NQ +0.8% into NVIDIA earnings and as Brent moves below $110/bbl; FOMC minutes ahead - Newsquawk US Market Open

- Iran-Pakistan cooperation has reportedly declined over the past two weeks, with a diplomatic source saying that Iran and Pakistan held conflicting positions on negotiation channels and the venue for talks.

- The EU has finalised the text of its US trade deal, as the bloc races to meet US President Trump's July 4th deadline.

- European bourses softer, chip names firmer ahead of NVDA earnings.

- Lacklustre trade across G10s with the DXY slightly firmer ahead of the FOMC Minutes.

- Fixed benchmarks find some reprieve as energy prices pull back, Gilts outperform following cooler-than-expected CPI.

- Crude futures on a softer footing, precious metals hold steady following Tuesday's selloff.

- Looking ahead, highlights include New Zealand Trade Balance (Apr), FOMC Minutes (Apr). Speakers include Fed's Barr, BoE's Bailey, Breeden, Dhingra & Mann. Supply from the US. Earnings from NVIDIA, Target & Intuit.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

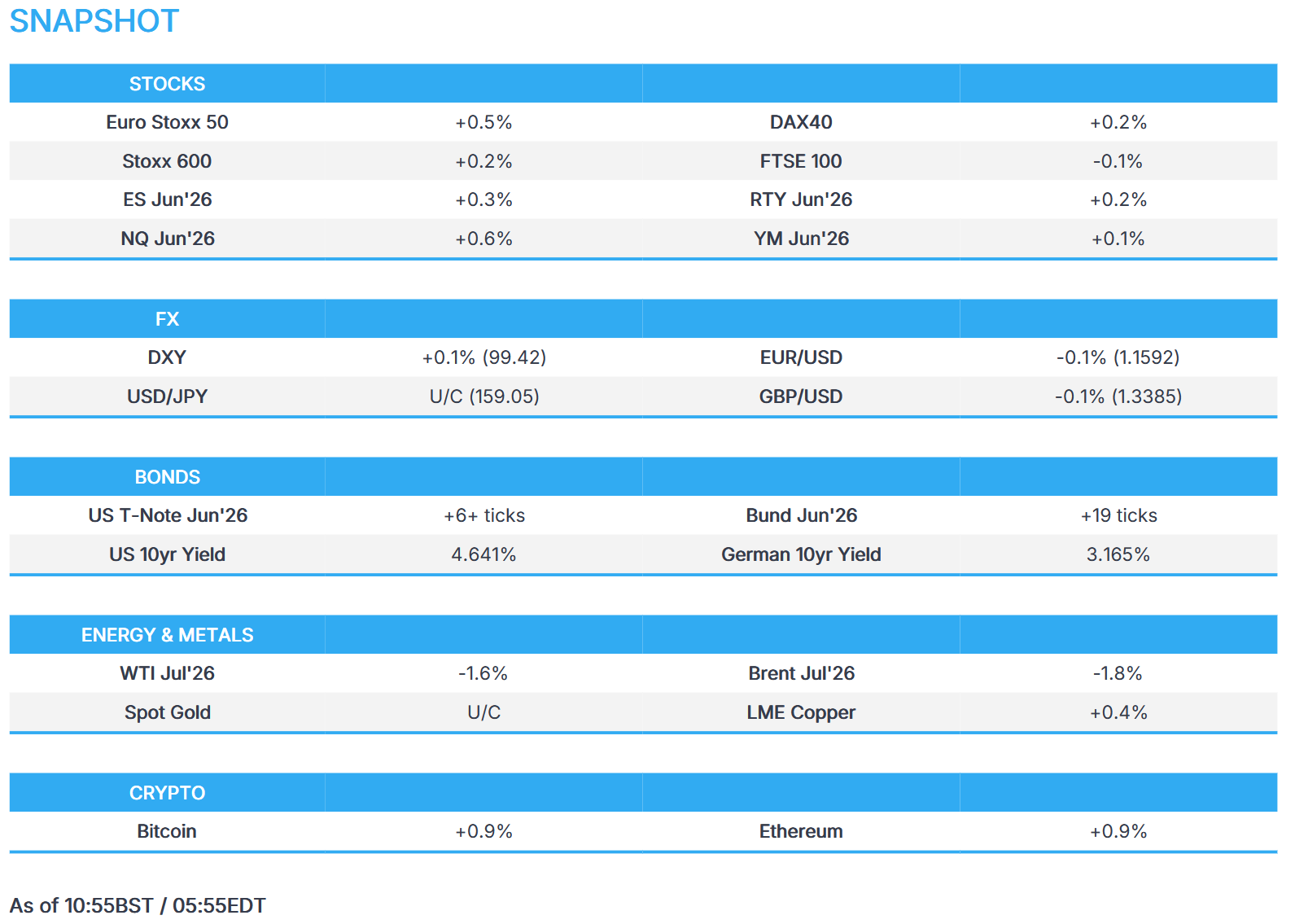

- European bourses (STOXX 600 +0.2%) were initially incrementally lower, but now display a more positive picture. On the trade front, the EU finalised the text of its US trade deal, in which the bloc would remove levies on US industrial goods in exchange for a 15% tariff ceiling on EU exports. Next steps are for the Parliament and EU countries to vote to ratify the text. The AEX (+0.4%) hovers around the U/C mark, with chip majors ASML (+3.2%) and BESI (+2.3%) supporting the index, while the FTSE 100 (-0.1%) sees little support following the cooler-than-expected UK inflation print.

- European sectors trade mixed. Basic Resources tops the sector pile as it manages to claw back some of Tuesday’s losses. Energy and Technology round out the top three sectors. To the downside, Media, Retail and Food, Beverages & Tobacco underperforms. UK supermarkets (Tesco -1.6%, Sainsburys -1.4%) have came under pressure after reports by the FT stated that the UK Treasury is pushing large supermarkets to introduce voluntary price caps on key groceries in return for lifting some regulations.

