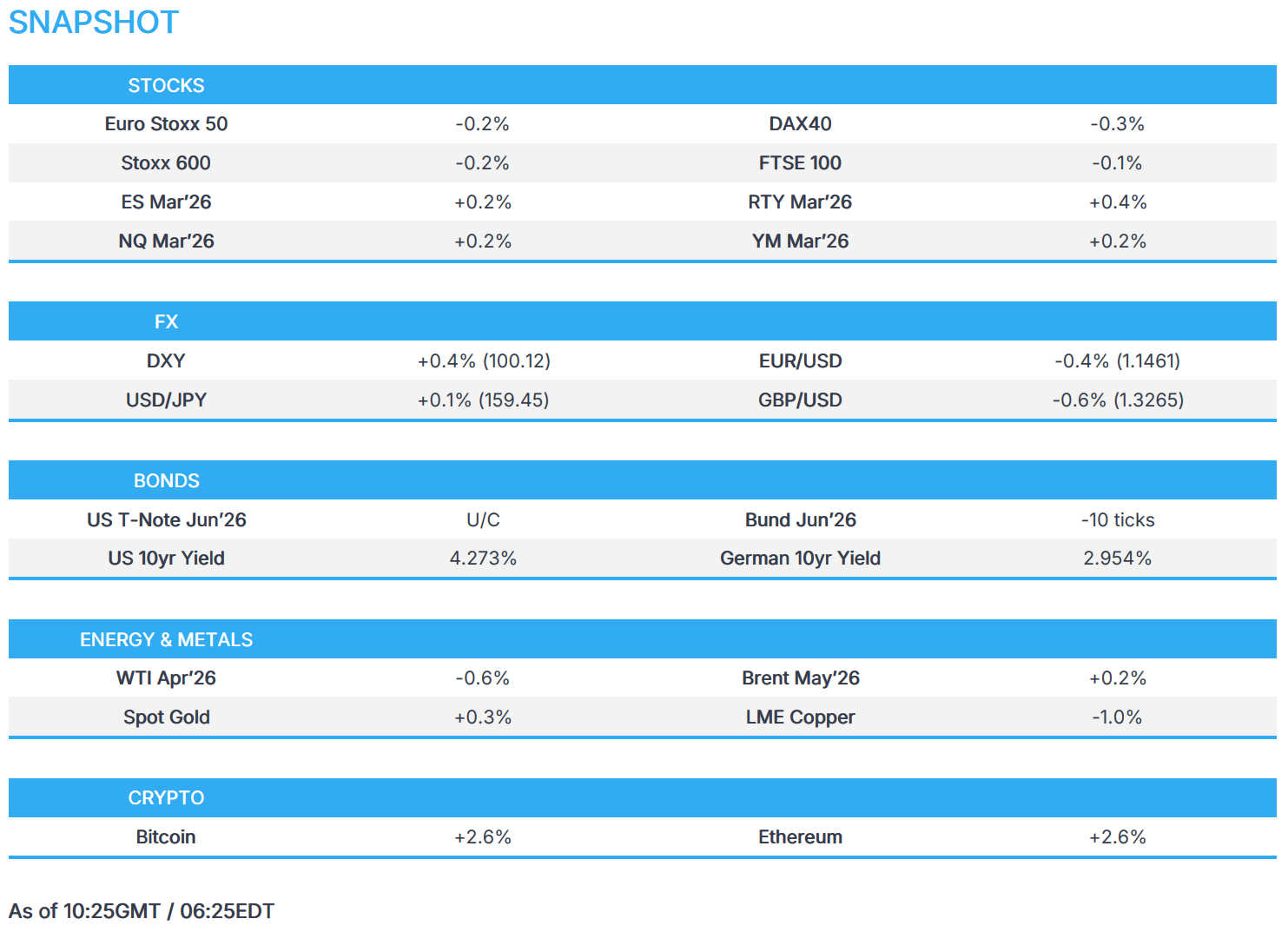

- European equities soften, BESI NA surges on takeover rumours; US equity futures muted ahead of PCE, GDP.

- DXY extends above the 100 handle, GBP slips post-GDP.

