NQ supported by ASML and SK Hynix strength, DXY and USTs lacklustre into PPI - Newsquawk US Market Open

- US struck Iran overnight, Trump said they will do so again on Wednesday night. Adding, they will hit power plants and bridges next week unless Iran negotiates.

- IRGC targeted weapons/storage in Bahrain and Kuwait, US positions in Jordan and the Fifth Fleet Command HQ. Iran said it is a mistake to think military action will force them to talk.

- ASML (+3.7%) reported Q2 earnings that beat estimates while raising its FY guidance above analyst expectations. Additionally, the Co. announced a partnership with Intel (INTC) for high-volume production of Intel 18A logic products using High NA EUV.

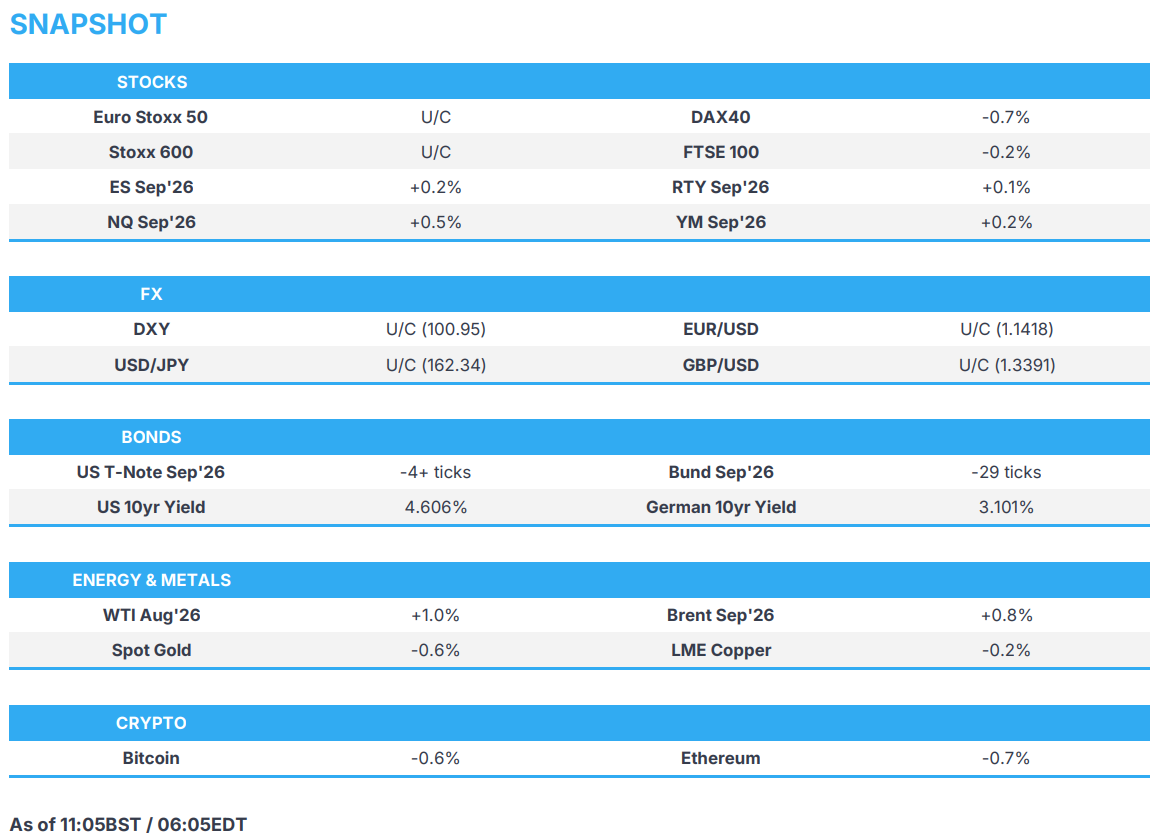

- US equity futures are firmer across the board, with NQ supported by ASML and SK Hynix upside overnight.

