Oil surges as Gulf producers cut output; Yields climb sparking hawkish re-pricing - Newsquawk US Market Open

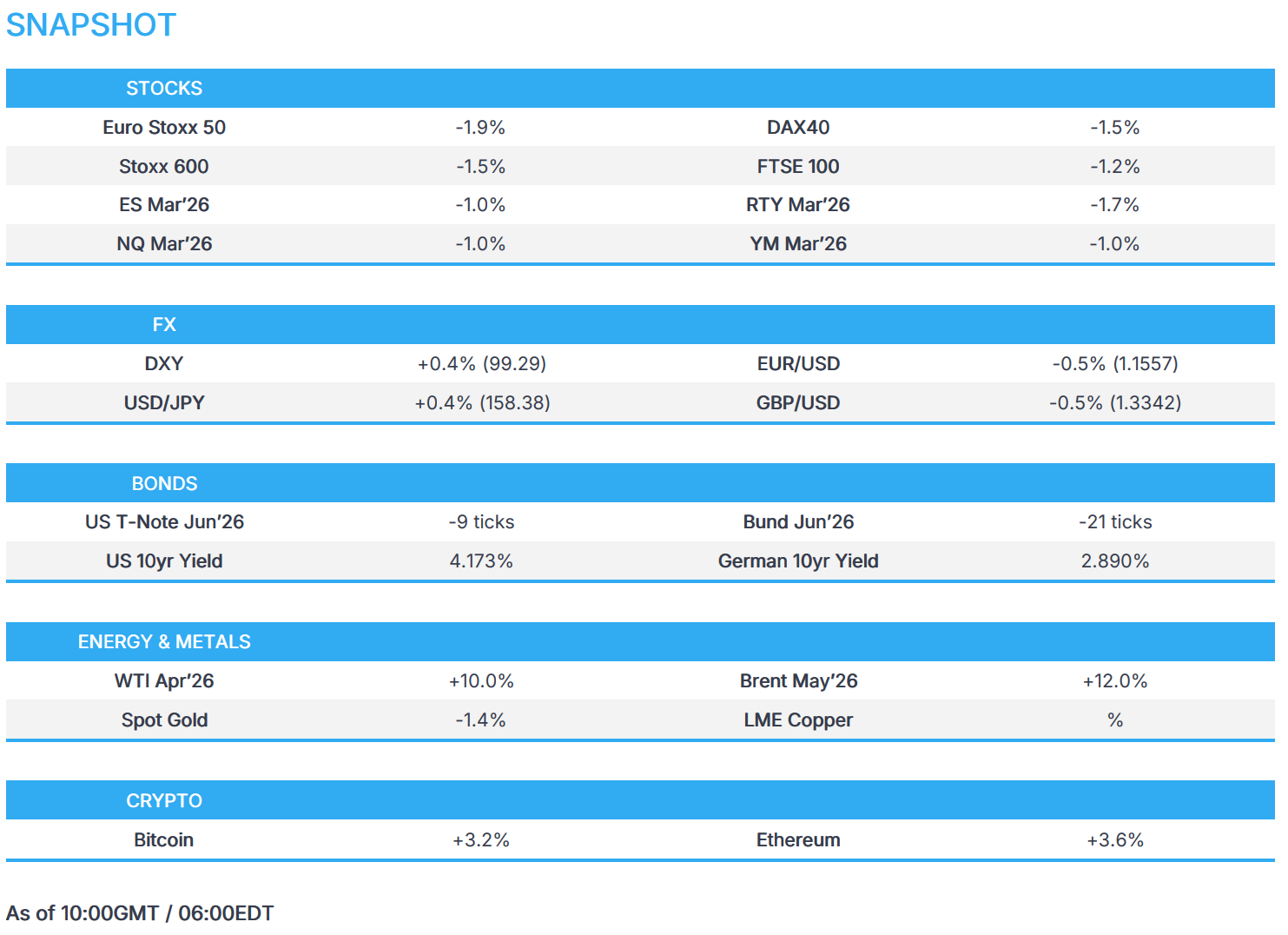

- Energy surges (Brent +12%) as key oil producers cut output.

