NQ outperforms as INTC +28% premarket, Brent on $107/bbl handle, UoM finals ahead - Newsquawk US Market Open

- "Israeli media: A limited operation against Iran may be carried out to avoid a prolonged war", Al Arabiya reports.

- Chinese Securities Regulator says that China is to allow qualified foreign investors to trade treasury futures from April 24, 2026, for hedging purposes only.

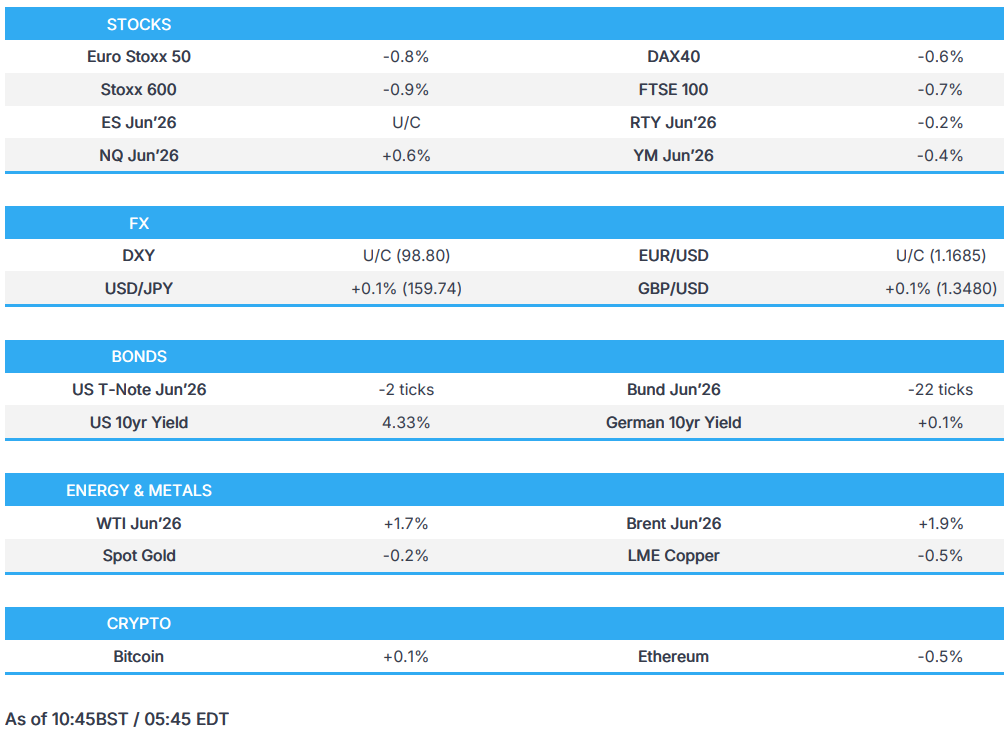

- Downbeat sentiment across European bourses, SAP +6% after a EUR 10bln share buyback; NQ outperforms, with INTC +23% post-earnings.

- FX price action lacklustre, CHF and JPY dodge intervention comments, UoM Final ahead

- Fixed falters as energy climbs, Gilts lag again in catch-up trade and after further hawkish impetus into the BoE.

- Crude underpinned as eyes remain on US-Iran ceasefire heading into the weekend.

- Looking ahead, highlights include Canadian Retail Sales (Feb), US UoM Survey Final (Apr), CBR Policy Announcement (Apr).

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

MIDDLE EAST

- US President Trump posted that the meeting between Israel and Lebanon went well, the US is to work with Lebanon to protect itself from Hezbollah and that the Israel-Lebanon ceasefire is to be extended by three weeks.

- US President Trump said nobody is trying to get through the US blockade.

- US President Trump said the Israel-Lebanon talks in the Oval Office went well and it would be great to resolve simultaneously with Iran. Looking forward to the next meeting with Israeli PM Netanyahu. Great chance of peace between Israel and Lebanon this year. Everyone seems united against Hezbollah. Israel-Lebanon peace should be an easy one. Israel will have to defend itself if they are shot at. Israel will be surgical in their self-defence. Iran has to cut its Hezbollah funding.

- Tanker Helga arrives at Iraq’s Basra offshore terminal to load 2mln BPD of crude, sources say; Helga is the second tanker to reach Basra terminals since the Hormuz closure.

- "Israeli media: A limited operation against Iran may be carried out to avoid a prolonged war", Al Arabiya reported.

