Israel strikes Iran's Larijani while Supreme Leader rejected peace proposals - Newsquawk US Market Open

- A senior Iranian official said the new Supreme Leader rejected proposals that were sent to Iran's Foreign Ministry by two intermediary countries, with the Leader stating it is not the right time for peace and that the US and Israel must be defeated.

- Israeli Defence Minister Katz said Iran's Top Security Chief Larijani was killed in the airstrike; Iran has not confirmed the status of Larijani.

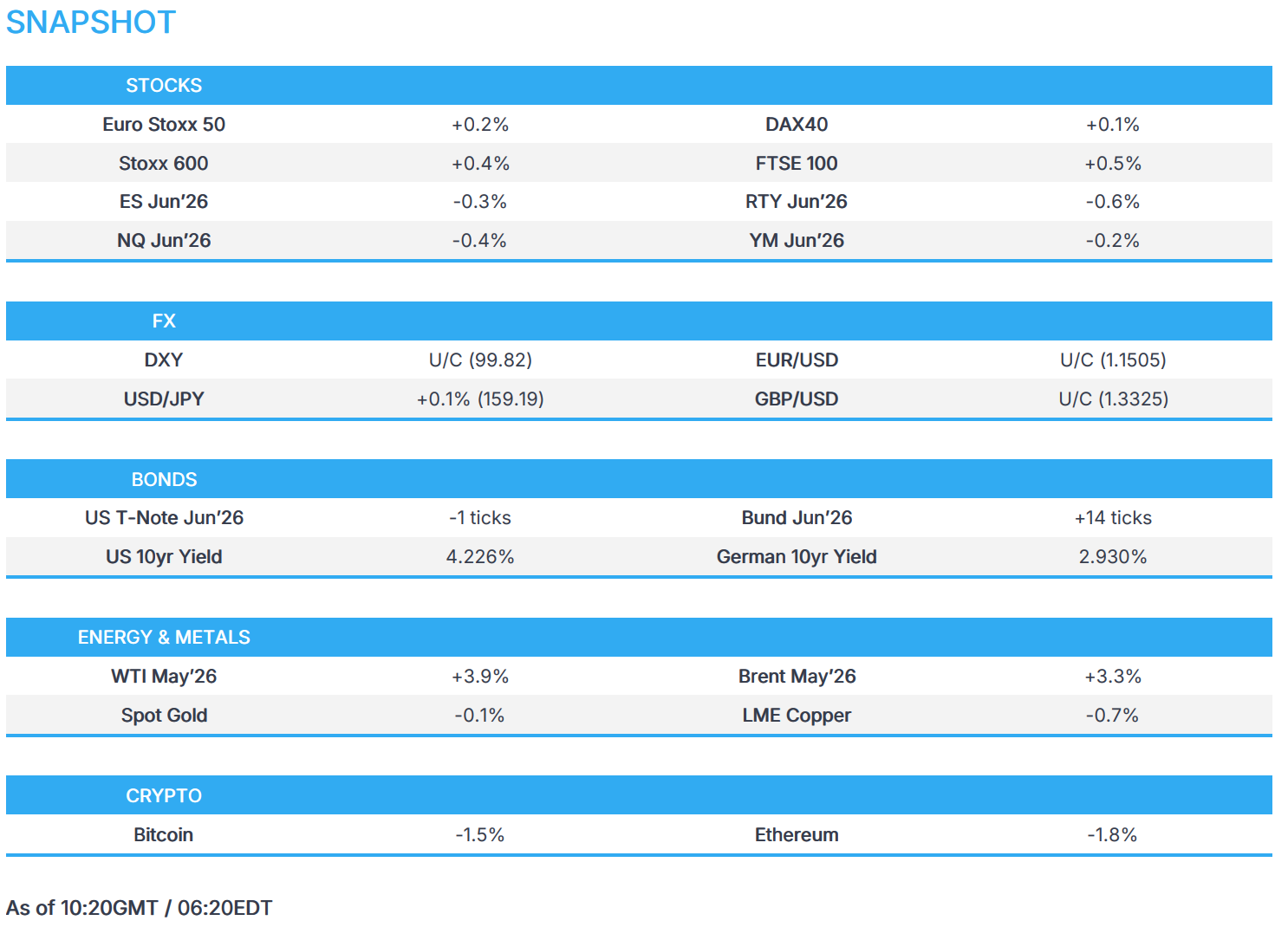

- Crude gains in choppy trade as the Iranian war continues; metals move with the dollar.