- US equity futures (ES +0.2% NQ +0.6% RTY +0.2%) are broadly firmer ahead of Nvidia’s (+1.5% pre-market) earnings after-hours. In terms of expectations for this quarter, adjusted EPS is seen at 1.78 and revenue at USD 78.98bln, while NVDA guided Q1 revenue to between USD 76.44-79.56bln. Note, the space is also attentive to updates from Samsung Electronics, with mediation occurring this morning ahead of imminent strike action.

- Samsung Electronics (005930 KS) union will go on strike as planned on Thursday as the mediation talks have ended.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- USD continues driving higher amid the continued unconstructive oil/yield environment with oil either side of USD 110/bbl and yields still elevated, albeit lower on the day. US/Iran news overnight was light, and nothing pertinent this morning, but the running commentary remains hostile. The Buck will remain attentive to Gulf developments, alongside expected hawkish FOMC minutes this evening, and NVIDIA earnings after the US close. DXY +0.1%, is now above all significant DMAs, with the 50DMA closest at 99.00.

- JPY remains rangebound amid the threat of intervention, with Yen fundamentals still bearish (Supplementary Budget/Energy). Demand at the overnight JGB auction was weak and saw some pressure in JGBs but no real follow-through to the FX space. USD/JPY is unchanged and testing 159.00 to the downside at the time of writing.

- GBP is a little weaker after soft April inflation data trimmed bets on BoE hikes. GBP/USD moved lower by c. 15pips post-data, now above pre-release levels as it attempts to regain a 1.34 handle. EUR/GBP moved higher by 10pips post-data, a move which swiftly pared amid resistance at 0.8670 and recent energy-related moves. (See 08:40 BST headline for more). EUR is also a touch weaker and seemingly moving lower in tandem with USD strength. EUR/USD -0.1%, the pair delved as low as 1.1583 before attempting to return back to a 1.16 handle, where it has traded throughout the week so far.

FIXED INCOME

- Global fixed benchmarks are firmer this morning, attempting to rebound from recent losses as energy prices pull back this morning. UK benchmarks outperform thanks to a cooler-than-expected regional inflation report, which has reduced the chance of a hike in June.