- DXY and Fixed Income rangebound ahead of a busy speaker slate.

- Crude benchmarks eke out mild gains, with another round of US strikes tonight.

- Looking ahead, highlights include US PPI (Jun), BoC Policy Announcement (Jul), Fed Beige Book (Jul), Speakers including Fed’s Williams, Musalem, Warsh & Cook, BoC Governor Macklem, BoE's Pill, Earnings from United Airlines, Johnson & Johnson, Morgan Stanley, PNC Financial Services, BNY Mellon.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 U/C) are broadly lower, with the outperformance in the AEX (+0.8%) following ASML earnings. Despite the lack of clear drivers for the underperformance, geopolitics persist, with US President Trump announcing that the US will conduct strikes again on Wednesday and threatening to hit power plants and bridges unless Iran starts to negotiate. Sectors are broadly negative. Consumer Products & Services (+1.2%) tops the sector pile, as positive Richemont earnings lift other luxury names, while Tech (+1.0%) also gains. To the downside lie Optimised Personal Care (-1.1%), Chemicals (-1.1%) and Telecoms (-0.8%).

- The highly anticipated ASML earnings did not disappoint. Top and bottom line figures beat estimates while raising its FY revenue guidance to EUR 43-45bln (exp. 39.4bln, prev. guided 36-40bln). Looking ahead to Q3, ASML projects sales of between EUR 11-12bln, above Jefferies' estimates of EUR 10.34bln. ASML stated that they are considering a 30% boost to EUV output for 2027 and again in 2028. Both Citi and JPMorgan highlighted this as a positive, with JPMorgan projecting it to add over EUR 65 in EPS in 2028. However, Citi points out that the 2027 production figure would amount to around 85 machines, which is below its forecast of between 90-100. Gains were seen as much as 7.4% at the start of trade, but has since pulled back to around 3.7%.

- US equity futures are firmer across the board. NQ (+0.5%) is the clear outperformer, helped by the ASML earnings and gains in SK Hynix overnight; however have come off in recent trade (in line with ASML). Banking earnings continue in the US, with Morgan Stanley on the docket.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s mixed against the Buck, which is flat on the day despite being off recent lows. AUD and GBP lead; NOK underperforms.

- DXY looks to breach 101.00 after lifting from recent lows in the wake of cool US CPI on Tuesday. As Fed Chair Warsh said during the House testimony on Tuesday, one series does not make a trend, so while bets are trimmed for an immediate hike (prev. markets saw a 50% probability of tightening in July), eyes remain on incoming data. In addition to the post-CPI bounce, the Buck is being helped by energy benchmarks, which remain elevated amid a lack of positive Gulf newsflow.

- NOK is the worst G10 performer after the Norges Bank’s preferred inflation gauge, CPI-ATE, came in cooler than analyst/Norges Bank forecasts. NOK saw immediate pressure on the release (which was originally scheduled for 10th July).

- AUD and GBP are the best-performing G10 currencies, helped by the above factor as the cooler-than-expected US CPI trimmed bets for near-term Fed tightening, increasing appetite for these high-yielders.

- For GBP specifically, the UK press suggested Energy Secretary Miliband was less-favoured in the race for Chancellor, now Foreign Secretary Cooper and Home Secretary Mahmood are favourites for the job. Markets think that Mahmood would be fiscally conservative given her view on immigration; however, she lacks experience in economic roles, whereas Cooper previously worked as Chief Secretary to the Treasury under Gordon Brown. GBP/USD +0.1% and either side of the 1.34 mark.

FIXED INCOME

- USTs remain contained, caught between CPI and Warsh. Bunds lower on energy, but off worst levels despite a sharp but ultimately short-lived decline in the early morning. Gilts opened on the backfoot, given energy.

- USTs flat in a narrow 108-24+ to 108-31+ band, fresh catalysts light. Commentary remains focused on June’s dovish CPI report and the subsequent hawkish Fed testimony from Chair Warsh. Today, we get more insight on both points via Warsh’s Senate testimony and US PPI for June. Additionally, Fed’s Williams (voter) is on the docket.

