Iran calls US demands "excessive"; Brent tops USD 109/bbl while US equities rebounds - Newsquawk US Market Open

- Iranian Foreign Ministry spokesperson said Iran has not had any direct negotiations with the US and that the US demands were excessive. The spokesperson added that Iran did not participate in the Pakistan meeting.

- Yemen’s Houthis fired missiles at Israel on Saturday morning, marking the first time it has been involved in the war; Israeli PM Netanyahu ordered the military to expand its invasion of southern Lebanon.

- US President Trump said the US could take oil in Iran and could take Kharg Island 'very easily', according to FT.

- Crude prices trade above USD 100/bbl amid geopolitical weekend escalation.

- Global equities rebound despite a lack of US-Iran de-escalation, miners benefit from surging aluminium prices.

- DXY choppy, USD/JPY rose above 160.00 before slipping on hawkish BoJ SOO and jawboning.

- Fixed income firmer despite energy being in the green, though off best.

- Looking ahead, highlights include German Inflation Prelim. (Mar), US Dallas Fed Manufacturing Index (Mar), Comments from Fed's Powell, Williams and President Trump.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

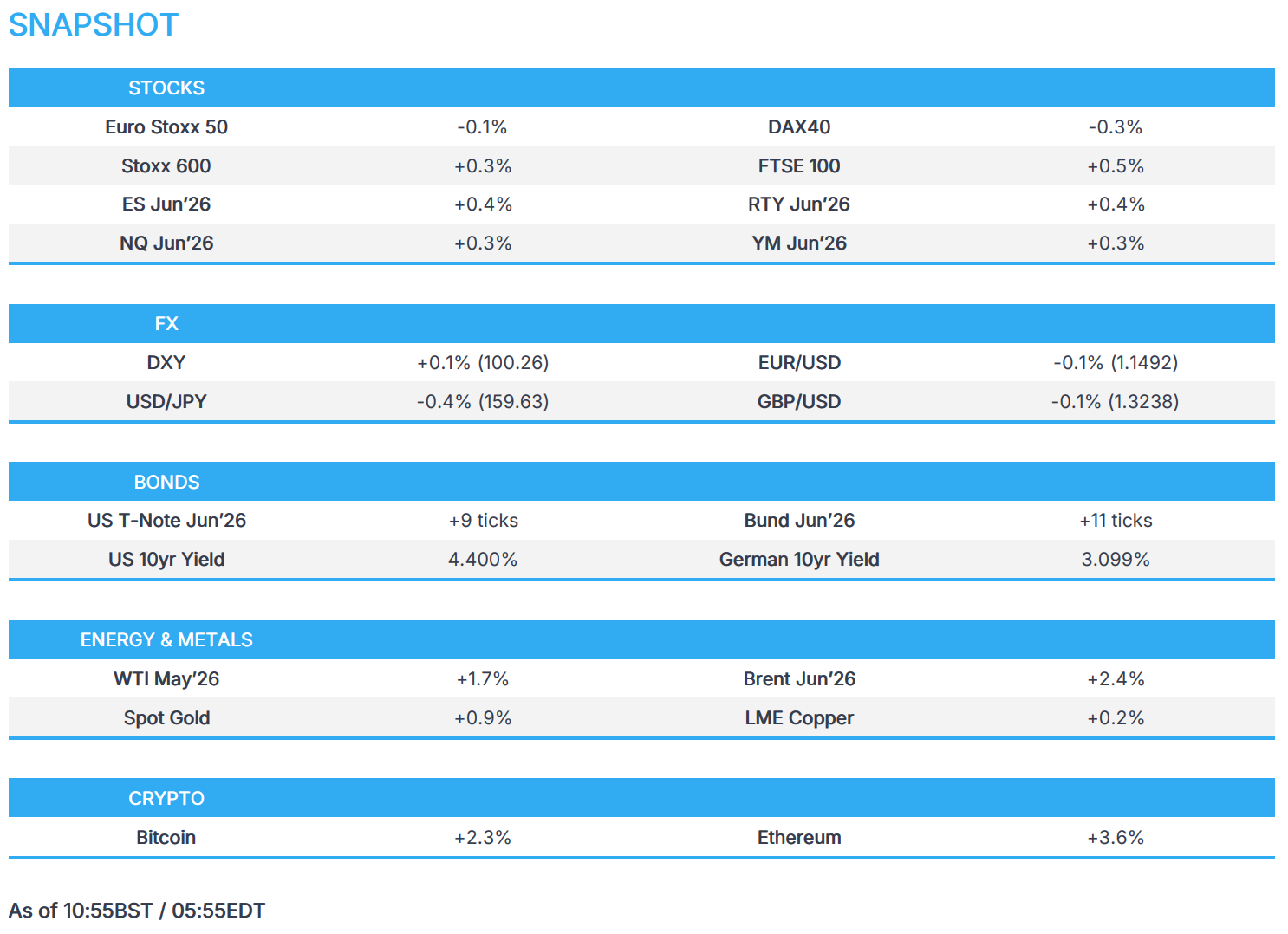

- European bourses (STOXX 600 +0.3%) are mixed, rebounding from losses seen pre-cash open. The FTSE 100 outperforms, helped by gains in miners as aluminium surged following attacks on producing plants in the Middle East. On the other hand, the DAX 40 remains the laggard. Complex is off best levels after the Iranian Foreign Ministry denied direct negotiations with the US, which slightly hit sentiment.

- European sectors are mixed. Basic Resources and Utilities top the sector pile, while Travel and Leisure and Banks underperform.

- US equity futures are modestly higher, rebounding from 5 straight weeks of losses. In terms of multi-asset allocation, Morgan Stanley downgraded global equities (more specifically, US and Japan) to equal weight from overweight, while upgrading USTs and cash to overweight from equal weight. Despite the downgrade, MS still maintains a preference for US equities given the higher EPS growth.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is currently trading within a 100.05-100.34 range, with very mild gains, as the geopolitical situation continues to keep the Dollar stronger. Near-term upside could see the index retest the Monday 16 high at 100.48. The geopolitical situation remains tense, with the weekend events seemingly showing no signs of near-term peace. The Iran-backed Houthis entered the war for the first time, whilst President Trump suggested that the US could take Kharg Island “very easily”. Most recently, an Iranian Foreign Ministry spokesperson says Iran has not had any direct negotiations with America, adding that they did not partake in Pakistan-led meetings. Now attention turns to Fed Chair Powell later.

