Quiet trade into US CPI, Crude/DXY flat, equities lower - Newsquawk US Market Open

- US launched fresh strikes on Iran in response to Monday’s downing of an Apache helicopter; the mission was a “proportional response” to Iranian aggression, while President Trump called it “very strong and powerful”.

- Iran responded with attacks on US bases in Bahrain, Kuwait and Jordan; Brent Aug’26 U/C.

- A White House senior official said nothing has changed in their position regarding an agreement with Iran, and it is still close despite the strikes.

- Iranian Foreign Ministry spokesperson Baghaei says they need to reassess, following the overnight clashes, when questioned on talks with the US, SNN reports.

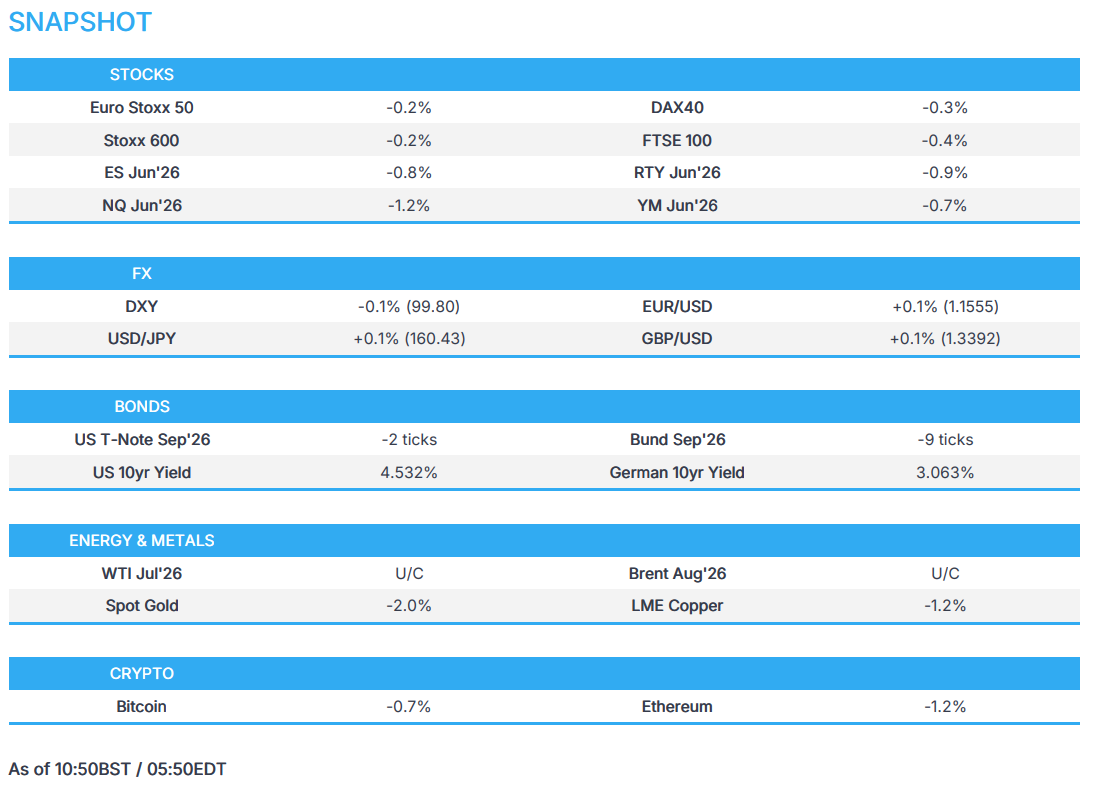

- US equity futures extend lower and currently reside at lows; NQ -1.2% underperforms.

- DXY is incrementally lower into US CPI; USD/JPY choppy on reports that BoJ Governor Ueda is in hospital and will not attend the June meeting.

- Global fixed benchmarks are slightly lower in quiet trade, US paper awaits data and a 10yr auction.

- Looking ahead, highlights include US CPI (May), BoC Policy Announcement (Jun), Speakers including BoC’s Macklem, Supply from the US, Earnings from Oracle.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- The US and Iran exchanged fire following the downing of a US Apache helicopter over the Strait of Hormuz. Iran's IRGC struck a US base in Jordan and 21 other targets in the Gulf, after the US hit Iranian air defence, ground control stations and surveillance radar sites near Hormuz. Sounds of explosions were reported in Qeshm Island and the port city of Sirik, while explosions were heard near Bandar Abbas and Jask. Following the initial exchange of missiles, US CENTCOM announced in the early hours of Wednesday that they have ended its self-defence strikes against Iran.

