Oil pares initial WSJ-related relief - Newsquawk US Market Open

- US President Trump reportedly told aides he's willing to end the war without reopening the Strait of Hormuz, according to the WSJ.

- IRGC's public relations channel reported the announcement that the Strait of Hormuz is fully under the control of IRGC soldiers, and "the slightest movement of the enemies will be hit by missiles and drones", adding that "the operation continues."

- Crude rangebound, while Oman's crude OSP for May nearly doubles from April.

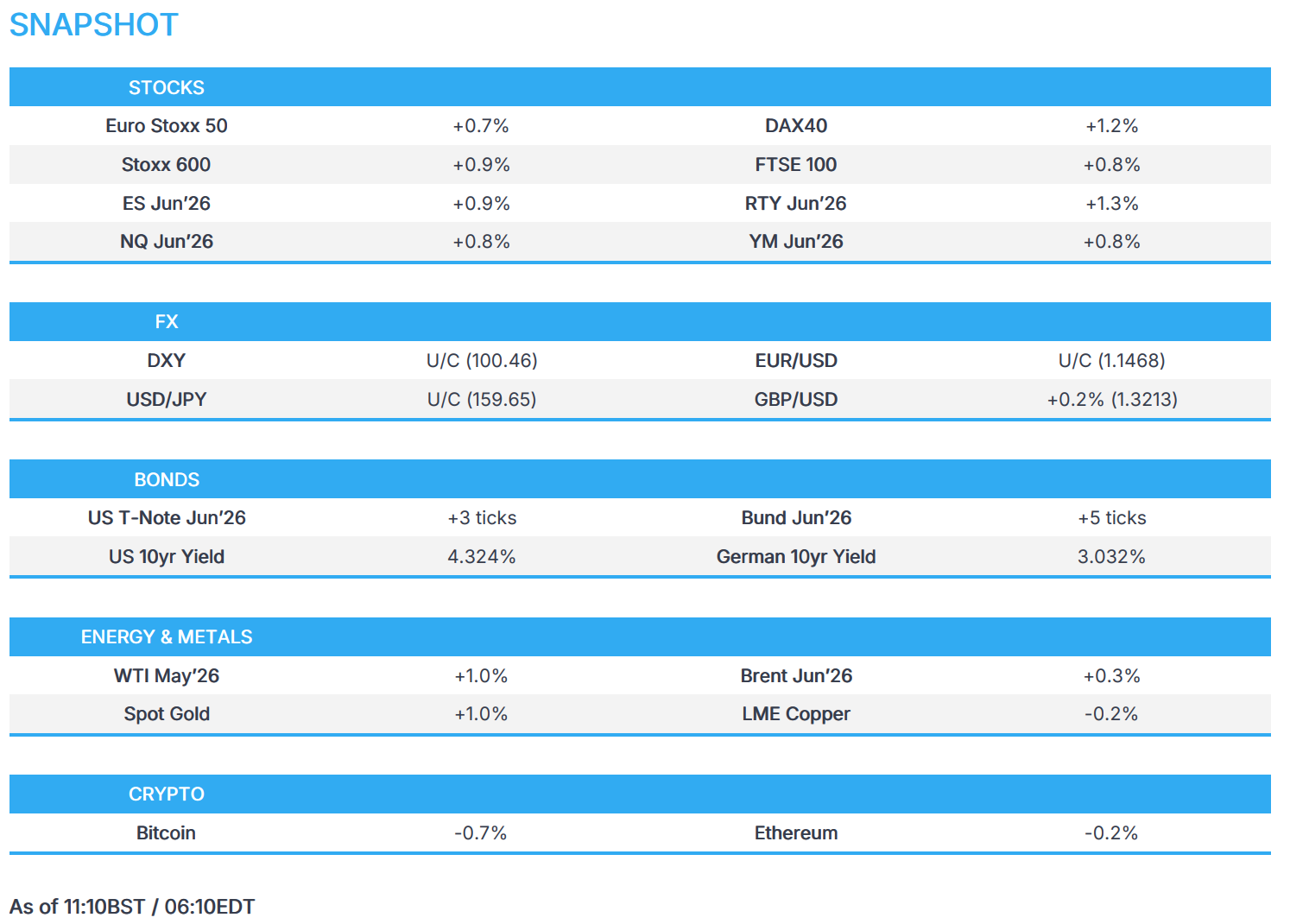

- European equities continues to rebound, ULVR LN gains ahead of possible MKC announcement; US equity futures gain.

- DXY lacks direction, GBP outperforms slightly while EUR moves a touch lower following cooler-than-expected EZ HICP.