- Given the USD strength, G10s are weaker across the board (ex-JPY). The Antipodeans lag, given the risk-tone and after the PBoC set a weaker yuan fix. The EUR slipped below the 1.1500 soon after the European cash open, and was ultimately little moved to the release of several German State CPI metrics, whereby key areas such as Bavaria and North Rhine Westphalia rose more than what is expected for the Nationwide figure, due at 13:00 BST. As it stands, EUR/USD holds towards the lower end of a 1.1487-1.1521 range.

- JPY remains the only currency firmer against the USD this morning. Initially USD/JPY broke above the 160.00 mark (peak 160.46), before reversing back below the mark following hawkish BoJ SOO and continued verbal intervention from Japanese officials. One suggested that they are watching market moves with an “extremely high sense of urgency”.

FIXED INCOME

- Despite crude still being firmer, fixed income has managed to benefit from crude easing off best levels, with both energy and debt benchmarks in the green, departing from the recent inverse correlation. Worth noting that a recent denial of US-Iran talks via the Iranian Foreign Ministry, has led to some mild pressure in the fixed income complex.

- USTs gains. Hit a 110-04 trough, lower by two ticks at worst. Since, USTs have rebounded to a 110-17+ peak. Ahead, the docket is headlined by Fed Chair Powell, who is scheduled to speak at Harvard University. Commentary that will be scrutinised for which side of the dual-mandate the Fed is currently most concerned about, and any hints as to whether action should be expected in the near-term.

- Bunds hit a 124.48 low early doors, matching Friday's close. Since, the benchmark has been gradually but notably making its way higher, to a 124.88 peak with gains of 40 ticks at best. Though, a short-lived bout of pressure was seen as German State CPIs lifted from the prior, as indicated by mainland consensus; figures due at 13:00BST. More recently, no move to a jump in consumer and selling price expectations.

- As is typically the case, Gilts are directionally following peers, but magnitudes are slightly larger. To an 87.60 peak with gains of nearly 50 ticks at best. Specifics for the UK light, awaiting to see what action the government and/or BoE may take to deal with the energy shock.

COMMODITIES

- WTI and Brent are stronger this morning. Over the weekend, the Houthis launched their first attacks on Israel since the war began, marking an expansion in the war, while strikes were reported across the region over the weekend. Trump said talks with Iran were progressing, though he also floated seizing Kharg Island, according to the FT.

- Most recently, an Iranian Foreign Ministry spokesperson says Iran has not had any direct negotiations with America, adding that they did not partake in Pakistan-led meetings. This spurred some modest strength in crude benchmarks at the time. Brent Jun’26 currently towards the upper end of a USD 106.33-109.46/bbl range.

- Spot gold prices are firmer despite a resilient dollar, possibly with some haven appeal returning to the yellow metal and as no signs of an imminent wind down can be seen. Spot gold trades in a USD 4,420-4,550/oz range at the time of writing vs Friday’s USD 4,555/oz peak.

