NQ rebounds despite energy adding to recent gains; US CPI and Warsh testimony due - Newsquawk US Market Open

- The US continued to launch strikes for a third night, after President Trump stated that he would hit Iran “very hard” on Monday and Tuesday. Separately, Trump threatened to hit Iran’s “Pickaxe Mountain”, an underground nuclear facility; Brent Sep’26 +4.0%.

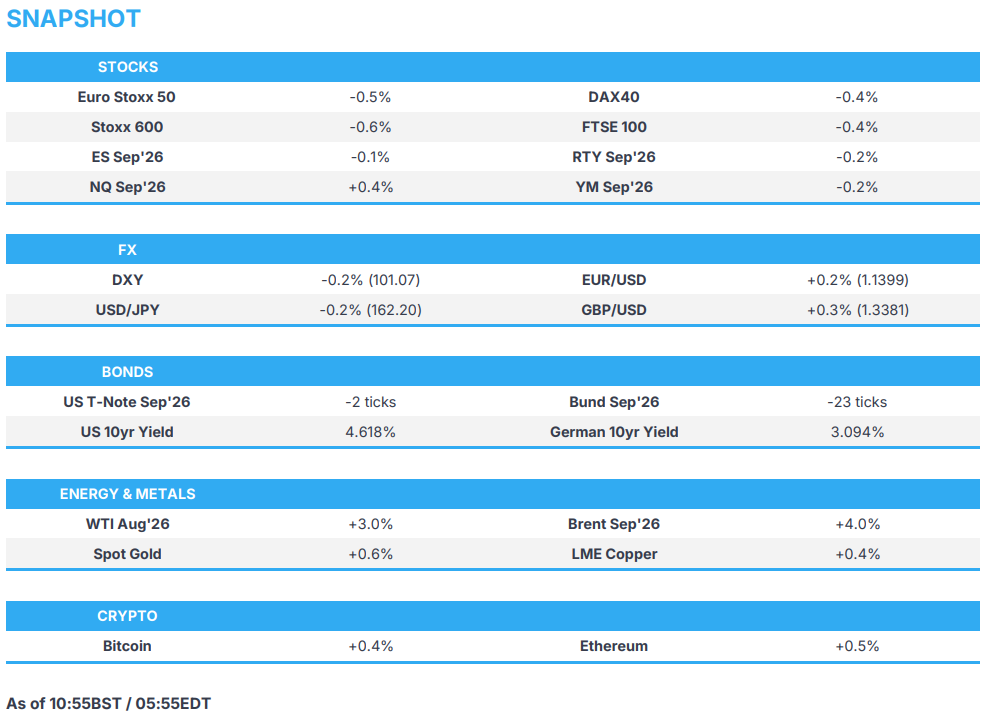

- US equity futures are mixed, with the NQ outperforming as it recovers from Monday's selloff; US banking names kick of earnings.

- DXY tentative heading into CPI and Fed Chair Warsh's testimony; Kiwi outperforms after further hawkish RBNZ rhetoric.

- Fixed income benchmarks are softer amid energy moves and continued post-Waller hawkishness.

- Crude benchmarks grind higher on continued US-Iran updates while spot gold finds support above USD 4k/oz.

- Looking ahead, highlights include US CPI (Jun), Fed Discount Rate Minutes (Jul), ECB President Lagarde-US Treasury Secretary Bessent meeting, Speakers include Fed Chair Warsh, Goolsbee, Barr, Cook and Bowman, BoE Governor Bailey, Earnings from Citi, Goldman Sachs, JPMorgan, Bank of America and Wells Fargo.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.6%) are lower across the board after Monday's choppy trade. Escalating US-Iran tensions return as a headwind for Europe, with energy prices rising, weighing on many of the continent's biggest industries (airlines, luxury).

- European sectors highlight the negative bias. Basic Resources (+1.3%) and Energy (+1.2%) are printing decent gains, while Utilities (+0.3%) and Chemicals (+0.2%) also trade in the green. To the downside is Travel & Leisure (-2.1%), Media (-2.0%), and Consumer Products & Services (-1.9%).

