Indices broadly lower as energy rebounds, NVIDIA a touch firmer post-earnings - Newsquawk US Market Open

- Tehran is studying the American text and has not yet submitted its response, Al Arabiya reported citing sources.

- "Pakistan’s mediation efforts between US and Iran are at a crucial stage where efforts are underway to secure an agreement or a framework for comprehensive talks which can eventually lead to a ‘deal’,"** according to journalist Mallick.

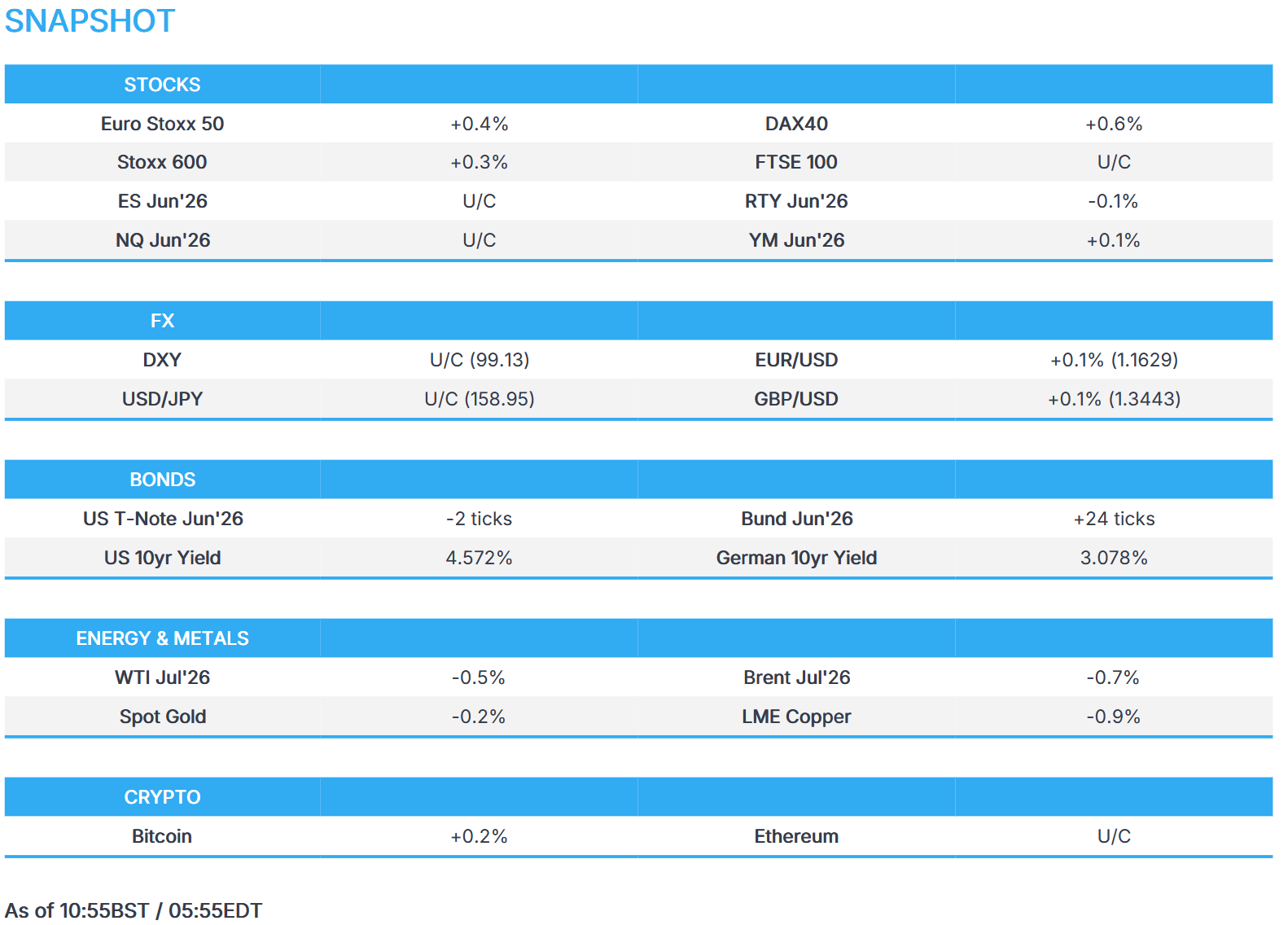

- European bourses are broadly higher despite disappointing PMIs; US equity futures are flat after NVDA sales guidance disappointed.

- DXY weighs hawkish FOMC and geopolitics; AUD lags post-jobs data.