- Bunds lower by around 20 ticks, but are a similar amount clear of the 124.79 trough. A base that printed in a bout of somewhat short-lived bout of pressure this morning. No obvious catalyst behind that, though it did occur in tandem with modest DAX and EUR downside. Ongoing focus on pension reform may have contributed, given reporting earlier in Politico that suggested pension points could be reduced in some scenarios, saving multiple billions; though, the debate continues and won’t be resolved this week.

- Alternatively, or additionally, the German Finance Ministry outlined that some EUR 13bln or energy-related relief is planned for 2027, funding for that to be sourced from the climate relief package.

- Gilts opened lower by 16 ticks and have since moved lower to an 86.89 base, holding above the 86.87 and 86.42 lows from the last two sessions. Pressure the typical underperformance seen in Gilts when energy leads. No real relief from reports, such as the FT, suggesting that Miliband has lost the race to be Chancellor; though, outlets make clear that no decision has been made yet, ahead of Burnham becoming PM this weekend.

- Germany sells EUR 0.753bln vs exp. EUR 1.0bln 2.50% 2054, EUR 0.768bln vs exp. EUR 1.0bln 2.90% 2056 & EUR 0.759 vs exp. EUR 1.0bln 0.00% 2052 Bund.

- Australia sells AUD 700mln 4.50% Apr 2033 bonds b/c 4.29, avg yield 4.6620%.

COMMODITIES

- Geopolitics remains in focus, with US and Iran still conducting strikes. Markets appear to be accustomed to the ongoing attacks, with focus now on how transits through the Strait are being impacted. On that note, 11 vessels went through the passage, 9 of those used the Iranian-designated route. Yen Ling Song of S&P Global Energy wrote that “we are seeing significantly greater caution among shipowners and operators”, given the threat of Iranian strikes. On this front, traders have continued to price in another supply glut this month – and recent rhetoric from President Trump/Iran, does not point to a near term resolution.

- To recap, Trump warned that they would be striking Iran on Wednesday night, and threatened to hit power plants/bridges next week, unless Iran negotiates. Iran stated that it is a mistake to think military action will force them to talk.

- Crude benchmarks are modestly firmer this morning. Price action overnight was fairly rangebound, but then dipped in early European trade – benchmarks have remained near recent lows since. Brent Sept’26 traded within a USD 85.02-86.55/bbl range.

- Spot gold is a little lower this morning, but ultimately within the prior day’s ranges. Price action which appears to be a bit of pull-back from the extremes seen on Wednesday, following the cooler-than-expected CPI print. The yellow-metal currently holds above the USD 4k/oz mark, in a USD 4,017-4,062/oz range. Base metals hold a negative bias, as markets digested mixed Chinese data. 3M LME Copper traded within a USD 13,550-13,677/t range.

- US Private Inventory Data (bbls): Crude -0.6mln (exp. -2.7mln), Distillates +2.3mln (exp. +1.0mln), Gasoline -1.7mln (exp. +0.6mln), Cushing +0.2mln.

NOTABLE EUROPEAN HEADLINES

- Ed Miliband's opponents in the Labour Party believe he has failed his bid to become Chancellor, with current Home Secretary Mahmoud seen by some MPs as favourite to take the Chancellor role in Andy Burnham's new government, according to FT.

- OECD said the UK economy to grow 0.9% in 2026 and 1.1% in 2027, with risks tilted to the downside. Added that fiscal discipline is essential to the UK.

- German government is planning a EUR 13.3bln energy relief package for 2027, which will be used to assist businesses and consumers.

NOTABLE EUROPEAN DATA RECAP

- EU Industrial Production MoM (May) M/M -0.2% vs. Exp. 0.3% (Prev. 0.1%, Low. -0.2%, High. 1.0%).

- EU Industrial Production YoY (May) Y/Y -1.2% vs. Exp. 0.2% (Prev. 0.3%, Low. -0.9%, High. 1.4%).

