Micron soars 18% after stellar earnings, boosting global sentiment; crude benchmarks continue to pull back - Newsquawk US Market Open

- Conflicting reports on whether Israeli forces have pulled away from southern Lebanon, with Israeli and Lebanese sources denying earlier comments by a US State Department official stating Israel has pulled back.

- A senior Iraqi Oil Ministry official said the nation will consider all available options if its OPEC quota is not significantly increased and has considered the idea of leaving OPEC.

- Micron surges over 16% pre-market after it beat expectations and issued stronger guidance, benefiting from surging AI-driven demand, rising memory prices and long-term customer agreements, NQ +2.1%.

- DXY consolidates just shy of YTD highs; G10s mixed with cable outperforming.

- Fixed income benchmarks trade mixed ahead of a busy US data docket.

- Energy prices continue to fall while spot gold holds below USD 4k/oz.

- Looking ahead, highlights include US PCE (May), GDP Final (Q1), Jobless Claims (Jun/20), Durable Goods (May), Chicago Fed Labour Market Indicator (Jun), Atlanta Fed GDP (Q2), Banxico Policy Announcement, Speakers including ECB's Lane & Cipollone, Fed's Bowman, Williams & Goolsbee, Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

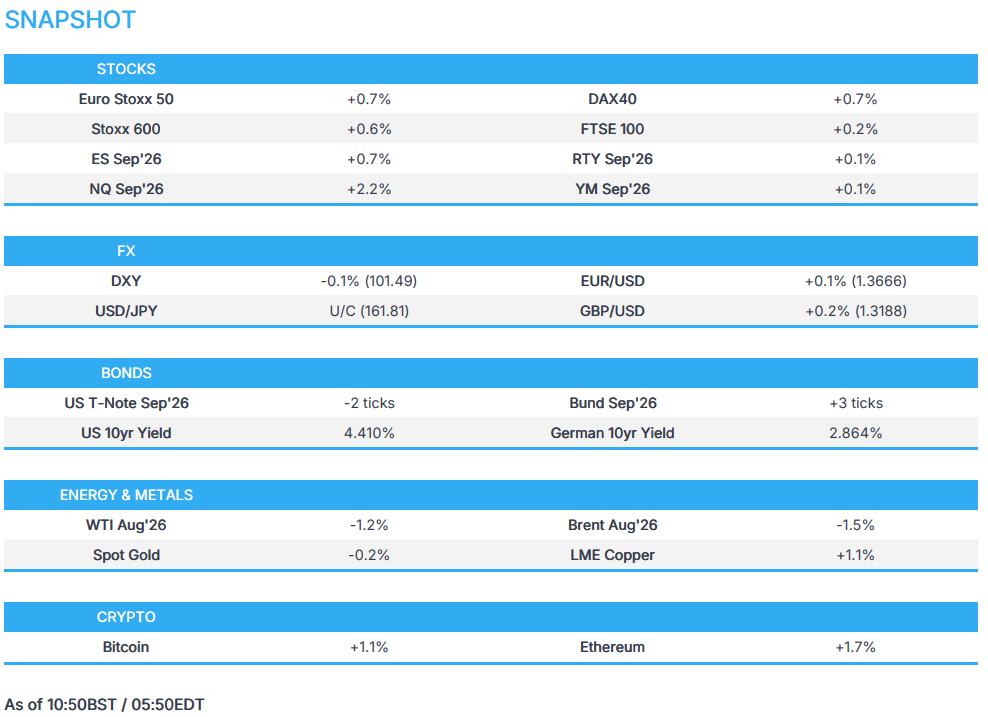

- European bourses (STOXX 600 +0.6%) begin Thursday's trade with broad gains, with tech-heavy indices leading following positive Micron earnings (AEX +0.8%, DAX 40 +0.6%). As the Iran conflict fades, with energy prices now reversing the wartime gains, equities in Europe can begin to catch up to their peers in the US and Asia. Investors are also seeing Europe as a safer place to place money due to its lack of tech giants, protecting themselves from any AI-related selloff.

- European sectors highlight the positive bias. Technology (+2.6%), unsurprisingly, is the clear outperformer. Utilities (+1.5%) and Financial Services (+0.8%) complete the top 3 sectors. To the downside is Media (-0.9%), Food, Beverages & Tobacco (-0.4%) and Chemicals (-0.3%).