- European bourses entirely in the red as higher energy prices weigh on broader sentiment; US equity futures follow suit.

- DXY bid on haven flows, EUR eyes the G7 ministers meeting on energy for reprieve.

- Global bond yields climb as energy benchmarks soar, sparking a hawkish move in central bank pricing.

- Precious metals weighed on by dollar strength.

- Looking ahead, highlights include US NY Fed SCE, Australian Westpac Consumer Confidence (Mar), & Japanese GDP Final (Q4), G7 meeting on emergency oil reserves. Speakers include ECB's Elderson & Cipollone.

- US clocks moved forward an hour over the weekend to Daylight Saving Time, with the London-NY time difference at 4 hours.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -1.5%) are entirely in the red, coming under significant pressure amid the surge in crude prices, which in turn holds back global growth. The FTSE 100 (-1.2%) is performing the best out of a bad bunch, as oil majors (Shell +1.6%, BP +1.0%) limit losses in the index. The SMI (-1.9%) is the laggard, weighed on by losses in Roche (-4.6%) after Genetech's persevERA breast cancer study did not meet the primary objective of a statistically significant improvement in progression-free survival.

- European sectors are completely in the red, with Real Estate (-3.2%) the worst performer as higher yields affect mortgage rates. Basic Resources (-3.1%) the worst performer after JPMorgan cut a number of European mining equities, warning that escalation in the Middle East could weigh on metal prices. Energy (U/C), unsurprisingly, sits at the top of the pile as Brent topped out just shy of USD 120/bbl.

- US equity futures (ES/NQ -1.0%, RTY -1.7%) have followed their European counterparts, with the RTY being hit the hardest as higher energy costs and potential Fed hikes affect smaller businesses.

- Novo Nordisk (NOVOB DC) and Hims & Hers (HIMS) is expected to announce a new partnership on Monday for Novo to sell its weight-loss drug on the Hims platform, Bloomberg reported citing sources.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is stronger this morning and trades at the upper end of a 98.83 to 99.69 range, with the index buoyed by the ongoing Iran war. In brief, there are currently no signs of a near-term resolution of the war, with oil prices surging some 30% at one point. (See the Newsquawk analysis piece at 08:25 GMT for details)

- Further upside for the index could bring into play a cluster of highs from late November 2025, and the key 100.00 mark on the 25th of November 2025; the high that day was 100.26. But, upside may be limited in the near-term as markets count down to the G7 ministers meeting at 08:30 GMT / 12:30 EDT. A source cited by the FT suggested a joint release in the range of 300-400mln barrels, 25-30% of the IEA's reserves, would be appropriate. For reference, the Ukraine-Russia war led to the IEA releasing some 182mln barrels in March and April 2022. Therefore, a release of 300-400mln barrels could spur some short-term pressure in the USD.

- EUR and GBP both continue to extend losses, as the net-importers of oil face significantly higher energy prices, stoking inflationary fears. As such, money markets now fully price in two ECB hikes in 2026 (vs none pre-war); markets now assign a 50% chance of a hike at the BoE (vs three cuts in 2026 pre-war). Elsewhere on a domestic footing, focus has been on the Baden-Württemberg election in Germany. The Greens won the election, whilst the CDU (29.7%) extended on its standing from the last election; importantly, the SPD fell to 5.6% (prev. 11%), which may stoke fears for Chancellor Merz, and the standing coalition.

- Havens (CHF & JPY) also extend losses, given both are net-importers of energy. For the CHF specifically, Switzerland has voted to introduce individual taxation; the government believes that the reform could bring back around 60k people to the labour force, and boost GDP by around 1%. As for Japan, USD/JPY continues to advance into “intervention territory”, which has been seen around 158-160. However, it can be argued that any attempt to intervene may prove to be inconsequential, as recent strength in oil prices show little sign of abating.

- Antipodeans were initially pressured by the USD strength, but have recently edged slightly higher; the Kiwi is the top G10 performer. Upside which could be facilitated by the firmer-than-expected Chinese inflation data overnight.

