Reports point to a US-Iran agreement on the horizon ahead of Trump deadline - Newsquawk US Market Open

- Pakistani reporter Anas Mallick suggested that the interlocutors are closer than ever for an agreement to get a "framework of understanding for ceasefire" between US and Iran.

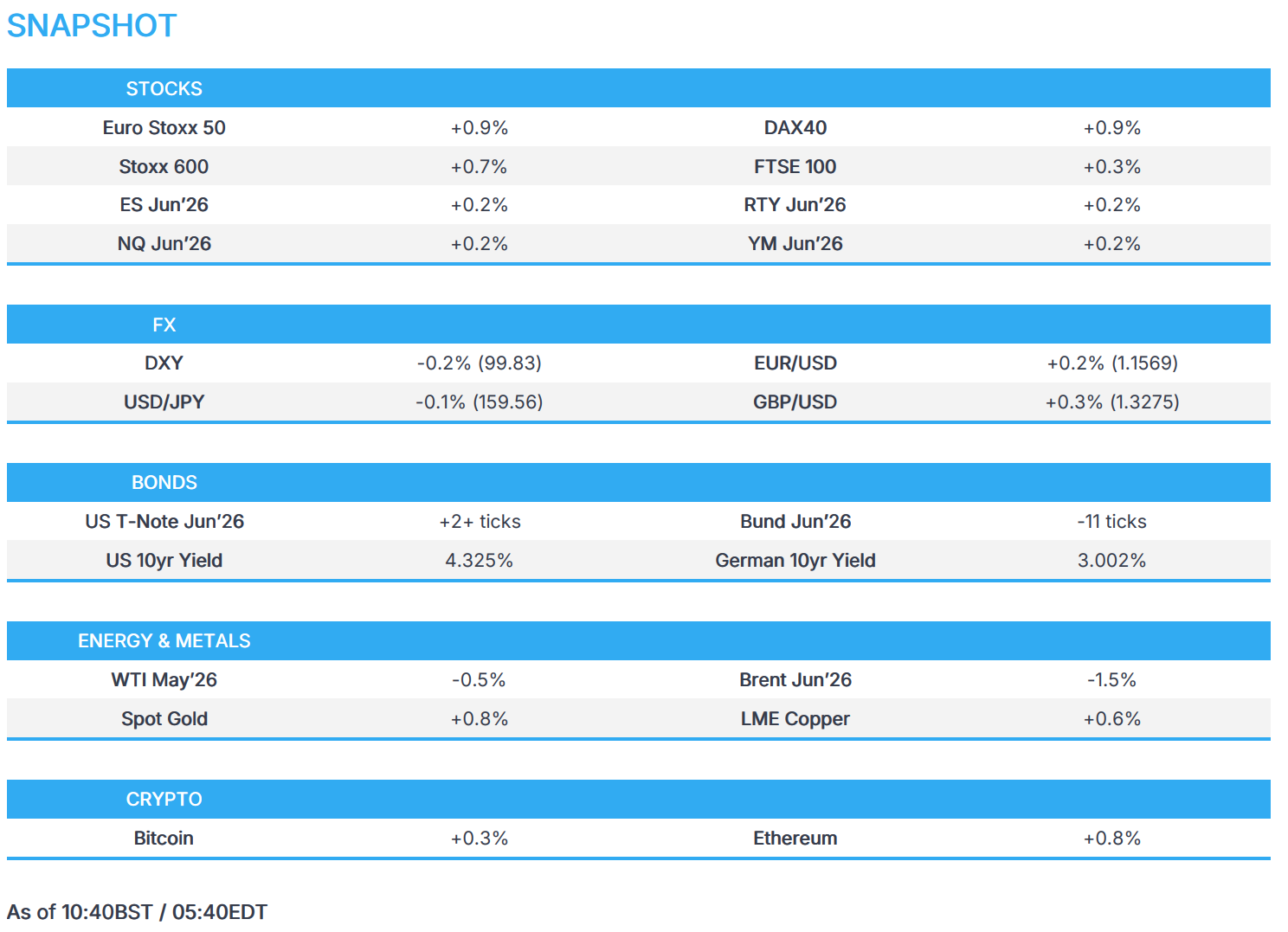

- Crude futures reverse earlier gains amid some positive noise ahead of Iran deadline.

- European bourses gain, UMG NA surges on PSH LN bid; US equity futures flat.

- USD returns below the 100.00 handle on US/Iran optimism.

- Fixed benchmarks higher as energy continues to dictate price action.

