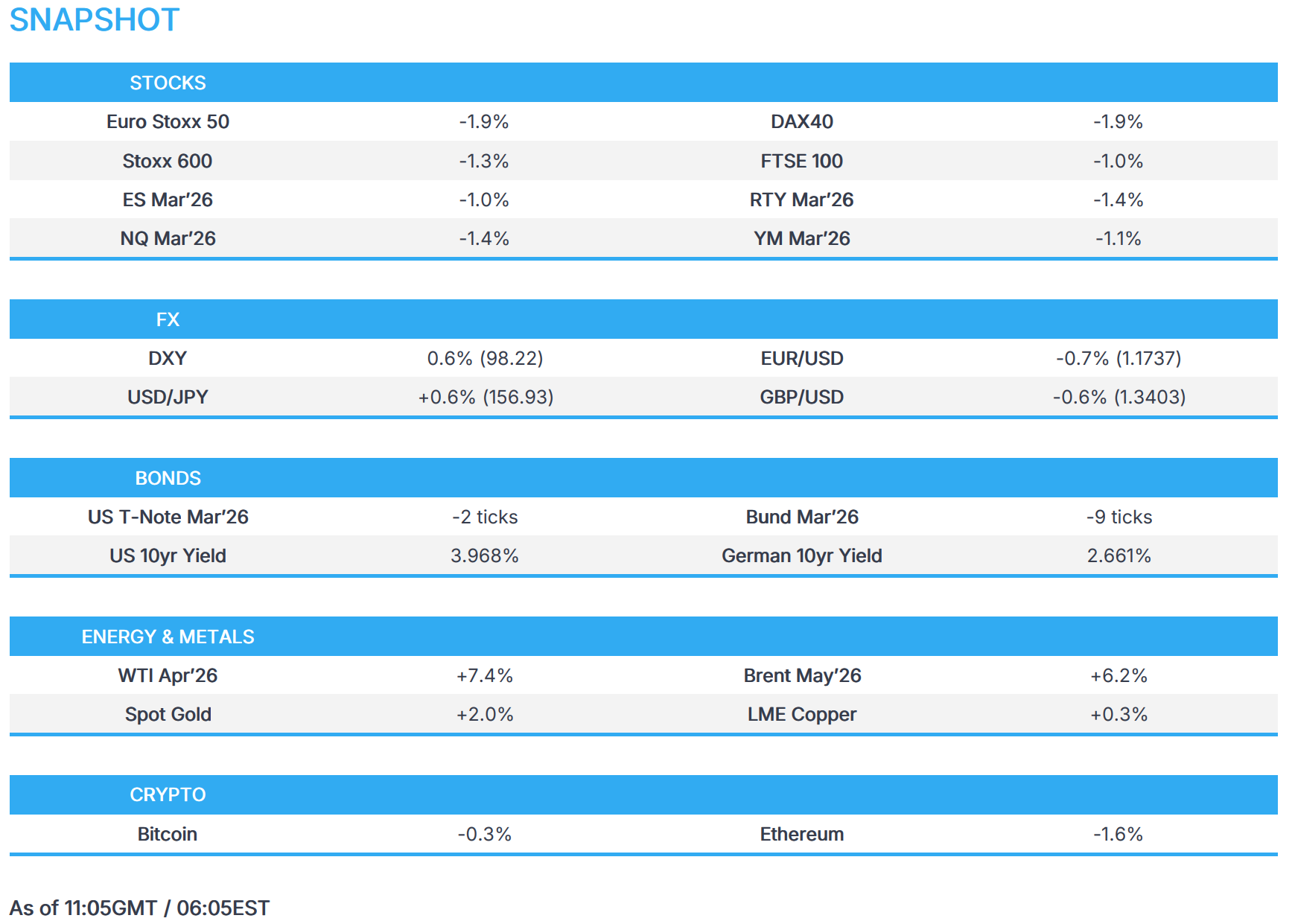

Risk off sentiment sparked by US-Israel-Iran war; NQ -1.4%, Brent +6% - Newsquawk US Market Open

- US and Israel launched a large-scale joint military operation against Iran on Saturday, 28th February; Iranian state television officially confirmed the death of Supreme Leader Ayatollah Ali Khamenei.

- Iran launched immediate retaliatory missile and drone attacks against Israel, and multiple US military installations across the Gulf and multiple Gulf states, including the UAE, Qatar, Kuwait and Bahrain. Global equities hit on risk tone, energy and defence names benefited, while airlines were significantly affected.

- Iran’s IRGC declared the Strait of Hormuz closed to international navigation until further notice; IRGC also announced on Sunday that they hit 3 US and UK oil tankers with missiles in the Gulf and Strait of Hormuz.

