Micron surges after Q3 earnings+guidance beat; NQ and European futures benefit - Newsquawk EU Market Open

- US stocks finished mixed. APAC trade was similar, but with KOSPI, +5.9%, leading and NQ, +1.9%, outperforming after strong Micron results, +18%.

- Micron beat expectations and issued stronger guidance, benefiting from surging AI-driven demand, rising memory prices and long-term customer agreements.

- DXY under modest pressure, peers generally contained. Brief JPY support seen on hawkish comments from BoJ's Tamura.

- Fixed contained, USTs unaffected by a weak 5yr sale, JGBs capped by the 20yr tap.

- Brent wiped out all upside from the US-Iran conflict. Precious metals choppy, base peers followed the risk tone higher.

- Looking ahead, highlights include German GfK Consumer Confidence (Jul), French Consumer Confidence (Jul), Spanish GDP Final (Q1), US PCE (May), GDP Final (Q1), Jobless Claims (Jun/20), Durable Goods (May), Chicago Fed Labour Market Indicator (Jun), Atlanta Fed GDP (Q2), Banxico Policy Announcement, German Finance Agency Issuance Outlook (Q3), Speakers including ECB's Lane & Cipollone, Fed's Bowman, Williams & Goolsbee, Supply from the UK & US.

- Click for the Newsquawk Week Ahead.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US President Trump reiterated that Iran will never have a nuclear weapon, while he adds that we will have peace in the Middle East. Trump separately commented that it is unacceptable to have fees on the Strait of Hormuz and they are doing great in negotiations with Iran, while he added that the Iran war powers vote is meaningless.

- US President Trump said Iran is making big concessions and it's going very well, while he also said that Iran is agreeing to everything he wants, and that they have to.

- US President Trump and Senator Cassidy of Louisiana clashed sharply over the administration’s war in Iran during a closed-door meeting at the Capitol on Wednesday, according to CNN, citing sources. It was separately reported that Trump said he had a great meeting with lawmakers.

- US Senate Republicans defeated a war powers resolution regarding Iran in a 50-47 vote, to appease President Trump following a heated lunch meeting, according to NYT

- US Secretary of State Rubio said the Hormuz Strait should be open and free and that the technical group on Iran will be back later this month. He added the US will help Lebanon "take control" of territory to act against Hezbollah.

- A source told Al-Mayadeen that the withdrawal schedule for the occupation army will be in accordance with the arrangements put in place to monitor the ceasefire and implement the first clause of the MoU.

- Iranian Foreign Ministry spokesperson said contradictory US statements on the MoU to end the war will not help in reducing Iranians' mistrust. The spokesperson also said NATO and its member states, including Italy and Romania, must be held accountable for any complicity in the crimes committed by the US and Israel against Iran

- IRGC Navy said safe passage through the Strait of Hormuz is only possible through routes announced by Iran and ship transits require coordination with Iran.

- Israeli Broadcasting Authority cited sources stating that negotiations between Israel and Lebanon took place at the Pentagon, and they were discussing the start of the withdrawal from southern Lebanon, while a partial Israeli withdrawal from some areas is expected, but not a complete withdrawal from southern Lebanon.

- The first day of negotiations between Israel and Lebanon in Washington on Tuesday ended without any progress and in some respects saw a setback, according to Axios citing sources. One source said parts of the talks were "ugly", while Israel acknowledged disagreements but maintained the atmosphere was "pleasant."

US TRADE

EQUITIES

- US stocks finished mixed as most sectors gained, with breadth strong, although continued tech weakness weighed on indices, resulting in the SPX and NDX closing in the red, looking to Micron. Major stock updates included Cerebras (CBRS) sinking 19% on expected declines in gross margins, Alphabet (GOOG) to replace Verizon in the Dow Jones, and OpenAI and Broadcom (AVGO) unveiling an LLM-optimised intelligence processor. A combination of tech risk off, lower energy prices, and quarter-end rebalancing saw T-Notes rally across the curve with the US 10yr yield down to 4.406%, while an unexpected decline in New Home Sales and a weaker US 5yr note auction sparked little reaction in the space.

- SPX -0.10% at 7,358, NDX -0.43% at 29,220, DJI +0.35% at 51,854, RUT +0.37% at 2,987.

- Micron Technology (MU): Micron shares rose almost 18% in extended US trading after the memory maker beat expectations and issued stronger guidance, benefiting from surging AI-driven demand, rising memory prices and long-term customer agreements. It reported Q3 adj. EPS of 25.11 (exp. 20.57), Q3 revenue of USD 41.456bln (exp. 35.56bln), adj. gross margin 84.9% (exp. 81.9%) and vs prev. 39.0% Y/Y as revenue more than quadrupled from USD 9.3bln amid surging AI-driven memory demand and tight supply. Micron ended the quarter with USD 30.2bln of cash, marketable investments and restricted cash. CEO said customers recognise memory and storage shortages will take considerable time to improve, with Micron expecting industry supply to improve gradually in 2028; added that tight conditions are expected to persist beyond FY27 and it has no line of sight on when supply can catch up with demand. Micron said it has signed 16 long-term customer agreements with data centre operators and automakers, representing expected financial commitments of USD 22bln, and declared a 0.15 dividend payable in July. Sees Q4 adj. EPS 31.00 (exp. 25.50), and sees Q4 revenue USD 50.0bln (exp. 42.915bln), sees Q4 capex of USD 10bln. Micron expects operating expenses to increase by approximately USD 1bln in FY27, and sees FY27 capex of USD 27bln.