- US equity futures are mixed, with the NQ (+0.4%) outperforming as chip names rebound from Monday's rout. Banks will kick off the US earnings season, with JPM, BAC, GS, WFC and C all due.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are mostly firmer as markets are reluctant to buy Dollars into US CPI, after it gained on Monday. Kiwi is the clear outperformer; energy exporters CAD and NOK also perform well.

- Geopolitics remain constructive for USD with Brent over USD 85/bbl, in addition to this, hawkish Fed speak from Waller saw markets assign a 50% probability of a Fed hike this month. (“Fed would need to consider a rate hike in the near term if core inflation is hot this week”). Despite these factors, the Buck is negative on the day as it stabilises below Monday’s 101.32 peak ahead of a packed session which is slated to see US CPI, and Warsh’s testimony to the US house which potentially sees a text release at 13:30 BST. The level to watch if momentum continues today is the 21DMA @ 101.00, should CPI come in hot, Monday’s 101.32 peak will be in focus, thereafter is July 2nd’s 101.43 high.

- Kiwi is the best performer once again as markets add to RBNZ tightening bets, interest rate futures now implying 58bps by year-end - around 5bps added vs. the end of Monday’s London session. Upside which comes after hawkish remarks from RBNZ's Conway and a strong quarterly NZIER Business Confidence.

FIXED INCOME

- US and Iran continued to strike each other for a third night, after President Trump warned that they would hit Iran “very hard”. POTUS also announced a naval blockade on all Iranian ports, which is set to begin at 21:00 BST / 16:00 EDT.

- Crude benchmarks were firmer throughout the APAC session, though price action was more-or-less sideways. Into the European morning, the bias turned a bit more bullish after the UKMTO reported another incident on a tanker near Oman. This comes after two Emirati tankers were struck overnight. It is clear that the IRGC will not accept any transits through undesignated paths through the Strait of Hormuz; as such, traffic through the Hormuz is waning. Marine Traffic data has shown that only two tankers completed passages through the Hormuz in the 24 hours up to 07:25 BST today; this compares to c. 28 ships/day following the US-Iran MoU signing.

- As it becomes apparent that ships are no longer going through the Hormuz (and added risk of the blockade and/or nuclear attacks), the crude complex has moved higher. Brent Sep’26 (+3.7%) sits at the upper end of a USD 83.68-87.38/bbl range.

- Spot gold is a little firmer this morning, and trades within a narrow USD 3,983-4,034/oz range; currently holding just above the USD 4k/oz mark. The yellow metal appears to be taking a breather following a couple of sessions in the red, which was spurred by recent geopolitical escalations and a hawkish Fed speak via Waller. Elsewhere, base metals hold a positive bias following stronger-than-expected Chinese data overnight. In brief, Exports and Imports both rose from the prior, and by more than the consensus. 3M LME Copper holds within a USD 13,461-13,624/t range.

- Germany sells EUR 4.222bln vs exp. EUR 6.0bln 2.70% 2028 Schatz: b/c 1.13x, average yield 2.77%, retention 29.63%.

- Japan sells JPY 530.9bln 20-year JGBs; b/c 4.52x (prev. 2.97), average yield 3.626% (prev. 3.542%), Tail in price 0.00 (prev. 0.24).

- The Netherlands sells EUR 3.27bln vs exp. EUR 2.5-3.5bln 2.50% Jan 2031 DSL: Average yield 2.911% (prev. 2.795%).

- Australia sells AUD 400mln 5.00% June 2036 bonds b/c 4.1, avg yield 4.908%.

COMMODITIES

- A bearish start for benchmarks as the complex reacts to the overnight energy move.

- Action that was sufficient to push Bunds below the 125.00 handle and to a 124.82 base, lower by just over 40 ticks on the day. Since, no real reaction to the morning’s updates, including a UKMTO tanker report in Oman, despite modest energy upside at the time.

- For Germany, June’s WPI was dictated by energy, with the Y/Y moderating from the prior but at an elevated level as mineral oil products were just under 22% higher vs June 2025. However, the same component was down 6.8% M/M, leading to a -0.7% headline M/M print (exp. 0.5%, prev. -0.6%). No move to the series.