- Pakistani official noted of a state of uncertainty regarding the second round of talks, "and we await Iran's response", Al Arabiya reported.

- Israel again attacks southern Lebanon, claiming retaliation for overnight rocket fire, Al Jazeera reported.

- Lebanese press Al-Jumhuriya noted of accelerated diplomatic efforts toward a Lebanon–Israel non-aggression agreement, driven by the US–Saudi–Egypt initiative, Journalist Kais reported. Plan revives idea of containing (not dismantling) Hezbollah’s weapons. Key proposed terms:. Israel withdraws to ceasefire line. Lebanese army deploys in south. Hezbollah moves north of Litani River. Start of weapons containment plan. Border disputes (Blue Line) adjusted. Prisoner releases, return of civilians, reconstruction. Deal would have international (especially US) guarantees. Coordination includes Iran to ensure Shiite/Hezbollah involvement. Parallel effort to resolve internal Lebanese political divisions. Saudi envoy pushing for meeting of Lebanon’s top leaders to create a unified position.

- "Iranian Foreign Ministry: Araqchi held two called with the Pakistani army chief and foreign minister to discuss a ceasefire.", Al Araby reported.

- Iranian Vice President said any attack on oil wells will be met with strikes on attackers’ oil facilities; said it will be beyond “eye for an eye” response, Mehr News reported.

- Senior IRGC Commander said Tehran is secure and its borders are stronger than before, Press TV reported.

- The US has put a USD 10mln bounty on the leader of the Iran-backed Shiite militia group in Iraq, CBS reported.

- Lebanese media reported that Israel have conducted airstrikes on the town of Al-Qasir in southern Lebanon a few hours after US President Trump announced the 3-week ceasefire extension, IRIB reported.

- Israel's ambassador to the UN said the extension of the Lebanon ceasefire is not 100% certain and that Israel is forced to answer every time a threat is detected, Tasnim reported citing CNN.

- US military are developing plans to target Iran's Hormuz defences if the ceasefire fails, CNN reported.

- Israel-Lebanon talks have gotten underway in the White House, according to reported.

- Hezbollah said it has launched rockets at Israel's Shtula region in response to Israel violating ceasefire and targeting towns in southern Lebanon.

- Israeli military said several launches crossed from Lebanon towards Israel were intercepted.

- An internal Pentagon email explores options to punishing NATO allies that the US believes failed to support the US operations against Iran, according to a US official. Options include:. Suspending Spain from NATO. Reviewing the US position on British claims to the Falkland Islands. Suspending difficult countries from important or prestigious positions at NATO.

EQUITIES

- European bourses started the European session with broad based losses, continuing the downbeat mood seen across APAC trade. From an index perspective, the IBEX 35 (-1.3%) lags peers, whilst the AEX (-0.1%) fares a bit better vs peers.

- European sectors hold a strong negative bias. Energy leads, buoyed by strength in underlying oil prices. Also for the sector, Siemens Energy (+2.4%) gains post-earnings after it reported a mixed set of results, but raised its FY outlook; elsewhere, Eni (+1%) beat on its Adj. EBIT metric, and announced a 90% increase to its share buyback, citing an upbeat commodities outlook. Tech and Telecoms complete the top three. The Tech sector has been boosted today by post-earnings strength in SAP (+6.4%). The Co. reported better-than-expected operating profit and revenue, with cloud metrics also topping expectations. It also said it will buy back EUR 10bln of shares. To the bottom of the pile resides Autos, Basic Resources and Retail. The autos sector is underperforming this morning with seemingly broad-based losses; Volvo (+1%) reported Q1 metrics today, where its metrics were mixed, but ultimately indicating resilience amidst challenges.

- US equity futures are mixed, with the NQ (+0.5%) outperforming, whilst ES (U/C) and RTY (-0.3%) lag. The tech-heavy index has been buoyed by significant pre-market strength in Intel (+23%, strong earnings and guidance), TSMC (+3%, Taiwan eases fund limits) and AMD (+7.4%). Ahead, US Michigan final sentiment is expected to see consumer sentiment at 47.6 (prev. 53.3, current conditions at 50.1 (prev. 55.8), expectations at 46.1 (prev. 51.7), while one-year inflation expectations are seen up to 4.8% (prev. 3.8%), and five-year expectations at 3.4% (prev. 3.2%). Canada retail sales are seen rising 0.2% M/M (prev. 0.9%).