- US President Trump told ABC that the US was responding to Iran and that it is important to respond to Iran downing the helicopter, as well as noted that the response is very strong and powerful.

- US VP JD Vance said the US is very close to reaching a deal that would address Iran's nuclear programme for the long term, which could come next week or months from now, but absolutely before the midterms, according to CBS.

- White House senior official said nothing has changed in their position regarding an agreement with Iran and it is still close despite the strikes.

- A US official said the US military carried out strikes on almost 20 targets inside of Iran, but noted preliminary assessments indicate most Iranian missiles and drones were successfully intercepted.

- Iranian Foreign Ministry spokesperson Baghaei said they need to reassess, following the overnight clashes, when questioned on talks with the US, SNN reported.

- Iranian Foreign Ministry statement strongly condemns America's crime in its military aggression against Iran.

- An Iranian military source tells IRIB that no offensive military operations have been conducted in the Strait of Hormuz over the past 24 hours. Warned that if the enemy carries out another hostile action under the pretext of the military helicopter crash, it will face a decisive response.

- A massive fire in the centre of Erbil and an explosion has been heard near the US base in the vicinity, Mehr news reported citing sources.

- Local sources reported that an explosion was heard in the area of Qeshm city, Mehr News reports. However, this was later denied by the Qeshm governor.

- UN Security Council debated reviving the Iran sanctions panel, although Russia and China opposed the revival of the Iran sanctions committee, according to Tasnim.

- Israeli air raids hit the Lebanese towns of Touline, Srifa and Kafra. It was separately reported that missiles were spotted from Lebanon that were headed towards Kiryat Shmona and its surroundings, while rockets launched from Lebanon towards Upper Galilee were also detected.

- UKMTO has received a report of an incident 20nm Northeast of Oman’s Sohar.

- UKMTO reported an incident involving a cargo vessel 88 nautical miles southwest of Balhaf, Yemen.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.2%) initially opened with mild gains, before dipping into the red as the morning progressed – currently at lows. In Tuesday's session, US President Trump vowed retaliation after the downing of a US Apache helicopter, resulting in US forces targeting Iranian air defences, ground control stations and surveillance radar sites around the Strait of Hormuz. In response, Iran's IRGC said they carried out attacks against a US base in Jordan and 21 other targets around the Gulf.

- European sectors are mixed. Topping the sector pile is Real Estate (+0.6%), with Optimised Personal Care (+0.4%) and Food, Beverages & Tobacco (+0.5%) rounding out the top three. Underperformance in Financial Services (-0.8%), Basic Resources (-1.2%) and Technology (-0.9%).

- US equity futures lags their European peers, with the NQ (-1.2%) underperforming. Today’s focus will be on the US inflation report, with headline CPI expected to print at 4.2% (prev. 3.8%). A hotter print would bring further hawkish pricing for the Fed to hike rates in 2026. Currently, markets are pricing 25bps of tightening in 2026.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s mostly range trading as the Buck positions into US CPI; CAD outperforms into BoC, antipodeans lag after soft Chinese inflation data, NOK outperforms post-CPI.

- DXY -0.1%, lower on the day but still holding onto most NFP gains despite a sharp reversal in crude over the past few days. Levels reached around NFP, just above the 100 mark, will be watched closely as an inline/hot CPI print will help the index return to these levels. MUFG suggests that a hot print CPI (>4.3%) would likely trigger a sharp sell-off in US front-end rates, potentially pulling forward expectations for a hike towards October. ING contends a soft print would see DXY test the 99.50/60 area.

- CAD is one of the best performers ahead of the BoC confab, USD/CAD -0.1%. BoC is widely expected to leave its policy rate unchanged at 2.25% for a fifth consecutive meeting as it balances trade uncertainty against lingering inflation risks. Attention will centre on whether policymakers are more attentive to inflation or growth risks. Markets will also be watching for acknowledgement of Canada's technical recession, alongside any emphasis on the apparent Q2 recovery, stable core inflation and the Bank's position near the lower end of neutral as justification for maintaining a wait-and-see approach. USD/CAD could look to test 1.40 if US CPI comes hot, and BoC does not provide food for hawks.