- Fixed income lifts as energy prices moderate, Bund lifts as EZ HICP underscores ECB's wait-and-see approach.

- Looking ahead, highlights include Canadian GDP Prelim. (Feb), US JOLTS (Feb), Australian Manufacturing PMI Final (Mar). Speakers include Fed's Goolsbee, Schmid, Barr & Bowman. Earnings from Nike.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.9%) continue to rebound, as the STOXX 600 bounces out of correction territory. The IBEX 35 and DAX 40 outperform, while the AEX is the slight laggard due to losses in ASML.

- European sectors are entirely in the green, ex. Energy. Basic Resources and Financial Services top the sector pile. While a rebound in metals prices supports Basic Resources, UBS is amongst the banks supporting financials after the FT reported that Swiss lawmakers have signalled some compromise on its USD 22bln capital plan.

- US equity futures are printing decent gains pre-cash. RTY continues to hold up compared to the ES and NQ, with the bearish 20-,200-SMA yet to occur and the RSI staying clear of oversold territory.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY lacks direction, and holds within a 100.30-100.64 range; the peak for today was made overnight, but then sank from these levels on reports via the WSJ, which suggested that US President Trump told aides he's willing to end the war without reopening Hormuz. A factor which clearly indicates some early signs of easing tensions, though it raises concerns regarding the future governance of the Strait itself. DXY swung from peaks to troughs within an hour of the report, before then gradually pushing back towards the mid-point of the aforementioned range, as the European session got underway. Focus from a US standpoint now turns to US JOLTS, which are expected to ease to 6.87mln (from 6.946mln). A slew of Fed speakers are also on the docket, including Bowman, Barr, Goolsbee and Schmid.

- G10s are mixed against the USD. GBP is the marginal outperformer, potentially benefiting from the lower energy prices, which somewhat alleviates growth-related concerns, at least for now. Sticking on the growth front, Final UK GDP growth in Q4 printed 1% Y/Y (exp. 1%, prev. 1.2%) – a report which spurred no move in Cable. To the bottom of the pile reside the CHF and Kiwi, albeit losses are incremental at this stage.

- Elsewhere, EUR is steady, and was little moved to a resilient German jobs report, whilst a cooler-than-expected EZ inflation metric spurred some pressure in the single currency. In a bit more detail, headline Y/Y jumped to 2.5% (prev. 1.9%) and a touch beneath the consensus. As is the case across Europe, the surge in inflation has been attributed to the recent strength in energy prices; for reference, the core figure actually cooled from the prior to 2.3% (prev. 2.4%). EUR/USD fell to 1.1462 post-day before scaling back a touch. The ECB will welcome this report, given that it favours a “wait and see" approach.

- JPY is flat this morning, after relative outperformance in the prior session, spurred by jawboning. USD/JPY currently resides within a 159.48-159.97 range, and towards the lower end of the prior day’s session. Overnight, the release of softer-than-expected Retail Sales and slower Tokyo inflation had a limited impact on the JPY – ING opines that the inflation figure will not “deter BoJ’s April hike”; analysts opine that the trifecta of 1) surging oil prices, 2) weak JPY and 3) rising Shunto wage growth, all play in favour of a near-term hike. Attention now turns to the Tankan survey on Wednesday, a report which policy members brought to focus at the last BoJ confab.

FIXED INCOME

- Fixed income on a firmer footing as energy benchmarks initially pulled back, though WTI remains above USD 100/bbl, Brent above USD 105/bbl and Dutch TTF north of USD 50/MWh. The main update came via the WSJ, reporting that US President Trump told his aides that he is willing to end the conflict even without reopening the Strait of Hormuz. The move towards potentially ending the conflict has weighed on energy and, in turn, pressured yields. However, the uncertainty around Hormuz means the energy, and by association, price risks have not meaningfully diminished at this point.

- USTs are firmer but off best levels, and within 110-22+ to 111-02 parameters. Ahead, the docket is headlined by Fed speak; however, the events/topics involved somewhat diminish the likelihood of pertinent updates.

- Bunds follow global action. Initially stronger, before giving back some of the earlier gains heading into the EZ inflation measures for March – a report which encapsulates the early impact of the Iran war, and the surge in energy prices. In brief, headline Y/Y was cooler-than-expected, and plays in favour of the ECB’s “wait and see approach”. In reaction, Bunds ticked higher by a handful of ticks, though the move proved fleeting.

- Gilts in-fitting with peers. Firmer by around 50 ticks at best but have given up around half of that and are below the 88.00 mark in 87.65-88.23 parameters. No reaction to the final Q4 GDP series, or a slight upward revision to the 2025 total.