- USTs are firmer by a handful of ticks and trades towards the upper end of a 108-19+ to 108-30+ range. Focus remains on the geopolitical environment, with a recent WSJ report suggesting that Iran's position in talks with the US to end the war hasn't changed much from earlier iterations that failed to yield progress towards a deal. Earlier today, the IRGC provided some punchy rhetoric after it stated that the war would extend “beyond the region” if Iran is attacked again. Ultimately, an environment which keeps energy-related inflation woes at the front of minds, allowing yields to remain at elevated levels. On that front, the US10yr is just off recent highs, residing at 4.65%; the US-30yr (5.17%) remains towards peaks, after it surged to levels not seen since 2007, in the prior session. Ahead, FOMC Minutes and a 20yr auction.

- Bunds are firmer by around 10 ticks, and hold within a 123.86 to 124.22 range. Earlier, German PPI M/M printed a touch above the expected (1.2% vs exp. 1%); the statistics office notes that it “is primarily due to higher prices for intermediate goods”, particularly in precious metals prices. The report also highlighted the continued surge in energy prices. There was little move in German paper following this report. On the central banking front, ECB’s Wunsch said that the bond sell-off is not impacting the ECB’s thinking of Iran, adding that the Bank will need to act at some point. Elsewhere, French President Macron nominated Emmanuel Moulin to head the Bank of France. He said at the Senate today that the ECB must be ready to act to combat inflation, and stressed the importance of an independent central bank. He now appears at the National Assembly, where the outcome of the votes for his nomination will be announced this afternoon.

- Gilts outperform vs peers, and are currently higher by around 45 ticks; UK paper holds at the upper end of an 86.07 to 86.54 range. From a yield perspective, unsurprisingly the UK curve is bull steepening; the 10yr is now eyeing the 5% mark to the downside, but will likely need some positive geopolitical updates for a decisive breach below the key level. Price action today follows a cooler than expected inflation report, where headline CPI slowed to 2.8% in April, from 3.3% in March and below consensus of 3.0%. This report spurred a dovish repricing at the BoE, with markets now assigning an 8% chance of a hike in June (vs 35% pre-release); July now 50% (vs 84% pre-release).

- Germany sells EUR 3.845 vs exp. EUR 5bln 2.90% 2036 Bund: b/c 1.5x (prev. 1.24x), average yield 3.16% (prev. 2.92%), retention 23.1% (prev. 23.66%).

- Japan sells JPY 525.8bln 20-year JGBs; b/c 4.01x (prev. 4.82), average yield 3.711% (prev. 3.327%).

COMMODITIES

- WTI and Brent July futures have been edging lower throughout the European morning thus far, with newsflow relatively mixed. Out of Iran, one official noted that the region is open to negotiations whilst an IRGC member stated that the war will extend beyond the region, if Iran is hit again. Most recently, Saudi press citing a diplomatic source suggested that Iran-Pakistan cooperation had declined/stopped over the past two weeks.

- Nonetheless, crude futures remain heavy, with WTI in a USD 102.50-104.45/bbl range while its Brent counterpart resides in a USD 109.52-111.49/bbl range at the time of writing, with some weakness seen in the European morning despite a lack of clear catalysts, although the moves did follow comments from the Iranian Deputy to the President. Dutch TTF is flat in choppy trade above the EUR 51.50/MWh mark.

- Spot gold is choppy and resides in a relatively narrow USD 4,453-4,508/oz at the time of writing, vs yesterday’s USD 4,464-4,589.58/oz parameter, with the yellow metal subdued by the firmer dollar. Spot silver, conversely, rebounds following yesterday’s 5% losses.

- Base metals are mixed with newsflow on the quieter side this morning as markets await further US-Iran updates, with its implications watched from inflationary/growth standpoints. 3M LME copper resides in a narrow USD 13,357.00-13,506.00/t range at the time of writing.

- US Private Inventory Data (bbls): Crude -9.1mln (exp. -3.4mln), Distillates -1.0mln (exp. -1.3mln), Gasoline -5.8mln (exp. -2.1mln), Cushing -1.4mln.

- Russia's Kremlin said there is an agreement with China regarding something important on energy. Russia's Kremlin spokesperson Peskov later said the details on the Power of Siberia 2 pipeline still needs to be agreed.