- European bourses are mixed, Neste lifts the Utilities sector; US equity futures fall following Nvidia's GTC event.

- DXY muted, G10s mixed while AUD outperforms after the RBA hiked rates.

- Fixed income continues to be driven by energy and geopolitics.

- Looking ahead, highlights include US ADP Employment Weekly, Japanese Trade Balance (Feb), Comments from ECB's Nagel, and Supply from the US.

EUROPEAN TRADE

EQUITIES

- European Bourses are all gaining as markets continue to price in the effects of oil prices. The IBEX 35 is the outperformer, closely followed by the FTSE 100. On the other hand, the DAX 40 is the laggard.

- European Sectors give no additional bias. Utilities outperform, with an upgrade for Neste at Barclays, lifting the entire sector. The Technology sector lies towards the bottom of the pile, not benefiting from the NVIDIA GTC event. Other key movers include Close Brothers, Fraport and Roche.

- US equity futures are subdued (ES -0.3%) as price action is dictated by oil. NVIDIA CEO Huang said at the Co. annual GTC event that its flagship AI processors for Blackwell and Vera Rubin systems would help generate USD 1tln in sales through 2027 with Vera Rubin set to ship later this year.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is flat within a narrow range, easing from overnight highs and trading closer to session lows after recent weakness. Price action remains sensitive to oil and geopolitics, with limited fresh escalation. Headlines around potential US–Iran dialogue and conflicting reports of contact have kept direction subdued, while reports of a senior Iranian security figure being killed briefly weighed on the USD.

- EUR/USD edges higher, reversing earlier weakness in line with the softer USD. Focus includes comments from EU’s Kallas, who suggested a Black Sea-style security model could be applied to the Strait of Hormuz and left the door open to EU participation. Broader EUR catalysts remain limited, with little reaction to progress on an EU–Australia trade deal. EUR saw downticks on the sub-par ZEW Economic Sentiment metrics.

- GBP/USD trades firmer alongside peers amid modest USD softness. UK-specific newsflow is light, though markets continue to monitor UK–US relations amid reported tensions over positioning in the Iran conflict. The pair holds near the top of its recent range.

- USD/JPY rebounded from a brief move below 159.00, supported by a partial recovery in the dollar and oil overnight. Upside is capped by broader USD softness during European hours, leaving the pair off recent highs and consolidating within yesterday's range.

- Antipodeans are mixed, with AUD/USD modestly firmer post-RBA. The initial dovish reaction to the rate decision reversed as Governor Bullock struck a hawkish tone, stressing that inflation remains elevated and that dissent centred on timing rather than the direction of further tightening.

FIXED INCOME

- USTs initially extended yesterday’s sell-off, with crude strength lifting yields and pushing prices to session lows. More recent headlines around Larijani triggered a pullback in oil and a recovery in risk sentiment, supporting bonds and bringing USTs back to broadly unchanged levels.

- Bunds followed a similar pattern, hitting early lows on higher yields driven by energy strength. The move reversed as oil pared gains on Larijani-related headlines, lifting Bunds back into positive territory. Negative ZEW Economic Sentiment propped up bunds in recent trade.

- Gilts opened amid the initial Larijani headlines and saw only modest early downside before sharply reversing higher. The benchmark rallied strongly alongside the pullback in yields and energy, outperforming peers.

- UK sells GBP 4bln 4.125% 2031 Gilt: b/c 3.33x (prev. 3.94x), average yield 4.228% (prev. 4.001%), tail 0.3bps (prev. 0.2bps).

- UK DMO plans to sell a new 10-year conventional gilt in April and long-maturity gilt in June. Also plans 2 syndicated gilt sales between April and June.

- Japan sold JPY 613bln 20-year JGBs; b/c 3.25x (prev. 3.08), average yield 3.141% (prev. 2.968%).