- Germany sells EUR 3.811bln vs exp. EUR 5.0bln 2.10% 2028 Schatz: b/c 1.5x (prev. 1.61x), average yield 2.62% (prev. 2.72%), retention 23.78% (prev. 22.6%).

- BoJ said it plans to buy JPY 255bln of 1–3 year JGBs three times a month in April–June (prev. JPY 270bln, three times); JPY 230bln of 3–5 year JGBs three times a month (prev. JPY 245bln, three times). Plans to buy JPY 80bln of 10–25 year JGBs three times a month in April–June (prev. JPY 95bln, three times). Plans to buy JPY 75bln of JGBs 25+ years of maturity two times a month (prev. JPY 75bln, two times).

- Japan sold JPY 2.15tln in 2-year JGBs; b/c 3.54x (prev. 3.32x); average yield 1.370% (prev. 1.244%).

- Australia sold AUD 1bln October 2037 bonds, b/c 3.43, avg. yield 5.0865%.

- Aluminium Corporation of China (2600 HK) is said to be considering an USD 800mln USD-denominated offshore bond sale.

COMMODITIES

- Crude futures are incrementally firmer this morning after reversing earlier losses despite light newsflow. WTI May’26 resides in a USD 100.83-107.15/bbl range, whilst Brent June’26 holds within a USD 104.72-109.99/bbl. Worth noting that in recent trade benchmarks are moving a touch higher, extending further into the green.

- Overnight, the complex dipped after the WSJ reported that US President Trump told aides he is willing to end the US military operation in Iran even if the Strait of Hormuz is not reopened. Do note the IRGC continues to provide hardline commentary, with attacks on Gulf countries ongoing. Geopolitics aside, some strength was seen in the crude complex after data showed that Oman’s crude OSP jumped USD 55.90/bbl.

- Spot gold rose after comments from Fed Chair Powell and Williams indicated policy remains in a good place, helping to temper rate-hike expectations; the bullion climbed before paring gains to trade near USD 4,555/oz, with the yellow metal currently holding in a USD 4,482.66-4,619.25/oz range at the time of writing. Goldman Sachs said gold could reach USD 5,400/oz by year-end, citing low speculative positioning, expectations for two Fed rate cuts and ongoing central bank demand, with official-sector buying seen at around 60 tonnes per month.

- Copper futures marginally benefitted from hopes of an earlier end to the Middle East conflict and after Chinese PMI data topped forecast, but then pared gains given the ongoing uncertainty in the Middle East conflict. 3M LME copper trades in a USD 12,122.00- 12,286.95/t range. Aluminium once again outperforms on the LME amid supply woes from the Middle East after Emirates Global Aluminium and Aluminium Bahrain were both targeted by Iran.

- Oman's crude OSP at USD 124.05/bbl for May (vs USD 68.15/bbl for April), +USD 55.90/bbl, GME data shows.

- EU countries should prepare for prolonged disruption to energy markets from the Iran war, the EU energy commissioner said in a letter to EU energy ministers. Immediate impact on EU energy security of supply remains contained. EU countries should delay any non-emergency refinery maintenance. Countries should avoid measures that would increase fuel consumption or curb EU refinery output.

- South Africa's Finance Minister is considering lowering the fuel levy, with the decision to be announced on Tuesday, according to a Government official.

- Libya's National Oil Corporation said full production resumed at the Sharara and El Feel oilfields.

- Guyana oil production averaged 915k BPD in January and 918k BPD in February.

- Goldman Sachs expects gold to reach USD 5,400/oz by the end of 2026. Low speculative positioning and two Fed rate cuts to support this view. Projects around 60 tonnes of central bank buying per month.

TRADE/TARIFFS

- USTR Greer slams WTO after ecommerce tariff talks fail, according to FT.

NOTABLE EUROPEAN HEADLINES

- German institutes to cut 2026 economic growth forecasts amid the Iranian war, Reuters sources suggest; 2026 growth outlook seen at 0.6% (prev. 1.2%), 2027 growth seen at 0.9% (prev. 1.4%). CPI is seen at 2.8% for 2026 and 2027. Iranian war and energy costs were cited as the reasons for the cuts.

NOTABLE EUROPEAN DATA RECAP

- Full Newsquawk EZ HICP Review

- EU Inflation Rate MoM Flash (Mar) M/M 1.2% vs. Exp. 1.4% (Prev. 0.6%).

- EU Inflation Rate YoY Flash (Mar) Y/Y 2.5% vs. Exp. 2.8% (Prev. 1.9%, Low. 2.4%, High. 3.1%).