- USTs are a little lower whilst Bunds digest Flash PMIs, which fuel stagflation woes.

- Crude wanes off highs amid further reports of diplomatic effects; Brent Jul -0.7%.

- Looking ahead, highlights include US S&P PMIs Flash (May), Initial Jobless Claims (May/16), EU Consumer Confidence Flash (May), Banxico Minutes (May). Speakers include BoE's Bailey & Taylor, ECB's Elderson, Fed's Barkin, Goolsbee. Earnings from Walmart & Deere.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- Tehran is studying the American text and has not yet submitted its response, Al Arabiya reported citing sources. Pakistan is working to bring closer the viewpoints between the US and Iran. ISNA further reported that Iran is in the process of responding to the text sent by the US and that "the sent text has reduced the gaps to some extent", but requires guarantees.

- "According to my sources in Tehran, Iran’s response hasn’t been handed to the Pakistani mediator. There’re ongoing deliberations, and serious efforts to reach a final draft," according to Al Jazeera's Hashem.

- "Pakistan’s mediation efforts between US and Iran are at a crucial stage where efforts are underway to secure an agreement or a framework for comprehensive talks which can eventually lead to a ‘deal’," according to journalist Mallick.

- Pakistani source tells Al Jazeera the Army Chief is still in Pakistan and his visit to Iran depends on the outcomes of the interior minister's visit, enriched uranium is the main sticking point in the US-Iranian negotiations.

- Pakistan's Army Chief is to travel to Tehran on Thursday for negotiations and as part of mediation efforts between the US and Iran, ISNA reported.

- Pakistani political and media circles point to accelerated mediation efforts after Pakistani Interior Minister's Tehran meetings, IRNA reported. The report adds that presenting a narrative that indicates that progress in negotiations between Tehran and Washington is likely.

- Iran's Foreign Ministry spokesperson said Iran is pursuing talks "in good faith" but views US with "deep suspicion", Press TV reported. Confirms multiple rounds of messages have been exchanged through Pakistani intermediaries based on the 14-point proposal.

- Iranian official said they are ready to use new weapons if the US makes an additional act of aggression again, while he said they have produced and advanced weapons inside the country that have not yet been used on the battlefield and have not yet been tested. Furthermore, the spokesman stated that in terms of equipment and defensive capabilities, they are not experiencing any shortages that would prevent the defence of the country, and this time, they do not intend to act with restraint.

- IRGC said forces are ready to respond to any enemy aggression and all armed forces are ready with fingers on the trigger, according to SNN and Tasnim.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) are entirely but modestly in the green, ex. FTSE 100 (-0.1%). Signs of an end to the Iran war seem to be emerging, with President Trump saying the US is in the final stages of negotiations with Iran, while Al Arabiya reported that Tehran is studying the American text. The source report added that Pakistan is working to bring closer the viewpoints between the US and Iran. Elsewhere, EZ flash PMIs disappointed, with commentary continuing to highlight stagflation worries despite ECB Lagarde’s persistence in moving away from the language.

- European sectors point to a positive bias. Autos (+1.2%) and Retail (+0.6%) top the sector pile while Energy (-0.2%) and Banks (-0.2%) underperform.

- US equity futures trade around the unchanged mark after hawkish FOMC minutes failed to spur a reaction, while NVIDIA (-0.1% pre-market) claws back after-hours losses. NVIDIA shares edged lower in extended trading, despite beating expectations and giving upbeat guidance. Some suggested the tech giant's sales guidance was disappointing, guiding Q2 sales around USD 91bln, beating estimates of USD 87bln but missing Bloomberg’s compiled upper end of USD 96bln.

- NVIDIA (NVDA) - Q1 2026 (USD): Adj. EPS 1.87 (exp. 1.75), Revenue 81.615bln (exp. 78.78bln); Q2 revenue view 89.18-92.82bln (exp. 86.79bln); Boosts buyback by USD 80bln and boosts dividend to USD 0.25/shr (prev. 0.01/shr)

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- The Dollar index is unchanged on the day and returns to Thursday’s lows around 99.00 after chopping on geopolitics and soft EZ/French data. Action ultimately dictated by geopolitics, with reports recently sounding constructive and has outweighed the Dollar positive factors which incl. poor EZ PMI metrics and hawkish FOMC Minutes.

- EUR saw decent weakness on dismal French data, which heightened the possibility of EZ-US differentials widening. French PMIs marked the steepest contraction since late 2020. Services and composite were expected to be broadly unchanged from priors, though both slipped significantly further into contraction territory. The Manufacturing picture was better, though the metric still fell into contraction. The EZ figure was also poor but provided some reprieve for the single currency. EZ Manufacturing was resilient, though still fell below expected and previous, while composite and services fell further into contraction. As the French series was released, EUR/USD saw a move c.24 pips lower to a 1.1594 trough, though pared some downside as German/EZ figures were not as bad as feared according to the indications from France.