- US equity futures are gaining across the board, with clear outperformance in the NQ (+2%) following earnings by Micron and an update from Qualcomm. For Micron (+16.4% pre-market), its Q3 adj. EPS and revenue beat estimates while its Q4 guidance also beat consensus. In terms of commentary, they said that tight conditions are expected to persist beyond FY27, and it has no line of sight on when supply can catch up with demand. For Qualcomm (+12% pre-market), the Co. raised its FY29 non-handset revenue target to USD 40bln, while announcing a strategic relationship with Hugging Face to advance open, developer-driven AI from devices to cloud infrastructure.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are mixed but mostly stronger against the Buck with breadth narrow as the Buck rally loses steam and fails to provide a bias to peers.

- USD benefitted this week from the risk-on mood into Micron earnings, which were released after US markets closed on Wednesday. Given the stellar report from the memory maker, risk-on trade has resumed, with equities (specifically tech–heavy indices) bid. DXY a touch lower on the day given the risk tone, trades at the lower end of its 101.44-101.66 range; now looking to PCE.

- Antipodeans lacklustre against the Buck despite the heightened sentiment. Aussie digested better-than-expected headline employment change, which failed to spark a meaningful reaction following on from the mixed inflation report in the prior session, with much of the change driven by temporary activity. AUD/USD +0.1% found buyers below 0.69, AUD/NZD +0.1% lifted from just below the 1.22 mark.

- USD/JPY continues to lack a bias as it hovers around levels not seen since July 2024. BoJ’s Tamura spoke overnight, sticking to the hawkish bias, advocating for tightening “once every few months” to a terminal of 2%. Despite the remarks initially helping the Yen, the move failed to stick, with the pair flat and approaching 162 to the upside.

- GBP remains focused on the Fiscal/Chancellor situation. Current Chancellor Reeves on the wires this morning, not providing too much new but seemingly teeing herself up to keep the role at no. 11. Prior to this, The Times reported that Miliband has been developing key economic policies for the new government, with particular reference to fiscal implications, a point potentially unwelcome by UK investors given his track record as Energy Secretary. GBP has not taken the skew from Gilts which underperform peers today amid the continued Miliband reporting, GBP/USD +0.1% after bouncing off 1.3150.

FIXED INCOME

- Global fixed benchmarks are softer across the board, albeit only modestly. This does come after the benchmarks surged in Wednesday's session, causing yields to break key markers, as energy prices continued to fall.

- USTs (-3 ticks) have pulled back from Wednesday's and Today's peak of 110-01, with 10yr yields slipping below the support level of 4.422%. Despite the positive 2-year auction on Tuesday, it failed to feed through to the 5-year tap. A busy data docket is ahead, with Core PCE Price Index (the Fed's preferred inflation gauge) expected to hold steady at 3.3% Y/Y. Final Q1 GDP is also expected to remain unchanged at 1.6%. Initial jobless claims, durable goods orders, Atlanta Fed GDP and a 7-year auction are also on the docket.

- Bunds (+3 ticks) and Gilts (-9 ticks) are also softer, but off worst levels. For German debt, its Q3 issuance plan was left unchanged, looking to raise EUR 138bln in the quarter. Bunds were unreactive following the announcement. ECB's Schnabel was on the wires this morning, reiterating her stance that the ECB will need to raise rates further to bring back inflation to 2%, while stating that although the short-term situation looks better than expected, the ceasefire is no reason for policymakers to let their guard down. For Gilts, although they were unreactive, the Guardian reported that some senior officials are pushing incoming-PM Burnham to issue GBP 20bln of "war bonds" to pay for higher defence spending. We are now attentive to specifics around the duration and magnitude of any theoretical issuance.

- JGBs (+5 ticks) consolidated, with a poor 20-year auction capping the upside. The b/c ratio dropped to 2.97, below the prior 4.01x and 12-month average. No significant move seen to hawkish BoJ speak overnight.

- German Q3 debt issuance plan unchanged, as expected: to raise EUR 138bln in Q3, set to issue EUR 512bln in 2026.

- UK sells GBP 1.5bln 0.50% 2029 Gilt via tender: b/c 3.61x (prev. 3.86x), average yield 4.062% (prev. 3.841%).

- Japan sells JPY 530.4bln 20-year JGBs; b/c 2.97x (prev. 4.01), average yield 3.542% (prev. 3.711%)

COMMODITIES

- Attention today has been on a recent route dispute on the Strait of Hormuz. The IRGC rejected a newly formed shipping lane, which traverses towards Omani waters, with the Group stating that it only accepts passage through it own routes. The IRGC warned that any attempts to pass through the Strait, outside of their own route, will be dealt with accordingly.

