NQ tentative approaching SK Hynix US debut; Japanese assets bid as FinMin touts domestic investment measures - Newsquawk US Market Open

- Mediators are working to get the US and Iran back at the negotiating table, CNN reported, citing sources, later echoed by Axios.

- Brent is softer by around USD 0.20/bbl, with the market essentially waiting for a resumption of negotiations or strikes.

- Japanese assets lead after Finance Minister Katayama said pension funds should be encouraged to invest more in the domestic market.

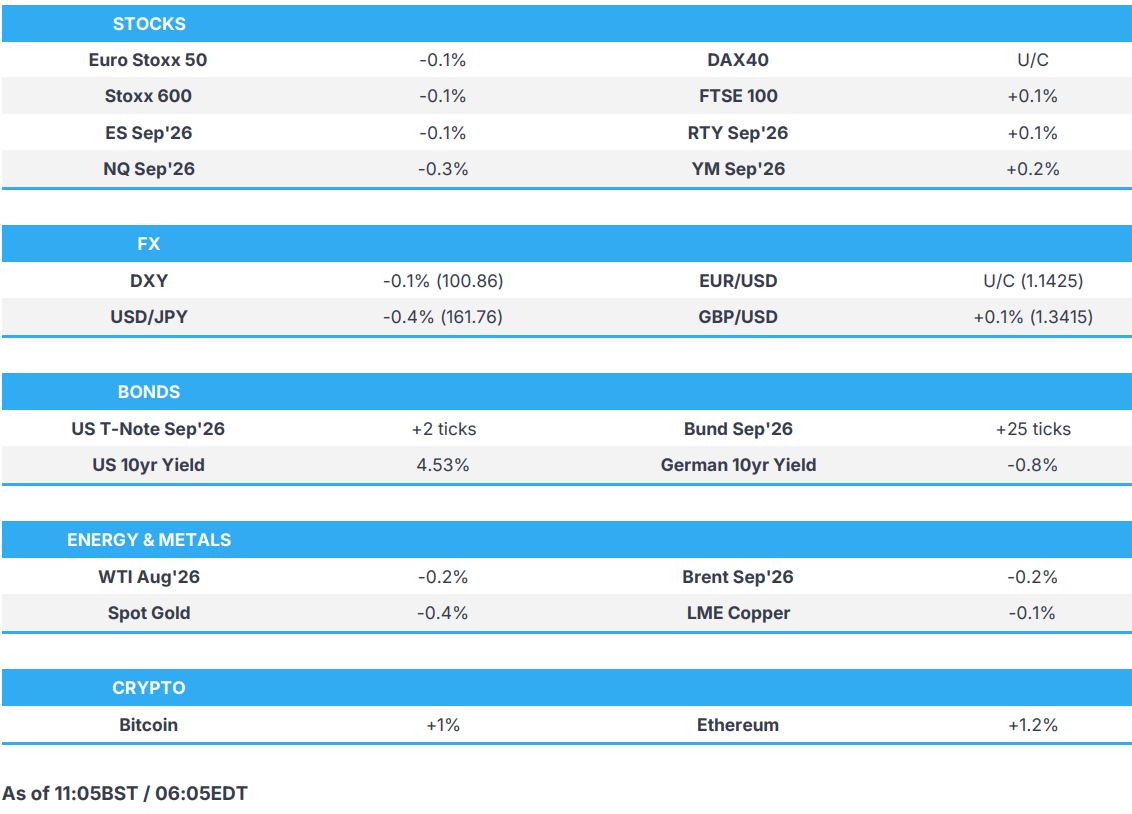

- European bourses are on a modestly firmer footing, Euro Stoxx 50 +0.1%. US futures are mixed; NQ lags, potentially ahead of SK Hynix's ADR debut on the 13th.

- USD under pressure, JPY leads given the above, NZD continues to climb, CAD flat into its jobs report.

- Looking ahead, highlights include Canadian Jobs Report (Jun). Earnings from Delta Air Lines and Credit Ratings from Fitch on the Netherlands, Morningstar DBRS on Switzerland and Scope Ratings on Japan.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.1%) began the session on a weaker footing despite APAC optimism ahead of SK Hynix’s US debut (KOSPI +2.5% at close). Geopolitical newsflow quietened overnight, as such energy benchmarks are off best levels with Brent around USD 75/bbl. IBEX continues to outperform after it slumped earlier in the week (also has more defensive composition), while tech heavy AEX is the worst performer as top constituent ASML looks to SK’s ADR debut.

- European sectors opened with a positive bias and continue this way. Comms and Travel/Leisure outperform, Tech and Energy are the laggards for the above factors. In terms of individual movers, Infineon (-2.7%) said it is raising prices in some segments; EasyJet (+14%) agreed to a GBP 5.7bln takeover by Apollo at 715p/shr; Vodafone (+11%) French telecom tycoon Niel acquired E&’s stake for a GBP 0.15/shr premium.