- DXY surging amid geopolitics; G10s pressured across the board.

- USTs initially gapped higher, before waning as traders assess the inflationary impacts of the US/Israel-Iran war.

- Crude surges on weekend geopolitics but capped by potential global economic impact; Precious metals see haven appeal.

- Looking ahead, highlights include US Final Manufacturing PMI (Feb), US ISM Manufacturing PMI (Feb), Japanese Unemployment Rate (Jan), Speakers including BoE’s Taylor & Ramsden, BoC’s Kozicki & Macklem, Earnings from Riot Platforms & ASM International.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US and Israel launched a large-scale joint military operation against Iran on Saturday, 28th February, with explosions reported across Tehran shortly after 09:30 local time (06:00 GMT / 01:00 EST), and additional strikes were confirmed in Isfahan, Qom, Karaj and Kermanshah, while the Israeli military confirmed it launched an additional wave of strikes on Sunday morning, targeting Iran's ballistic missile and aerial defence systems.

- Iran launched immediate retaliatory missile and drone attacks against Israel, and multiple US military installations across the Gulf and multiple Gulf states, including the UAE, Qatar, Kuwait and Bahrain. Iranian state television officially confirmed the death of Supreme Leader Ayatollah Ali Khamenei following Saturday’s US–Israeli “decapitation strike” on his secure residence and office compound in central Tehran. Furthermore, IRGC declared the Strait of Hormuz closed to international navigation until further notice, while major tanker operators and global trading houses have halted crude, fuel and LNG shipments through the waterway. IRGC also announced on Sunday that they hit 3 US and UK oil tankers with missiles in the Gulf and Strait of Hormuz.

- Iran launched a fresh wave of missile and drone attacks on Sunday, while Iranian sources stated that 27 US bases across the region were targeted, along with Israel’s military headquarters in Tel Aviv. It was also reported that Iran fired missiles towards British military bases in Cyprus and that rockets landed near British troops in Bahrain.

- Israeli Air Force launched a new wave of attacks on Iranian regime targets in Tehran early on Monday and bombarded Hezbollah strongholds in the southern suburb of Beirut, while Hezbollah fired rockets towards Northern Israel for the first time since the ceasefire agreement, and it was also reported that Hezbollah parliamentary bloc head Mohammed Raad was killed in an Israeli raid.

- US President Trump said the US military launched “major combat operations” in Iran with the objective of defending the American people by eliminating imminent threats from the Iranian regime. Trump said people in Iran should stay at home and that bombs will be dropping everywhere, while he called for Iranians to take over the government.

- US President Trump said that Iran’s Supreme Leader Khamenei had died, and he was informed that they destroyed and sank nine Iranian ships, as well as largely destroyed the naval headquarters. Trump separately commented that the military operations are ahead of schedule and that 48 leaders were killed in strikes on Iran, while he also stated that Iranian leaders want to talk and he has agreed to talk, but couldn’t say if it would happen soon, according to Atlantic Magazine and Daily Mail. Furthermore, Trump suggested that the fighting with Iran could go on for four weeks, while he also stated on Sunday that they have hit hundreds of targets in Iran under ‘Operation Epic Fury’ and combat operations will continue in full force until all objectives are complete.

- US President Trump said he could lift sanctions on Iran if its next leader proves pragmatic and that he had three very good choices for Iran's next leader, although he also commented that the people he considered for Iran's next leader died in the air attacks.

- US Secretary of War Hegseth is to hold a press conference at 08:00EST/13:00GMT. White House separately announced that US Secretary of State Rubio and Secretary of War Hegseth are to brief a full Congress on Tuesday.

- US officials told Al Jazeera that the strikes on Iran are focused on military targets and will be far more extensive than the US strikes last June, while the US reported that three US service members died and five were seriously wounded amid the operations against Iran.

- Israeli PM Netanyahu said the US and Israel operations are to remove the existential threat from the Iranian regime, while Israeli officials characterised the action as a “pre-emptive strike” to prevent Iran from obtaining nuclear weapons. Israel ordered the shutdown of some natural gas fields as a security measure following the US-Israel strike on Iran, while it pre-approved a USD 2.9bln supplement to the defence budget to fund the war with Iran.

- Other incremental updates can be seen below.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -1.3%) are entirely in the red due to instability in the Middle East. In brief, the US-Israeli war with Iran has entered its third day, with all sides conducting large-scale airstrikes. Airspaces have been closed, oil refineries and tankers have been hit, and threats of further attacks continue (see "Iran Situation Report - Day 3" on the headline feed for more detailed analysis). The FTSE 100 (-1.0%) is being supported, albeit posting slight losses, helped by the major oil names (BP +1.8%, Shell +2.2%) as oil prices rise. The banking-heavy IBEX 35 (-2.2%) and FTSE MIB (-1.7%) have been hit the hardest on the prospect of increased war-risk claims.