- Intel (+23%) after stronger-than-expected earnings and revenue in Q1, robust Q2 guidance, growing signs of a business revival, strong data centre and foundry growth, and optimism around rising AI-related CPU and advanced packaging demand.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX price action is lacklustre on the final trading day of the week. DXY leads marginally, while CHF and JPY are slightly lower.

- DXY trades tentatively and broadly in tandem with oil prices. A light calendar ahead with the Fed on blackout ahead of next week's meeting and only UoM final data on the docket. USD-specific news light, though the Japanese Finance Minister said overnight there were no plans to change currency swap lines with the US. DXY still remains supported above 100 and 200 DMAs at 98.50; upside resistance is 98.90, which marks the session high.

- SNB Chairman Schlegel was on the wires a couple of times. He said they have "unrestricted" room for manoeuvre when it comes to the policy rate and FX intervention - Vice Chair Martin also echoed these remarks. EUR/CHF is unchanged on the session; it attempted to approach 0.92, but the move faltered at 0.9199.

- Katayama is also on the wires, she said "will take decisive action on speculative activity", JPY unchanged, in a signal that markets are becoming comfortable with the Finance Minister's threats. USD/JPY unchanged, looks at 160 to the upside. BoJ rate decision next week, likely to remain on hold, with all eyes on Governor Ueda's tone at the presser.

- GBP shrugged off strong UK Retail Sales for March, as it does not change the narrative into next week's BoE, where a hold is the base case. The data showed upside was driven by an increase in fuel sales, with retailers reporting that motorists were filling their tanks when buying following the start of the Middle East conflict. Online sales saw upside and are potentially indicative of a robust spring sale period. However, the core figures were in line/softer-than-expected, and potentially point to some greater-than-expected caution among consumers during the early stages of the Middle East conflict. EUR/GBP and Cable both unchanged, the former on a 0.8670 handle.

FIXED INCOME

- A modestly bearish session for fixed benchmarks, initial action a function of the modest and since increasing energy upside as we count down to and participants position into a potentially risk-packed weekend.

- Amidst this, USTs post downside of a handful of ticks in a thin 110-30 to 111-03 band. Ahead, the US docket is light, and we look to next week's FOMC.

- Bunds post slightly larger downside, perhaps as Dutch TTF has been leading oil benchmarks throughout the morning. Currently, in the red by c. 30 ticks but also in a relatively narrow 125.20-44 band. The European docket is light, aside from Italian supply (should be well received, particularly after the sizeable demand at last week's syndications); as such, price action will likely be dictated by geopolitical developments.

- Gilts gapped lower at the open, acknowledging the pressure in fixed peers seen late-Thursday. Opened at 87.10, lower by 41 ticks. Thereafter, slipped another 28 to an 86.82 low and has held there since; the second bout of pressure spurred by further energy upside and a hawkish BoE DMP. The DMP spurred end-2026 BoE pricing to 59bps of tightening from c. 54bps this morning and significantly above the 23bps implied this time last week.

- To recap the day's data. UK Retail Sales were strong on a headline level but in-line/soft on a core basis, with consumer motor fuel purchases driving the headline, no implications for the BoE next week (hold expected, guidance in focus). Thereafter, Germany's Ifo was soft across the board, with no real follow-through to EGBs.

- Italy sold EUR 2.5bln vs exp. EUR 2.25-2.5bln 2.20% 2028 BTP Short Term: b/c 1.63x (prev. 1.78x) & average yield 2.80% (prev. 2.89%).

- Australia sold AUD 1bln vs exp. AUD 1bln 2.50% 2030 AGB: b/c 3.82x (prev. 3.44x), average yield 4.6947% (prev. 4.2888%).

COMMODITIES

- In geopolitics, fresh updates have been light as focus remains on the state of the US-Iran ceasefire and talks. The week ahead centres on four key watchpoints. First, the Strait of Hormuz “red line”: President Trump has warned the US Navy could actively engage IRGC vessels suspected of laying mines or interfering with traffic, shifting from shadowing to potential direct strikes, particularly after an IRGC-escorted Iranian ship defied the blockade. Second, the nuclear deal standoff: Washington is pushing for a comprehensive deal, while Tehran insists the nuclear file is not part of the current talks, raising the risk that negotiations collapse if neither side compromises on uranium enrichment. Third, internal dynamics in Tehran: reports of leadership friction and IRGC influence over the negotiating team point to possible policy inconsistency or hardline escalation. Fourth, ceasefire fragility: despite the extended Israel-Lebanon truce, sporadic clashes and reported drone activity underline how easily a trigger event could occur.