- Elsewhere in metals, aluminium rose after Iran struck two production sites in the Middle East, with LME aluminium outpacing peers. Peers, however, are lifted in tandem despite the resilient USD and cautious sentiment across markets. 3M LME copper resides in a USD 12,019.00- 12,259.88/t range at the time of writing.

- EU Energy Ministers are to discuss on Tuesday, the coordination of the EU response on energy to the Middle East situation; said energy supply remains relatively protected at this stage. EU needs to take measures to address high energy prices, whilst maintaining functioning of EU electricity market. EU faces no immediate supply shortages, but tightening in diesel and jet fuel market.

- A Russian tanker carrying a humanitarian shipment of 100k tonnes of crude oil has arrived in Cuba, IFX reported.

- Two China-linked ships, owned by Cosco Shipping (601919 CN), appear to attempt to cross the Strait of Hormuz.

- SocGen sees a growing likelihood of Brent topping USD 150/bbl amid the Iran war; said Brent may average USD 125/bbl in April amid the Middle East situation.

NOTABLE EUROPEAN DATA RECAP

- German North Rhine Westphalia CPI MoM (Mar) M/M 1.2% (Prev. 0.2%).

- German North Rhine Westphalia CPI YoY (Mar) Y/Y 2.7% (Prev. 1.8%).

- EU Consumer Inflation Expectations (Mar) 43.4 (Prev. 25.8)

- EU Consumer Confidence Final (Mar) -16.3 vs. Exp. -16.3 (Prev. -12.2)

- Spanish Retail Sales YoY (Feb) Y/Y 2.2% vs. Exp. 3.8% (Prev. 4%).

- Spanish Retail Sales MoM (Feb) M/M -0.1% (Prev. 0.1%).

- Swiss KOF Leading Indicators (Mar) 96.1 vs. Exp. 102 (Prev. 104.2).

CENTRAL BANKS

- BoJ Governor Ueda said BoJ will guide policy appropriately by scrutinising how FX moves could affect the likelihood of achieving growth and price forecasts as well as risks. FX is a factor that makes big impacts on the economy and prices, adds will be closely monitoring the FX market.

- BoJ Summary of Opinions from March meeting stated that a member said it is appropriate to continue raising interest rates if the economic and price forecasts materialise. Conditions remain accommodative even after rate hikes. Member said the BoJ can keep rates steady for now due to Middle East uncertainty. Need to monitor Middle East developments and wages for rate decisions. Member said future rate hike timing depends on Middle East impact, as well as wages, inflation and financial conditions.

- BoJ said that if recent price rises in food prices were to persist, they could exert a sustained upward impact on overall consumer prices. Increases in energy can affect underlying inflation in both directions. Need to pay attention to the possibility that upward price pressures from rising crude may have strengthened as firms become more proactive in hiking prices and wages. Given changes in firms' price-setting behaviour, prices may now be more susceptible to JPY depreciation.

- ECB's Stournaras said a longer conflict could mean that the baseline no longer holds.

- ECB's Lane said there will be no paralysis on potential rate moves, nor any kind of pre-emption; said this is not a like-for-like situation to 2022.

- ECB's Villeroy said ECB is ready to act, but too early to discuss dates for possible rate hikes. Some over-interpretation on markets recently. Sees no risk of banking crisis in Europe.

- Westpac now sees the RBA terminal rate at 4.85%, versus the previous 4.10% view.

- Nomura expects the US Fed to deliver 25bp rate cuts in September and December, compared to previous forecasts of June and September.

NOTABLE US HEADLINES

- US President Trump will participate in a policy meeting on Monday at 13:30EDT/18:30BST and will participate in 'Signing Time' at 16:00EDT/21:00BST.

- US Treasury is to meet with domestic and international insurance regulators in coming weeks to discuss recent developments in private credit markets.

GEOPOLITICS

MIDDLE EAST

- Iranian Foreign Ministry spokesperson says Iran has not had any direct negotiations with America. "What has been discussed are the messages we received through intermediaries that the US wants to negotiate.", Tasnim reports. The materials that were conveyed to us were excessive and unreasonable requests. The meetings held by Pakistan are a framework that they established and we did not participate.

- US President Trump said the US could take oil in Iran and could take Kharg Island 'very easily', according to FT. Trump also stated that indirect talks with emissaries are progressing well and a deal could be made fairly quickly.

- US President Trump said there were good negotiations with Iran on Sunday, and the US destroyed many targets that day, while they are negotiating directly and indirectly with Iran. Trump said regarding Hormuz that Iran gave them 20 boats of oil to pass through, and he thinks they will make a deal pretty soon, but also said it's possible that they won't. Trump said Iran responded to the 15-point plan and agreed to most points but provided no further details when asked if Iran had responded. He also claimed that Middle East countries are fighting back against Iran.