COMMODITIES

- Crude futures rebounded overnight after the prior session’s pullback, as the Iran conflict continues without major escalation. Late US trade saw pressure on reports of US–Iran contact, which were subsequently denied, alongside renewed Iranian attacks on regional energy assets, supporting prices. In Europe, headlines added further volatility: Fujairah port suspended oil loadings, while Israel indicated Iran’s top security chief Larijani may have been killed. Strait of Hormuz developments remain in focus, with EU’s Kallas suggesting a Black Sea-style framework, while Iraq noted ongoing discussions with Iran to allow tanker passage—prompting some intraday softness.

- Spot gold trades in a narrow range, largely tracking USD moves. Geopolitical tensions and inflation concerns are limiting haven-driven upside, keeping price action contained around the USD 5,000/oz level.

- Base Metals are mixed, with copper consolidating after prior gains supported by improved risk sentiment. Prices remain capped below the USD 13,000/t level, with momentum flattening following the recent advance.

- Fujairah port has suspended oil loadings, Bloomberg reported citing sources; loading berths at the Fujairah Oil Tanker Terminals were halted as of Tuesday morning.

- UAE's Fujairah confirms a fire in its petroleum industrial area.

- Chinese state oil majors have recommenced seeking Russian oil shipments following the US waiver, according to sources.

- Iraq's oil minister said they are in contact with Iran to allow some oil tankers to pass through the Strait of Hormuz, state news reported.

- Kazakhstan and Russia have discussed increasing Russian oil transit to China to 12.5mln tonnes per year, according to Kazakhstan’s Kaztransoil.

- EU's Kallas said a model similar to the Black Sea could be used in the Strait of Hormuz but the question is what neighbouring countries, including Iran, could agree on; the door is not closed on the participation in the Strait.

- Allies of the US President are concerned that Iranian attacks on oil tankers within the Strait of Hormuz are boxing in the US, Politico reported.

- Iranian oil exports continue without interruption, Tasnim reported citing the Parliamentary Energy Committee spokesperson.

- Some Japanese aluminium buyers have reportedly agreed with a global producer to pay a premium of USD 350/t for shipments between April and June.

NOTABLE EUROPEAN HEADLINES

- UK, Finland and others are reportedly exploring new defence financing mechanism by 2027, with the aim of increasing the availability of critical capabilities such as munitions.

NOTABLE EUROPEAN DATA RECAP

- EU ZEW Economic Sentiment Index (Mar) -8.5 vs Exp. 24 (Prev. 39.4).

- German ZEW Economic Sentiment Index (Mar) -0.5 vs Exp. 39 (Prev. 58.3, Low. 30, High. 54.5).

- Italian Inflation Rate MoM Final (Feb) M/M 0.7% vs. Exp. 0.8% (Prev. 0.4%).

- Italian Inflation Rate YoY Final (Feb) Y/Y 1.5% vs. Exp. 1.6% (Prev. 1%).

CENTRAL BANKS

- RBA hikes the Cash Rate by 25bps to 4.10%, as expected, with the decision made by a majority decision (5-4 vote split). Five members voted for a 25bps hike and four voted to leave the Cash Rate unchanged. Material risk inflation will stay above target for longer. Inflation risks have tilted further to the upside. Board will do what’s necessary to deliver price and jobs goals. Short-term inflation expectations have already risen. The conflict in the Middle East poses substantial risks in both directions and has resulted in sharply higher fuel prices, which, if sustained, will add to inflation. Will be attentive to data, evolving outlook, and risks in decisions. Wide range of data over recent months confirmed inflationary pressures picked up materially in H2 2025.

- RBA Governor Bullock said rise in oil prices is not the reason for the rate increase and that inflation was already too high, adds risks to inflation are to the upside and cash rate was not high enough to bring inflation back to the target. All members agreed inflation was too high, board agreed inflation was too high. Had a very robust meeting. Members that voted to hold, voted in a hawkish sense. Discussion was about timing, not the direction of policy and hike. Difference was timing and those who voted against, still felt the need for an eventual rate increase. Today's hike does not say anything about the forward path, and the forward path for rates is uncertain.