- Click here for a detailed summary.

NOTABLE HEADLINES

- Fed said 32 large banks are well positioned to weather a severe recession and continue lending under the latest stress test, while the banks tested absorbed more than USD 700bln in hypothetical losses and saw capital decline only 1.6%, to remain above minimum requirements. Furthermore, the Fed reaffirmed its plan to maintain capital levels steady as it adjusts the testing process and will set new stress capital buffers following the 2027 test.

- NY Fed's Money Markets Director Marchioni downplayed the new FOMC language regarding an ample reserves system, stating the new FOMC language is not a policy change and the Fed retains flexibility on reserve management.

- US President Trump said we need a low interest rate, while Trump spoke with oil companies on Wednesday and said oil companies are not reducing gas prices enough, as well as warned they will be in trouble if they are gouging.

- US President Trump's administration sent Congress a USD 87.6bln supplemental budget request.

APAC TRADE

EQUITIES

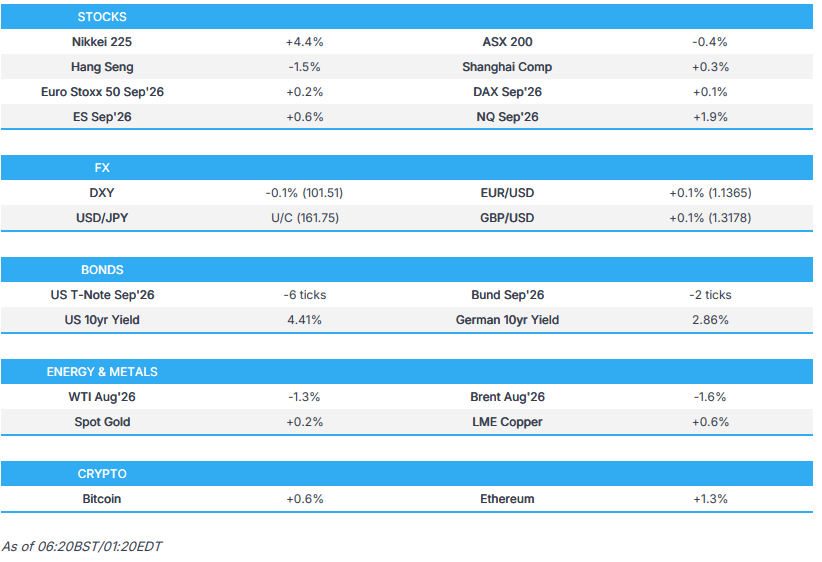

- APAC stocks traded mixed, albeit with a mostly positive bias and with the KOSPI leading the gains as tech and Nasdaq futures rebounded from the prior day's lows following strong earnings from Micron.

- ASX 200 was dragged lower by weakness in mining, materials, resources and energy stocks, while better-than-expected headline Australian jobs data failed to inspire and was mostly driven by part-time jobs.

- Nikkei 225 rallied back above the 72,000 level amid a resurgence in tech and lower oil prices, while markets were unfazed by comments from BoJ hawk Tamura, who called for hiking rates every few months.

- KOSPI outperformed amid a rally in Samsung Electronics and SK Hynix, with the latter sitting on double-digit percentage gains amid its US IPO plans.

- Hang Seng and Shanghai Comp were mixed in the absence of any major fresh drivers and with the Hong Kong benchmark dragged lower by losses in miners and further weakness in hyperscalers, including Alibaba, after Anthropic accused the Co. of illicitly accessing AI models in a letter to US officials.

- US equity futures rebounded with Nasdaq futures leading the upside following a blowout report from Micron.

- European equity futures indicate a slightly positive cash market open with Euro Stoxx 50 futures up 0.1% after the cash market closed with losses of 0.3% on Wednesday.

FX

- DXY slightly eased back after gaining yesterday alongside equity volatility, with price action contained amid light geopolitical developments and ahead of incoming data, including final Q1 GDP and the Fed's preferred inflation gauge.

- EUR/USD got some slight reprieve after steadily retreating to a one-year low beneath the 1.1400 handle.

- GBP/USD nursed some of its losses after declining to sub-1.3200 territory, but with the rebound contained amid quiet pertinent newsflow and a lack of data for the UK.

- USD/JPY lingered at the 161.00 territory, with only brief headwinds seen following hawkish comments from BoJ's Tamura, who called for further hikes, and said he opposed pausing tapering at last week's BoJ meeting.