- From a sectoral perspective, Energy leads the pile, given the strength in underlying oil prices; Defence names are also stronger across the board, given the increased tensions; Rheinmetall +1.3%, BAE +5.2%, Leonardo +4.7%. One other key space of the market that has benefited is shipping names such as Maersk (+4.5%), Kuehne+Nagel (+0.4%), due to higher freight rates.

- US equity futures (ES -1.0%, NQ -1.4%, RTY -1.4%) have followed the global risk tone; in recent trade, contracts are attempting to rebound off worst levels, though remain significantly in the red.

- ASML (ASML NA) is planning to expand into advanced packaging for AI chips, and is exploring larger chip sizes and scanner systems

- Citi upgrades UK equities on Middle East conflict due to commodity and aerospace exposure.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY gains but trades off best levels as participants flock to the USD in light of the weekend geopolitics, with the initial US-Israel strike on Iran expanding throughout the Gulf and Middle East. Analysts at ING highlight three main channels that keep the USD in demand: 1) the US is less dependent on imported energy vs Europe and most of Asia. Higher energy hurts importers (EUR, JPY), whilst European Nat Gas opened up around 25%. 2) Markets are scaling back expectations for rate cuts from the Fed, with higher energy also proving headwinds for disinflation. A “bearish flattening” in the US yield curve (short-end yields rising) supports the dollar. 3) Higher energy and reduced Fed easing expectations could reverse capital flows into EM, which would further support the USD. DXY is around the middle of a 97.768-98.566 range after hitting highs around an hour after the European cash open.

- GBP is the worst performer amid the RAF base in Cyprus being struck by an Iranian drone. The UK has confirmed it is not participating in offensive operations but is permitting defensive use of bases. GBP/USD slipped from a 1.3456 peak to a 1.3314 trough.

- EUR has been hit by the aforementioned surge in energy prices, with EUR/USD slumping from near 1.1800 to lows of 1.1698 before trimming losses at the time of writing. ING suggests EUR/USD could slide back toward the 1.1575–1.1600 area if escalation continues.

- JPY and CHF are softer despite their haven appeals, with the USD sought after given its reduced dependency on energy imports. USD/JPY is +0.6% in a 156.04-157.25 range. USD/CHF trades +0.5% in a 0.7668-0.7742 parameter.

- Antipodeans also post losses amid their high-beta properties and sensitivity to risk. AUD/USD resides in a 0.7032-0.7117 range and NZD/USD in a 0.5928-0.5995 band.

FIXED INCOME

- USTs opened higher, then jumped to a session high of 114-12, before quickly paring much of the upside as the APAC session progressed. The narrative quickly shifted from “haven” related upside, to traders assessing and then pricing in the inflationary impacts of the closure of the Strait of Hormuz. This impacts both: a) energy prices, b) prices of goods which are subject to longer trading routes, as shipping giants avoid the chokepoint. From a central banking perspective, inflationary pressures could see policymakers shift hawkishly – though, Danske Bank suggested that the Fed is unlikely to trigger speculations of near-term policy shifts following the rise in energy prices. Geopols aside, the US ISM manufacturing survey for February is expected to be little changed at 52.3 (from 52.6). The Atlanta Fed will update its GDPnow tracking estimate, which is currently modelling growth of 3.0% in Q1. Later in the session, the Fed will publish its Senior Loan Officer Survey. USTs currently trade around 113-23 within a 113-22+ to 114-12 range.

- Bunds moving in-line with peers and currently trading around 130.05 to 130.53 range. Price action is similar to the above, initial haven flows buoyed German paper, before markets began factoring in inflationary impacts. Danske expect short-term widening Schatz spreads, but the bank highlights that safe-haven inflows are often short-lived and modest.

- Gilts are underperforming, and trades lower by around 30 ticks within a 93.31 to 93.57 range. Underperformance, which perhaps can be explained given that the region is a net-importer of oil, and as such has long been considered highly vulnerable to energy volatility. Elsewhere, ahead of this week’s UK Spring Statement, Chancellor Reeves has received a GBP 22bln windfall as tax receipts outperformed forecasts, according to Bloomberg; analysis of official data showed stronger than expected self-assessed income tax and sales levy revenues, alongside lower debt-interest spending, contributing to the improvement in the public finances.