- Looking ahead, highlights include US ADP Employment Change Weekly, Durable Goods (Feb), RCM/TIPP Economic Optimism Index (Apr), Atlanta Fed GDP, President Trump's Iran deadline, EIA STEO, Speakers including Fed's Williams, Goolsbee & Jefferson, Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.7%) re-open from the 4-day Easter closure with mild gains, as traders countdown to Trump's Iran deadline at 20:00EDT/01:00BST. France's CAC 40 outperforms its peers, while the FTSE 100 underperforms. Worth noting that European indices opened mixed, but then moved higher, without a clear driver. Some may point to reports via a Pakistani journalist which suggested that a "framework of understanding for ceasefire" between US and Iran is “closer than ever”.

- European sectors are broadly in the green. Media is the clear outperformer, driven by gains in UMG (+12.2%) after Pershing Square announced a EUR 9.4bln bid to take over the media company. Technology sits at the bottom of the pile. Despite the majority of the sector components in the green, ASML (-2.3%) is weighing on the sector. This comes following a group of US politicians proposing a law to impose further export restrictions on computer chipmaking equipment to China.

- US equity futures trades either side of the unchanged mark, ahead of the Iran deadline. ES futures closed Monday's session beyond the downward trendline and has found support at the 20-SMA. Further upside could be supported if bond volatility continues to pullback and the VIX remains stable around the 25 mark. However, any significant upside will less likely be seen before the deadline passes.

- Samsung announced prelim. Q1 operating profit of KRW 57.2tln (exp. 40.6tln), and Q1 revenue of KRW 133tln (exp. 119.2tln). Prelim Q1 operating profit was up more than eightfold Y/Y, while revenue rose 68% Y/Y, driven by strong AI infrastructure demand, tight memory chip supply and higher chip prices.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX markets saw a sharp risk-on move in the European morning, with no specific headline, but several outlets reporting optimism in US/Iran negotiations ahead of Tuesday's deadline. DXY fell as much as 0.2% from 100.04 to a trough of 99.77, and high-beta FX was helped against the weaker buck, with Aussie the outperformer and Sterling also performing notably well.

- Some participants flagged an Axios article six hours before the move, which quoted a US official, "If the president sees a deal is coming together, he'll probably hold off..." it is unclear whether this led to the reaction, though other reports following this initial move have added to the constructive risk environment, "mediators are close to reaching an agreement" on a "framework of understanding for ceasefire", according to Pakistani reporter Anas Mallick.

- Elsewhere, EUR and GBP were unreactive to mixed European Final PMIs. To recap, the EZ wide composite and services were revised a touch higher while the UK's were revised lower.

- The session ahead sees US ADP Employment Change Weekly, US Durable Goods RCM/TIPP Economic Optimism Index (Apr), Atlanta Fed GDP and President Trump's Iran deadline. Fed speak is expected from Fed's Williams (13:30 BST), Goolsbee (17:35 BST) and Jefferson (22:50 BST). Full primer on the Newsquawk headline feed.

FIXED INCOME

- Initial bearish bias across the fixed income was facilitated by stronger energy prices, as the geopolitical environment remains exceptionally turbulent and as traders count down their clocks to President Trump’s 20:00EDT Iran deadline. However, in recent trade the crude complex took a tumble – but lacked a clear driver. Some market participants pointed towards an Axios piece from overnight, which reported that Trump may hold off from strikes on Iran if he sees a “deal coming together”. Markets also appear to be digesting some relatively positive mood from the Pakistani side, with a couple analysts suggesting a breakthrough could be close; whilst another suggested that a “framework of understanding” for a ceasefire is close. The pressure in energy prices therefore helped to boost fixed benchmarks to session highs.

- USTs were initially lower and were holding near troughs throughout the early portion of the morning, before then surging alongside the pressure in the crude complex. Currently holding at the upper end of a 110-21+ to 110-29+ range. On the data front, weekly ADP jobs figures, durable goods orders for February. On today’s speakers’ slate, Fed's Williams (voter) will speak on Bloomberg TV; Fed’s Goolsbee (2027 voter, dovish) will speak on the outlook for policy and the economy; Fed’s Vice Chair Jefferson (voter, dovish) will speak on the economic outlook and the labour market.

- Bunds followed the above, and currently holding at the upper end of a 125.31-125.73 range – though still remains incrementally in the red. Geopols aside, German benchmarks have had a number of European PMI Final metrics to digest; Spain topped expectations, Italy missed whilst the EZ-wide figure was revised incrementally higher. Interesting commentary from within the German release suggested that, “the lack of pricing power in the service sector is important from a monetary policy perspective, as it limits the amount of upward pressure on core inflation, a measure that the ECB will be closely watching when considering interest rate increases.”