- US President Trump reportedly weighs a military operation to extract Iran's uranium, although the President hasn't made a decision on the operation, according to US officials cited by WSJ.

- US President Trump claimed Middle East countries are fighting back against Iran.

- Yemen’s Houthis fired missiles at Israel on Saturday morning, marking the first time it has been involved in the war. Houthis said they will continue operations until strikes on Iran and its proxy military groups, such as Hezbollah, stop.

- Iranian Parliament's National Security member Borujerdi said the time has come for Iran to withdraw from the Nuclear Non-Proliferation Treaty and the permanent monitoring of the Strait of Hormuz, IRNA reported. According to the plan prepared by the Islamic Council and will be approved as soon as possible, a new system will rule the Strait of Hormuz and traffic will not be possible without the permission of the Islamic Republic of Iran.

- Iran's acting Defence Minister told the Turkish counterpart that Tehran will continue to punish aggressors, create deterrence and ensure war will not repeat itself, via IRNA.

- In meetings between the commander of the US Central Command in Israel, with the Chief of Staff and senior IDF officials, "the path forward was planned and outlined - for the continuation of the operation.", i24News sources say. "According to the source, the visit was "successful, and the successes so far in the war were also summarized.".

- Tehran has agreed to UN's request for safe passage of ships carrying humanitarian aid through Strait of Hormuz, according to IRNA.

- The start of firing a new wave of Iranian missiles towards Israel; reported of missiles from Lebanon to Israel also reported.

- Local accounts report at least 20 explosions near the oil refinery and petrochemical complex in Abadan, Iran.

- Iranian petrochemical facility was targeted in northwestern Tabriz, Iran according to state media. The fire in Iran's Tabris Petrochem was extinguished.

- Iraq's Defence Ministry said the Mohamad Alaa air base was attacked by a rocket. An aircraft was destroyed but no injuries reported; Iraq said "We will not hesitate to pursue anyone who dares to harm Iraq's security and sovereignty".

- Iranian attack on one service building in a power and water desalination plant in Kuwait caused serious damage.

- Media sources report simultaneous explosions and attacks on American positions in several countries, including Bahrain, Saudi Arabia, UAE, Kuwait, and Iraq, according to ISNA.

- Successive explosions in American facilities in Kuwait, SNN reported. "According to some sources, the explosions in Kuwait were so formidable and powerful that their sound was clearly heard in the border areas of Iraq.".

- Explosions and plumes of smoke rising at the American Victory Base in Iraq's capital of Baghdad.

RUSSIA-UKRAINE

- Ukrainian President Zelensky says Ukraine is ready for a potential Easter ceasefire with Russia, believes there is no deadlock in talks and that Ukraine has received signals from allies on scaling back strikes on Russia's oil sector.

OTHERS

- US President Trump said Cuba is going to be next and within a short period of time, Cuba is going to fail.

- Chinese President Xi invites Taiwan opposition leader for first visit to the mainland in a decade.

CRYPTO

- Bitcoin rebounds from 4 days of losses, currently trading back above USD 67k.

APAC TRADE

- APAC stocks were pressured following the geopolitical escalation over the weekend, in which Yemeni Houthis launched missiles towards Israel to enter the conflict for the first time, while the US and Israel also conducted strikes on Iran's largest steel plants and some energy-related facilities. Furthermore, there were some mixed comments from US President Trump, who said the US could take oil in Iran and could take Kharg Island 'very easily', but also stated that they had good negotiations with Iran and claimed Iran responded to the 15-point plan and gave them most points, without providing further details.

- ASX 200 declined with the downside led by underperformance in tech and financials, although losses were somewhat cushioned by resilience in the energy, defensives and commodity-related sectors.

- Nikkei 225 suffered with intraday losses of more than 2000 points amid pressure from higher oil prices and jawboning by Japanese officials, while the Summary of Opinions continued to show a hawkish bias, and money markets are currently pricing in a near coin flip between a hike and a hold at the next BoJ meeting in April.

- Hang Seng and Shanghai Comp were mixed as participants digested a deluge of earnings, including from ICBC, China Construction Bank, BoCom, PetroChina and BYD, while it was also reported late last week that China began probes on US trade practices in retaliation for the US Section 301 investigations.

NOTABLE ASIA-PAC HEADLINES

- Japan's top FX diplomat Mimura said bold action may be needed if the situation in the Middle East continues, adds hearing that speculative activity is increasing and targeting all fronts in market for action.

- Japanese Government spokesperson says closely watching market moves with a extremely high sense of urgency. Currently seeing large volatility in financial markets.

- S&P affirms Japan at "A+/A-1"; outlook stable.

Loading...