FIXED INCOME

- A bearish start to the week for benchmarks as yields react to energy prices. See the 08:25GMT update for a full geopolitical brief, but in brief, the ongoing Middle East conflict, supply/production disruptions, and no clear signs that the US or Iran are set to back down have lifted crude to above USD 100/bbl, a level not seen since 2022.

- This saw USTs begin the week with losses of nearly 20 ticks, Bunds down by over 90 ticks and Gilts gapping lower by 119 ticks at a 88.80 trough, just above the 88.52 contract base.

- For the UK, the move lifted the 10yr yield to a 4.78% peak, the highest since October 2025 and takes us back to the September 2025 peak of 4.86%. Action that has seen a marked shift in BoE repricing, with markets implying around a 70% chance of a hike by the end of 2025; a marked shift from mid-February, when two cuts were essentially priced. Note, this move will likely moderate as while easing is likely off the cards in the near-term, the UK's job market situation does not support tightening in the near term.

- Back to USTs, the benchmark is lower by around 15 ticks as it stands, just off a 111-26+ base. The day ahead is focused entirely on energy, with a G7-IEA meeting expected at 12:30GMT to discuss a potential strategic release.

- For Bunds, they are also off worst and by quite some way. Down by around 25 ticks currently, but around 70 off a 125.94 trough. A moderation that has perhaps come as the benchmark finds some modest haven allure given the broader risk tone. Additionally, a rethinking of ECB pricing from the knee-jerk this morning may be factoring; at most, markets priced in two 25bps hikes by the ECB in 2026.

- Bank of Korea is reportedly to purchase up to KRW 3tln of government bonds.

COMMODITIES

- Oil opened in panic mode, with WTI and Brent initially surging above USD 100/bbl and rising 30% to briefly approach USD 120/bbl as the Iran conflict entered a second week and Gulf supply disruptions intensified (full Newsquawk analysis on the feed). Crude prices later pulled back after reports that the G7 will discuss a coordinated emergency reserve release, with some US officials said to favour a 300–400mln barrel draw (~25–30% of IEA system reserves), with the call set to take place at 12:30 GMT (08:30 EDT) amid the US clock change.

- European gas prices surged sharply by some 30% at the open amid Hormuz risk and Gulf infrastructure disruption. Severe tanker interference, soaring war-risk premiums and regional refinery attacks exacerbated volatility. While alternative routes (e.g., Red Sea) may cushion some flows, they cannot fully offset Hormuz volumes. Gas remains sensitive to any reopening signals or reserve coordination outcomes.

- Spot gold softened alongside a firmer USD and broader risk-off liquidation from energy-induced inflationary fears. Central bank demand remains supportive, with the PBoC reportedly extending gold purchases for a 16th consecutive month. Spot gold currently resides in a USD 5,015.04-5,171.95/oz range at the time of writing (vs Friday's 5,063.21-5,176.63/oz parameter).

- Copper slumped at the reopen as oil’s surge and geopolitical risk dampened cyclical appetite. Prices recovered modestly off worst levels following firmer-than-expected Chinese inflation data, but the tone remains fragile. Persistent energy disruption and USD strength pose downside risks, while any easing in Gulf tensions could stabilise sentiment. 3M LME copper resides in a USD 12,594.00-12,845.00/t range at the time of writing.

- Japan METI orders oil reserve station to prepare for a release, according to Nikkei.

- Japanese Chief Cabinet Secretary Kihara sees crude prices rising further amid the Middle East situation and said no decision on all reserve release.

- Bahrain's Bapco declares a force majeure.

- G7 is to discuss a joint release of emergency oil reserves in an emergency meeting on Monday, according to FT; call at 08:30 EDT (12:30 GMT).

- Some officials are discussing a potential 300-400mln barrel release, up to 30% of the IEA’s 1.2bln barrel emergency stockpile, according to Kpler's Bakr.

- China raises its gas and diesel prices by CNY 695 and 670/ton respectively from March 10th.