- Gilts opened lower by a handful of ticks before extending below the 87.00 handle, and then moving sharply lower to an 86.42 base, catching up to the above and continuing the pattern of greater magnitudes of action vs peers on energy-related moves. Pressure may also be a function of pricing into the Burnham coronation on Friday, as he will become UK PM from the point Starmer formally hands over. On that, Rathbones has reduced its Gilts holding in order to protect against “fiscal irresponsibility” ahead of Burnham and the Chancellor decision. Note, likely outgoing Chancellor Reeves speaks at Mansion House this evening.

- USTs also lower, down to a 108-17 trough given the energy move, which has seen a modest extension on the pressure after Fed’s Waller on Monday evening said another hot core inflation read would mean the Fed needs to consider a near-term hike. CPI today is seen at -0.1% M/M (prev. 0.5%), while the now even more pertinent core is seen at 0.2% M/M (prev. 0.2%). Following Waller and the recent energy moves, pricing for July has moved in favour of a hike, with around a 60% chance of a 25bps move currently implied. We now look to testimony from Chair Warsh, which is scheduled for after CPI; note, a text release alongside CPI is possible.

- BP (BP/ LN) says upstream production is expected to be between 2,170-2,220mboepd (prev. 2,339mboepd Q/Q), due to seasonal maintenance predominantly in the Gulf of America and the effects of disruption in the Middle East.

- Pakistan LNG is reportedly seeking an additional LNG cargo for July as US-Iran hostilities in the Strait of Hormuz constrain supplies from Qatar, according to Bloomberg.

- Turkey’s energy minister said Iraq requested retaining oil export capacity of 750K BPD through the Kirkuk-Ceyhan pipeline for 12 months under an agreement.

- Iran’s Oil Minister Paknejad said Iran’s oil exports continue as usual despite the US removal of oil waivers.

- Freeport-McMoRan (FCX) Indonesia unit is targeting 2026 copper production of 0.8bln pounds.

NOTABLE EUROPEAN HEADLINES

- EU Commission approved EUR 659mln German State aid for four new semiconductor facilities.

NOTABLE EUROPEAN DATA RECAP

- German Wholesale Prices MoM (Jun) M/M -0.7% vs. Exp. 0.2% (Prev. -0.6%).

- UK BRC Retail Sales Monitor YoY (Jun) Y/Y 1.7% vs. Exp. 2.9% (Prev. 3.4%).

CENTRAL BANKS

- RBNZ Chief Economist Conway said the Middle East conflict complicates monetary policy like all supply shocks, while he added that understanding how firms respond to cost shocks is crucial in maintaining low and stable inflation. Furthermore, he said that despite easing prices, the effects of the shock are expected to continue impacting the economy for some time, and that a further reduction in monetary stimulus is likely to be required.

- BoE Governor Bailey said that the core banking system in the UK is resilient and that debt levels are not stretched. He stated that renewed hostilities in the Gulf underline continuing instability. The UK's position is supported by its fiscal framework as well as monetary policy.

NOTABLE US HEADLINES

- US House will vote today on merging the SAVE America Act with a national security and State Department funding bill, Fox reported.

- NY has become the first US state to halt construction of large new data centres, imposing a one-year moratorium on 14th July, Reuters reported. The move responds to concerns over power costs, water supplies and community impacts as states consider limits on AI infrastructure’s effects on electricity grids and utility bills.

GEOPOLITICS

MIDDLE EAST

- US President Trump reiterated that Iran has no air force, no navy and no military, while he said they will hit Iran very hard on Monday night and on Tuesday. Trump said they had a deal yesterday and that Iran breaks deals, as well as commented that the MoU was built to test Iran and that Iran didn't honour it. Trump also stated that they will hit 'Pickaxe Mountain' pretty soon and have their eyes on the site all the time, which is a good potential target

- US Central Command announced that it conducted and completed a third consecutive night of strikes against Iran, with US strikes reported in Bushehr, Bandar Abbas and Bandar Kangan, while explosions were also reported in Iran's Qeshm Island and Kish Island. More recently, there have been reports of explosions have been heard near Bandar Abbas, Bushehr and Choghadak.

- Details of US President Trump’s proposed Strait of Hormuz toll plan are still being finalised, according to Semafor, saying Trump is 'very serious about the tolls.