- Focus also on the Lebanon situation. Initially a US official stated that Israel had pulled back from parts of its buffer zone in Lebanon, which was then pushed back by Lebanese sources; it was then later confirmed by the Israelis that it had not received any instructions to pull back. This spurred some mild strength in the crude complex at the time.

- WTI and Brent are once again on a weak footing this morning, trading lower by c. 1.2% and 1.3% respectively. Markets continue to cheer the reopening of the Strait, with dozens of ships continuing to pass through daily. It is unclear how long this exuberance will last, given the risks surrounding the new Strait route and conflicting remarks and the volatile Lebanon-Israel situation.

- Also interesting was comments made by a senior Iraqi Oil Ministry official, who said the nation will consider all available options if its OPEC quota is not significantly increased and have considered the idea of leaving OPEC

- Spot gold trades shy of the USD 4k/oz mark, and holds within a USD 3,962-4,018/oz range, which is towards the bottom end of Wednesday’s trading bands. Analysts highlight several factors for the recent move lower in gold, which includes: 1) loss of safe-haven appeal, 2) stronger USD, 3) hawkish shift at the Fed, spurred following Warsh’s debut. On the latter point, Warsh ultimately highlighted the importance of price stability, which helped to push back on traders eyeing a debasement trade.

- Elsewhere, for the yellow metal, Bloomberg reported that major Chinese banks are reportedly shutting services supporting retail precious metals trading after gold and silver volatility. Elsewhere, 3M LME copper is firmer this morning, and trades within a USD 13,056.5-13,242.13/t range.

- US President Trump said he spoke with oil companies and that oil companies are not reducing gas prices enough, adding they will be in trouble if they are gouging.

- Saudi Arabia is reportedly set to restart Ras Tanura (550k BPD) oil exports as Gulf flows rise.

- Senior Iraqi Oil Ministry official said the nation will consider all available options if its OPEC quota is not significantly increased and have considered the idea of leaving OPEC. The current plan is to remain and gain higher quota.

- Iraqi Government spokesperson said the nation is working to restore full oil export capacity and aims to raise production to 7mln BPD over the coming years.

- China is reportedly raising its refined fuel export allowance for July, according to reports.

- Early reports suggest oil export and production were unaffected by the Venezuela earthquakes, according to Bloomberg's Blas.

- Chevron (CVX) CFO said gas prices will normalise, following pressure from President Trump on big oil companies, CNBC reported.

- Major Chinese banks are reportedly shutting services supporting retail precious-metals trading after gold and silver volatility, Bloomberg reported.

TRADE/TARIFFS

- The EU has given the US trade deal final approval, according to Bloomberg.

- UK Government announced new steel trade measures, effective July 1st. It will reduce the overall quota volumes by 51% and that any imports above would have a 50% tariff.

NOTABLE EUROPEAN HEADLINES

- UK Chancellor Reeves reiterated her backing for MP Andy Burnham, and stated that it is clear he is committed to the fiscal rules. On borrowing more for defence spending, she said the DIP will involve more money. Will not maintain current level of economic growth due to Middle-East conflict and decisions to be make on Jackdaw and Rosebank soon.

- Two of the UK's largest trade unions are increasing pressure on Andy Burnham not to pick Ed Miliband as the Chancellor, arguing that his North Sea oil policy has damaged jobs in the sector, according to FT.

- German Deputy Defence Minister Schmid said they are well underway on reaching the 3.5% defence spend target and that different options to be discussed on the subject of the Eurofighter.

NOTABLE EUROPEAN DATA RECAP

- German GfK Consumer Confidence (Jul) -29.2 vs. Exp. -28 (Prev. -29.8).

- Spanish GDP Growth Rate QoQ Final (Q1) Q/Q 0.6% vs. Exp. 0.6% (Prev. 0.8%).

- French Consumer Confidence (Jun) 84 vs. Exp. 84 (Prev. 82).

CENTRAL BANKS

- ECB's Schnabel said the short term situation now looks better than had been expected but the ceasefire is no reason for policymakers to let their guard down. We will need to raise interest rates further in order to bring inflation back to the two percent target over the medium term.

- BoJ Board Member Tamura said it is important to push the BoJ’s policy rate closer to neutral to avoid being forced to hike rates sharply later, and his view is for the BoJ to raise its policy rate once every few months towards a neutral level of around 2%. Tamura also stated that if upside price risks become more likely to materialise, the BoJ should not hesitate to speed up rate hikes or raise rates by a larger amount, while he voted against the decision to pause tapering from next fiscal year, as the BoJ should normalise the balance of its bond holdings as soon as possible.