COMMODITIES

- Crude futures surged at the reopen in reaction to the geopolitical escalation in the Middle East owing to the strikes against Iran and the killing of its Supreme Leader, as well as its retaliation against the US and several neighbours in the Gulf, while it also announced the closure of the Strait of Hormuz. (Newsquawk analysis available on the feed). However, prices waned off their opening highs as Brent returned to beneath the USD 80/bbl and WTI briefly retreated to below 70/bbl levels before recovering, with Brent May'26 currently within USD 74.54-80.82/bbl (+6.2% at the time of writing) and WTI Apr'26 within USD 71.88-75.33/bbl (+7.3% at the time of writing).

- Spot gold rallied on a haven bid amid the weekend geopolitics (Newsquawk analysis available on the feed) but then mildly pulled back after stalling just shy of the USD 5,400/oz level in APAC trade, before mounting the level to a USD 5,419.15/oz peak. Spot silver hit a USD 92.42/oz peak from a USD 92.02/oz trough.

- Copper futures ultimately weakened overnight but trades flat in European hours, in choppy trade amid the mostly negative risk appetite in the region, with all focus on geopolitics. 3M LME copper resides in a narrow USD 13,249.60-13,444/t range at the time of writing.

- OPEC+ is to resume oil output increases, in which it will add 206k bpd in April. It had been previously reported over the weekend that OPEC+ could consider a larger production hike of as much as 441k bpd following the strike on Iran.

- IRGC declared the Strait of Hormuz closed to international navigation until further notice, while major tanker operators and global trading houses have halted crude, fuel and LNG shipments through the waterway. Furthermore, analysts warned of a potential Brent crude move above USD 100/bbl if the blockade persists.

- Oil facilities of regional countries are not Iran's targets, via Mehr.

- Chevron (CVX) said it was instructed by Israel's Ministry of Energy to temporarily shut-in production at the Leviathan gas production platform.

- Middle East crude benchmark Dubai's premium rises to around USD 5.90/bbl, the highest since 2022, sources say.

- IAEA Director General Grossi said we have no indication that any of Iran's nuclear installations have been damaged or hit. The situation is very concerning, cannot rule out a possible radiological release with serious consequences. No elevation of radiation levels above the usual background levels have been detected so far in countries neighbouring Iran.

- Saudi Energy Ministry says limited fire at Aramco's Ras Tanura refinery, no impact on supplies.

- The limited fire at Ras Tanura refinery was due to shrapnel falling during an interception operation, Al Hadath reported.

- Saudi Arabia's Ras Tanura refinery shuts down after a drone strike, Bloomberg reported.

- Iran's Ahwaz oil refinery has reportedly been struck in a suspected US airstrike.

- Gulf Keystone temporarily shuts in output operations in Shaikan field.

- The fire at Saudi Aramco's oil depot is under control, Sky News Arabia reported.

- Goldman Sachs said the Hormuz disruption could add USD 18/bbl of oil risk premium, and it flags natgas upside and defensive tilt.

- JPMorgan said that a spike in oil prices will result in a revision of near-term inflation forecasts.

- Kpler AIS tracking shows tanker queues building inside the Middle East Gulf and east of the strait, while eastbound Hormuz exits collapsed to just three observed laden ships on 1 March across crude and products, according to Kpler's Bakr.

- S&P Global Platts suspends bids and offers for Middle East oil products requiring Strait of Hormuz transit.

- Goldman Sachs estimates an USD 18/bbl real-time risk premium in crude oil prices and sees impact moderates to + USD 4/bbl if only 50% of Strait of Hormuz flows are impacted for one month. Sees significant upside to TTF/JKM prices from a potential sustained disruption of LNG.

- China's UBS SDIC silver futures fund said trading is suspended from market open on March 3rd until 10:30am the same day.

TRADE/TARIFFS

- India's Foreign Ministry announces that they have signed an uranium supply agreement with Canada.

- Singapore and South Korea are in talks to upgrade a free trade agreement.

NOTABLE EUROPEAN DATA RECAP

- UK S&P Global Manufacturing PMI Final (Feb) 51.7 vs. Exp. 52.0 (Prev. 52.0, Rev. From 51.8).

- EU HCOB Manufacturing PMI Final (Feb) 50.8 vs. Exp. 50.8 (Prev. 49.5).

- German HCOB Manufacturing PMI Final (Feb) 50.9 vs. Exp. 50.7 (Prev. 49.1).

- French HCOB Manufacturing PMI Final (Feb) 50.1 vs. Exp. 49.9 (Prev. 51.2).

- Italian HCOB Manufacturing PMI (Feb) 50.6 vs. Exp. 49.5 (Prev. 48.1).