- Fixed income choppy and energy prices and risk tone continue to dictate price action.

- Brent hovers around USD 100/bbl and metals dragged by a firmer dollar.

- Looking ahead, highlights include Canadian Jobs Report (Feb), US Core PCE Price Index (Jan), Durable Goods Orders (Jan), Personal Spending (Jan), JOLTS (Jan), University of Michigan Consumer Sentiment Prelim. (Mar), Atlanta Fed GDP. Rating updates include Scope Ratings on UK & Spain, S&P on Spain, Moody's on Greece & Germany, Fitch on Spain & Italy.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.2%) continue to trade on the softer side as energy prices remain at elevated levels. Once again, the IBEX 35 (-0.2%) is the worst performer as Banks continue to weigh on the index. The FTSE 100 (-0.1%) is also under modest pressure, after the UK showed no growth M/M in January.

- European sectors are mixed, with Energy (+0.8%) outperforming as Brent holds above USD 100/bbl. Basic Resources (-1.2%) lags as the stronger dollar weighs on metals prices. Consumer Products and Services (-1.4%) and Banks (-0.7%) are also underperforming as higher inflation expectations and poor growth prospects weigh on the sectors. For the semiconductor space, BE Semiconductor has reportedly been fielding takeover interests and has refused to respond to the rumour.

- US equity futures (ES U/C, NQ/RTY -0.1%) are muted ahead of a flurry of US data later in the day. BofA's weekly flow showed inflows returning into US equities, with the bank also offering a trading view to fade the S&P 500 below 6600 as it should provoke a policy response.

- Samsung Electronics (005930 KS) accelerates next-generation NAND development with NVIDIA (NVDA).

- ByteDance reportedly plans to tap NVIDIA (NVDA) Blackwell processors that are barred for export to China, with the Co. working with Aolani Cloud on plans to use some 500 Blackwell computing systems in Malaysia, according to WSJ.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is stronger this morning and currently just off best levels, within a 99.58-100.29 range; upside today lacked a fresh fundamental driver, but came alongside the strength in crude prices, where Brent once again topped USD 100/bbl. Interestingly, the USD-Brent correlation is currently 0.91. On the oil situation, the US issued a new Russia-related general licence permitting the sale of Russian crude oil – this only applies to oil in transit. A waiver which did little to cull the upside in the oil complex, given this does not nearly replace the lost supply from the Gulf. ING writes that “we cannot see investors wanting to fight this dollar rally, given there is so little certainty as to when this crisis will end”. Focus now turns to Core PCE Price Index (Jan), Durable Goods Orders (Jan), Personal Spending (Jan), JOLTS (Jan), University of Michigan Consumer Sentiment Prelim. (Mar) and Atlanta Fed GDP.

- EUR has now sunk below the 1.1500 mark, and made a trough at 1.1433 – levels not seen since early August, where the single currency made a low at 1.1391 (1 Aug). Ultimately, the region's status as a net-importer of oil continues to weigh on the single currency. In the meantime, focus will be on any hints of government intervention to ease the impact of higher energy costs, before focus then turns to the ECB next week, where the Bank is likely to raise concerns about the Middle East situation, with an outside chance that it signals possible policy adjustments.

- GBP also remains pressured alongside peers. Sterling opened lower, given the USD strength, but then reacted negatively to the region’s GDP metrics, which showed that the UK stagnated in January, even before the Iran war started. Cable fell from 1.3315 to 1.3306 within a couple of minutes, before trundling lower as the USD strength picked up. The impact on the BoE following this data will likely not be impactful on policy in the near term, given the Iran war.

- JPY remains the only G10 flat vs USD. Potentially a function of traders seeing the possibility of near-term intervention/rate checks as USD/JPY sits firmly in the intervention zone, beyond 158.00. Overnight, Finance Minister Katayama said that they are in closer contact with US authorities on FX, and separately commented that they are prepared to take all necessary steps on FX. As a reminder, the NY Fed conducted a rate check on USD/JPY back in January. As mentioned previously, intervention seems unlikely given a) it would prove to be ineffective given the current geopolitical environment, b) low volume short positions on the JPY, c) the move is fundamentally driven by higher energy prices, and d) the recent lack of verbal intervention suggests potentially a higher bar for USD/JPY to rise. Nonetheless, markets will be cognizant of any jawboning heading into the BoJ meeting and wage negotiations next week.