- Qatar to reportedly push LNG expansion to 2027 following drone attacks.

- EU Commission Spokesperson said European oil and gas supply groups are to meet on Thursday 12th to discuss the Middle East situation.

- US President Trump posted "Short term oil prices, which will drop rapidly when the destruction of the Iran nuclear threat is over, is a very small price to pay for U.S.A., and World, Safety and Peace. ONLY FOOLS WOULD THINK DIFFERENTLY!".

- Mizuho's Rochester writes "oil is now on a USD 100/bbl handle and it might be there to stay" with increasing likelihood of USD 130-150/bbl as the Middle East conflict/supply situation persists.

- Kpler's Bakr posted "Europe has few options to replace lost jet fuel flows from the Middle East following disruption in Hormuz. With Asian markets pulling cargoes eastward and export restrictions tightening supply...". Cont'd.. "attention is shifting to the Atlantic Basin – particularly the US Gulf Coast and West Africa – though available volumes are unlikely to fully offset the shortfall.".

TRADE/TARIFFS

- US Customs and Border Protection told a court it cannot immediately refund about USD 166bln in tariffs deemed illegal by the Supreme Court, as its computer systems, administrative procedures and staffing do not enable it to comply at once.

- US President Trump and Chinese President Xi's summit is said to unlikely yield a breakthrough, with five people briefed on preparations saying the summit is unlikely to create room for even a limited reset of business and investment ties.

- Chinese Foreign Minister Wang Yi said China and the US could make 2026 a landmark year for sound, steady and sustainable development of China-US relations, while he added that China’s attitude is always positive and open. Furthermore, he stated regarding US President Trump’s planned visit to Beijing, that the agenda of high-level exchanges is already on the table and that both sides now need to make preparations accordingly.

- Japanese Trade Minister Akazawa said Japan requested that the US exempt it from the planned tariff increase from 10% to 15%, following a meeting with US Commerce Secretary Lutnick. It was also reported that Japan is said to be considering JPY 15tln for a second US investment project and that the government approached Japan Display (6740 JT) about operating a USD 13bln cutting-edge factory in the US as part of the USD 550bln investment package.

- South Korea’s Industry Minister Kim said the US is unlikely to impose the previously threatened 25% tariffs on South Korea if the Korean parliament move swiftly to ratify the investment legislation in the week ahead.

NOTABLE EUROPEAN DATA RECAP

- German Industrial Production MoM (Jan) M/M -0.5% vs. Exp. 0.9% (Prev. -1.9%).

- Swiss Sight Deposits (w/e Mar 6). Domestic Banks CHF 428.861bln (prev. 440.5bln), Total CHF 454.072bln (prev. 459.8bln).

- Swiss Consumer Confidence (Feb) -30 vs. Exp. -29 (Prev. -30).

- Norwegian PPI YoY (Feb) Y/Y -9.4% (Prev. -7.8%).

NOTABLE US HEADLINES

- US FDA is planning to ease some requirements for drugmakers to develop copycat versions of expensive biologic medications, Bloomberg reported citing an FDA official.

GEOPOLITICS

IRAN CONFLICT

- US President Trump said that Iran would be hit very hard on Saturday and the US would consider targeting areas and groups in Iran that were not previously considered as targets.

- US President Trump said there would have to be a very good reason for the US to deploy ground troops in Iran, while Trump also said that he has ruled out having Kurdish forces go into Iran.

- US President Trump is said to be considering the option of deploying special forces on the ground in Iran to seize its near-bomb-grade uranium, according to Bloomberg, citing three diplomatic sources briefed on the matter.

- US envoys Kushner and Witkoff cancelled their planned arrival in Israel tomorrow, local Israeli reported suggest.

- US may be responsible for the bombing of a girls' school in Iran that killed 168 people on February 28, according to sources cited by CBS News.

- US President Trump tells Times of Israel in a brief interview that it will be a mutual decision with Israeli PM Netanyahu regarding when the Iran war ends.

- US Secretary of War Hegseth reiterates that US strikes on Iran are only just the beginning during a CBS 60 Minutes interview.