- Gilts are currently flat. As above, initially weighed by stronger energy prices, but UK paper then soared to highs as energy prices dipped. Currently towards the upper end of a 88.23-88.72 range. UK PMI Finals were revised lower, with analysts citing slower output growth as a result of the war in the Middle East. It also highlighted increasing risks to “stagflation”, and increasing costs pressures.

- Germany sells EUR 1.046bln vs exp. EUR 1.5bln 2.50% 2035 and 0.00% 2050 Green Bund.

- Japan sold JPY 450.4bln 30-yr JGBs; b/c 3.12x (prev. 3.66x), and average yield 3.697% (prev. 3.398%).

- Poland is to sell 5-, 10- and 30-year USD-denominated noted via syndicate.

- Brazil is to sell EUR-denominated bonds.

COMMODITIES

- Crude futures gained at the start of the APAC session and held onto gains as European traders stepped in as US President Trump's 20:00EDT deadline approaches. If Iran does not agree to a ceasefire and reopen the Strait of Hormuz, he said the US will decimate Iran's bridges and didn't rule out striking power plants. However, Trump did also state that he thinks talks are going well and that Iran has "an active and willing participant on the other side." Further reporting throughout the European morning indicates that an agreement could be near, with Pakistani reporter Mallick suggesting that the interlocutors are 'closer than ever for an agreement' to get a "framework of understanding for ceasefire" between the US and Iran.

- WTI and Brent topped at USD 116.56/bbl and USD 111.80/bbl, respectively, before sinking – a move which lacked a clear driver. However, the move appeared to follow the aforementioned reports from the Pakistani reporter. At the time of writing, WTI May'26 has returned below USD 113/bbl while Brent Jun'26 oscillates on either side of USD 110/bbl.

- Spot gold trades relatively contained within a USD 4617-4691/oz range. Upticks have picked up pace in recent trade as the USD softens amid downside in energy prices. However, the 20-SMA at USD 4,732/oz and last week's high of USD 4,800/oz remain as near-term resistance levels. To add, China added gold to its reserves for a 17th consecutive month, highlighting that demand for the yellow metal is still high. However, UBS lowered its end-June forecast to USD 5,200/oz due to softer investor demand.

- 3M LME copper is rangebound, oscillating in a USD 12.37k-12.46k/t range. This comes as participants remain cautious as the Trump deadline looms.

- Hungary to agree to buy oil from US at Orban-Vance meeting, Bloomberg reported. Hungary’s Mol will agree to purchase 500,000 tons for approximately USD 500mln.

- Kazakhstan's Energy Ministry said the oil shipments via CPC pipeline is stable, IFX reported.

- IRGC's public relations channel reported of "explosion and extensive damage to the Al-Jubeil industrial area".

- Attacks reportedly hit Saudi Aramco's petrochemical plant in Saudi Arabia, AFP reported citing sources.

- China has provided Iran with a financial lifeline during the past half decade by purchasing most of its oil, according to WSJ.

- Tanker explosion near the Bridge of Americas in Panama City caused a massive fire.

- Japan's Industry Minister Akazawa said crude oil procurement is progressing.

- China gold reserves at end-March (USD) 342.76bln (prev. 387.59bln).

- UBS lowers end-June gold forecast to USD 5,200/oz, amid softer investor demand amid elevated volatility.

- Goldman Sachs analyst raises 2026 copper price forecast to USD 12,650/ton from USD 11,400/ton and expects copper prices to remain volatile as the market continues to assess impacts of the events in the Middle East on economic growth.

NOTABLE EUROPEAN DATA RECAP

- UK S&P Global Services PMI Final (Mar) 50.5 vs. Exp. 51.2 (Prev. 53.9). "Stagflation risks appear to have increased, with the final Services PMI data signalling slower growth and higher cost pressures than the earlier 'flash' estimates based on data compiled up to 20th March."

- UK S&P Global Composite PMI Final (Mar) 50.3 vs. Exp. 51 (Prev. 53.7).

- EU S&P Global Composite PMI Final (Mar) 50.7 vs. Exp. 50.5 (Prev. 51.9). "The near-stalling of growth in March drags the PMI’s signal for first quarter GDP growth down to 0.2%. More worrying is that there are clear risks of the economy contracting in the second quarter unless there is a swift resolution to the conflict."

- EU S&P Global Services PMI Final (Mar) 50.2 vs. Exp. 50.1 (Prev. 51.9).

- German S&P Global Services PMI Final (Mar) 50.9 vs. Exp. 51.2 (Prev. 53.5).