- JPY remains reluctant to deviate from the 159.00 mark despite hawkish remarks from BoJ's Koeda. JPY fundamentals remain bearish amid reporting around the Supplementary Budget and terms of trade. Koeda’s remarks overnight, “BoJ needs to continue to raise the policy interest rate”, mark the second non-dissenting member to indicate willingness to tighten policy (Masu+Koeda). This shows that last meeting’s 6-3 vote split will be vulnerable in June’s meeting, with the aforementioned members’ remarks indicating a possible 5-4 vote split for a hike, where interest rate futures currently imply a 77% probability of such action.

FIXED INCOME

- USTs are off by a few ticks, but have been clambering off worst levels throughout the European session; currently towards the upper end of a 109-05 to 109-12 range. Wednesday saw sentiment lift amidst positive geopolitical newsflow, and this has continued into today’s session. Most recently, reports have suggested that Iran is in the process of responding to the text sent by the US, adding that it has “reduced the gaps to some extent”. This led to some pressure in the energy complex, in turn, lifting US paper.

- Bunds trade firmer today and towards the upper end of a 124.71 to 125.12 range. Strength today has been facilitated by a) geopolitical optimism (see above), and b) a dire set of PMI metrics. In brief, the French figures were awful, with Manufacturing surprisingly slipping into contractionary territory and Composite/Services also deteriorating; the German metrics also indicated the downbeat Manufacturing environment, but were more or less in line with expectations. The EZ-wide figure concluded that activity in the region is softening across both the Manufacturing and Services; "The survey data indicate that the euro area economy looks set to contract by 0.2% in the second quarter”. The report concludes by suggesting that price gauges suggest inflation is running close to 4%, which, alongside slowing growth, “creates a deepening dilemma for policymakers”.

- Gilts move higher alongside the pressure in the crude complex. The region had its own PMI metrics to digest. Manufacturing remained solid whilst Services surprisingly fell into contractionary territory. UK paper was choppy in reaction to the data, but ultimately little moved – perhaps as attention turns to Chancellor Reeves, who is due to speak at 11:30 BST. Reports suggest that she will announce targeted cuts to agrifood tariffs expected to save consumers more than GBP 150mln annually. She is also expected to announce free summer bus travel for children, and a GBP 400mln package for motorists and hauliers, including a postponed 5p fuel duty rise. Political analysts view her speech as an attempt to secure herself as the Labour Party’s long-term chancellor in the midst of recent political turmoil.

- UK sells GBP 4bln 4.875% 2036 Treasury Gilt: b/c 3.45x, average yield 5.026%, tail 0.3bps.

- France sells EUR 14bln vs exp. EUR 12-14bln 2.40% 2029, 2.75% 2030, 3.25% 2032 and 3.50% 2033 OAT.

- Spain sells EUR 6.055bln vs exp. EUR 5.5-6.5bln 2.60% 2031, 3.00% 2033 and 1.00% 2050 Bono.

COMMODITIES

- In geopolitics, US President Trump said Iran talks were in the “final stages” but warned the US could get “a little bit nasty” if no deal is reached, while stressing sanctions relief would only come after an agreement. Iran said dialogue was continuing around its 14-point proposal, but rejected surrender, ultimatums or deadlines. Tehran is studying the American text and has not yet submitted its response.

- WTI and Brent crude futures are moving lower following the aforementioned constructive geopolitical headlines. WTI Jul briefly topped USD 100/bbl before returning under the level, currently in a USD 97.29-100.11/bbl range. Brent Jul resides in a 103.68-106.80/bbl parameter. Dutch TTF is now softer by over 1%, with downticks also seen in light of the constructive US-Iran commentary.

- Spot gold is contained to a USD 4,512-4,570/oz range, on a modestly softer footing intraday but off extremes as the yellow metal moves in lockstep with the USD, which is influenced by energy prices. Spot silver found intraday resistance at USD 77/bbl before printing a USD 74.67/oz low.

- Base metals are lower despite the broader optimism from the US-Iran relatively flat DXY at the time of writing, whilst PMI data in Europe pointed to an overall bleak picture, with the data pointing to contractions in the EZ and the UK. 3M LME copper resides in a USD 13,477.65- 13,713.40/t range.

- ADNOC said that while it can ramp up its oil production in a matter of weeks, it will take 4 months for oil flows through Hormuz to return to 80% of pre-war levels.