- UK Treasury said Chancellor Reeves is expected to introduce broad reforms that would allow Parliament to authorise critical energy infrastructure projects.

- EU Commission official thinks EU countries can reduce gas consumption by 15bcm this year.

- The EU have reportedly shortlisted tungsten, rare earths, magnesium and gallium for potential stockpiling.

TRADE/TARIFFS

- The EU has finalised the text of its US trade deal, as the bloc races to meet US President Trump's July 4th deadline. The deal would see the EU remove levies on US industrial goods in exchange for a 15% tariff ceiling on EU exports. EU's von der Leyen later said she welcomes agreement reached by the European Parliament and Council on reducing tariffs for US industrial exports to the EU, while she calls on the co-legislators to move swiftly and finalise the process on this.

- EU Trade Commissioner Sefcovic has reportedly been in contact with US Commerce Secretary Lutnick, US Treasury Secretary Bessent and USTR Greer.

- China's MOFCOM confirmed China will purchase 200 Boeing (BA) jets and said the US is expected to provide engines and parts support for the China Boeing deal. MOFCOM announced a resumption of poultry imports from certain US states and said China reinstated qualified US beef exporter registrations, while it stated the US and China are seeking to extend the Kuala Lumpur trade agreement.

NOTABLE EUROPEAN DATA RECAP

- UK Inflation Rate MoM (Apr) M/M 0.7% vs. Exp. 0.9% (Prev. 0.7%, Low. 0.8%, High. 1.3%).

- UK Inflation Rate YoY (Apr) Y/Y 2.8% vs. Exp. 3% (Prev. 3.3%, Low. 2.8%, High. 3.4%); Services 3.2% (prev. 4.5%). ONS: "There was a notable fall in annual inflation led by lower electricity and gas prices. This was due to the government’s energy bill support package reducing variable and fixed tariffs, along with lower global wholesale energy prices before the conflict in the Middle East, which fed through to the reduction in the Ofgem cap."

- UK Core Inflation Rate MoM (Apr) M/M 0.7% (Prev. 0.4%).

- UK Core Inflation Rate YoY (Apr) Y/Y 2.5% vs. Exp. 2.6% (Prev. 3.1%, Low. 2.5%, High. 3.2%).

- EU Inflation Rate MoM Final (Apr) M/M 1% vs. Exp. 1% (Prev. 1.3%, Low. 1%, High. 1.1%).

- EU Inflation Rate YoY Final (Apr) Y/Y 3% vs. Exp. 3% (Prev. 2.6%, Low. 3%, High. 3.1%).

- EU Core Inflation Rate YoY Final (Apr) Y/Y 2.2% vs. Exp. 2.2% (Prev. 2.3%, Low. 2.2%, High. 2.2%).

- German PPI MoM (Apr) M/M 1.2% vs. Exp. 1% (Prev. 2.5%).

- German PPI YoY (Apr) Y/Y 1.7% (Prev. -0.2%).

CENTRAL BANKS

- Fed's Paulson (2026 voter) said inflation remains too high and interest rate cuts may only happen after inflation is controlled, while he also commented that current policy is appropriate and it is healthy for markets to consider an extended hold or hikes. Paulson stated the US labour market is stable and consumption is slowing, but is resilient, and a rate hike may be considered if growth moves above potential or other inflation risks emerge. Furthermore, he reiterated that he did not see a need to change language at the last policy meeting, as well as noted that risks are 'super-elevated' right now to both inflation and the outlook.

- ECB's Wunsch said the bond selloff is not impacting the ECB's thinking of Iran and that the ECB will need to react at some point.

- JPMorgan expects the BoE to hike 25bps in July (prev. forecast of hike in June).

NOTABLE US HEADLINES

- US President Trump signed a fintech Executive Order to protect the US financial system from illicit activity, while it was reported that the White House plans to release an Executive Order on cybersecurity and AI safety as soon as this week, which seeks early government access to advanced models.

GEOPOLITICS

MIDDLE EAST

- US intelligence assessment recently showed that US forces identified at least 10 mines in the Strait of Hormuz, according to CBS citing US officials.

- US Senate voted 50-47 to advance war powers resolution that would end US strikes on Iran unless approved by Congress.