- NOK is the best G10 performer after hot CPI-ATE this morning surpassed consensus and was mildly above the Norges Bank's own forecast of 3.3%. Sell-side banks saw some risk that a hot inflation report could see board members begin to mull another hike at the June meeting. However, it is more likely that policymakers wait for more data and assess the developments in the Middle East. Nonetheless, CPI-ATE remains persistently high, which clouds the environment. NOK/SEK +0.4%, looks to test par after surpassing the level overnight.

- Antipodeans underperform after Chinese inflation printed cooler than expected. CPI was steady at 1.2% Y/Y, cooler than economists had expected. PPI rose to 3.9%, lower than most estimates. As such, both Aussie and Kiwi weaker against the Buck by 0.2% and 0.1% respectively.

FIXED INCOME

- Global fixed benchmarks are trading tentatively on either side of the unchanged mark, following similar indecisive action in the energy space. This follows on from overnight US strikes on Iran, in response to the downing of a US helicopter earlier in the week. This latest attack led Iran to launch retaliatory strikes against Bahrain, Kuwait and Jordan. As for the progress to peace, a WH official stated that “nothing has changed in their position regarding an agreement with Iran, and it is still close despite the strikes”. However, the Iranian Foreign Minister stated that they need to reassess, following the recent strikes; he added that the US harms diplomatic efforts.

- USTs (-2 ticks) trade with very mild losses and hold towards the bottom of a 109-03 to 109-08 range. The tentative action today is explained by the uncertain geopolitical environment, and as markets await US CPI/10yr auction later today.

- Bunds (-9 ticks) and Gilts (-6 ticks) trade incrementally lower, following the tentative action seen above. Domestic updates today have been lacking, but focus for the EGBs will be on a 10yr Bund auction. As it stands, the GE 10yr yield holds slightly above the 3% mark, driven higher by elevated energy prices and sticky inflation. The sale should go well, with some traders potentially booking profits at elevated levels. The geopolitical environment appears to be easing (but remains incredibly uncertain), and with some fund managers believing fixed income will reclaim its safe-haven status, yields should begin to ease from recent peaks.

- Germany to sell EUR 3.982bln vs exp. 5bln 2036 2.90% Bund: b/c 1.71x (prev. 1.5x), average yield 3.06% (prev. 3.16%), retention 20.4% (prev. 23.1%).

- Japan sells JPY 450.8bln 30-yr JGBs; b/c 2.94x (prev. 3.49x), and average yield 3.860% (prev. 3.842%), Lowest accepted price 97.40 vs prev. 97.80, Average accepted price 97.78 vs prev. 98.02, Tail in price 0.38 vs prev. 0.22.

- Australia sells AUD 1bln 1.00% October 2037 bonds b/c 4.25, avg yield 4.9566%.

COMMODITIES

- In geopolitics, The US and Iran exchanged fire following the downing of a US Apache helicopter over the Strait of Hormuz. Iran's IRGC struck a US base in Jordan and 21 other targets in the Gulf, after the US hit Iranian air defence, ground control stations and surveillance radar sites near Hormuz. Sounds of explosions were reported in Qeshm Island and the port city of Sirik, while explosions were heard near Bandar Abbas and Jask. Following the initial exchange of missiles, US CENTCOM announced in the early hours of Wednesday that they have ended its self-defence strikes against Iran.

- Crude futures trade around the unchanged mark despite the US-Iran strikes. WTI Jul'26 oscillates in a USD 87.39-90.00/bbl range while Brent Aug'26 rotates in a USD 90.77-93.26/bbl band. Saxo's chief investment strategist says, "Geopolitics is being treated as a headline risk, not a macro shock for now. Oil holding around USD 90 despite fresh Iran headlines suggests markets are not pricing a sustained supply disruption."

- Precious metals continue to trade under pressure. Spot gold slips below the USD 4200/oz handle, at the lower end of its USD 4161-4258/oz range. The yellow metal has been under pressure in recent sessions, which was initially spurred by the stronger-than-expected US jobs report last Friday. The US inflation print at 13:30BST/08:30EDT will be a highly-watched data point for metals traders, another hot print could spur further downside. The next level below market is the USD 4099/oz low from March 23rd.