- German S&P Global Composite PMI Final (Mar) 51.9 vs. Exp. 51.9 (Prev. 53.2).

- French S&P Global Services PMI Final (Mar) 48.8 vs. Exp. 48.3 (Prev. 49.6).

- French S&P Global Composite PMI Final (Mar) 48.8 vs. Exp. 48.3 (Prev. 49.9).

- Italian S&P Global Services PMI (Mar) 48.8 vs. Exp. 50.8 (Prev. 52.3).

- Italian S&P Global Composite PMI (Mar) 49.2 (Prev. 52.1).

- Spanish S&P Global Composite PMI (Mar) 52.4 (Prev. 51.5).

- Spanish S&P Global Services PMI (Mar) 53.3 vs. Exp. 50.5 (Prev. 51.9).

- Swedish CPIF MoM Prel (Mar) M/M -0.6% vs Exp. 0.0% (Prev. 0.6%).

- Swedish CPIF YoY Prel (Mar) Y/Y 1.6% (Prev. 1.7%).

- Swedish Inflation Rate MoM Prel (Mar) M/M -0.6% (Prev. 0.6%).

- Swedish Inflation Rate YoY Prel (Mar) Y/Y 0.6% (Prev. 0.5%).

CENTRAL BANKS

- ECB's Wunsch said he is open to an interest rate rise at the April meeting; a lasting crisis would warrant a series of rate rises.

- ECB's Radev said the ECB must be ready to act if inflation persists, sees a rising likelihood of adverse scenario but too early to say if April rate hike is needed. Inflation expectations at risk of rising too quickly.

NOTABLE US HEADLINES

- Republicans are reportedly weighing how broadly to structure a party-line bill to fund President Trump’s immigration enforcement, with some senators seeking multi-year DHS funding and others favouring a narrower ICE and CBP measure, Semafor reports.

GEOPOLITICS

MIDDLE EAST

- Pakistani reporter Anas Mallick suggests that, "to my understanding, the interlocutors (Pakistan, Turkiye and Egypt) are 'closer than ever for an agreement' to get a "framework of understanding for ceasefire" between US and Iran".

- Some geopolitical analysts say signals from Pakistan suggest a possible breakthrough in the coming hours, with Egypt, Turkey, Saudi Arabia and reportedly Beijing involved. said that a ceasefire could be near, but the situation remains early and fragile, so caution is warranted.

- Pakistan in last-minute efforts, along with Turkey and Egypt, to convince Iran to agree to the outline proposed by Pakistan, according to I24's Stein.

- Five friendly countries leaders' and eight intelligence agencies have reached out to Iran seeking to open a path for a ceasefire, Fars News reported.

- Israeli Source tells N12 news "The next 24 hours are the most decisive in the war, if it were up to political leadership in Iran, there would have been a ceasefire long ago, there is doubt about their control", N12's Segal reported.

- Iran's Spokesperson of the National Security Commission of the Parliament said "we are making special arrangements for the Strait of Hormuz", via Tasnim.

- Spokesman of Iran's National Security and Foreign Policy Committee of Parliament said oil exports are going on as usual, and with even more capacity than before, IRIB reported.

- Iran atomic agency said heavy bombs won't halt nuclear tech progress.

- China has provided Iran with a financial lifeline during the past half decade by purchasing most of its oil, according to WSJ.

- Saudi Arabia, UAE and Israel report Iranian drone and missile attacks, according to CBS.

- Israel announces a new wave of strikes on Iran and issues incoming missile alert.

- Iran launches new batch of missiles towards southern Israel.

- Israeli military said it completed airstrike wave aiming to damage Iranian terror regime infrastructure in Tehran and additional areas across Iran.

- US House Democrat Ansari intends to introduce articles of impeachment against Secretary of War Hegseth, cites Iran war and war crimes as grounds for Hegseth impeachment, according to NBC.

- Japanese PM Takaichi said in parliament said in Parliament, want to take next step in talks with Iran and is strongly urging Iran to allow Hormuz safe passage, while she is seeking phone talks with the presidents of US and Iran.

- Iranian Parliament Speaker Ghalibaf's adviser Mohammadi said it is Trump who has about 20 hours to either surrender to Iran or his allies will return to the Stone Age, while he added that they will not back down.

- Iran said non-hostile countries can coordinate access to the Strait of Hormuz, according to Press TV.

- US Vice President J.D. Vance is on standby for Iran negotiations, according to POLITICO. "The negotiations are led by Steve Witkoff and Jared Kushner but Vance could be tagged in if there is a direct meeting with Iranian officials.".

- Iran's top joint military command said Trump's threats are 'delusional' and his threat have no effect on operations against US and Israel.