- Iran's IRGC said that if the attack on Iran occurs again, the war will extend beyond the region, Fars News reported.

- Iranian Deputy to the President Banah said Tehran is open to negotiations within national interests, Al Mayadeen reported.

- Iranian Foreign Minister Araghchi said months after the start of the war on Iran, US Congress acknowledged the loss of dozens of aircraft worth billions, and Iran's powerful Armed Forces are confirmed as the first to strike down a touted F-35, while he added that with lessons learned and the knowledge they gained, a return to war will feature many more surprises.

- Iran-Pakistan cooperation had declined/stopped over the past two weeks, Al Arabiya and Al Hadath reported citing a senior diplomatic source. A diplomatic source says Iran and Pakistan held conflicting positions on negotiation channels and the venue for talks, and says mistrust was affecting coordination between Iran and Pakistan.

- Pakistan's Interior Minister Naqvi is on route to Tehran, according to Journalist Mallick.

- "On the verge of a decision: Trump and Netanyahu held a phone conversation last night that was described as “lengthy and dramatic,” according to journalist Segal.

- Two Chinese supertankers, carrying 4mln barrels of oil, exited the Strait of Hormuz on Wednesday, according to tracking data. It was later reported that India was preparing to send oil tankers through the Strait of Hormuz following prior reports regarding the Chinese tankers.

RUSSIA-UKRAINE

- EU governments are discussing whether former ECB President Draghi or former German Chancellor Merkel could represent the bloc in potential negotiations with Russian President Putin, according to FT.

- Russian strike killed two in Ukraine's Dnipro and Ukraine reports multiple regional drone attacks, while Russia claims interception of 273 Ukrainian drones, according to AFP.

- Ukraine's military confirms it struck a Russian oil refinery in the region of Nizhny Novgorod.

OTHER

- Some Trump advisers reportedly left the US-China summit thinking that a Chinese move on Taiwan was growing more likely, Axios reported. The piece suggested that Taipei is not in panic, at least on the surface

- US President Trump said Cuba is a failed nation that needs help from the US, while he believes a diplomatic deal can be made, according to Semafor.

- US indictment of former Cuban president Raúl Castro is expected to be announced today, according to two federal sources familiar with the investigation cited by NBC News.

CRYPTO

- Bitcoin regained the USD 77k handle, Ethereum consolidated above USD 2.1k.

APAC TRADE

- APAC stocks declined following the weak handover from the US, with sentiment dampened amid headwinds from a higher yield environment and the uncertain geopolitical backdrop.

- ASX 200 retreated with the declines led by underperformance in the mining and materials sectors, while a lack of data and firmer yields contributed to the uninspired mood.

- Nikkei 225 fell beneath the 60,000 level with notable pressure in machine tool and electrical equipment manufacturers, while recent comments from Japan's Finance Minister, and current FX levels were seen to stoke intervention risks.

- Hang Seng and Shanghai Comp conformed to the downbeat sentiment amid bond and inflation woes, with the declines in Hong Kong led by mining, solar and property stocks, while there was a lack of surprises from the PBoC announcement to maintain the benchmark Loan Prime Rates for the 12th consecutive month.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi met Russian President Putin in Beijing and said that relations have reached their current level due to deepened political mutual trust and strategic cooperation, while Putin said ties between Russia and China support broader international stability. Furthermore, China and Russia plan to deepen continuous strategic coordination, and Putin invited Chinese President Xi Jinping to travel to Russia next year, while Xi told Putin that the world faces the risk of regressing into a “law of the jungle.”

- Japanese PM Takaichi said she is not currently at a stage where she can comment on the possible size of the extra budget. She further said that plans to protect people’s lives and businesses while curbing issuance of deficit-financing bonds as much as possible.

NOTABLE APAC DATA RECAP

- Chinese Loan Prime Rate 1Y (May) 3.0% vs. Exp. 3.0% (Prev. 3.0%)

- Chinese Loan Prime Rate 5Y (May) 3.5% vs. Exp. 3.5% (Prev. 3.5%)

- Taiwan Export Orders (Apr) Y/Y 48.1% vs exp. 45.0% (prev. 65.9%).

Loading...