FIXED INCOME

- A choppy start to the day with benchmarks in narrower ranges than usual, though still posting a c. 50 ticks band for Bunds, for instance. Action this morning has largely been a function of energy and, by extension, the general risk tone. A grind higher in the first few hours in energy benchmarks to a USD 98.09/bbl peak for WTI sparked a bout of fixed downside, equity pressure and USD strength.

- However, the move in fixed income has pared with benchmarks marginally firmer as energy wanes from best. The main headline update amidst this was Axios reporting that US President Trump told the G7 on Wednesday that Iran was close to surrender; however, commentary from the new Supreme Leader on Thursday and Iran announcing a fresh wave of attacks today somewhat disputes that assessment.

- Specifically, USTs in a 111-12 to 111-20 band, currently firmer by a tick or two in that. Nonetheless, the benchmark is set to end the week lower by around a full point.

- For Bunds, they are yet to make a lasting move into the green, despite hitting a 126.18 peak with gains of two ticks briefly. Drivers much the same as above. Furthermore, the benchmark is also set to end the week lower by around a full point.

- Finally, Gilts opened lower by just under 20 ticks today before slipping to a 88.49 low and then rebounding to near-enough unchanged. Downside a function of the benchmark catching up to post-close action and the morning's initial energy move. However, this was somewhat offset by the morning's data showing the UK started the year with no growth. A series that may have otherwise cemented a March cut by the BoE. However, the recent Middle East related energy disruption and associated moves mean a near-term cut is entirely off the table, though the MPC will likely remain divided next week in another split decision.

- Japan sold JPY 300bln in 10yr Climate Transition Bonds b/c 3.42 (Prev. 3.56).

COMMODITIES

- WTI and Brent futures are off their best and worst levels at the time of writing, with traders gearing up for another week of geopolitical risks as the war shows no signs of abating. It was reported that the US issued a second short-term waiver allowing buyers to receive Russian oil already at sea, expanding a previous India-only authorisation without materially benefiting the Russian government. Modest downticks were seen in the complex following an Axios report that US President Trump told G7 leaders in a virtual meeting Wednesday that Iran is "about to surrender," according to three officials from G7 countries briefed on the contents of the call, although the report caveats that 24 hours later after that call, Iran's new supreme leader issued his first public statement vowing to keep fighting. WTI resides in a USD 94.52-98.09/bbl range and Brent in a 99.51-102.75/bbl range. Nat Gas prices are flat at the time of writing, but remain above EUR 50/MWh amid the ongoing energy woes emerging from the Iranian crisis.

- Spot gold rose above USD 5,100/oz overnight and hovers on either side of the figure in recent trade, but still remains on track for a second weekly decline, as the Middle East conflict keeps oil near USD 100/bbl and in turn pushes up the USD (DXY north of 100) amid inflationary woes. Spot gold resides in a USD 5,061.32-5,128.47/oz. Spot silver resides closer to weekly lows after finding resistance at USD 90/oz on Tuesday.

- In terms of base metals, 3M LME copper is on a softer footing amid the firmer USD and with sentiment also dampened as the US opened a Section 301 probe into forced-labour practices across 60 economies, including the EU, China, Japan, South Korea, Canada, Mexico, India, Taiwan and the UK. Iron is set for its biggest weekly gain in more than a year after China state-backed buyers expanded restrictions on BHP Group (BHP AT) products.

- India asks Iran to allow tankers through the Strait of Hormuz, according to the WSJ; India is in active talks to allow 23 tankers through the Strait, with first crossing expected this weekend

- Kremlin envoy Dmitriev said US sanctions waiver affects around 100mln barrels of Russian oil.

- US has issued a new Russia-related general license permitting the sale of Russian crude oil and petroleum products loaded on vessels as of March 12, according to the Treasury website. US license permits sale of such Russian crude oil and petroleum products until 12:01 AM EDT on April 11th.

- US Treasury Secretary Bessent clarified that new general licence applies only to Russian oil already in transit and will not provide significant financial benefit to the Russian government.