- EU Core Inflation Rate YoY Flash (Mar) Y/Y 2.3% vs. Exp. 2.4% (Prev. 2.4%, Low. 2.2%, High. 2.6%).

- French HICP Prelim. M/M 1.1% vs. Exp. 1.00% (Prev. 0.70%, Low. 0.8%, High. 1.2%).

- French HICP Prelim. Y/Y 1.9% vs. Exp. 1.90% (Prev. 1.10%, Low. 1.5%, High. 2.1%).

- Italian Inflation Rate MoM Prel (Mar) M/M 0.5% vs. Exp. 0.5% (Prev. 0.7%).

- Italian Inflation Rate YoY Prel (Mar) Y/Y 1.7% vs. Exp. 2.3% (Prev. 1.5%).

- UK GDP Growth Rate YoY Final (Q4) Y/Y 1% vs. Exp. 1% (Prev. 1.2%, Low. 1%, High. 1%).

- UK GDP Growth Rate Final (Q4) Q/Q 0.1% vs. Exp. 0.1% (Prev. 0.1%, Low. 0.1%, High. 0.2%).

- German Retail Sales YoY (Feb) Y/Y 0.7% vs. Exp. 1% (Prev. 1.2%).

- German Retail Sales MoM (Feb) M/M -0.6% vs. Exp. 0.3% (Prev. -0.9%, Low. -0.3%, High. 1.0%).

- German Import Prices MoM (Feb) M/M 0.3% vs. Exp. 0.2% (Prev. 1.1%).

- German Import Prices YoY (Feb) Y/Y -2.3% vs. Exp. -2.1% (Prev. -2.3%).

- Polish Inflation Rate MoM Prel (Mar) M/M 1.0% exp. 1.3% (prev. 0.3%).

- Polish Inflation Rate YoY Prel (Mar) Y/Y 3.0% vs exp. 3.2% (prev. 2.1%).

CENTRAL BANKS

- Fed's Williams (voter) said uncertainty around inflation path is 'high' but the economy has been more resilient than expected and the base outlook for the economy has been good. Tariffs and Iran war will push up headline inflation. Expects the unemployment rate to edge down this year and next. Economy facing ‘unusual set of circumstances’. Expects higher headline inflation near term on war and tariffs. War could both push up inflation, and depress growth. Inflation expectations consistent with 2% inflation. Expects US GDP to be 2.5% this year amid help from various factors. Expects inflation to end this year at 2.75%, and back to 2% in 2027. Economy has been resilient among changes. No signs of second round inflation impact from tariffs. Low hiring rate might be boosting economic pessimism. Job market sending out mixed signals.

- ECB's Muller said it is probable that rates will rise in the coming quarters, an April rate hike cannot be ruled out and reiterates that a hike may be needed if energy prices stay high.

- ECB’s Panetta warns against second-round wage effects; says monetary policy is better positioned vs 2022.

- RBA Minutes from March meeting stated that board members agreed financial conditions needed to be restrictive and that a further tightening would likely be needed but disagreed on whether to hike at the meeting. Agreed it is not possible to predict the future path of the cash rate with any confidence given the Middle East conflict. Rise in oil prices increased risk inflation would remain above target for a prolonged period. Oil prices around USD 100 would lift annual CPI inflation to around 5% in the June quarter. Rate hike could reduce the risk oil shock would flow into inflation expectations.

- PBoC is to maintain moderately loose monetary policy with stronger counter-cyclical adjustments, reiterates to make use of various tools in monetary policy control and to maintain ample liquidity and keep CNY stable.

- BoK Governor nominee Shin sees Middle East crisis as risk to the Korean economy and said inflationary pressure from extra budgets is limited, adds KRW liquidity is good and external factors affecting KRW have improved considerably.

GEOPOLITICS

MIDDLE EAST

- US President Trump tells aides he's willing to end the war without reopening Hormuz, according to the Wall Street Journal.

- The IRGC announced that the Strait of Hormuz is fully under the control of its soldiers, and "the slightest movement of the enemies will be hit by missiles and drones", adding that "the operation continues", IRGC's public relations channel reported.

- Strait of Hormuz to be run by multinational coalition under White House plan, The Telegraph reported; Second proposal put forward by Pakistan and regional powers. Rubio stressed there would be “no fees, and free circulation” through the key shipping route, according to one interpretation of his intervention.

- Israeli PM Netanyahu said it is possible to bypass the Strait of Hormuz issue and that economic interests exist to ensure free flow of oil and gas, while ideas have been proposed for post-war transfer of energy from Persian Gulf to Mediterranean ports.