- Oil rose for a fifth day as limited US-Iran progress towards resumed de-escalation talks kept supply concerns elevated; Brent climbed above USD 106/bbl (vs weekly lows of ~ USD 91/bbl) and is set for its biggest weekly gain since the war’s first week. WTI June, however, remains sub-USD 100/bbl. Brent currently trades in a daily range between 105.02-107.40/bbl while WTI resides in a USD 95.55-97.85/bbl range.

- Gold edged lower, below USD 4,970/oz, with investors weighing whether higher crude prices from the US-Iran conflict could keep inflation and interest rates elevated. XAU/USD resides in a USD 4,658.03-4,711.23/oz range at the time of writing.

- Copper heads for a weekly loss, with the broader base metals complex also mostly under pressure, as uncertainty over the Middle East war clouds the global growth outlook, while the US and Iran show little sign of returning to talks after Trump extended the ceasefire indefinitely, and the Strait of Hormuz remained largely blocked. 3M LME copper resides in a USD 13,215.58- 13,322.33/t. LME aluminium spread experiences the largest backwardation since 2024.

- Japanese PM Takaichi said she is urging the cabinet to seek new sources for oil imports.

- Union Spokesperson said workers at Australia's INPEX (1605 JT) LNG plant vote in favour of strikes.

- EU leaders have tasked Finance Ministers to come up with new measures to deal with potential energy shortages after assessing that current proposals were not enough, Bloomberg reported, citing sources.

- Japan's METI said Japan is to release 5.8mln kL of national oil reserves, starting May 1st.

- Imports of Russian fuel oil to Singapore has jumped with volume in April already more than double the average monthly amount in 2025, according to FT citing Vortexa data.

- The fire at Russia's Tuapse oil terminal is under control.

- US President Trump said that the US does not have an oil shortage and are taking millions of barrels of oil from Venezuela. Have a great relationship with Venezuela.

- CME cuts initial margin on its Comex 100 gold futures to 6% from 7% and Comex 5000 silver futures to 11% from 14%.

TRADE/TARIFFS

- China reportedly to add seven EU companies to export control list, according to reported. Hensoldt (HAG GY) was added.

- Canada is reportedly to seek talks with the EU regarding access to ‘Made in Europe’ scheme, according to FT.

- China's Commerce Minister met with the President of European Automotive Manufacturers Association to talk about the China-EU auto industry cooperation and EU trade restrictions. Commerce Minister stated that China will firmly safeguard Chinese firm's rights.

- US President Trump tells the Telegraph that the US will retaliate if the UK continues to target companies such as Apple (AAPL) , Google (GOOGL) and Meta (META) through the digital services tax.

- US President Trump said the US will put a tariff on the UK if the digital service tax is not dropped.

NOTABLE EUROPEAN DATA RECAP

- German Ifo Current Conditions (Apr) 85.4 vs. Exp. 85.5 (Prev. 86.7, Low. 83, High. 87).

- German Ifo Business Climate (Apr) 84.4 vs. Exp. 84.8 (Prev. 86.4, Low. 83.7, High. 87.5).

- German Ifo Expectations (Apr) 83.3 vs. Exp. 83.9 (Prev. 86.0, Low. 82, High. 87.3).

- Spanish PPI YoY (Mar) Y/Y 3.4% (Prev. -7%).

- French Consumer Confidence (Apr) 84 vs. Exp. 88 (Prev. 89, Low. 87, High. 89).

- Hungarian Unemployment Rate (Mar) 4.7% (Prev. 4.9%).

- UK Retail Sales YoY (Mar) Y/Y 1.7% vs. Exp. 1.3% (Prev. 2.5%, Low. 0.8%, High. 2.2%).

- UK Retail Sales ex Fuel YoY (Mar) Y/Y 1.7% vs. Exp. 2.0% (Prev. 3.4%, Low. 1.5%, High. 2.5%).

- UK Retail Sales ex Fuel MoM (Mar) M/M 0.2% vs. Exp. 0.2% (Prev. -0.4%, Low. -0.5%, High. 0.6%).

- UK Retail Sales MoM (Mar) M/M 0.7% vs. Exp. 0.0% (Prev. -0.4%, Low. -0.8%, High. 1.8%).

- Swedish PPI YoY (Mar) Y/Y 2.0% (Prev. -1.7%).

- Swedish PPI MoM (Mar) M/M 0.6% (Prev. 0.2%).