- EU Commission said gas storage filling levels in the EU remain stable and oil stocks are at a high level, via statement; gas storage should not be refilled at all costs.

- Japan's Defence Minister Koizumi said it would be possible to provide escort for Japanese ships through Hormuz, however PM Takaichi clarified that no decisions have been made.

- Saudi Aramco offers to sell 2 mln barrels of Arab Light crude for March loading at Yanbu port.

- Australia's energy minister announces lowering minimum stock obligations for diesel and fuel. said: To address fuel supply chain disruption by reducing up to 20% of the baseline minimum stockholding obligation for petrol and diesel, which would allow the release of up to 762mln litre of petrol and diesel from Australia's domestic reserves.

- Venezuela and Repsol (REP SM) signed strategic agreements, while Venezuela's interim president Rodriguez said that the deal can make Venezuela a gas exporter.

- Rio Tinto (RIO AT) suspends all mining operations at its Kennecott copper facility following a fatal incident.

- Goldman Sachs expects Brent crude prices to average over USD 100/bbl in March and USD 85/bbl in April, while it sees Brent crude gradually easing back to the low USD 70s late in the year.

TRADE/TARIFFS

- USTR confirms to start 60 Section 301 investigations related to failures to take action on forced labour.

- China's MOFCOM said US 301 tariffs violate WTO rules, urges the US to correct wrong practices and return to dialogue. China is analysing and assessing the situation. Will take necessary measures to safeguard legitimate rights and interests.

- China's MOFCOM is to impose tariffs of up to 30.1% on imports of rubber from Japan and Canada, effective March 14th.

- US ambassador to India said they're moving to a critical stage of finalising critical minerals agreement, adds expect countries we have made deals with to honor those deals.

NOTABLE EUROPEAN DATA RECAP

- UK GDP YoY (Jan) Y/Y 0.8% vs. Exp. 0.9% (Prev. 0.7%, Low. 0.8%, High. 1.0%).

- UK GDP MoM (Jan) M/M 0.0% vs. Exp. 0.2% (Prev. 0.1%, Low. 0.1%, High. 0.3%).

- UK Balance of Trade (Jan) 3.922B vs. Exp. -6.2B (Prev. -4.340B).

- UK Goods Trade Balance (Jan) -14.45B vs. Exp. -22.2B (Prev. -22.72B, Low. -23.3B, High. -21.2B).

- Spanish Inflation Rate YoY Final (Feb) Y/Y 2.3% vs. Exp. 2.3% (Prev. 2.3%).

- Spanish Core Inflation Rate YoY Final (Feb) Y/Y 2.7% vs. Exp. 2.7% (Prev. 2.6%).

- Spanish Inflation Rate MoM Final (Feb) M/M 0.4% vs. Exp. 0.4% (Prev. -0.4%).

- French Inflation Rate YoY Final (Feb) Y/Y 0.90% vs. Exp. 1% (Prev. 0.3%).

- French Inflation Rate MoM Final (Feb) M/M 0.6% vs. Exp. 0.7% (Prev. -0.3%).

- EU Industrial Production MoM (Jan) M/M -1.5% vs. Exp. 0.5% (Prev. -1.4%, Low. -0.8%, High. 1.0%).

- German Wholesale Prices MoM (Feb) M/M 0.6% vs. Exp. 0.4% (Prev. 0.9%).

- German Wholesale Prices YoY (Feb) Y/Y 1.2% vs. Exp. 1.0% (Prev. 1.2%).

- Polish Inflation Rate MoM (Feb) M/M 0.3% vs. Exp. 0.6% (Prev. 0.6%).

- Polish Inflation Rate YoY (Feb) Y/Y 2.1% (Prev. 2.2%).

CENTRAL BANKS

- US Treasury Secretary Bessent said the Fed is a long way from returning to quantitative easing.

NOTABLE US HEADLINES

- US Secretary of State Rubio will join US President Trump during his trip to China later this month.

- US Treasury Secretary Bessent said Trump-Starmer relationship will get back on track.