- Spanish HCOB Manufacturing PMI (Feb) 50.0 vs. Exp. 50.1 (Prev. 49.2).

- German Retail Sales YoY (Jan) Y/Y 1.2% (Prev. 1.5%).

- German Retail Sales MoM (Jan) M/M -0.9% vs. Exp. -0.2% (Prev. 0.1%).

- UK Nationwide Housing Prices MoM (Feb) M/M 0.3% vs. Exp. 0.3% (Prev. 0.3%).

- UK Nationwide Housing Prices YoY (Feb) Y/Y 1.0% vs. Exp. 0.7% (Prev. 1.0%, Rev. From 1%).

CENTRAL BANKS

- BoJ Deputy Governor Himino said to raise rates if economic outlook is met, adds the goal is to maintain price stability by avoiding excessive inflation and deflation, thereby supporting sustainable economic growth. said:Impact of rate hikes has been limited so far.

- SNB states that in view of the international situation, we are more prepared to intervene in the FX market.

- Swiss Sight Deposits (w/e Mar 1). Domestic Banks CHF 440.5bln (prev. 440.6bln), Total CHF 459.8bln (prev. 457.6bln).

NOTABLE US HEADLINES

- China Foreign Ministry said they are in communication with the US about exchanges between their leaders.

GEOPOLITICS

MIDDLE EAST

- Israeli military says it has begun additional strikes on Tehran.

- Qatar Defence Ministry says it intercepted two Iranian drones, which targeted energy facilties; one drone headed towards QatarEnergy's Raf Laffan facility

- "Israel army said there is no reason for Lebanon ground invasion for now", via Al Arabiya citing AFP.

- Israel's IDF said "We are discussing the option of carrying out a ground operation inside Lebanon", via Al Jazeera.

- Iran's ambassador to the IAEA said Israel and the US attacked Iranian nuclear facilities on Sunday.

- Iran's Larijani said they will not negotiate with the US.

- Iran's Secretary of the Supreme National Security Council Larijani said US President Trump has brought chaos to the region with "false whims" and is now worried of more casualties among US forces. Trump is sacrificing American soldiers for Israel's quest for power.

- Iran warns that those responsible for killing Supreme Leader Khamenei will face consequences.

- US President Trump said he could lift sanctions on Iran if its next leader proves pragmatic, according to New York Times. said:He had three very good choices for next Iran leader.

- US President Trump said the people he considered for Iran's next leader died in the air attacks, according to ABC News.

- US President Trump said Iran does not want to go quite far enough and it's too bad and are not happy with Iran negotiation.

- US Secretary of State Rubio designating Iran as state sponsor of wrongful detention; Iran must stop taking hostages; will consider other measures if Iran does not stop.

- US State Department said no American should travel to Iran for any reason and reiterate their call for Americans who are currently in Iran to leave immediately.

- Hezbollah reportedly fires rockets towards Northern Israel for the first time since the ceasefire agreement, according to Israel Broadcasting Corporation.

- Omani Foreign Minister said "The single most important achievement, I believe, is the agreement that Iran will never, ever have a nuclear material that will create a bomb...", according to CBS interviewing Albusaidi. "

RUSSIA-UKRAINE

- Ukraine President Zelensky says long war in Iran may impact air defence for Ukraine.

- Russia is said to consider a halt in peace talks unless Ukraine cedes land. Talks planned for the week ahead will be decisive on whether or not the sides can agree on terms to end the war, while Russia will likely walk away if Ukrainian President Zelensky fails to make the concession.

- A fuel terminal in Russia's Novorossiysk is on fire, according to local authorities.

CRYPTO

- Bitcoin finds resistance at USD 67,000 amid global risk-off tone.

APAC TRADE

- APAC stocks were mostly pressured as all focus centred on geopolitics following the US and Israeli strikes on Iran, which killed its Supreme Leader and dozens of officials, while Iran responded with retaliatory strikes against the US and allies, including several neighbours in the Gulf.

- ASX 200 was rangebound with weakness seen in tech, financial and airlines stocks as the latter got a double whammy from flight disruptions and higher fuel costs, while energy stocks benefitted from the surge in oil due to the Iran conflict.

- Nikkei 225 fell beneath the 58,000 level as exporters suffered from the worsening geopolitical climate and disruption in the Strait of Hormuz, which the IRGC shut.

- Hang Seng and Shanghai Comp were mixed with heavy losses in Hong Kong due to tech weakness, while the mainland shrugged off early jitters and climbed ahead of the annual 'two sessions' in Beijing, where top officials are set to unveil economic strategies.

Loading...