- 3M LME Copper traded rangebound throughout the Asia-Pac session but is currently extending to lows, slipping below the USD 13.5k/t mark. Chinese inflation failed to move the red metal, after headline inflation held at 1.2% Y/Y but was cooler than the expected 1.3%.

- US Private Inventory Data (bbls): Crude -9.1mln (exp. -3.4mln), Distillates +1.3mln (exp. -0.2mln), Gasoline -1.2mln (exp. -0.6mln), Cushing -1.1mln.

- US Deputy Secretary of State Landau said the US is working to release energy reserves and boost sales of LPG and LNG to ASEAN.

- Kuwait is reportedly in discussions with Saudi Arabia and the UAE to secure pipeline capacity to export crude and oil products, Argus reported.

- Oman sets a price of USD 86.47/bbl for Omani crude oil with an August delivery.

- Kazakhstan Energy Ministry sees 2026 oil output at 98mln T (prev. 99.4mln T).

TRADE/TARIFFS

- India's Trade Minister said they are looking into various measures including duties to deal with the amount of dumped steel products.

CENTRAL BANKS

- BoJ Governor Ueda said to have been hospitalised, reports suggest, and is expected to be absent for the June 15-16 meeting. Deputy Gov. Himino will chair June meeting.

NOTABLE EUROPEAN HEADLINES

- Germany's DIW cuts its 2026 growth forecast for Germany to 0.5% (prev. 1.0%); Germany risks slipping into a technical recession this year following the energy shock.

- European Parliament's budgetary control committees are to examine the Commissions plan to unlock EUR 16bln of funding for Hungary on the 14th of July, Politico reported citing sources.

NOTABLE EUROPEAN DATA RECAP

- Norwegian Core Inflation Rate YoY (May) Y/Y 3.4% vs. Exp. 3.3% (Prev. 3.2%).

- Norwegian Core Inflation Rate MoM (May) M/M 0.4% vs. Exp. 0.3% (Prev. 0.7%).

- Norwegian Inflation Rate YoY (May) Y/Y 3.1% vs. Exp. 3.1% (Prev. 3.4%).

- Swedish GDP MoM (Apr) M/M 0.5% (Prev. 1.9%).

- Italian Industrial Production YoY (Apr) Y/Y 1.3% (Prev. 1.5%).

- Italian Industrial Production MoM (Apr) M/M 0.5% vs. Exp. 0.1% (Prev. 0.7%).

NOTABLE US HEADLINES

- US House passes USD 70bln immigration enforcement funding bill.

- US Agriculture Secretary Rollins said the first US calf with screwworm is healthy and recovering, while she said they will start eradicating screwworm in a couple of months.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukrainian President Zelensky confirmed that the targeted the Russian Novokuibyshevsk refinery.

- Ukraine hit two Russian pumping stations; namely, Vtorovo and Lobkovo.

OTHER

- US Pentagon said Defence Secretary Hegseth is to travel to the US Navy base at Guantanamo Bay on Wednesday to engage with troops, as the US continues to pressure Cuba.

CRYPTO

- Bitcoin returns to its selloff, slipping back below the USD 61k handle. Ethereum nears USD 1.6k.

APAC TRADE

- APAC stocks mostly declined following the tech weakness on Wall St and amid the escalation in the Middle East after the US conducted strikes on Iran in response to the downing of an Apache helicopter, while Iran retaliated with strikes targeting US bases in the region.

- ASX 200 bucked the trend amid gains in the consumer sectors, financials and defensives.

- Nikkei 225 retreated amid tech-related headwinds, while firmer-than-expected PPI data and the latest BoJ source report continued to point to a looming hike for next week's meeting.

- Hang Seng and Shanghai Comp conformed to the downbeat mood in the region owing to the recent geopolitical escalation. Elsewhere, Chinese inflation data was mixed as CPI Y/Y printed softer-than-expected, but PPI Y/Y topped forecasts and printed its highest since July 2022.

NOTABLE APAC DATA RECAP

- Chinese CPI YY (May) 1.2% vs. Exp. 1.3% (Prev. 1.2%).

- Chinese PPI YY (May) 3.9% vs. Exp. 3.8% (Prev. 2.8%).

- Japanese PPI MM (May) 0.9% vs. Exp. 0.5% (Prev. 2.3%).

- Japanese PPI YY (May) 6.3% vs. Exp. 5.5% (Prev. 4.9%).

Loading...