CENTRAL BANKS

- US President Trump opens door to alternative Fed renovation probe, Semafor reported;.

- US Fed Balance Sheet (Apr/22) 6.707.

- US President Trump said Kevin Warsh is terrific, while he repeats criticism on Fed Chair Powell and said Powell should have lowered rates.

- BoE DMP:. Raises 1yr ahead CPI to 3.5% (prev. 3.1). Raises 3yr ahead CPI to 2.8% (prev. 2.7%). 1yr ahead wage growth 2.4% (prev. 3.5%). 64% of firms expected to increase their prices (with 4% lowering prices).

- BoE's Breeden said equity markets look overvalued and could decline, according to the BBC.

- SNB Chairman Schlegel said they have "unrestricted" room for manoeuvre when it comes to the policy rate and on FX intervention. Sees slower growth and higher inflation from the Middle East conflict.

- SNB's Schlegel said the Bank will not hesitate to move rates into negative territory and that a move below zero is a bigger step than a normal cut.

NOTABLE US HEADLINES

- Chinese Securities Regulator said that China is to allow qualified foreign investors to trade treasury futures from April 24, 2026, for hedging purposes only.

- US official said Russia is to be included in G20 summit invitations.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukrainian authorities say a foreign-flagged ship bound for Odesa was attacked by Russian drones.

- Imports of Russian fuel oil to Singapore has jumped with volume in April already more than double the average monthly amount in 2025, according to FT citing Vortexa data.

- The fire at Russia's Tuapse oil terminal is under control.

- US official said Russia is to be included in G20 summit invitations.

CRYPTO

- Bitcoin is a little firmer this morning and trades around USD 77.5k, whilst Ethereum is a touch lower.

APAC TRADE

- APAC stocks traded mostly in the red, ex. Nikkei 225, as bourses caught up to the selloff seen stateside, as risk-off flows dominated the tape after the reports that Israel is on high alert in anticipation of a possible renewed war this weekend.

- ASX 200 slipped further below the 8,800 handle, as losses in IT offset the gains made by Energy names.

- Nikkei 225 outperformed, supported by the tech sector as chips benefitted from Intel’s earnings (see more below). Ibiden, one of Japan’s biggest electronics companies, hit a new ATH while Canon fell after cutting its FY profitability guidance.

- Hang Seng and Shanghai Comp traded with the biggest losses, albeit just slightly, after a flurry of earnings. China Telecom reported Q1 net that fell by 17% Y/Y while autos underperformed.

NOTABLE APAC DATA RECAP

- Japanese Services PPI Y/Y 3.1% vs exp. 3.0% (prev. 2.7%).

- Japanese Inflation Rate YoY (Mar) Y/Y 1.5% (Prev. 1.3%).

- Japanese Inflation Rate MoM (Mar) M/M 0.4% (Prev. -0.2%).

- Japanese Inflation Rate Ex-Food and Energy YoY (Mar) Y/Y 2.4% (Prev. 2.5%).

- Japanese Core Inflation Rate YoY (Mar) Y/Y 1.8% vs. Exp. 1.8% (Prev. 1.6%, Low. 1.4%, High. 1.9%).

NOTABLE APAC EQUITY HEADLINES

- Samsung Electronics (005930 KS) has produced the first working single-digit nanometer DRAM working die, TheLec reported citing sources; Co. intends to adjust processing conditions based on this.

- Nomura Holdings (8604 JT) FY25/26 (JPY): Net 362.1bln (prev. 340.7bln Y/Y), Pretax 539.8bln (prev. 432.1bln Y/Y), Revenue 4.76tln (prev. 4.74tln Y/Y). Cuts dividend.

- Hyundai Steel (004020 KS) Q1 (KRW) oper. profit 15.7bln (prev. loss 19.0bln Y/Y).

- Kia Motor (000270 KS) Q1 2026 (KRW): Net 1.83tln (exp. 1.93tln), Operating Profit 2.21tln (exp. 2.3tln), Revenue 29.5tln (exp. 29.3tln).

- Mercuria is to take a 25% stake in an aluminium smelter, as well as hunt for copper mining investments, the FT reported.

- Taiwan regulator is to increase the equity exposure limit per stock to 25% from 10% for funds and ETFs.

- Renesas (6723 JT) Q1 2026 (JPY): Revenue 380.3bln (prev. 308.8bln Y/Y) , Operating profit 90.6bln (prev. 21.5bln Y/Y).

Loading...