- Israeli PM Netanyahu said Iran's enriched uranium is Trump's focus right now and US is leading military options to open Strait of Hormuz. Refuses to set any timeline on ending the Iran war.

- Israel Military Spokesperson said "we are prepared to keep operating for weeks to come".

- Houthis in Yemen are monitoring American movements at bases in the Horn of Africa that may signal an imminent American move in the Red Sea, according to Israeli Radio journalist. According to the Yemeni intelligence sources, Washington intends to create a maritime security zone in the Red Sea region and the base in Djibouti will become the center of command and control and rapid intervention. Yemeni officers said that there are American movements in order to bring the Red Sea and the Bab al-Mandab strait into the campaign.

- Iran’s Ministry of Foreign Affairs denied US President Trump’s assertions that Washington and Tehran were engaged in talks, according to WSJ.

- One of Iran's desalination plants on Qeshm Island is out of service since the strike and short-term repairs are deemed impossible, Borna reported citing a Health Ministry official.

- US reportedly attacks large ammunition depot in Isfahan, Iran, according to WSJ.

- Drone crashes in an open area at Iraq's West Qurna 1 oilfield without exploding, state news reported.

- Chinese Foreign Ministry said three Chinese ships recently sailed through the Strait of Hormuz.

- Saudi Arabia intercepts 10 drones, Al Jazeera reported.

- Power outage hits east of Tehran following explosions.

- Explosions heard in Iraq's Sulaymaniyah province and from US HQ in Baghdad's Victoria base, according to Tasnim.

- Italy denies the US use of its Sigonella naval air station, according to Italian press.

- Russia’s Foreign Minister Lavrov says the Middle East crisis may spill over into a wider conflict.

CRYPTO

- Bitcoin finds resistance just above USD 68k, Ethereum holds above USD 2k.

APAC TRADE

- APAC stocks were mixed with some indecision seen amid fluctuations in oil and mixed geopolitical headlines, including US President Trump's threats to obliterate Iran's energy infrastructure if a deal is not made soon, although he was also reported to have told aides he is willing to end the military operation in Iran without reopening Hormuz.

- ASX 200 rallied with gains led by strength in tech, telecoms and financials, while there was little impact from the RBA minutes, which stated that board members agreed financial conditions needed to be restrictive and that a further tightening would likely be needed, but disagreed on whether to hike at the meeting. Furthermore, members agreed that it is not possible to predict the future path of the cash rate with any confidence, given the Middle East conflict.

- Nikkei 225 retreated at the open but is off lows amid mixed data and fluctuations in oil.

- Hang Seng and Shanghai Comp failed to sustain early gains and dipped into negative territory despite better-than-expected Chinese official PMI data, and with participants reflecting on a deluge of earnings releases.

NOTABLE APAC DATA RECAP

- Chinese NBS Non-Manufacturing PMI (Mar) 50.1 vs. Exp. 49.9 (Prev. 49.5).

- Chinese NBS General PMI (Mar) 50.5 vs. Exp. 50.2 (Prev. 49.5).

- Chinese NBS Manufacturing PMI (Mar) 50.4 vs. Exp. 50 (Prev. 49.0, Low. 48.8, High. 50.5).

- Japanese Tokyo CPI YoY (Mar) Y/Y 1.4% vs. Exp. 1.7% (Prev. 1.6%).

- Japanese Tokyo Core CPI YoY (Mar) Y/Y 1.7% vs. Exp. 1.8% (Prev. 1.8%, Low. 1.6%, High. 2.1%).

- Japanese Tokyo CPI Ex Fresh Food and Energy YoY (Mar) Y/Y 2.3% vs. Exp. 2.4% (Prev. 2.5%).

- Japanese Retail Sales YoY (Feb) Y/Y -0.2% vs. Exp. 0.8% (Prev. 1.8%, Low. -1.1%, High. 1.3%).

- Japanese Retail Sales MoM (Feb) M/M -2.0% vs. Exp. -0.9% (Prev. 4.1%).

- Japanese Industrial Production MoM Prel (Feb) M/M -2.1% vs. Exp. -2.0% (Prev. 4.3%).

- Japanese Industrial Production YoY Prel (Feb) Y/Y 0.3%.

- Japanese Unemployment Rate (Feb) 2.6% vs. Exp. 2.7% (Prev. 2.7%, Low. 2.6%, High. 2.7%).

- South Korean Industrial Production YoY (Feb) Y/Y -2.2% (Prev. 7.1%).

- South Korean Industrial Production MoM (Feb) M/M 5.4% (Prev. -1.9%).

Loading...