GEOPOLITICS

MIDDLE EAST

- NATO intercepts an Iranian missile targeting Turkey, the 3rd occasion since the Middle East conflict began. Missile was launched from Iran and destroyed by defences in the eastern Mediterranean.

- US President Trump told G7 leaders in a virtual meeting Wednesday that Iran is "about to surrender," according to three officials from G7 countries briefed on the contents of the call, Axios reported.

- US has burned through ‘years’ of munitions since the Iran war began, while the rapid depletion of stockpile including Tomahawk missiles raises pressure on US President Trump regarding the cost of the war, according to FT.

- US officials say Iran has begun laying mines in the Strait of Hormuz as of today, according to NYT.

- US Treasury Secretary Bessent said we know that Iran has not mined the Strait of Hormuz, noted a lower oil price regime over the medium-term after the conflict.

- US weapons package for Taiwan could be approved after US President Trump's China trip, according to sources.

- Israeli Security Official said that Iran has around 150 missile launch platforms, these will continue to be targeted.

- Israeli army said it has begun a wave of air strikes targeting government infrastructure in Iran’s capital, Tehran, Al Jazeera reported.

- Israeli air strikes are underway in Iran and explosions were reported in Tehran.

- Israel's army identified missiles launched from Iran and defence systems were activated to counter threat.

- Israel conducts a series of raids on southern suburbs of Beirut.

- Israeli army issues orders to evacuate areas in the southern suburbs of Beirut, Sky News Arabia reported.

- Iran announces a fresh wave of attacks on US bases and Israel, ISNA reported.

- "Iranian state television reported a large explosion in a Tehran square where demonstrations are happening", via AP's Gambrell.

- Iranian missile successfully hits target after Israeli interceptors failed to stop it.

- Iran claims responsibility for shooting down US refueling plane, said US refueling plane was downed with all crew killed in Western Iraq, according to Tasnim.

OTHERS

- Afghan government said Pakistan conducts strikes on Kabul and other areas in Afghanistan.

- North Korea accused Japan of pushing the region into danger for its long-range missile deployments and claims Japan's military buildup is part of preparations for a reinvasion, according to KCNA.

CRYPTO

- Bitcoin extends above USD 70k while Etherum extends above USD 2.1k.

APAC TRADE

- APAC stocks were mostly subdued with the region cautious amid headwinds from the recent double-digit surge in oil prices after Iran's new Supreme Leader dug in and called for a continued closure of the Strait of Hormuz, as well as warned that other fronts will be opened if the war persists, while the US also initiated 60 Section 301 investigations related to failures to take action on forced labour.

- ASX 200 traded indecisively as strength in financials and energy offset the losses in mining and materials.

- Nikkei 225 underperformed as oil and inflationary-related pressures weighed on the large exporting industries, including tech and autos, with Honda among the worst hit after it cancelled three planned EV launches in North America and revised its FY25/26 outlook to a loss of as much as JPY 690bln from the previous guidance of JPY 300bln profit.

- Hang Seng and Shanghai Comp were lacklustre in rangebound trade with a lack of conviction heading into talks between US Treasury Secretary Bessent, USTR Greer and Chinese Vice Premier He Lifeng in Paris beginning on Sunday.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama said prepared to take all necessary steps on FX and are in closer contact with US authorities on FX.

- South Korea could reportedly see KRW 20tln extra budget on chip boom, according to Chosun.

NOTABLE APAC DATA RECAP

- China February YTD Aggregate Financing (CNY) 9.6tln (exp. 9.245tln); New Yuan Loans 5.61tln (exp. 5.576tln); M2 Money Supply 9% Y/Y (exp. 8.9%).

- Chinese New Yuan Loans (Feb) 900B vs. Exp. 979B (Prev. 4710B).

- Chinese Outstanding Loan Growth YoY (Feb) Y/Y 6.0% vs. Exp. 6% (Prev. 6.1%).

- Chinese Total Social Financing (Feb) 2380B vs. Exp. 2130B (Prev. 7220B).

- Chinese M2 Money Supply YoY (Feb) Y/Y 9% vs. Exp. 8.8% (Prev. 9%).

- New Zealand Business NZ PMI (Feb) 55.0 (Prev. 55.2).

Loading...