"Perfect Storm": Bond Traders "Stunned" At How Quickly SpaceX Bonds Are Selling Off

Media reports earlier this week about SpaceX's inaugural post-IPO investment-grade bond (and we mean inaugural, as the company rushed to tap the corporate bond market just days after going public with a low-IG rating of Baa1/BBB) which priced on Tuesday, had it as almost 4x oversubscribed, at roughly $90BN in orders for the $25 billion offering (upsized from $20 billion), signaling relentless demand for the paper. Alas, it took just 48 hours for the myth of sterling demand to crash and burn, with Bloomberg reporting today that the "blockbuster bond sale is weakening so quickly in the secondary market that traders say they can’t recall another recent deal that widened this sharply."

This is what we mean.

Confirming the TRACE data shown above for the company's bonds due 2056, Bloomberg says that a large dealer was quoting the SpaceX bonds at levels as much as 0.32 percentage point wider than the issue price of 1.75 percentage points above Treasuries.

Parallel selling across the entire SpaceX bond complex means that paper losses on the company's $25 billion offering have mounted since the debt broke for trading Wednesday and totaled roughly $400 million as of Friday, relative to Treasuries. The longest-dated SpaceX bonds, which drew more skepticism than those with shorter maturities, have erased all the tightening from underwriters that followed as orders swelled to nearly $90 billion.

So much for that oversubscription.

Traders who spoke to Bloomberg said the moves suggest fast-money accounts, rather than traditional buy-and-hold investors, piled into the deal looking to flip it for a quick profit. In other words, the momentum monkeys who have dominated stonks, decided to try their hand at flipping bonds. It didn't work out well: the selling pressure stands out even more because SpaceX shares have been largely stable since the bonds priced on Tuesday, after lurching 16% lower the day before, which it not say that the stock has been especially stable and it once again broke below its first day of trading price earlier today when it briefly dipped below $150.

Even if there are more technical reasons behind the selling - hedge funds covering or hedging short positions, for example - the unprecedented magnitude of the rapid selling points to SpaceX’s unique profile. The company, which at its peak this month had a $2.64 trillion market value, won investment grades despite expectations for years of negative cash flow and a dependence on Elon Musk that Fitch Ratings deemed a “key rating constraint.”

“We expected SpaceX to widen from issuance level, but not this much,” said Tony Trzcinka, a portfolio manager at Impax Asset Management. “That magnitude is likely a perfect storm of the stock shedding $600 billion+ since launch, weak technicals from the upsized supply, and investors still scratching their heads over how to price its unique risk profile.”

SpaceX's selling is a rare move compared with how other recent mega bond sales have traded in the secondary market.

Take Nvidia, which raised $25 billion in a seven-part high-grade offering this month. The spreads on its 5.55% bonds maturing in 2046 have widened by just 11 basis points since issuance, while the spreads on its 5.625% bonds maturing in 2056 are 12 basis points wider. The spread on Alphabet’s longer-dated bonds issued in February have broadly tightened.

Meanwhile, after weakening, SpaceX’s credit curve is now trading more in line with those of similarly rated Oracle, whose longer-dated bonds also widened soon after they were first sold.

One way to track the SpaceX relative credit performance is through CDS, as Credit-default swaps tied to the company began actively trading after the company sold high-grade bonds this week for the first time, allowing investors to hedge against potential losses or to speculate on the creditworthiness of the firm. And yes, SPCX CDS has blown wider since breaking for trading, indicating the market is not as hopeful on the company's "otherworldly" ambitions, as Elon Musk or the friendly Wall Street sellside, which expects 100x higher revenues by 2030.