- Spanish Inflation Rate YoY Final (Jun) Y/Y 3.2% vs. Exp. 3.2% (Prev. 3.2%).

- Spanish Inflation Rate MoM Final (Jun) M/M 0.6% vs. Exp. 0.6% (Prev. 0.1%).

- Swedish CPIF YoY Final (Jun) Y/Y 1.3% vs. Exp. 1.3% (Prev. 1.5%).

- Swedish CPIF MoM Final (Jun) M/M 0.3% vs. Exp. 0.3% (Prev. 0.9%).

- Norwegian CPI-ATE (Jun): 2.7% Y/Y (exp. 3.3%, prev. 3.4%), -0.1% M/M (exp. 0.5%, prev. 0.4%).

TRADE/TARIFFS

- EU Trade Commissioner Sefcovic said they are aiming to have the EU-India FTA implemented in 2027.

CENTRAL BANKS

- ECB's Nagel said from a monetary policy perspective, it remains advisable to react with caution but to act decisively if needed. Monetary policy will maintain its vigilant stance.

- ECB's Panetta said EZ inflation is currently around 3% and expected to remain above that level until early 2027. Risks linked to higher energy prices, tighter financial conditions and persistent geopolitical uncertainty appear to be only partially incorporated into market evaluations. Several indicators suggest the rise in equity markets seen after the Iran conflict is due to an underestimation of risks. ECB's goal is to keep inflation expectations firmly anchored, limiting indirect and second-round effects of shocks.

- ECB's Kocher said they are ready to take monetary policy actions at any time if needed, adding that the ECB will do what is needed to bring inflation to 2% in medium-term and no second round effects seen currently.

- ECB's Cipollone said that he is not currently seeing second round inflation effects, but monitors inflation expectations "very closely".

NOTABLE US HEADLINES

- Trump administration may pursue further executive action addressing China-related concerns over open-source AI models, according to Semafor citing an unnamed senior White House official.

- Alibaba’s (BABA) Qwen AI will be integrated into Apple (AAPL) Intelligence in China, according to Chinese state media.

GEOPOLITICS

MIDDLE EAST

- US President Trump said in a pre-recorded Fox News interview that they are beating up Iran badly and Hormuz has to stay open, while he added that strikes will continue until he says it is enough, as well as stated they will save energy targets for last and will ultimately hit energy targets. Trump also said they will hit Iran hard on Wednesday night, and that next week will get really bad for Iran, in which they will hit Iran's power plants and bridges next week unless Iran comes to the negotiating table. Furthermore, he said US officials spoke to Iran on Tuesday and told Iran that it better make a deal.

- US Central Command forces began launching an additional round of strikes against Iran at 15:00EDT/20:00BST on Tuesday, to continue degrading Iranian capabilities used to attack commercial shipping in the Strait of Hormuz, while CENTCOM later announced the completion of strikes against Iran.

- US struck Qeshm Island in southern Iran, and explosions were heard in the maritime area of eastern Hormozgan and Sirik, while explosions were heard in Bandar Abbas and Hengam Island. Explosions were also heard in Bampur and Chabahar in Iran, although Iran's semi-official news agency Tasnim noted officials denied reports of explosions in Chabahar, while explosions were reported in Iran's port city of Bandar Imam Khomeini, and a mineral water plant in Deloran was hit by three projectiles. Furthermore, reports noted that air defences around the Bushehr Nuclear Power Plant in Iran became active.

- IRGC said it targeted enemy weapons and parts storage in Bahrain and Kuwait, while it targeted a drone ramp in Kuwait's Ali Al Salem air base and targeted US positions at Jordan's Azraq base, as well as the US Fifth Fleet Command HQ, fuel facilities and equipment in Bahrain. IRGC said as long as the US evil stays in the region, not a drop of oil and gas will be exported from the region, and that US aggression will have no result other than delaying the opening of the Strait of Hormuz.

- Iran will respond to the US attacks, Tasnim reported.