- Stateside, index futures pull back a touch after solid gains on Thursday. NQ (-0.6%) is the laggard after outperformance on Thursday, ES and RTY are resilient and only post modest -0.2% losses.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are mixed against the Buck. JPY leads after FinMin Katayama touted measures to promote domestic inflows, Kiwi continues to eek gains post-RBNZ as markets look to price a cumulative 50bps tightening by year end and NOK is the worst performer after broadly cool inflation data.

- USD a touch weaker as JPY firms alongside the tempered recent Gulf updates. Geopolitical newsflow quietened overnight, with energy benchmarks off best levels with Brent around USD 75/bbl, about 5 Bucks off the week’s highs. DXY slipped throughout APAC as the JPY firmed, but found buyers below 21DMA at 100.85 which has proven support in recent sessions.

- JPY digests updates from FinMin Katayama who said she was to pursue steps to promote investment in Japanese assets by GPIF and others. This, on the face of it, would be a textbook tactic to encourage domestic investment and passively limit outflows, especially with a large composition (50%) of pension funds allocated to foreign investments. Several strategists note this is a positive sign in attempts to shore up the currency; though CapEco said “Much of its domestic bond portfolio is invested passively, and shifting more assets into domestic bonds would come at a sizeable fiscal cost if it requires selling equities”, and others highlight Katayama is not in a position to direct changes, it would be under the jurisdiction of the Labour Ministry. USD/JPY gradually trundled lower from a 162.50 peak, to mark a trough below 161.30 (session low 161.28), with a modest kneejerk lower on not-too-surprising BoJ sources. ING notes the JPY-funded carry keeps risks to the upside for the pair.

- NOK is the clear underperformer vs. both the USD and SEK after the soft inflation data series. Most metrics cooled beneath expectations, core Y/Y the sole figure rising above consensus, albeit unch. from May. CPI-ATE, the Norges Bank’s preferred gauge of inflation fell was 2.9%, well below the Bank’s estimate of 3.3%, will likely provide conviction for doves with the bank likely to remain on hold in the August meeting; then tighten in September should the next (August) CPI metrics not provide a dovish surprise. NOK/SEK fell from a 0.9940 peak to mark a trough at 0.9882. 8th July low at 0.9861 is the next level below.

- South Korean Forex Authority said USD/KRW market remains misaligned with economic fundamentals.

FIXED INCOME

- Overall, fixed benchmarks are firmer in reaction to the modest but increasing pullback seen in the energy space overnight and as JGBs lead on domestic updates.

- JGBs got to a high of 127.76 in the European morning, continuing the overnight rally after comments from Japanese Finance Minister Katayama, who said that pension funds should be encouraged to invest more in the domestic market. Commentary that underpinned Japanese assets across the board, and sent the 10yr yield lower by around 16bps on the day, down to 2.71% and now essentially flat on the month, reversing from the 2.89% YTD high.

- Commentary that also lifted peers at the time. While the shift would be a positive for the Japanese market generally, there are a few unknowns, most pertinently being whether Katayama can make such an announcement as the GPIF is under the Labour Ministry, not the Finance Ministry. As such, for FX in particular, there is an argument that Katayama’s commentary is conducting another form of jawboning, and therefore the move may well fade in the days/weeks ahead, unless a relevant official to the GPIF (i.e. Ueno, or PM Takaichi) backs the shift publicly.

- USTs got to a 109-12 peak in the early morning, as energy hit a low and the JGB-driven move topped out. Since, newsflow has been particularly light with the market essentially waiting for a resumption of negotiations or strikes, though as is often the case we might not get clarity on the next step until the weekend.

- Bunds followed suit, peaking at 125.74 with gains of around 35 ticks. Specifics limited. Continued focus on the EU funding plans, and the lack of agreement on the next 7yr plan is arguably supporting EGBs for net-contributing nations, as no agreement would see the current EUR 1.4tln figure continue as opposed to the planned uplift to EUR 2tln.

- Gilts opened lower by a few ticks, before then swiftly moving above the 88.00 mark to a 88.07 peak, in-fitting with the above. Action that leaves it just above Wednesday’s high but someway shy of the 88.93 opening level at the start of the week. Last night the first tally was done for the Labour nominations, and while the count theoretically leaves space for a challenger it is not realistic and therefore Burnham is now formally, for all intents and purposes, the incoming UK PM.

- Italy sold EUR 7.5bln vs exp. 6.0-7.5bln 3.00% 2029, 3.35% 2033 & 3.95% 2041 BTPs.

- China's MOF sold 2-year and 3-year bonds. 2-year sold at 1.2305%. 3-year sold at 1.2629%.