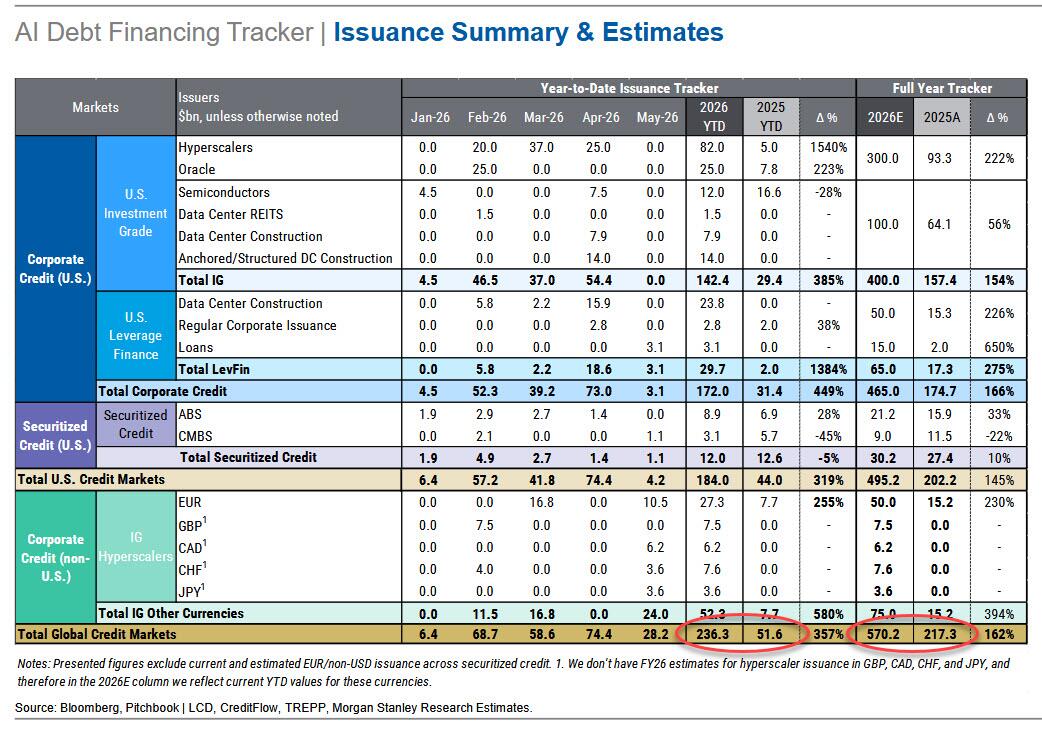

But here a bigger problem emerges: as we have been pounding the table since last October, when we said that "AI Is Now A Debt Bubble Too, Quietly Surpassing All Banks To Become The Largest Sector In The Market" and most recently two weeks ago when we profiled "The $1.8 Trillion Off-Balance Sheet Time Bomb At The Heart Of The AI Supercycle", bondholders have been inundated with massive hyperscaler bond sales this year as tech giants race to raise billions of dollars to finance artificial intelligence projects (read: pay memory chip makers ridiculous prices for their commodity product). US high-grade supply of $180 billion as of Wednesday has set a new June record, surpassing 2020’s $169 billion haul, according to Bloomberg calculations. Morgan Stanley's internal calcs are even more insane: the bank's latest Debt Financing Tracker (available to pro subscribers) found that YTD $236BN in AI-linked debt has been issued, a 357% increase from the same period last year. By year-end, MS expect this number to more than double to $570 billion.

Even more amazing is the recent explosion in hyperscaler gross leverage, which has surged from 0.9x in Q3 '25 to 1.8x currently, doubling in just over two quarters, and surpassing the gross leverage of the entire energy sector. At this rate, hyperscaler debt is growing at about 0.3x turn per quarter.

Echoing Bloomberg's observation that the borrowing spree is starting to weigh on corporate bond spreads, pushing average high-grade risk premiums out of a historically tight range, Morgan Stanley noted that hyperscalers are drifting wider, and after trading insider AA spreads for much of 2025, are now on top of A, and as MS warns, "may widen further on supply." And it's not just outlier Oracle: META is now trading wider to CDX IG.

Not surprisingly, Bloomberg reported earlier this week that demand for the SpaceX bond sale was strongest for the five-year notes, i.e. the lowest duration part of the offering, which let the company cut borrowing costs more on that portion of the deal than on the longer maturities. Interest was weaker in the 20-year and 30-year bonds, which saw the biggest drop-off in demand. Ironically that's precisely where the bulk of the "shareholder value" is concentrated, deep in the future when SpaceX is expected to be colonizing Mars, flying through worm holes, and enjoying other activities that push its EBITDA north of $1 trillion, or something.

SpaceX’s long-dated bonds are widening despite “some initial excitement and demand,” with bondholders “seemingly concluding that there may be plenty more debt issuance to come, as the loss-making company finances its future path to profitability,” Mark Dowding, CIO for fixed income at RBC BlueBay Asset Management, wrote in a note.

Mark is undoubtedly correct, and we expect both SpaceX and other IG names to continue flooding the market until spreads eventually blow up like they did one year ago, and shut the debt issuance window for good, at which point the capex cycle will end as there is no more free cash flow, and in a few months, there will be no more debt either.

We recommend reading the latest Morgan Stanley Debt Financing Tracker for a comprehensive analysis of the hyperscaler debt flooding the investment grade bond market (available to pro subscribers).