- Iran's Deputy Foreign Minister Gharibabadi said the US is making a mistake if it thinks its military attacks and blockade will force them to request negotiations, but also commented that Iran's return to negotiations and tolerance regarding the Strait of Hormuz is possible. Furthermore, he said the MoU effectively no longer exists and that no country should expect Iran to continue implementing the terms of the memorandum.

- Israeli PM Netanyahu is reportedly to travel to Washington on Saturday evening, aiming to meet with US President Trump, Yedioth reported.

CRYPTO

- Bitcoin pulled back slightly from Tuesday's gains, currently trading either side of the USD 65k handle.

APAC TRADE

- APAC stocks traded with a positive bias as most major indices took impetus from the gains on Wall St, where sentiment was underpinned, and Fed rate hike bets were trimmed following softer-than-expected CPI data, while US President Trump also abandoned plans for a 20% Hormuz fee.

- ASX 200 eked out marginal gains with outperformance in miners following Rio Tinto's quarterly update, although the upside in the index was capped as defensives lag.

- Nikkei 225 rallied amid tech strength, but with further upside limited following weak Machinery Orders.

- KOSPI was boosted by the tech-related momentum and with SK Hynix shares up by a double-digit percentage as it played catch-up to the 27% surge in its ADRs.

- Hang Seng and Shanghai Comp diverged with the mainland lagging after a slew of mixed data releases, including Chinese GDP and activity data.

NOTABLE ASIA-PAC HEADLINES

- China announced a five-year plan to boost consumption and targets CNY 60tln yuan in retail sales by 2030, according to Nikkei.

- China's stats bureau deputy head said China's CPI and PPI are in reasonable ranges and hard won given most countries face big price increases, while the official added that China's energy supplies are sufficient, production is stable, and imports are under control. Furthermore, it was stated that the Q2 GDP growth slowdown is due mainly to short-term factors and external factors, while H1 GDP growth lays a good foundation for achieving the full-year growth target.

- Japan added a footnote on BoJ autonomy to its revised fiscal policy draft, Bloomberg reported.

- Japanese PM Takaichi said FX rates should be determined by the market; boosting international competitiveness will boost the credibility of JPY.

- India announced INR 1.28tln new semiconductor manufacturing plan, according to reports.

NOTABLE APAC DATA RECAP

- Chinese GDP Growth Rate QoQ (Q2) Q/Q 0.9% vs. Exp. 0.9% (Prev. 1.3%, Low. 0.8%, High. 1.2%).

- Chinese GDP Growth Rate YoY (Q2) Y/Y 4.3% vs. Exp. 4.4% (Prev. 5%, Low. 2.7%, High. 4.8%).

- Chinese Retail Sales YoY (Jun) Y/Y 1.0% vs. Exp. -0.1% (Prev. -0.6%, Low. -1.2%, High. 0.7%).

- Chinese Fixed Asset Investment (YTD) YoY (Jun) Y/Y -5.7% vs. Exp. -5% (Prev. -4.1%, Low. -6.0%, High. -2.5%).

- Chinese Industrial Production YoY (Jun) Y/Y 5.3% vs. Exp. 4.7% (Prev. 4.5%, Low. 4.3%, High. 5.5%).

- Chinese Unemployment Rate (Jun) 5.0% vs. Exp. 5.1% (Prev. 5.1%).

- Chinese M2 Money Supply YoY (Jun) Y/Y 8% vs. Exp. 8.5% (Prev. 8.6%).

- Chinese Outstanding Loan Growth YoY (Jun) Y/Y 5.2% vs. Exp. 5.4% (Prev. 5.5%).

- Chinese Total Social Financing (Jun) 3360B vs. Exp. 3770B (Prev. 2030B).

- Japanese Machinery Orders MoM (May) M/M -12.4% vs. Exp. -4.2% (Prev. 8.7%, Low. -6.7%, High. 0.4%).

- Japanese Machinery Orders YoY (May) Y/Y -1.9% vs. Exp. 12.9% (Prev. 15.6%, Low. 0.6%, High. 17%).

Loading...