- Australia sold AUD 900mln 1.75% 2032 AGBs: b/c 3.16x (prev. 4.10x), average yield 4.6189% (prev. 4.1987%).

COMMODITIES

- The geopolitical situation appears to have calmed down this morning, with no fresh reports of strikes on Iran/regional neighbours. However, the situation remains tense given some of yesterday’s actions. Iran reported a couple of strikes at two military bases, but US officials denied any involvement of this. Despite the earlier reports, some Iranian officials denied any explosions taking place.

- Despite the recent flare-up, a US official stated that the US remains committed to a resolution with Iran and technical discussions are ongoing. This, alongside the lack of new strikes overnight has led to a bearish bias in crude benchmarks this morning. Brent Sep’26 (-0.2%) is only mildly lower and trades at the towards the mid-point of a USD 75.36-76.95/bbl range. Some mild downticks were seen in the benchmark after the release of the IEA Oil Market Report. It cut 2026 oil demand, noted that the UAE is upping its supply and oil transits are passing through the Hormuz.

- Spot gold (-0.6%) trades lower this morning, hovering on either side of the USD 4.1k/oz mark; currently within a USD 4,094-4,134/oz band. The range today is very thin, amidst the lack of pertinent newsflow and fairly steady USD. Elsewhere, base metals hold a negative bias. 3M LME Copper trades within a USD 13,455-13,562/t range. For aluminium, analysts at Morgan Stanley recently stated that they see a smaller supply deficit in 2026, and likely to move into a surplus from 2027.

- Oman has set its OSP at USD 69.29/bbl for September delivery.

- IEA OMR: forecasts global oil demand in 2026 to fall by 1.05mln BPD (prev. exp. 1.12mln); global oil demand recovery is under way. Global oil demand estimated at 103.46mln bpd for 2026 and is expected to grow by 2mln BPD in 2027 and reach 105.47mln BPD. Oil supply may expand 7.5mln BPD in 2027 if transits improve.

- A fire broke out at two oil product storage facilities due to a UAV attack in the Rostov region, according to the governor; fires are being pushed out in Taganrog's Seaport, reported no injuries.

- Krasnodar task force said a fire has broken out at the Ilsky oil refinery due to the fall of a drone's debris, Interfax reported.

- QatarEnergy set August Marine Crude OSP at Oman/Dubai -USD 5/bbl; Land Crude OSP at -USD 4.50/bbl, according to a pricing document.

- China National Summer grain output reached 150.7mln tonnes, +0.7% Y/Y.

TRADE/TARIFFS

- China's MOFCOM announces a temporary ban on helium exports.

- US White House announces the adjustment of imports of commercial aircraft, jet engines, and aircraft and engine parts into the US; no immediate tariffs be imposed under section 232 to address the threatened impairment to the national security.

NOTABLE EUROPEAN HEADLINES

- UK Chancellor Reeves is to announce a new City "skills compact" that will commit financial firms to retraining thousands of workers for the AI revolution, The Guardian reported.

NOTABLE EUROPEAN DATA RECAP

- Italian Industrial Production MoM (May) M/M -0.3% vs. Exp. 0.1% (Prev. 0.5%).

- Italian Industrial Production YoY (May) Y/Y 1.1% vs. Exp. 1.3% (Prev. 1.3%).

- French Inflation Rate YoY Final (Jun) Y/Y 1.8% vs. Exp. 1.8% (Prev. 2.4%).

- French Inflation Rate MoM Final (Jun) M/M -0.3% vs. Exp. -0.2% (Prev. 0.1%).

- Norwegian Core Inflation Rate MoM (Jun) M/M 0.4% vs. Exp. 0.5% (Prev. 0.4%).

- Norwegian Core Inflation Rate YoY (Jun) Y/Y 3.4% vs. Exp. 3.3% (Prev. 3.4%).

- Norwegian Inflation Rate YoY (Jun) Y/Y 2.7% vs. Exp. 3.2% (Prev. 3.1%).

- Norwegian Inflation Rate MoM (Jun) M/M -0.2% vs. Exp. 0.3% (Prev. 0.2%).

- German Inflation Rate MoM Final (Jun) M/M -0.3% vs. Exp. -0.3% (Prev. -0.2%).

- German Inflation Rate YoY Final (Jun) Y/Y 2.3% vs. Exp. 2.3% (Prev. 2.6%).

- BRC said the number of people visiting British shops fell 3.4% in June, due to the heatwave keeping shoppers indoors.

CENTRAL BANKS

- BoJ reportedly to keep rates unchanged in July but maintain policy guidance and also raise growth outlook, according to sources.

- PBoC injected CNY 20bln via 7-day reverse repos with rate maintained at 1.40%.

- PBoC set USD/CNY mid-point at 6.7989 vs exp. 6.7931 (prev. 6.8036); strongest midpoint since February 2023.