- Iran's armed forces have begun targeting US naval vessels in the Strait of Hormuz with cruise missiles, Al Mayadeen reported.

- Iranian Army Spokesperson said the Strait of Hormuz will not be open with US aggressions and war, SNN reported.

- IRGC said it targeted weapons warehouses, satellite communications centres, and US forces' housing building at Bahrain's Juffair base. Iran's army also targeted US military facilities and equipment in Kuwait with drones, as well as targeted a 'hostile' US vessel with cruise missiles, while it was separately reported that a US military base in Jordan was hit by a missile attack and that a missile attack hit an Iranian Kurdish opposition group site east of Iraq's Erbil.

- UKMTO received a report that a tanker was hit by an unknown projectile 40NM northeast of Qalhat, Oman. UKMTO reports of an incident 13NM southeast of Lima, Oman, the tanker was reportedly hit by a missile transiting outbound on the southern route

- The UAE Defence Ministry reported that two national tankers were targeted by Iranian cruise missiles in the southern Strait of Hormuz, with the incident occurring in Omani territorial waters, although the fires on both tankers were brought under control, and it reserved the right to respond to the escalation.

- ADNOC confirmed tankers "Al Bahyah" and "Mombasa B" were hit in the Strait of Hormuz.

- Oman’s Foreign Minister said complex talks are under way to make a long-term arrangement to guarantee freedom of navigation through the Strait of Hormuz.

RUSSIA-UKRAINE

- Russian ballistic missiles targeted Ukraine's capital of Kyiv, with sirens and explosions heard across the Ukrainian capital, according to FT.

- Russian forces conducted group strikes at night, damaging military industry and enterprises involved in missile production in Kyiv, while it damaged infrastructure facilities in Odessa, used to store Ukrainian armed forces' fuel and lubricants.

- Ukraine Navy spokesperson said Russia struck a civilian vessel near Ukraine’s Black Sea port of Odesa. Additionally, Ukraine said it struck two Russian oil refineries in the Bashkortostan and Krasnodar regions.

OTHER

- US President Trump said they're looking into whether Cuba is storing Iranian drones, while he added that they will take care of it if Cuba has Iranian drones.

CRYPTO

- Bitcoin rebounded slightly but remains below the USD 63k mark. Ethereum held below USD 1.8k.

APAC TRADE

- APAC stocks were mostly in the red following the weak lead from the US, where risk sentiment was weighed on by tech selling and geopolitical escalation, while US-Iran strikes persisted for the third consecutive night and Trump announced to reinstate the naval blockade on Iran, as well as touted a 20% Hormuz shipping fee.

- ASX 200 was dragged lower by weakness in tech, industrials, consumer staples and financials, but with the downside stemmed by resilience in energy and utilities, while there was also an improvement in Westpac Consumer Sentiment.

- Nikkei 225 initially dropped below the 67,000 level amid tech weakness and higher oil prices, but then gradually nursed its losses and returned to flat territory as domestic yields softened.

- Hang Seng and Shanghai Comp conformed to the tech-related weakness and ultimately failed to benefit from the better-than-expected Chinese trade data.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama suggested it is time to consider including JGBs in NISAs, and stated that if the environment surrounding asset management changes sharply, a change to GPIF's portfolio could be examined, while she hopes to quickly establish details on steps to make Japanese government bonds more attractive.

NOTABLE APAC DATA RECAP

- Chinese Balance of Trade (Jun) 125.8B vs. Exp. 121B (Prev. 105.43B).

- Chinese Exports YY (Jun) 27% vs. Exp. 18.2% (Prev. 19.4%).

- Chinese Imports YY (Jun) 36% vs. Exp. 24% (Prev. 27.4%).

- Singaporean GDP Growth Rate QQ (Q2 A) 1.1% vs. Exp. 1.1% (Prev. 1.0%).

- Singaporean GDP Growth Rate YY (Q2 A) 5.7% vs. Exp. 5.3% (Prev. 6.0%).

- Australian Westpac Consumer Confidence Index (Jul) 83.9 (Prev. 80.6).

- Australian NAB Business Confidence (Jun) -5 (Prev. -14).

- New Zealand NZIER Business Confidence (Q2) 8% (Prev. -4%).

Loading...