- Antipodeans remained lacklustre following recent declines in commodities and amid the mixed risk appetite, while better-than-expected headline employment change for Australia failed to spur any meaningful reaction.

- PBoC set USD/CNY mid-point at 6.8209 vs exp. 6.8048 (prev. 6.8195).

- BoC Minutes showed members agreed monetary policy will need to remain nimble. Members agreed that if inflation data showed pressures spreading, it would signal that tighter policy is warranted, while also noting that the economic situation presents a dilemma for monetary policy. The summary added that unfavourable USMCA negotiations could have broader effects on jobs and investment in Canada.

FIXED INCOME

- 10yr UST futures took a breather after climbing yesterday alongside a slide in oil prices and as equities dipped, which spurred haven demand flows, while T-notes were unfazed by a weaker 5yr note auction and further incoming supply.

- Bund futures paused overnight and held on to recent spoils after advancing above the 127.00 level, while participants look ahead to approaching data, including German GfK consumer confidence.

- 10yr JGB futures were choppy at the open, but eventually edged higher, despite comments from BoJ hawk Tamura, who said it is important to push the BoJ’s policy rate closer to neutral to avoid being forced to hike rates sharply later, and that he voted against the BoJ’s decision to pause tapering from next fiscal year, as they should normalise the balance of its bond holdings as soon as possible. Furthermore, upside was capped following the latest 20yr JGB auction, which resulted in a lower bid-to-cover and higher accepted prices.

COMMODITIES

- Crude futures remained pressured with WTI back below USD 70/bbl and with Brent wiping out all Iran war gains as Strait of Hormuz traffic continues to pick up with US Energy Secretary Wright noting that roughly 72 ships have exited the waterway over 24 hours, amounting to 20mln barrels of oil, but suggested the normalisation of oil flows was delayed due to Iranian mines in the strait, while it was also reported that five South Korean ships exited the waterway.

- US Energy Secretary Wright said roughly 72 ships exited the Strait of Hormuz in the last 24 hours, amounting to 20mln barrels of oil, while he stated that a return to normal oil flows is being delayed by Iranian mines in the Strait and that Iran will not have the ability to block the waterway going forward. Wright also commented that the US will ensure oil flows continue even without a deal with Iran and said normal conditions could return within a few weeks. Furthermore, he said Venezuela's oil exports could reach 2mln BPD during this administration, and that the SPR could reach 500mln barrels with creative refill measures.

- Five South Korean ships were said to have exited the Strait of Hormuz.

- Iran has exported 40mln barrels of crude oil since June 15th, according to TankerTrackers data.

- Iraq ordered a halt to production at the West Qurna 2 oilfield with a capacity of 480k BPD, while Iraq's PM said Iraq wants OPEC to raise its oil output in line with production capacity and population.

- Russia is expected to ship a record 2.7-2.8mln BPD of crude from its western ports this month, according to three trade and port sources.

- Spot gold was choppy around the USD 4,000/oz level following recent dollar strength and rate hike expectations.

- Copper futures gradually rebounded from the prior day's trough alongside the mostly positive risk tone.

CRYPTO

- Bitcoin retreated beneath the USD 61,000 level then proceeded sideways for most of the session.

NOTABLE ASIA-PAC HEADLINES

- BoJ Board Member Tamura said it is important to push the BoJ’s policy rate closer to neutral to avoid being forced to hike rates sharply later, and his view is for the BoJ to raise its policy rate once every few months towards a neutral level of around 2%. Tamura also stated that if upside price risks become more likely to materialise, the BoJ should not hesitate to speed up rate hikes or raise rates by a larger amount, while he voted against the decision to pause tapering from next fiscal year, as the BoJ should normalise the balance of its bond holdings as soon as possible.

- Japan's government will call for appropriate monetary policy to support private demand in its economic blueprint, according to a draft cited by Reuters.

DATA RECAP

- Australian Employment Change (May) 40.3K vs. Exp. 30.3K (Prev. -18.6K)

- Australian Full Time Employment Chg (May) 5.2K (Prev. -10.7K)

- Australian Unemployment Rate (May) 4.4% vs. Exp. 4.4% (Prev. 4.5%)

- Australian Participation Rate (May) 66.7% vs. Exp. 66.8% (Prev. 66.7%)

GEOPOLITICS

OTHER

- US State Department said it is concerned by reports that Chinese Coast Guard vessels operating in waters east of Taiwan harassed commercial ships.

GLOBAL

- USGS reported a magnitude 7.1 earthquake struck off the coast of Venezuela and that a second 7.5 magnitude earthquake hit the same area, while it warned of a potential massive catastrophe from the Venezuela quake, and estimated the quake death toll could exceed 1000, according to NYT.

EU/UK

NOTABLE HEADLINES

- Two of the UK's largest trade unions are increasing pressure on Andy Burnham not to pick Ed Miliband as the Chancellor, arguing that his North Sea oil policy has damaged jobs in the sector, according to FT.

Loading...