- China raises gas and diesel prices by CNY 75 and CNY 70 per ton, respectively, from May 22nd.

- UAE's new pipeline that bypasses the Strait of Hormuz is reportedly around 50% complete.

- Goldman Sachs said global oil stockpiles fell at a record pace of 8.7mln bpd so far in May, while it added that physical markets continue to tighten with estimated oil exports through the Strait of Hormuz remaining at a very low 5% of normal.

TRADE/TARIFFS

- China's MOFCOM said the EU is using overcapacity as an excuse to concoct new trade tools against China.

NOTABLE EUROPEAN HEADLINES

- EU Commission downgrades 2026 GDP growth forecast to 0.9% (prev. 1.2%), 2026 inflation revised to 3.00% (prev. 1.9%).

- UK Chancellor Reeves is to announce cuts to food tariffs and children's bus fares on Thursday in a cost-of-living push to win back voters. It was separately reported that Reeves will not announce a proposed voluntary cap on supermarket prices for essential groceries following strong backlash from the sector, according to Financial Times. Furthermore, Politico reported that Reeves is to announce a cut to agrifood tariffs on some products and a rise in mileage rates.

NOTABLE EUROPEAN DATA RECAP

- UK S&P Global Composite PMI Flash (May) 48.5 vs. Exp. 51.6 (Prev. 52.6, Low. 50.8, High. 52.5). "The May PMI data indicate that the economy contracted at a 0.2% quarterly rate, representing a marked contrast to the robust growth seen earlier in the year," adding that things could well get worse in the coming months.

- UK S&P Global Services PMI Flash (May) 47.9 vs. Exp. 51.7 (Prev. 52.7, Low. 50.3, High. 53).

- UK S&P Global Manufacturing PMI Flash (May) 53.7 vs. Exp. 53 (Prev. 53.7, Low. 50.5, High. 54).

- EU S&P Global Composite PMI Flash (May) 47.5 vs. Exp. 48.8 (Prev. 48.8, Low. 47.5, High. 49.5). “The rise in the survey’s price gauges already hints at inflation running close to 4% in the coming months which, combined with the growing signs of the region slipping into an economic downturn, creates a deepening dilemma for policymakers."

- EU S&P Global Services PMI Flash (May) 46.4 vs. Exp. 47.7 (Prev. 47.6, Low. 45.9, High. 49).

- EU S&P Global Manufacturing PMI Flash (May) 51.4 vs. Exp. 51.8 (Prev. 52.2, Low. 50.2, High. 53).

- French S&P Global Composite PMI Flash (May) 43.5 vs. Exp. 47.7 (Prev. 47.6, Low. 46.1, High. 48.5). "The inflationary impact of the oil-price shock continues to proliferate, with price indices in both manufacturing and services moving higher once again."

- French S&P Global Services PMI Flash (May) 42.9 vs. Exp. 46.6 (Prev. 46.5, Low. 44.5, High. 47.3).

- French S&P Global Manufacturing PMI Flash (May) 48.9 vs. Exp. 52.2 (Prev. 52.8, Low. 51.3, High. 53.2).

- German S&P Global Composite PMI Flash (May) 48.6 vs. Exp. 48.4 (Prev. 48.4, Low. 47.4, High. 51.4). "...slower rises in both manufacturing and services output prices point to businesses shouldering a greater proportion of the burden. This suggests some containment of inflationary pressures, but it also hints at an increased squeeze on company margins which has consequences of its own..."

- German S&P Global Services PMI Flash (May) 47.8 vs. Exp. 47 (Prev. 46.9, Low. 44.9, High. 50.2).

- German S&P Global Manufacturing PMI Flash (May) 49.9 vs. Exp. 51 (Prev. 51.4, Low. 49.6, High. 52.5).

CENTRAL BANKS

- BoJ Board Member Koeda said the BoJ needs to continue to raise the policy interest rate in response to developments in economic activity and prices, as well as financial conditions, while she thinks the BoJ needs to continue examining the extent to which underlying inflation is anchored. Koeda said given the situation in the Middle East, she sees some possibility that underlying inflation may exceed 2% looking ahead, and noted it is reasonable for BoJ to raise the policy interest rate at an appropriate pace to address high inflation, whilst also considering the trade-offs for the economy. Furthermore, she warned that if real interest rates continue to deviate markedly in a negative direction from the natural rate of interest, unintended distortions could arise in future resource allocation, as well as stated that the BoJ should proceed steadily with normalising its balance sheet in a predictable manner, while ensuring flexibility.

- ECB's Rehn said economy is moving towards the adverse scenario of projections; may need to raise rates to maintain credibility.