NOTABLE US HEADLINES

- Fed said 32 large banks are well positioned to weather a severe recession and continue lending under the latest stress test, while the banks tested absorbed more than USD 700bln in hypothetical losses and saw capital decline only 1.6%, to remain above minimum requirements. Furthermore, the Fed reaffirmed its plan to maintain capital levels steady as it adjusts the testing process and will set new stress capital buffers following the 2027 test.

- Acting US AG Blanche has told several GOP senators he is willing to take formal action to kill the USD 1.8bln “anti-weaponization fund", Punchbowl reported citing sources.

GEOPOLITICS

MIDDLE EAST

- US President Trump reiterated that Iran will never have a nuclear weapon, while he adds that we will have peace in the Middle East. Trump separately commented that it is unacceptable to have fees on the Strait of Hormuz and they are doing great in negotiations with Iran, while he added that the Iran war powers vote is meaningless.

- US Secretary of State Rubio said we hope to reach a final agreement with Iran, but not at any price, and are now entering a new phase that hopefully leads to peace. Will not accept that Hormuz belongs to any nation-state. US President Trump has been fundamentally clear about the tolling issue. It can be a toll or a fee, but it is all semantics.

- US Senate Republicans defeated a war powers resolution regarding Iran in a 50-47 vote, to appease President Trump following a heated lunch meeting, according to NYT

- A US State Department official said Israel has pulled back from part of its buffer zone in southern Lebanon as an act of good faith. However, this was later refuted, with a Lebanese military source telling Al-Araby that the Israeli army has not withdrawn from any point in the areas it occupies in southern Lebanon. This was also denied by a senior Israel official.

- "Lebanese media outlets are reporting that an Israeli drone attacked the village of Tabit, in the Nabatia region in southern Lebanon", via Kan's Kais.

- Five South Korean ships were said to have exited the Strait of Hormuz, although the time frame is uncertain.

RUSSIA-UKRAINE

- Ukraine President Zelensky confirmed its military hit an oil depot in Russia’s Krasnodar region and two oil refineries in the Ufa region.

CRYPTO

- Bitcoin has rebounded modestly after bottoming at a new YTD low at USD 59.01k in Wednesday's lesson, currently trading at the upper end of a narrow USD 60.58k-61.87k range.

APAC TRADE

- APAC stocks traded mixed, albeit with a mostly positive bias and with the KOSPI leading the gains as tech and Nasdaq futures rebounded from the prior day's lows following strong earnings from Micron.

- ASX 200 was dragged lower by weakness in mining, materials, resources and energy stocks, while better-than-expected headline Australian jobs data failed to inspire and was mostly driven by part-time jobs.

- Nikkei 225 rallied back above the 72,000 level amid a resurgence in tech and lower oil prices, while markets were unfazed by comments from BoJ hawk Tamura, who called for hiking rates every few months.

- KOSPI outperformed amid a rally in Samsung Electronics and SK Hynix, with the latter sitting on double-digit percentage gains amid its US IPO plans.

- Hang Seng and Shanghai Comp were mixed in the absence of any major fresh drivers and with the Hong Kong benchmark dragged lower by losses in miners and further weakness in hyperscalers, including Alibaba, after Anthropic accused the Co. of illicitly accessing AI models in a letter to US officials.

NOTABLE ASIA-PAC HEADLINES

- USGS reported a magnitude 7.1 earthquake struck off the coast of Venezuela and that a second 7.5 magnitude earthquake hit the same area, while it warned of a potential massive catastrophe from the Venezuela quake, and estimated the quake death toll could exceed 1000, according to NYT.

- Earthquake reportedly hit Japan off the Iwate prefecture with a preliminary magnitude of 6.9, while NHK said Japan quake shaking intensity was 6+ on a scale of 7, while no tsunami warning was issued.- Japan's LDP is facing internal friction, with lawmaker Obuchi reportedly offering to resign if consumption tax is cut to 0%, NTV reported.

NOTABLE APAC DATA RECAP

- Australian Employment Change (May) 40.3K vs. Exp. 30.3K (Prev. -18.6K).

- Australian Unemployment Rate (May) 4.4% vs. Exp. 4.4% (Prev. 4.5%).

- Australian Full Time Employment Chg (May) 5.2K (Prev. -10.7K).

- Australian Participation Rate (May) 66.7% vs. Exp. 66.8% (Prev. 66.7%).

Loading...