- NBP's Wnorowski said signal about possible motion to cut interest rates in September is premature; do not see space for more than one cut this year.

NOTABLE US HEADLINES

- US President Trump reportedly fired all 3 federal election commission members.

GEOPOLITICS

RUSSIA-UKRAINE

- Ilsky (138k BPD), Russia oil refinery fire has now been extinguished.

MIDDLE EAST

- Qatar, Pakistan and other regional mediators are trying to de-escalate tensions between the US and Iran and revive negotiations on a nuclear deal, Axios reported citing sources.

- A member of the National Security Commission of Iran's parliament said the UAE will pay the price for cooperating with America.

- A US official said talks with Iran will continue, Fox's Hasnie reported; The administration is still committed to finding a resolution so technical talks continue to prevent Iran from having a nuclear weapon. Iran's attacks on ships in the streets are acts of terrorism. The MoU is performance-based, and Iran's actions constitute failed performance at an unacceptable level.

- Israel reportedly shared new intelligence with the US that indicated a new Iranian plan to kill US President Trump, WSJ reported citing sources.

- A US official said the US remains committed to a resolution with Iran and technical discussions are ongoing.

- Turkey has decided it will not join the Canadian Defence Bank initiative at this point, sources suggest.

- The Israeli army said "we will continue our operations to eliminate any threat and will not allow Hezbollah to harm us", Al Jazeera reported.

- Al Jazeera reported that Israeli forces are conducting extensive demolitions in southern Lebanon.

- Krasnodar task force said a fire has broken out at the Ilsky oil refinery due to the fall of a drone's debris, Interfax reported.

- Pakistan has begun mediating between Libya's rival eastern and western data centres with the backing of the US and Saudi Arabia, Nikkei reported citing sources.

- Lebanese media reported of new Israeli drone strikes in southern Lebanon, Tasnim reported.

- Four Japanese-linked vessels remain in the Persian Gulf, Kyodo reported.

- Konarak Governor said this area was targeted by enemy fighter jets in two stages on Thursday evening.

CRYPTO

- Bitcoin is a little firmer and trades back towards USD 64.5k; Ethereum also extends higher but still remains shy of USD 1.8k.

APAC TRADE

- Asia-Pac stocks traded entirely in the green, as they followed the tech-led gains seen stateside. Military strikes continued on Thursday, but energy prices and equity markets seemed to have brushed it aside and instead took a stronger liking to President Trump’s comments, in which he said Iran had reached out to the US and wanted to make a deal, easing concerns over a further escalation that could threaten energy infrastructure. To note, the Taiwan markets were closed due to the typhoon, and worries of the typhoon hitting China and Japan.

- ASX 200 initially opened with modest losses but has since reversed and printed modest gains. Metals & Mining topped the sector pile, cutting 4 consecutive days of losses, while Health Care was the sector laggard.

- Nikkei 225 gained, with SUMCO leading the way as it benefited from the semiconductor strength stateside. On the earnings front, Seven & I and Fast Retailing both posted strong earnings and raised their FY guidance; however, shares traded lower after highlighting the effects of a weaker yen.

- KOSPI surged, helped by gains in Samsung Electronics while SK Hynix shares traded choppy ahead of its US ADR listing. The choppiness in SK Hynix comes as investors position themselves for the ADR, with analysts stating that the US ADR may be preferred over its domestic listing, due to US ADRs commonly trading at a premium (typically at a 5-15% premium).

- Shanghai Comp. and Hang Seng were firmer, with another set of IPOs in Hong Kong, resulting in 15 listings this week. Today, markets were focused on Nexchip Semiconductor. The IPO price was set at HKD 32.30/shr, and shares rose at the open and briefly topped HKD 36/shr but have since come off.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama said they are to pursue steps to promote investment in Japanese assets by GPIF and others.

- Japanese Finance Minister Katayama does not comment on specific bond yield levels; specific monetary tools are up to the BoJ, closely monitoring economic indicators and market situations. Important that the government position secures market confidence. Will ensure fiscal sustainability to gain market trust. BoJ can adjust monetary policy regardless of what the government said. Predicts gradual increases in interest rates as the government is engaged in a proactive fiscal policy. Want to speed up discussions on expansion of JGB products targeting households.

- Japan's GPIF spokesperson said they are aware of Finance Minister Katayama's comments but declines to comment.

- Japan's Economy Minister Kiuchi said the government has consistently communicated its stance of taking policy that heeds to fiscal sustainability.

NOTABLE APAC DATA RECAP

- Japanese PPI MoM (Jun) M/M 0.4% vs. Exp. 0.3% (Prev. 0.9%).

- Japanese PPI YoY (Jun) Y/Y 7.1% vs. Exp. 6.8% (Prev. 6.3%).

Loading...