- Norges Bank Expectations Survey (Q2): 12-month ahead CPI 3.3% (prev. 2.8%), 2026 real wages 1.1% (prev. 1.3%).

GEOPOLITICS

RUSSIA-UKRAINE

- Ukraine’s Drone Forces commander said Ukrainian drones attacked Russia’s Syzran oil refinery (147k-170k capacity) in the Samara region of Russia.

OTHER

- US Defence Undersecretary Colby may visit China ahead of a possible trip by Pentagon chief Hegseth amid tension over Taiwan arms sales, SCMP reported.

- US deployed the USS Nimitz carrier strike group to the Caribbean in a show of force as President Trump pressures Cuba, according to NYT.

- US President Trump said on Wednesday he would speak with Taiwan's President Lai in an unprecedented move for a US leader that could roil US relations with China, according to The Guardian.

- Beijing is reportedly holding up a proposed visit by a Pentagon top policy official as China pressures US President Trump regarding a USD 14bln arms sale to Taiwan, according to FT.

- Chinese President Xi may visit North Korea by as early as next week, according to Yonhap.

CRYPTO

- Bitcoin continued to extend higher, nearing USD 78k.

APAC TRADE

- APAC stocks mostly rallied as the region took impetus from the gains on Wall Street, with global risk sentiment underpinned following a slide in oil prices due to increased optimism regarding a resolution to the Middle East conflict, after President Trump stated that they are in the final stages of talks with Iran. Furthermore, it was also reported that the Pakistani Army Chief may visit Iran today to announce the achievement of a final draft agreement, while the US side gave Iran a text through a Pakistani mediator after having received Iran's 14-point text a few days ago.

- ASX 200 climbed higher with the gains led by outperformance in the real estate, mining and materials industries, while the index also shrugged off the weak flash PMIs and disappointing jobs data.

- Nikkei 225 surged higher amid the decline in energy prices and heavy buying in tech stocks, with SoftBank shares up around 20% following the earnings beat from NVIDIA, while there was a slew of data from Japan which were ultimately mixed, but included stronger-than-expected trade figures.

- KOSPI outperformed amid tech strength with SK Hynix surging by a double-digit percentage, while Samsung Electronics was boosted by an eleventh-hour tentative wage agreement with the labour union to avert an 18-day mass walkout.

- Hang Seng and Shanghai Comp lagged despite the increased liquidity effort by the PBoC, with price action rangebound and Chinese markets constrained amid weakness in energy stocks and automakers.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama said Japan's fiscal policy is proactive and not expansionary.

- Japan's draft extra budget is reportedly around JPY 3tln, while it was also reported that Japan plans to spend JPY 500bln in reserve funds on energy measures.

- India is said to weigh options to boost the rupee, including a rate hike, with the RBI also considering options such as currency swaps and raising dollars from overseas investors.

- South Korea's NPS may hike domestic stock holding target by 5 percentage points amid rises in domestic stock market, Maeil reported.

NOTABLE APAC DATA RECAP

- Japanese S&P Global Composite PMI Flash (May) 51.10 vs. Exp. 51.8 (Prev. 52.2).

- Japanese S&P Global Manufacturing PMI Flash (May) 54.5 vs. Exp. 54.5 (Prev. 55.1).

- Japanese S&P Global Services PMI Flash (May) 50.0 vs. Exp. 50.7 (Prev. 51.0).

- Japanese Balance of Trade (Apr) 301.9B vs. Exp. -29.7B (Prev. 667B).

- Japanese Exports YY (Apr) 14.8% vs. Exp. 9.3% (Prev. 11.7%, Low. 7.0%, High. 12.5%).

- Japanese Imports YY (Apr) 9.7% vs. Exp. 8.3% (Prev. 10.9%, Low. 5.1%, High. 10.1%).

- Australian Employment Change (Apr) -18.6K vs. Exp. 17.5K (Prev. 17.9K, Low. 10K, High. 25K).

- Australian Unemployment Rate (Apr) 4.5% vs. Exp. 4.3% (Prev. 4.3%, Low. 4.2%, High. 4.4%).

- Australian S&P Global Composite PMI Flash (May) 47.80 vs. Exp. 50 (Prev. 50.40).

- Australian S&P Global Manufacturing PMI Flash (May) 50.2 vs. Exp. 50.6 (Prev. 51.3).

- Australian S&P Global Services PMI Flash (May) 47.7 vs. Exp. 49.9 (Prev. 50.7).

- New Zealand Balance of Trade (Apr) 1920B vs. Exp. 0.842B (Prev. 0.698B).

Loading...