- US data centres of Amazon (AMZN), Microsoft (MSFT), Oracle (ORCL), and Equinix (EQIX) in the UAE are now identified as potential targets for Iran's counter response in the region.

- Iranian securities exchange chief outlines conditions needed to reopen the Iranian capital markets: said outcomes could include a ceasefire with a formal agreement and full reopening, or a ceasefire without agreement and a gradual reopening.

- Explosions reported in eastern regions of Saudi Arabia and alarms sounding in Bahrain, Tasnim reported.

- Israeli reporter Stein said "Unexpectedly: the press conference planned for today with Defence Minister Hegseth and US Chief of Staff was cancelled".

- Fars news citing an informed source said "Trump is clearly looking for a meeting and an agreement. The American proposal includes the removal of "Witkoff" due to his closeness to Netanyahu's circle and negotiations with "Vance" to build a serious path. In the end, this source noted: Americans believe that fuel prices will increase explosively from next week and are not willing to accept this risk.

- The Iranian Ambassador to Pakistan said Pakistan's positive and productive attempt to step the war is approaching a critical and sensitive stage.

- Iranian outlets report that Yazd and Shiraz were shaken by blasts.

- Large barrage of missiles were reportedly headed for Bahrain, with air raid sirens and alerts in multiple areas.

- Drone strike reportedly hit US Victoria base in Baghdad, according to Iraqi sources cited by Fars.

- Missiles hit Saudi Arabia's Jubail which is largest industrial hub in the Middle East where large petrochemical and energy facilities are located.

- IRGC Aerospace Force Commander said they targeted the oil refinery, power plants, ports, and railway lines in Haifa Bay, and no interception of our missiles was recorded, Al Jazeera reported.

RUSSIA-UKRAINE

- Russia's Yamal LNG ships first cargo to China since November, LSEG data shows.

- Russia's Ministry of Defence reported that air defence forces have downed 45 Ukrainian drones over Russian regions overnight.

CRYPTO

- Bitcoin is slightly lower and trades just shy of the USD 69k mark.

APAC TRADE

- APAC stocks traded cautiously following the positive lead from the US and with all focus remaining on geopolitics heading into US President Trump's Tuesday evening deadline for Iran to open up the Strait of Hormuz or face the US destroying its power plants and bridges, although President Trump had also previously stated that he thinks talks are going well with Iran and they would like to be able to make a deal.

- ASX 200 rallied with tech and miners leading the upside and with almost all sectors in the green aside from industrials and consumer staples.

- Nikkei 225 failed to sustain its initial advances with the index pressured amid headwinds from higher oil prices and following disappointing Household Spending data.

- KOSPI surged at the open with strong gains in Samsung Electronics after its preliminary results topped forecasts and showed around an eight-fold jump in Q1 operating profit, although most of the advances were then pared as shares in the index heavyweight also pulled back.

- Shanghai Comp lacked conviction on return from the long weekend, with upside limited after another meek PBoC liquidity operation and with the Stock Connect still closed as Hong Kong markets remained shut.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama said won't comment on JGB yield levels and will refrain from commenting on levels in the markets, adds impact of Middle East and oil prices on the market is high.

- Chinese President Xi called for new energy system as war on Iran rocks global economy and said China needs to accelerate planning and construction of a new energy system to ensure the country’s energy security.

- South Korean FX Chief said are to deploy bold measures in the FX market, if needed.

- South Korea policy chief Kim said the chip industry secures four month's worth of helium and it is premature to discuss a second extra budget.

- Morgan Stanley cuts its China 2026 GDP growth forecast to 4.7% due to oil shock.

NOTABLE APAC DATA RECAP

- Australian S&P Global Services PMI Final (Mar) 46.3 vs. Exp. 46.6 (Prev. 52.8).

- Australian S&P Global Composite PMI Final (Mar) 46.60 vs. Exp. 47 (Prev. 52.4).

- Chinese Foreign Exchange Reserves (Mar) 3.342T vs. Exp. 3.40T (Prev. 3.428T).

- Japanese Coincident Index Prel (Feb) 116.3 (Prev. 117.9).

- Japanese Leading Economic Index Prel (Feb) 112.4 (Prev. 112.1).

- Japanese Foreign Exchange Reserves (Mar) 1374.7B (Prev. 1410.7B).

- Japanese Household Spending YoY (Feb) Y/Y -1.7% vs. Exp. -0.7% (Prev. -1%).

- Japanese Household Spending MoM (Feb) M/M 1.5% vs. Exp. 2.6% (Prev. -2.5%).

Loading...