- Iranian President Pezeshkian said on Saturday that he instructed the military not to attack any country that is not striking Iran and apologised to Iran’s neighbours for conducting strikes against them, although reports noted that there were no signs that Iranian forces had stopped striking their Arab Gulf neighbours.

- Iran’s Foreign Minister Araghchi said he is in constant contact with his Saudi counterpart and that Saudi officials said they were fully committed to not letting their territory, water and airspace be used against Iran.

- Iran’s Supreme National Security Council Secretary Larijani said the US must pay for its actions and that Iran would not leave US President Trump alone for killing Supreme Leader Khamenei, while he also stated that Tehran has no problem with regional countries but warned Tehran would continue attacking neighbouring countries if they allow their territories to be used for attacks against Iran.

- Iran picked former Supreme Leader Ali Khamenei’s son Mojtaba as the next Supreme Leader, while Iran's Revolutionary Guards said they are ready to follow and obey new Supreme Leader Mojtaba Khamenei.

- Iranian Foreign Ministry spokesperson said there is no doubt the US is after Iranian oil resources and aims to weaken and break up the country, SNN reported. When asked about a possible ceasefire, said as long as attacks continue, there is no point in talking about anything but defence and retaliation against enemies.

- Launches from Iran towards Northern Israel and Lachish area were identified, according to Kan News.

- Iran's Revolutionary Guards say they are ready to follow and obey new Supreme Leader Mojtaba Khamenei.

- Iranian missile attack causes power outage in Tel Aviv, according to ISNA.

- Iranian strike hit a Bahraini desalination plant, according to Semafor.

- Israeli Channel 12 estimates that the battle with Iran may continue for at least five additional weeks, Sky News Arabia reported.

- Israel conducts raid on Kfar Kila in southern Lebanon.

CRYPTO

- Bitcoin returns above USD 68k while Ethereum breaches USD 2k.

APAC TRADE

- APAC stocks sold off heavily with global markets rattled after the Iran war entered a second week with no signs of abating and as oil prices surged around 30% intraday on continued disruption, with more producers forced to cut output.

- ASX 200 slumped at the open with heavy losses across all sectors aside from energy due to the oil price surge.

- Nikkei 225 suffered intraday losses of more than 4,000 points as manufacturers and exporters suffered from the rising energy costs and shipping disruption.

- Hang Seng and Shanghai Comp conformed to the broad risk-off mood with sources tempering expectations for a breakthrough in the upcoming Trump/Xi summit, but with the downside in the mainland somewhat cushioned after firmer-than-expected Chinese inflation data.

NOTABLE ASIA-PAC HEADLINES

- China NPC Standing Committee said it is to revise law on enterprise state-owned assets, will strengthen research on legislation in AI and other sectors, will also revise PBoC law and banking regulation law.

- Japanese Finance Minister Kato said a weak yen is one factor behind rising prices.

- Japanese Trade Minister Akazawa said will make all efforts to ensure all price rises do not affect Japanese people's lives negatively.

NOTABLE APAC DATA RECAP

- Chinese Inflation Rate YoY (Feb) Y/Y 1.3% vs. Exp. 0.8% (Prev. 0.2%).

- Chinese Inflation Rate MoM (Feb) M/M 1.0% (Prev. 0.2%).

- Chinese PPI YoY (Feb) Y/Y -0.9% vs. Exp. -1.1% (Prev. -1.4%).

- Japanese Eco Watchers Survey Current (Feb) 48.9 vs. Exp. 48.2 (Prev. 47.6).

- Japanese Eco Watchers Survey Outlook (Feb) 50.0 (Prev. 50.1).

- Japanese Labour Cash Earnings (Jan) 3.0% vs Exp. 2.5% (Prev. 2.4%).

- Japanese Real Cash Earnings YY (Jan) 1.4% vs Exp. 0.9%.

- Japanese Overtime Pay YoY (Jan) Y/Y 3.3% (Prev. 0.9%, Rev. From 1.5%).

Loading...