- BoJ Governor Ueda said price trend is rising gradually and underlying inflation is gradually accelerating towards the 2% target. Will implement appropriate policy to maintain stable prices. Will guide monetary policy suitably to steadily and durably achieve the 2% price target. Expect underlying inflation to approach the target in the latter half of fiscal 2026 through fiscal 2027. Reaffirmed stance that it will act flexibly in exceptional situations when JGB yields suddenly rise. BoJ to conduct bond operations flexibly in exceptional cases.

- Indonesian Interest Rate Decision 4.75% (Prev. 4.75%).

NOTABLE US HEADLINES

- US President Trump announces and signs executive orders to bring more community banks back into the mortgage business and to lower construction costs for building more affordable homes.

- China's Foreign Minister, on US President Trump seeking a delay to the summit with Chinese President Xi, said China and the US are in communication over Trump's visit to China.

GEOPOLITICS

MIDDLE EAST

- Israeli Defence Minister Katz said Iran's Top Security Chief Larijani was killed in the airstrike.

- Israel struck senior Iranian official Larijani but it is unknown if he was injured or killed, an Israeli official tells the Jerusalem Post.

- Israel Defence Forces announce wide-scale strikes against Iranian infrastructure and began additional wave of strikes on Hezbollah infrastructure in Beirut.

- A senior Iranian official says the new Supreme Leader rejected proposals that were sent to Iran's Foreign Ministry by two intermediary countries, with the Leader stating it is not the right time for peace and that US and Israel must be defeated.

- New Iranian Supreme Leader Mojtaba Khamenei is to deliver a message soon, according to Iranian media.

- Iran's Revolutionary Guard arrests 10 foreigners on espionage charges in northeast of country.

- Iran officials say the US has crossed the line and they signalled an intention to deliver a major lesson.

- Iran's Foreign Minister Araghchi said his last contact with US envoy Witkoff was before the American attack on Iran.

OTHERS

- UAE updated that air navigation has returned to normal across its airspace.

- Pakistan confirmed it carried out airstrikes on Kabul and Nangarhar.

- US President Trump's administration was said to tell Cuba its president has to go for there to be meaningful progress in negotiations, according to NYT.

- US President Trump said he believes he'll have the honour of taking Cuba.

- South Korea's Foreign Minister Cho and US Secretary of State Rubio discussed ensuring safe navigation in the Strait of Hormuz.

CRYPTO

- Bitcoin falls away from USD 76k while Ethereum holds above USD 2.3k.

APAC TRADE

- APAC stocks eventually traded mixed, with the region initially following suit to the gains on Wall Street, where sentiment was underpinned amid softer yields and oil price declines, although gains were capped overnight as oil prices partially rebounded and with participants bracing for this week's central bank bonanza, which was kicked off by the RBA, which delivered a widely expected back-to-back 25bps rate hike.

- ASX 200 was kept afloat as gains in miners, utilities, and financials offset the losses in tech and consumer discretionary, although the upside was limited amid the RBA rate decision, in which the central bank hiked rates for the second consecutive meeting in a 5-4 vote split.

- Nikkei 225 briefly reclaimed the 54,000 status but later fell into the red as oil partially rebounded from an early trough.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark outperforming in early trade amid strength in consumer stocks, while the mainland lagged after US President Trump revealed the US asked to delay the Trump-Xi summit by a month or so due to the Iran war.

NOTABLE ASIA-PAC HEADLINES

- China's Ministry of Finance said more pro-active fiscal policy is to continue in 2026, while it is to support the domestic market and self-reliance in tech, as well as ensure necessary expenditure levels.

- Japanese PM Takaichi reiterates that not considering further increase in consumption tax.

NOTABLE APAC DATA RECAP

- Japanese Tertiary Industry Index MoM (Jan) M/M 1.7% (Prev. -0.5%).

- New Zealand Food Inflation YoY (Feb) Y/Y 4.5% (Prev. 4.6%).

- South Korean Import Prices YoY (Feb) Y/Y 1.2% (Prev. -1.2%).

- South Korean Export Prices YoY (Feb) Y/Y 10.7% (Prev. 7.8%).v

Loading...